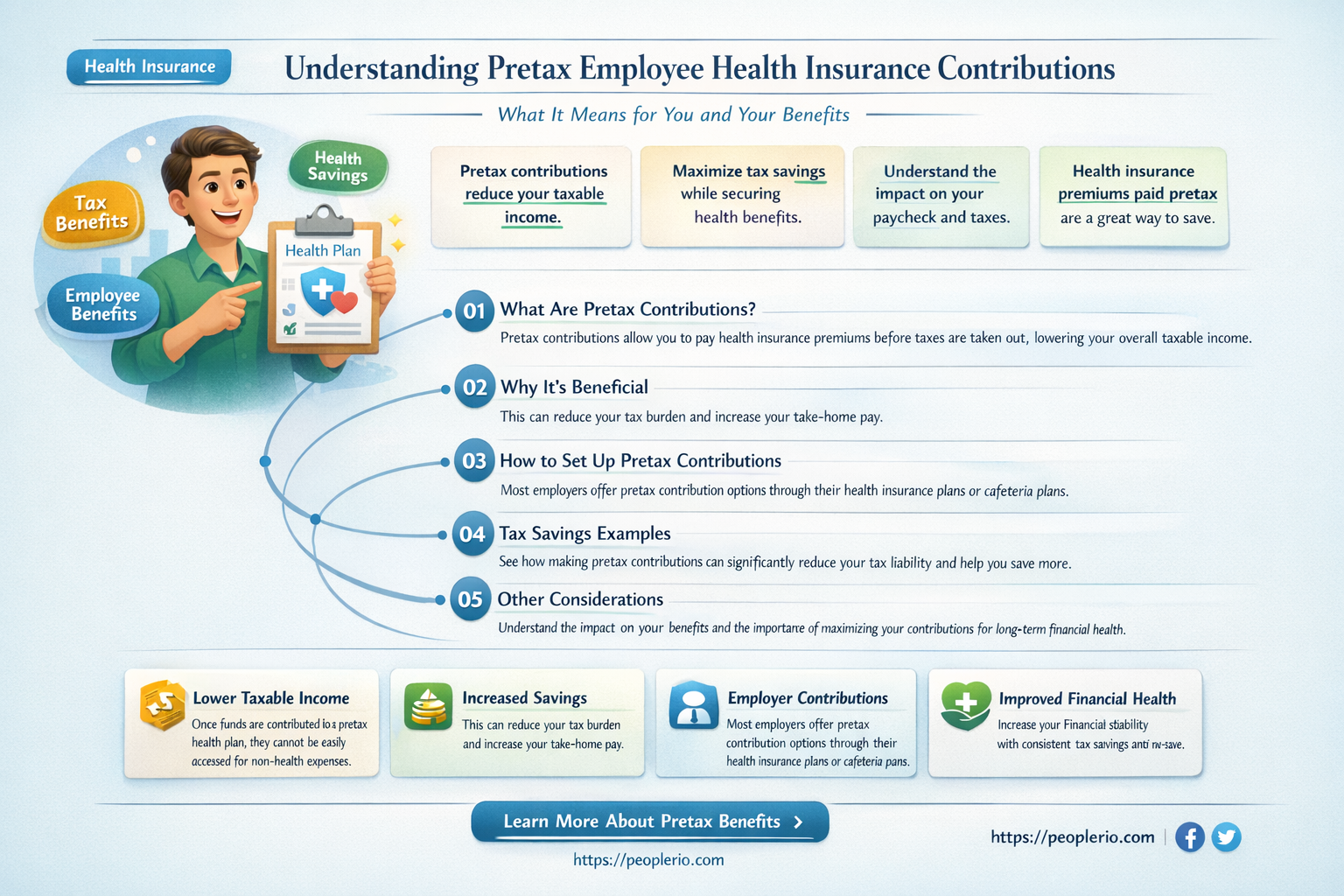

Employee contributions to health insurance are often made on a pretax basis, which means the money is deducted from an employee's paycheck before taxes are calculated. This can provide a significant tax advantage because it reduces the employee's taxable income, thereby lowering the amount of federal, state, and local taxes withheld. Additionally, pretax contributions can also reduce the employee's Social Security and Medicare taxes. Employers may also contribute to health insurance on a pretax basis, which can further reduce the overall tax burden for both the employer and the employee. Understanding how these pretax contributions work can help employees make informed decisions about their health insurance and tax planning.

