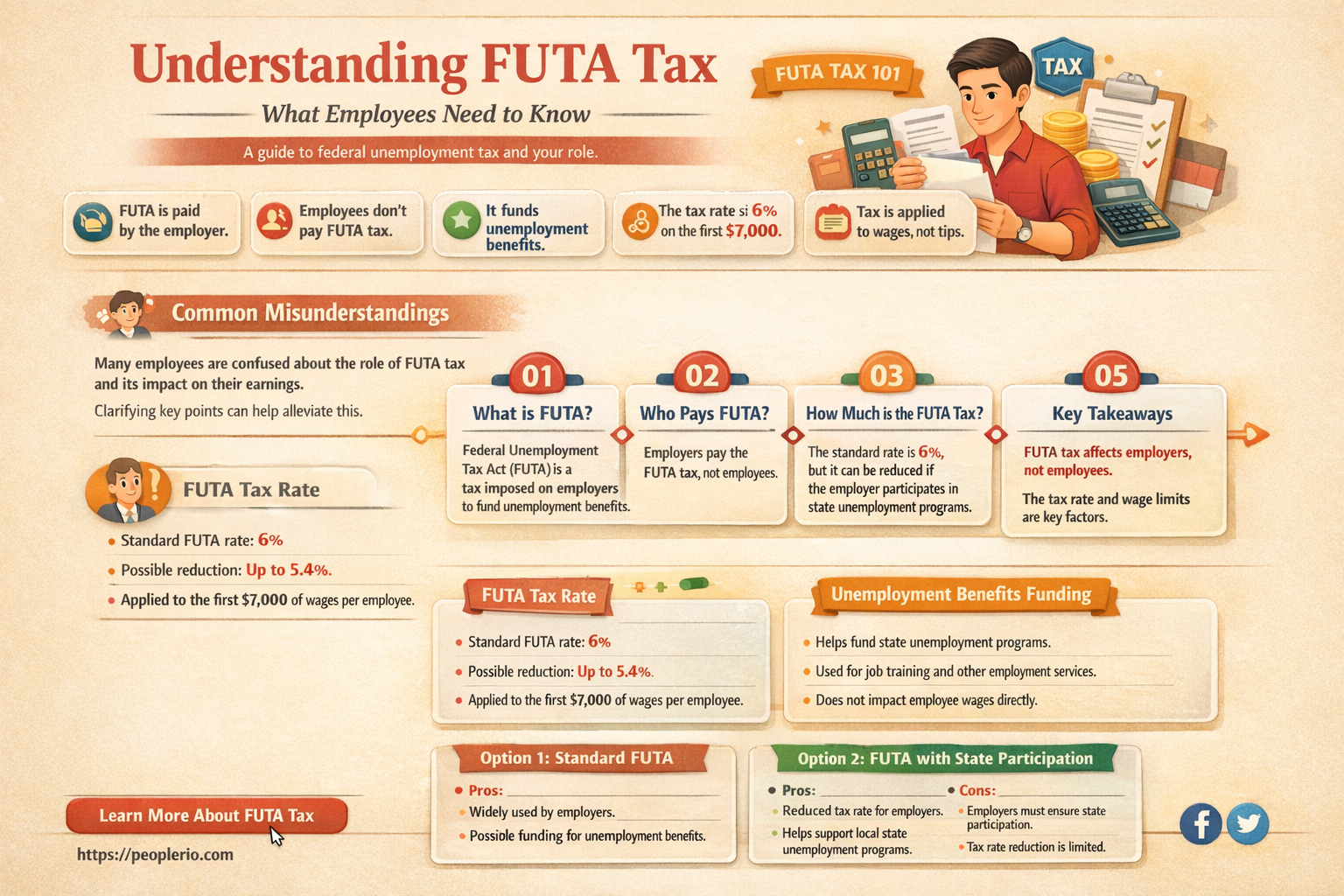

The Federal Unemployment Tax Act (FUTA) is a federal law that imposes a tax on employers to fund unemployment insurance programs. While FUTA taxes are primarily paid by employers, employees may also contribute to state unemployment insurance programs through payroll deductions. However, FUTA taxes themselves are not typically deducted from employee paychecks. Instead, employers are responsible for paying FUTA taxes on a quarterly basis to the Internal Revenue Service (IRS). The tax rate and wage base for FUTA taxes may vary from year to year, and employers must stay informed about these changes to ensure compliance with federal tax laws.

| Characteristics | Values |

|---|---|

| Tax Type | Federal Unemployment Tax Act (FUTA) |

| Purpose | Funds state unemployment insurance programs |

| Payment Responsibility | Employers |

| Employee Contribution | None |

| Tax Rate | 6% (federal rate) |

| Wage Base | First $7,000 of each employee's wages |

| Filing Frequency | Quarterly |

| Impact on Employees | Indirect impact through reduced take-home pay |

Explore related products

$4.99 $9.99

What You'll Learn

![]()

What is FUTA tax?

