Calculating payroll for PPP (Paycheck Protection Program) loans requires a thorough understanding of the program's guidelines and the specific components that make up payroll costs. The PPP, established under the CARES Act, provides financial assistance to eligible businesses to cover payroll and certain other expenses during the COVID-19 pandemic. To calculate payroll for PPP purposes, you need to include salaries, wages, tips, commissions, bonuses, and certain other compensation paid to employees, as well as employer contributions to health insurance and retirement plans. Additionally, you must consider the program's rules regarding loan forgiveness and the documentation required to support your payroll calculations. By accurately determining your payroll costs, you can ensure compliance with PPP requirements and maximize the potential for loan forgiveness.

| Characteristics | Values |

|---|---|

| Calculation Basis | Employee count, average monthly payroll |

| Covered Period | February 2020 to June 2020 |

| Maximum Loan Amount | $10 million |

| Interest Rate | 1% |

| Loan Forgiveness Criteria | Retain employees, maintain salary levels, use loan funds for eligible expenses |

| Eligible Expenses | Payroll costs, rent, mortgage interest, utilities |

| Documentation Required | Payroll records, employee count documentation, proof of eligible expenses |

| Application Process | Submit application through SBA-approved lender |

| Repayment Terms | 2 years, interest-only payments deferred for 6 months |

| Tax Implications | Loan forgiveness may be taxable, consult a tax professional |

Explore related products

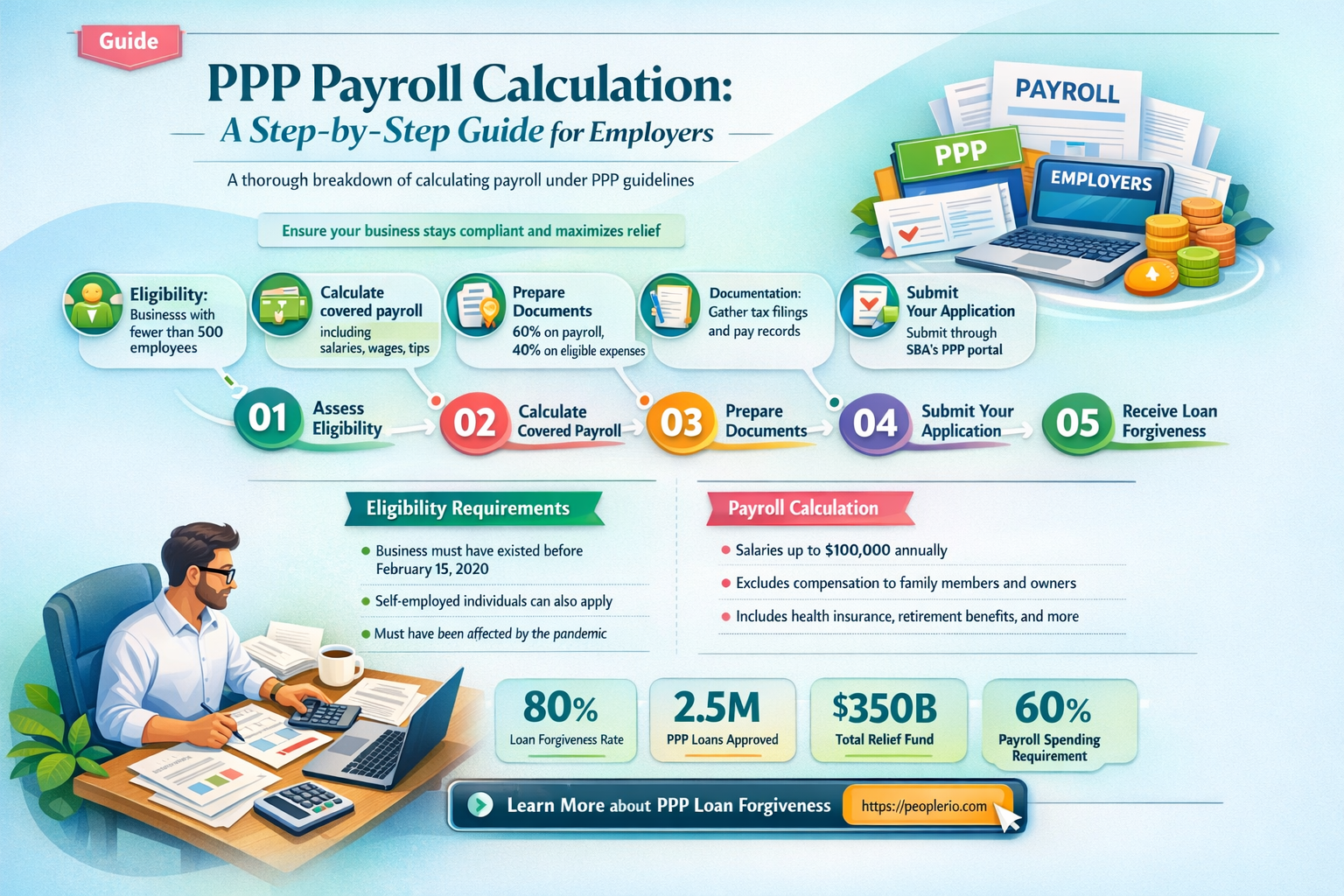

What You'll Learn

- Determine eligible employees: Identify workers who meet PPP loan criteria, such as full-time status and salary thresholds

