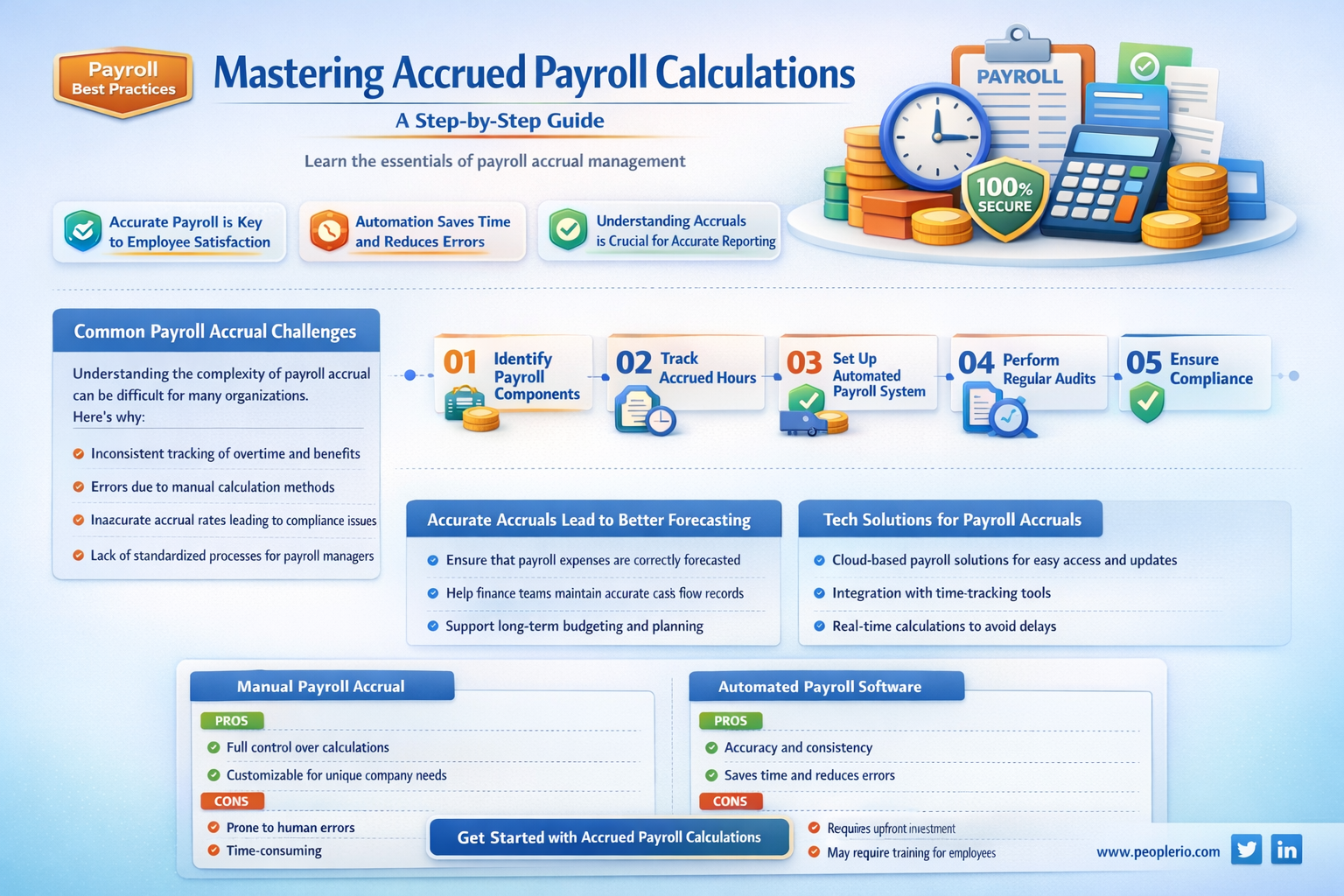

Accrued payroll refers to the amount of money that employees have earned but have not yet been paid. Calculating accrued payroll is essential for businesses to ensure accurate financial reporting and to meet their payroll obligations on time. To calculate accrued payroll, you need to track the hours worked by each employee and multiply those hours by their hourly wage or salary. You should also consider any additional earnings, such as overtime pay, bonuses, or commissions. Once you have calculated the total earnings for each employee, you can sum these amounts to determine the total accrued payroll for the period. It's important to note that accrued payroll is typically recorded as a liability on the balance sheet until it is paid out to employees.

| Characteristics | Values |

|---|---|

| Calculation Basis | Hours worked or days worked |

| Pay Period | Weekly, bi-weekly, semi-monthly, monthly |

| Overtime Calculation | Based on labor laws and company policies |

| Deductions | Taxes, social security, Medicare, etc. |

| Gross Pay | Total earnings before deductions |

| Net Pay | Total earnings after deductions |

| Accrued Payroll Formula | Gross Pay - Net Pay |

| Frequency of Accrual | End of each pay period |

| Record Keeping | Maintain detailed records of hours worked and pay calculations |

| Compliance | Ensure compliance with labor laws and regulations |

Explore related products

What You'll Learn

- Determine Pay Period: Establish the start and end dates for the pay period to calculate accrued payroll