FUTA tax, or Federal Unemployment Tax Act tax, is a federal tax imposed on employers to fund unemployment insurance programs. This tax is a crucial component of the U.S. unemployment insurance system, which provides temporary financial assistance to workers who have lost their jobs through no fault of their own. Unlike other payroll taxes, FUTA tax is not withheld from employees' wages but is instead paid entirely by employers.

The FUTA tax rate is currently 6% on the first $7,000 of each employee's wages per year. However, employers in states with approved unemployment insurance programs may be eligible for a credit of up to 5.4% against their FUTA tax liability, effectively reducing the tax rate to as low as 0.6%. This credit is designed to incentivize states to maintain robust unemployment insurance systems.

Employers are required to file a Form 940, Employer's Annual Federal Unemployment Tax Return, to report their FUTA tax liability and make payments to the IRS. The deadline for filing Form 940 is January 31st of the year following the tax year. Employers may also need to make estimated FUTA tax payments quarterly if their liability exceeds $500.

One common misconception about FUTA tax is that it is similar to state unemployment taxes. While both types of taxes fund unemployment insurance programs, they are distinct in terms of their rates, wage bases, and filing requirements. Employers must be aware of the specific rules and regulations governing FUTA tax to ensure compliance and avoid penalties.

In summary, FUTA tax is a federal tax paid by employers to support unemployment insurance programs. It is calculated as a percentage of each employee's wages and is reported and paid annually to the IRS. Understanding the intricacies of FUTA tax is essential for employers to maintain compliance and take advantage of available credits and incentives.

Demoting Employees: Legal Considerations for Reducing Roles and Pay

You may want to see also

Explore related products

![]()

Who pays FUTA tax?

The Federal Unemployment Tax Act (FUTA) is a federal law that imposes a tax on employers to fund unemployment insurance programs. This tax is paid by employers, not employees, and is calculated as a percentage of the first $7,000 of each employee's wages. The current FUTA tax rate is 6%, but employers in states with approved unemployment insurance programs may be eligible for a credit of up to 5.4%, effectively reducing the tax rate to 0.6%.

Employers are responsible for paying FUTA tax on a quarterly basis, using Form 940, which is filed with the Internal Revenue Service (IRS). The tax is typically paid by the employer and is not deducted from an employee's wages. This means that employees do not pay FUTA tax directly, but rather, it is an additional cost borne by their employer.

It's important to note that FUTA tax is separate from state unemployment insurance taxes, which may also be required. Employers must pay both federal and state unemployment taxes, and the rates and requirements for each can vary. While employees do not pay FUTA tax, they may be subject to state unemployment insurance taxes, depending on the state in which they work.

In summary, FUTA tax is paid by employers, not employees, and is used to fund federal unemployment insurance programs. Employers are responsible for calculating and paying the tax on a quarterly basis, and while employees do not pay FUTA tax directly, they may be subject to state unemployment insurance taxes.

Paying Employees Without Social Security Numbers: A Comprehensive Guide

You may want to see also

Explore related products

![]()

How much is FUTA tax?

The Federal Unemployment Tax Act (FUTA) imposes a tax on employers to fund unemployment insurance programs. As of 2023, the FUTA tax rate is 6% on the first $7,000 of wages paid to each employee annually. This means that for each employee earning up to $7,000, the employer is responsible for paying 6% of that amount in FUTA taxes. For employees earning more than $7,000, the tax is capped at $420 per employee per year.

It's important to note that FUTA tax is an employer's responsibility, and employees do not pay this tax directly. However, the cost of FUTA tax can indirectly affect employees through reduced take-home pay or potential job losses if employers need to cut costs to cover the tax expenses.