| Characteristics | Values |

|---|---|

| Type of Contribution | Pretax |

| Contributor | Employee |

| Purpose | Health Insurance |

| Tax Treatment | Not taxable as income |

| Benefit | Reduces taxable income |

| Common in | Many employer-sponsored health plans |

| Alternatives | Post-tax contributions, employer-only contributions |

| Impact on Take-Home Pay | Increases take-home pay by reducing tax liability |

| Enrollment | Typically during open enrollment periods |

| Changes | Can be changed during qualifying life events or open enrollment |

Explore related products

What You'll Learn

- Definition of Pretax Contributions: Understand what pretax contributions mean in the context of health insurance

- Tax Benefits: Explore the tax advantages of making pretax contributions to health insurance

- Impact on Take-Home Pay: Analyze how pretax contributions affect an employee's net income

- Employer's Role: Discuss the employer's involvement and responsibilities regarding pretax health insurance contributions

- Common Misconceptions: Address and clarify any misunderstandings about pretax health insurance contributions

![]()

Definition of Pretax Contributions: Understand what pretax contributions mean in the context of health insurance

Pretax contributions refer to the amount of money an employee sets aside from their gross income to fund their health insurance premiums before taxes are deducted. This financial strategy is commonly used in employer-sponsored health insurance plans, where both the employer and employee share the cost of the premiums. The employee's portion is typically deducted from their paycheck on a pretax basis, meaning the deduction occurs before federal, state, and local taxes are calculated.

One of the primary benefits of pretax contributions is the tax advantage they provide. By deducting the health insurance premiums before taxes, employees can reduce their taxable income, which in turn lowers the amount of taxes they owe. This can result in significant savings, especially for individuals in higher tax brackets. For example, if an employee contributes $200 per month to their health insurance premiums on a pretax basis and they are in a 25% tax bracket, they would save $50 per month in taxes.

Pretax contributions are also advantageous for employers. By offering pretax deductions for health insurance premiums, employers can provide a more attractive benefits package to their employees without increasing their own costs. This is because the employer's contribution to the health insurance plan is also tax-deductible as a business expense. Additionally, pretax contributions can help employers comply with certain tax regulations, such as the Affordable Care Act (ACA), which requires employers to provide affordable health insurance options to their employees.

It is important to note that pretax contributions are subject to certain limits and regulations. For example, the IRS sets a maximum limit on the amount of pretax dollars that can be contributed to a health insurance plan each year. This limit is adjusted annually for inflation. Additionally, pretax contributions are only available for certain types of health insurance plans, such as those offered through an employer or a health insurance exchange. Individuals who purchase health insurance independently may not be eligible for pretax contributions.

In conclusion, pretax contributions are a valuable financial tool for both employees and employers in the context of health insurance. They provide a tax-efficient way to fund health insurance premiums, resulting in cost savings and a more attractive benefits package. However, it is essential to understand the limits and regulations surrounding pretax contributions to ensure compliance and maximize their benefits.

Decoding Employee Health Insurance Premiums: Taxable or Not?

You may want to see also

Explore related products

![]()

Tax Benefits: Explore the tax advantages of making pretax contributions to health insurance

Making pretax contributions to health insurance can offer significant tax benefits. When employees contribute to their health insurance premiums before taxes are deducted, they reduce their taxable income. This can lead to lower federal and state income taxes, as well as lower payroll taxes such as Social Security and Medicare. For example, if an employee contributes $200 per month to their health insurance, they could potentially save around $40 to $60 per month in taxes, depending on their tax bracket and the specific tax laws in their state.