- Calculate Gross Wages: Compute the total earnings before deductions, including hourly wages, salaries, and overtime

- Account for Time Off: Adjust gross wages for any unpaid time off, such as vacation or sick leave

- Subtract Deductions: Remove taxes, insurance, and other deductions from gross wages to find net pay

- Prorate Pay: If necessary, prorate the pay for partial periods worked, such as when an employee starts or leaves mid-period

![]()

Determine Pay Period: Establish the start and end dates for the pay period to calculate accrued payroll

To calculate accrued payroll accurately, the first step is to determine the pay period. This involves establishing the start and end dates for the period in question. The pay period is the timeframe over which an employee's work is evaluated for payment. It can vary in length, commonly ranging from weekly to monthly.

When determining the pay period, it's essential to consider the company's payroll schedule and policies. Some companies may have a fixed pay period, while others might adjust it based on business needs or employee work patterns. For example, a company might choose to have a bi-weekly pay period, where employees are paid every other week.

To establish the start and end dates, you'll need to know the company's pay period policy and the specific dates of the period you're calculating. For instance, if the pay period is weekly and starts on Monday, the end date would be the following Sunday. If it's monthly, you might need to account for the exact number of days in the month.

Once you have the start and end dates, you can calculate the accrued payroll by multiplying the employee's hourly rate by the number of hours worked during that period. It's important to ensure that you're using the correct hourly rate and accounting for any overtime or additional pay that may be applicable.

In some cases, you might need to adjust the accrued payroll amount for factors such as unpaid leave, holidays, or other deductions. This will depend on the company's policies and the specific circumstances of the employee.

By accurately determining the pay period and following the company's payroll policies, you can ensure that employees are paid fairly and on time. This is crucial for maintaining employee satisfaction and compliance with labor laws.

Understanding Payroll's Role in Cost of Goods Sold Calculations

You may want to see also

Explore related products

![]()

Calculate Gross Wages: Compute the total earnings before deductions, including hourly wages, salaries, and overtime

To calculate gross wages, you must first understand the components that make up an employee's total earnings before deductions. This includes hourly wages, salaries, and overtime pay. Hourly wages are calculated by multiplying the number of hours worked by the employee's hourly rate. Salaries are typically annual amounts divided by the number of pay periods in a year to determine the amount per pay period. Overtime pay is calculated by multiplying the number of overtime hours worked by the employee's overtime rate, which is usually 1.5 times the regular hourly rate.

Once you have calculated each component, you can add them together to determine the gross wages. For example, if an employee works 40 regular hours at an hourly rate of $15, their regular wages would be $600. If they work an additional 5 hours of overtime, their overtime pay would be $112.50 (5 hours x $15 x 1.5). Adding these amounts together gives a gross wage of $712.50 for the pay period.

It's important to note that gross wages do not include any deductions such as taxes, social security, or health insurance premiums. These deductions will be subtracted from the gross wages to determine the employee's net pay. Additionally, gross wages may vary depending on the pay period and any changes in the employee's work schedule or pay rate.

When calculating gross wages, it's essential to ensure accuracy and consistency. This can be achieved by using a payroll system or software that automates the calculation process and reduces the risk of human error. It's also important to keep detailed records of all calculations and deductions for compliance and auditing purposes.

In summary, calculating gross wages involves determining the total earnings before deductions by adding together hourly wages, salaries, and overtime pay. This process requires attention to detail and accuracy to ensure that employees are paid correctly and that all payroll records are maintained properly.

Understanding Payroll Workers' Comp Reports: A Calculation Guide

You may want to see also

Explore related products

![]()

Account for Time Off: Adjust gross wages for any unpaid time off, such as vacation or sick leave

To accurately calculate accrued payroll, it's essential to account for any unpaid time off employees may have taken. This includes vacation days, sick leave, or any other type of leave that doesn't result in payment. The process begins by determining the employee's gross wages, which is the total amount earned before deductions. From there, you'll need to adjust these gross wages to reflect the unpaid time off.

One common method is to calculate the daily wage of the employee and then multiply it by the number of unpaid days off. For example, if an employee earns $50,000 per year and works 260 days, their daily wage would be approximately $192.31 ($50,000 / 260). If this employee took 10 unpaid vacation days, you would subtract $1,923.10 from their gross wages ($192.31 x 10).

Another approach is to use a prorated system, where the employee's pay is reduced proportionally to the amount of time they've taken off. Using the same example, if the employee took 10 unpaid vacation days out of a total of 260 working days, you would reduce their gross wages by 3.85% (10 / 260). This would result in a reduction of $1,923.10 from their gross wages, which is the same amount as the daily wage method.