Employers can reduce their FUTA tax liability by taking advantage of state unemployment tax credits. Many states offer credits to employers who pay state unemployment taxes, which can offset the federal tax liability. Additionally, employers can minimize their FUTA tax burden by ensuring accurate and timely reporting of wages and taxes to avoid penalties and interest charges.

In summary, while employees do not pay FUTA tax directly, the 6% tax rate on the first $7,000 of wages can have indirect implications for them. Employers, on the other hand, need to be aware of their FUTA tax obligations and explore ways to reduce their liability through state tax credits and proper reporting practices.

Can Employers Legally Deduct Pay from Salaried Employees? Key Insights

You may want to see also

![]()

Are there any exemptions?

Generally, all employees are subject to FUTA tax, but there are a few exemptions. One notable exemption is for employees who are considered "exempt" under the Fair Labor Standards Act (FLSA). These employees are typically salaried professionals who meet certain criteria, such as earning above a certain threshold and performing specific job duties. Additionally, certain types of workers, such as independent contractors, freelancers, and some agricultural workers, may be exempt from FUTA tax.

Another exemption applies to employees who work for certain types of organizations, such as government entities, non-profit organizations, and certain educational institutions. These organizations may be exempt from paying FUTA tax on behalf of their employees. Furthermore, employees who are considered "casual" or "seasonal" workers may also be exempt from FUTA tax, depending on the specific circumstances of their employment.

It's important to note that while these exemptions exist, they are relatively limited. The majority of employees are still subject to FUTA tax, and employers are responsible for withholding and paying this tax on behalf of their employees. If an employer fails to pay FUTA tax, they may be subject to penalties and fines.

In conclusion, while there are some exemptions to FUTA tax, they are relatively narrow and apply to specific types of employees and organizations. Employers should carefully review the criteria for these exemptions to ensure they are in compliance with FUTA tax regulations.

Can Salaried Employees Face Pay Deductions? Understanding Wage Docking Rules

You may want to see also

![]()

How to calculate FUTA tax?

To calculate FUTA tax, employers must first determine their taxable wage base. This includes all wages paid to employees during the calendar year, up to a certain limit. For 2023, the wage base limit is $7,000 per employee. Employers then multiply the total taxable wages by the current FUTA tax rate, which is 6%. However, employers may be eligible for a credit reduction of up to 5.4% if they pay state unemployment taxes on time.

The calculation process involves several steps. First, sum up the total wages paid to all employees for the year. Next, apply the wage base limit to each employee's earnings. For example, if an employee earned $8,000, only $7,000 would be subject to FUTA tax. Then, calculate the FUTA tax by multiplying the taxable wages by 6%. In the case of the employee who earned $8,000, the FUTA tax would be $420 ($7,000 x 6%).

Employers must also consider any credit reductions they may be eligible for. If an employer pays state unemployment taxes on time, they can reduce their FUTA tax liability by up to 5.4%. This credit is applied after calculating the total FUTA tax. For instance, if an employer's total FUTA tax is $1,000 and they are eligible for the maximum credit reduction, their final FUTA tax liability would be $460 ($1,000 - $540).

It's important to note that FUTA tax is an employer-only tax; employees do not pay FUTA tax. Employers must deposit their FUTA tax payments quarterly with the IRS, using Form 940 to report and pay the tax. Annual reconciliation and reporting are also required to ensure accurate tax payments and to claim any credit reductions.

In summary, calculating FUTA tax involves determining the taxable wage base, applying the current tax rate, and considering any eligible credit reductions. Employers must carefully follow the calculation steps and reporting requirements to ensure compliance with FUTA tax regulations.

Can Employers Legally Pay Employees Two Different Hourly Rates?

You may want to see also

Frequently asked questions

FUTA tax, or Federal Unemployment Tax Act tax, is a federal tax that employers pay to fund unemployment insurance programs. Employers are responsible for paying FUTA tax on their employees' wages.

The FUTA tax rate is 6% on the first $7,000 of each employee's wages per year. This means that for each employee earning $7,000 or more, the employer will pay $420 in FUTA tax annually.

Yes, there are some exceptions and exemptions to paying FUTA tax. For example, employers who pay wages to certain types of workers, such as independent contractors or certain types of agricultural workers, may not be required to pay FUTA tax. Additionally, some employers may be eligible for a reduced FUTA tax rate under certain circumstances.