One of the key advantages of pretax health insurance contributions is that they allow employees to pay for their health care expenses with pre-tax dollars. This can be particularly beneficial for individuals who have high medical expenses or who anticipate needing to use their health insurance frequently. By paying for these expenses with pre-tax dollars, employees can effectively reduce their overall health care costs.

Another important consideration is that pretax contributions can also impact an employee's eligibility for certain tax credits and deductions. For instance, if an employee makes pretax contributions to a Health Savings Account (HSA) or a Flexible Spending Account (FSA), they may be eligible for additional tax benefits. HSAs and FSAs allow employees to set aside pre-tax dollars for qualified medical expenses, which can further reduce their taxable income and overall tax liability.

Employers can also benefit from offering pretax health insurance contributions. By providing this option, employers can help their employees save money on taxes, which can lead to increased job satisfaction and retention. Additionally, employers may be able to reduce their own payroll tax liabilities by offering pretax health insurance contributions.

However, it's important to note that there are some limitations and considerations when it comes to pretax health insurance contributions. For example, the amount that employees can contribute pretax may be limited by IRS regulations. Additionally, if an employee's health insurance premiums are already paid with pre-tax dollars through their employer, they may not be able to make additional pretax contributions.

In conclusion, exploring the tax advantages of making pretax contributions to health insurance can be a valuable exercise for both employees and employers. By understanding the potential benefits and limitations, individuals can make informed decisions about their health insurance contributions and maximize their tax savings.

Understanding FICA: Are Employee Health Insurance Contributions Subject to FICA?

You may want to see also

Explore related products

![]()

Impact on Take-Home Pay: Analyze how pretax contributions affect an employee's net income

Pretax contributions to health insurance can significantly impact an employee's take-home pay. When an employee contributes to their health insurance premiums before taxes are deducted, this reduces their taxable income. As a result, the amount of federal, state, and local taxes withheld from their paycheck decreases, leading to a higher net income. For example, if an employee contributes $100 per month to their health insurance premiums and their marginal tax rate is 25%, they would save $25 in taxes, effectively increasing their take-home pay by $25.

However, it's important to note that the impact on take-home pay can vary depending on the employee's tax bracket and the specific tax laws in their jurisdiction. Employees in higher tax brackets may see a more significant increase in their net income due to the larger reduction in taxable income. Additionally, some states may not allow pretax contributions to health insurance, or they may have different rules regarding the tax implications of such contributions.

To analyze the impact of pretax contributions on an employee's net income, one can use a simple formula: Net Income = Gross Income - Taxes. By calculating the taxes owed on the gross income and then subtracting that amount from the gross income, an employee can determine their net income. If pretax contributions to health insurance are made, the taxable income should be reduced by the amount of the contributions before calculating the taxes owed.

For instance, let's consider an employee with a gross income of $5,000 per month. If they contribute $200 to their health insurance premiums pretax, their taxable income would be $4,800. Assuming a marginal tax rate of 22%, the employee would owe $1,056 in federal income taxes. Therefore, their net income would be $4,800 - $1,056 = $3,744. Without the pretax contribution, their taxable income would be $5,000, resulting in federal income taxes of $1,100 and a net income of $5,000 - $1,100 = $3,900.

In conclusion, pretax contributions to health insurance can have a positive impact on an employee's take-home pay by reducing their taxable income and, consequently, their tax liability. However, the exact impact will depend on the employee's tax bracket and the specific tax laws in their jurisdiction. By understanding how pretax contributions affect net income, employees can make informed decisions about their health insurance and tax planning strategies.

Evaluating CVS Employee Health Plan's Compliance with Minimum Value Standards

You may want to see also

Explore related products

![]()

Employer's Role: Discuss the employer's involvement and responsibilities regarding pretax health insurance contributions

Employers play a pivotal role in the administration and management of pretax health insurance contributions. They are responsible for setting up and maintaining the necessary infrastructure to allow employees to make pretax contributions to their health insurance premiums. This involves working with insurance providers to establish a plan that accommodates pretax contributions and ensuring that the payroll system is configured to deduct the appropriate amounts from employees' paychecks before taxes are applied.