It's important to note that different companies may have different policies regarding unpaid time off, so it's crucial to refer to your company's handbook or HR guidelines to ensure you're following the correct procedures. Additionally, some states or countries may have specific laws or regulations governing unpaid leave, so it's essential to comply with these requirements to avoid legal issues.

In conclusion, accounting for unpaid time off is a critical step in calculating accrued payroll. By adjusting gross wages to reflect the time an employee has taken off, you can ensure that your payroll calculations are accurate and compliant with company policies and legal requirements.

Understanding Payroll Minutes: A Comprehensive Guide for Accurate Calculations

You may want to see also

Explore related products

![]()

Subtract Deductions: Remove taxes, insurance, and other deductions from gross wages to find net pay

To calculate net pay, you must first understand the various deductions that are subtracted from gross wages. These deductions typically include federal and state income taxes, Social Security and Medicare taxes, health insurance premiums, retirement plan contributions, and any other voluntary or mandatory deductions. Each of these deductions serves a specific purpose, such as funding government programs, providing health coverage, or saving for retirement.

The process of subtracting deductions from gross wages involves several steps. First, you need to determine the total amount of gross wages earned during the pay period. This includes all forms of compensation, such as hourly wages, salary, bonuses, and overtime pay. Next, you need to calculate the amount of each deduction based on the employee's earnings and applicable rates. For example, federal income tax is calculated based on the employee's taxable income and filing status, while Social Security tax is calculated at a fixed rate of 6.2% of gross wages up to a certain limit.

Once you have calculated the amount of each deduction, you can subtract them from the gross wages to arrive at the net pay. This can be done using a pay stub or payroll software, which will automatically calculate and deduct the appropriate amounts. It's important to note that the order in which deductions are subtracted can affect the final net pay amount, as some deductions may be based on a percentage of gross wages while others are fixed amounts.

In addition to understanding the deductions themselves, it's also important to be aware of any legal requirements or regulations that may impact the calculation of net pay. For example, there may be minimum wage laws, overtime regulations, or tax withholding requirements that need to be taken into account. Failure to comply with these regulations can result in penalties or legal action against the employer.

By carefully following the steps outlined above and staying informed about relevant laws and regulations, you can ensure that your employees receive accurate and timely net pay. This not only helps to maintain employee satisfaction and morale but also helps to avoid potential legal and financial issues for your business.

Mastering QuickBooks: How to Override Payroll Calculations

You may want to see also

Explore related products

![]()

Prorate Pay: If necessary, prorate the pay for partial periods worked, such as when an employee starts or leaves mid-period

To calculate prorated pay accurately, you must first determine the employee's regular pay period and their rate of pay. For example, if an employee is paid bi-weekly at a rate of $1,000 per pay period, you would need to calculate their daily rate by dividing $1,000 by the number of working days in the pay period (typically 10 days for bi-weekly pay). This gives you a daily rate of $100.

Next, you need to determine the number of days the employee worked in the partial period. For instance, if the employee started work on the 15th day of the pay period, they would have worked 6 days by the end of the period (assuming a 10-day pay period). You would then multiply the daily rate ($100) by the number of days worked (6 days) to get the prorated pay amount, which in this case would be $600.

It's important to note that prorated pay should be calculated based on the actual days worked, not the number of hours. This means that if an employee works a partial day, you should still count it as a full day for prorating purposes, unless the employee is specifically paid by the hour.

When calculating prorated pay for an employee who is leaving mid-period, the process is similar. You would calculate the daily rate as before, then multiply it by the number of days the employee worked in the partial period. However, you should also consider any unused vacation or sick days that the employee may be entitled to, as these may affect the final prorated pay amount.

To avoid errors when calculating prorated pay, it's essential to double-check your calculations and ensure that you're using the correct pay period and rate of pay. You should also communicate the prorated pay amount to the employee in advance, to avoid any confusion or disputes later on.

In summary, calculating prorated pay involves determining the employee's regular pay period and rate of pay, then multiplying the daily rate by the number of days worked in the partial period. By following these steps and double-checking your calculations, you can ensure that your employees are paid accurately and fairly for their work.

Mastering Payroll Calculations: A Comprehensive Guide to Accurate Compensation

You may want to see also

Frequently asked questions

Accrued payroll refers to the amount of money that employees have earned but have not yet been paid. It is important to calculate accrued payroll to ensure accurate financial reporting, maintain proper cash flow management, and comply with payroll tax obligations.

To calculate accrued payroll for salaried employees, you need to determine the total annual salary for each employee and then divide it by the number of pay periods in a year. This will give you the amount of salary that has been earned but not yet paid for each pay period.

For hourly employees, accrued payroll is calculated by multiplying the number of hours worked by the hourly wage rate. You should also consider any overtime hours worked and apply the appropriate overtime pay rate.

Yes, in addition to the basic calculations for salaried and hourly employees, you should also consider factors such as payroll taxes, employee benefits, and any deductions or garnishments that may apply. It is important to accurately account for these factors to ensure compliance with legal requirements and to provide employees with the correct compensation.