- Calculate employee retention credit: Compute the credit based on wages paid during the covered period, up to $10,000 per employee

- Assess qualified expenses: Evaluate costs like rent, utilities, and mortgage interest that can be covered by the PPP loan

- Compute loan forgiveness: Calculate the amount of loan forgiveness based on eligible expenses and employee retention

- Prepare documentation: Gather and organize all necessary documents to support PPP loan application and forgiveness requests

![]()

Determine eligible employees: Identify workers who meet PPP loan criteria, such as full-time status and salary thresholds

To determine eligible employees for the Paycheck Protection Program (PPP) loan, you must first understand the criteria set by the Small Business Administration (SBA). Full-time status is a key requirement, which typically means employees who work at least 35 hours per week. However, the SBA has provided some flexibility, allowing employers to consider employees who work fewer hours but are still integral to the business operations.

Next, you need to evaluate the salary thresholds. The PPP loan criteria stipulate that eligible employees must earn less than $100,000 per year. This cap applies to the annual salary, not the hourly wage. Therefore, you'll need to calculate the annual salary for each employee to determine their eligibility. For employees who work variable hours or have fluctuating pay, you may need to estimate their annual salary based on historical data or projected earnings.

It's also important to note that the PPP loan criteria may vary depending on the specific loan program and the time of application. For instance, the SBA has introduced different criteria for first-time and second-time PPP loan applicants. Additionally, there may be industry-specific requirements or exceptions that you need to be aware of.

To ensure accuracy and compliance, it's recommended to consult with a payroll professional or an SBA-approved lender who can provide guidance on the specific criteria and calculations required for your business. They can help you navigate the complexities of the PPP loan program and ensure that you're correctly identifying eligible employees.

In summary, determining eligible employees for the PPP loan involves a careful evaluation of full-time status and salary thresholds, as well as consideration of any industry-specific requirements or exceptions. By understanding these criteria and seeking professional guidance when needed, you can ensure that your business is in the best position to take advantage of the PPP loan program.

Efficient Payroll Management: Kenya's Aren Calculator Explained

You may want to see also

Explore related products

![]()

Calculate employee retention credit: Compute the credit based on wages paid during the covered period, up to $10,000 per employee

To calculate the employee retention credit, you need to focus on the wages paid during the covered period. The credit is computed based on these wages, up to a maximum of $10,000 per employee. This means that for each employee, you should tally the wages paid during the specified timeframe and then apply the credit calculation.

The first step is to identify the covered period. This is the time frame during which the wages are eligible for the credit. Once you have this period established, you can begin to calculate the wages paid within it. Be sure to include all eligible wages, such as regular pay, overtime, and any other compensation that qualifies.

Next, you'll need to determine the credit rate. This rate is applied to the wages paid during the covered period to calculate the actual credit amount. The credit rate can vary depending on the specific program or legislation, so be sure to check the relevant guidelines for the most accurate information.

Once you have the credit rate, you can calculate the credit amount for each employee. Multiply the wages paid during the covered period by the credit rate to get the total credit. Remember, the maximum credit per employee is $10,000, so if the calculated credit exceeds this amount, you'll need to cap it at $10,000.

Finally, you'll need to aggregate the credits for all employees to get the total credit amount for your business. This can be done by simply adding up the individual credits for each employee. The total credit can then be used to offset payroll taxes or other eligible expenses, depending on the specific program requirements.

It's important to note that the employee retention credit is a complex calculation that may require additional guidance or assistance. Be sure to consult with a qualified professional or refer to the relevant program guidelines to ensure that you are calculating the credit correctly and maximizing your potential benefits.

Mastering Manual Payroll: Calculating Hours and Minutes Step-by-Step

You may want to see also

Explore related products

![]()

Assess qualified expenses: Evaluate costs like rent, utilities, and mortgage interest that can be covered by the PPP loan

To accurately assess qualified expenses for the Paycheck Protection Program (PPP) loan, it's crucial to understand which costs are eligible. The PPP loan covers rent, utilities, and mortgage interest, but each category has specific criteria. For rent, the loan can cover the cost of leasing or renting a business location, but it must be a contractual obligation in place before February 15, 2020. Utilities include electricity, gas, water, transportation, telephone, or internet access, and these must also have been established prior to the aforementioned date. Mortgage interest is eligible if the mortgage was in place before February 15, 2020, and the interest payments are for the business's primary residence or a business asset.

When evaluating these expenses, it's important to gather all relevant documentation. This includes lease agreements, utility bills, and mortgage statements. The documentation should clearly show the dates and amounts of the expenses to ensure they meet the PPP loan criteria. Additionally, it's advisable to create a detailed spreadsheet or ledger to track these expenses, as this will make it easier to calculate the total amount eligible for the loan.