One of the key responsibilities of employers is to educate their employees about the benefits and implications of making pretax health insurance contributions. This includes providing clear information about how pretax contributions can reduce an employee's taxable income, thereby lowering their overall tax liability. Employers should also be transparent about any limitations or restrictions on pretax contributions, such as maximum contribution amounts or eligibility requirements.

In addition to facilitating pretax contributions, employers must also ensure compliance with relevant tax laws and regulations. This includes accurately reporting pretax contributions on employees' W-2 forms and maintaining proper documentation to support these contributions in case of an audit. Employers may also need to work with tax professionals to ensure that their health insurance plans meet the necessary criteria to qualify for pretax treatment.

Employers should also consider the impact of pretax health insurance contributions on their own financial situation. While pretax contributions can provide tax benefits to employees, they may also reduce the amount of payroll taxes that employers are required to pay. However, employers should carefully weigh these potential savings against the administrative costs associated with managing pretax contributions and ensuring compliance with tax laws.

Overall, employers have a significant role to play in facilitating pretax health insurance contributions. By setting up the necessary infrastructure, educating employees, ensuring compliance with tax laws, and considering the financial implications, employers can help their employees take advantage of the tax benefits associated with pretax contributions while also managing their own responsibilities effectively.

Understanding Employee Health: Key Factors for Workplace Well-Being

You may want to see also

![]()

Common Misconceptions: Address and clarify any misunderstandings about pretax health insurance contributions

One common misconception about pretax health insurance contributions is that they are a form of tax evasion. This is not the case. Pretax contributions are a perfectly legal way for employees to pay for their health insurance premiums before their income is taxed. This can actually reduce the overall tax burden for both the employee and the employer.

Another misconception is that pretax contributions are only available to large corporations. In reality, many small businesses and even some non-profit organizations offer pretax health insurance options to their employees. The size of the company does not determine eligibility for pretax contributions; rather, it is up to the employer to decide whether or not to offer this benefit.

Some people also believe that pretax contributions are only for traditional health insurance plans. However, this is not true. Pretax contributions can also be used for other types of health coverage, such as dental and vision insurance, as well as for health savings accounts (HSAs) and flexible spending accounts (FSAs).

A fourth misconception is that pretax contributions are always the best option for every employee. While pretax contributions can be a great way to save money on health insurance premiums, they may not be the right choice for everyone. For example, employees who have a high deductible health plan may find that they are better off paying for their premiums with after-tax dollars and then deducting the cost on their tax return.

Finally, some employees may believe that their employer is required to offer pretax health insurance contributions. However, this is not the case. Employers are not legally required to offer pretax contributions, and they may choose to offer other types of health insurance benefits instead.

In conclusion, there are several common misconceptions about pretax health insurance contributions. By understanding the facts, employees can make informed decisions about whether or not pretax contributions are the right choice for them.

Are Employee Health Insurance Contributions Taxable? Key Facts Explained

You may want to see also

Frequently asked questions

Yes, employee contributions to health insurance are typically deducted from pretax earnings. This means the amount is subtracted from your gross income before taxes are calculated, which can lower your taxable income and potentially reduce your tax liability.

Pretax health insurance contributions offer several benefits. They reduce your taxable income, which can lead to lower federal and state taxes. Additionally, these contributions are often matched by employers, increasing the total amount put towards health coverage. This setup encourages employees to participate in health insurance plans and promotes financial wellness.

While pretax health insurance contributions reduce your gross income, they generally result in a higher take-home pay due to lower tax deductions. The exact impact depends on your income level, tax bracket, and the amount contributed. It’s advisable to consult with a financial advisor or use tax calculators to understand the specific implications for your situation.