One common mistake businesses make is assuming all expenses related to rent, utilities, and mortgage interest are eligible. However, the PPP loan only covers these expenses if they are directly related to the business's primary operations. For example, if a business owner has a home office and uses a portion of their home mortgage interest as a business expense, only the portion directly attributable to the business is eligible. It's essential to carefully review each expense to ensure it meets the PPP loan's criteria and to avoid any potential issues during the loan forgiveness process.

In conclusion, assessing qualified expenses for the PPP loan requires a thorough understanding of the eligibility criteria and meticulous record-keeping. By gathering all necessary documentation and carefully reviewing each expense, businesses can ensure they are maximizing the loan's benefits while avoiding any potential pitfalls.

Mastering Monthly Payroll: A Step-by-Step Calculation Guide for Employers

You may want to see also

Explore related products

![]()

Compute loan forgiveness: Calculate the amount of loan forgiveness based on eligible expenses and employee retention

To compute loan forgiveness for the Paycheck Protection Program (PPP), you must carefully calculate the amount based on eligible expenses and employee retention. The process involves several key steps and considerations.

First, identify the eligible expenses that can be used to calculate loan forgiveness. These typically include payroll costs, rent, mortgage interest, and utilities. Ensure that you have detailed records of these expenses, as you will need to provide documentation to support your calculations.

Next, determine the percentage of your PPP loan that can be forgiven based on employee retention. The forgiveness amount is directly tied to the number of employees you have retained and the level of their compensation. For example, if you have maintained your full workforce and their salaries, you may be eligible for full loan forgiveness.

Once you have gathered the necessary information, use the following formula to calculate the loan forgiveness amount:

\[ \text{Loan Forgiveness Amount} = \frac{\text{Eligible Expenses}}{\text{Total Loan Amount}} \times \text{Employee Retention Percentage} \]

For instance, if your eligible expenses total $100,000 and your employee retention percentage is 80%, the calculation would be:

\[ \text{Loan Forgiveness Amount} = \frac{100,000}{125,000} \times 0.80 = 64,000 \]

In this scenario, you would be eligible for $64,000 in loan forgiveness.

It is crucial to note that there are specific guidelines and requirements set by the Small Business Administration (SBA) for PPP loan forgiveness. Be sure to review these guidelines carefully to ensure that you are following the correct procedures and meeting all necessary criteria.

Finally, consult with a financial advisor or accountant to review your calculations and ensure that you are maximizing your loan forgiveness potential. They can provide valuable insights and help you navigate the complexities of the PPP loan forgiveness process.

Mastering Payroll Budgeting: A Step-by-Step Calculation Guide

You may want to see also

Explore related products

$43.95

![]()

Prepare documentation: Gather and organize all necessary documents to support PPP loan application and forgiveness requests

To successfully apply for a Paycheck Protection Program (PPP) loan and request forgiveness, meticulous documentation is crucial. This process involves gathering and organizing a variety of financial and operational documents that substantiate your business's eligibility and compliance with PPP requirements.

First, you'll need to compile payroll records, including employee payment histories, tax filings, and benefit contributions. These documents will help establish your business's average monthly payroll, which is a key factor in determining the loan amount you're eligible for. Additionally, you should gather records of any recent changes in ownership, such as stock sales or transfers, as these may impact your business's eligibility.

Next, collect financial statements, such as balance sheets, income statements, and cash flow statements, to demonstrate your business's financial health and stability. You may also need to provide copies of business licenses, permits, and insurance policies to verify your business's legal standing and operational capacity.

Once you've gathered all necessary documents, it's essential to organize them in a clear and accessible manner. Create a digital or physical file system that categorizes documents by type and date, making it easy to locate and submit specific items as needed. Consider using a checklist to ensure you've included all required documents and to track your progress throughout the application and forgiveness process.

Finally, be prepared to provide additional documentation as requested by the lender or the Small Business Administration (SBA). This may include supplemental financial information, explanations of any discrepancies in your records, or evidence of how PPP funds were used to support your business operations. By maintaining thorough and organized documentation, you can streamline the PPP loan application and forgiveness process, reducing the risk of delays or denials.

Mastering Payroll: A Guide to Calculating Fringe Benefits for Certified Payroll

You may want to see also

Frequently asked questions

The formula to calculate payroll costs for PPP includes the following components:

- Gross wages paid to employees

- Federal, state, and local payroll taxes

- Employee benefits (such as health insurance and retirement contributions)

Not all employee benefits are eligible for inclusion in the PPP payroll calculation. Eligible benefits typically include health insurance premiums, retirement contributions, and certain other benefits that are directly related to employee compensation.

The eligible payroll period for PPP is typically the time period for which you are requesting loan forgiveness. This period must be within the loan's covered period, which starts on the date the loan is disbursed and ends on the date that is 8 weeks after the loan is disbursed, unless extended by the SBA.