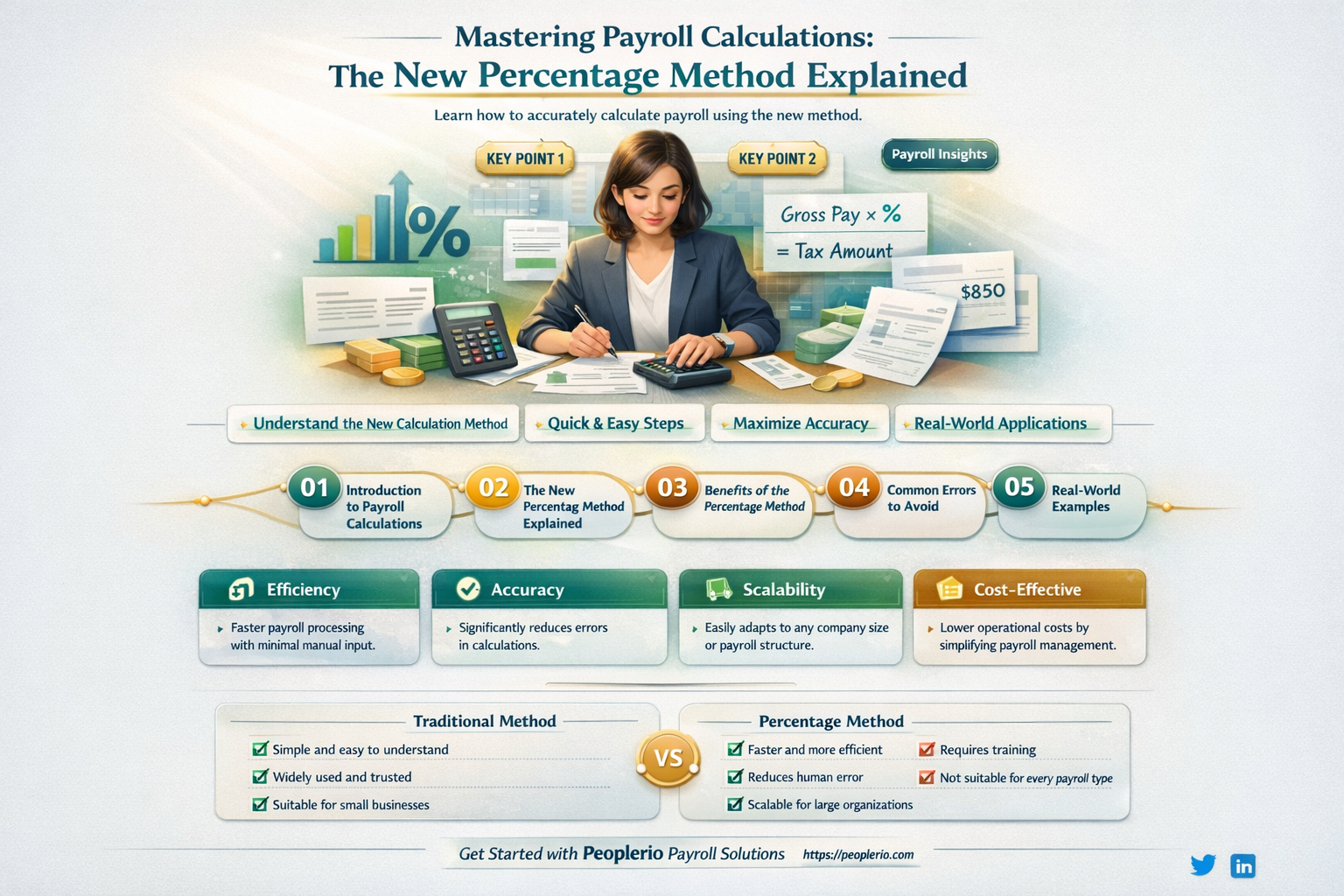

To calculate payroll using the new percentage method, you'll need to follow a series of steps that ensure accuracy and compliance with tax regulations. First, determine the employee's gross wages for the pay period, which includes all forms of compensation such as hourly rates, salaries, bonuses, and commissions. Next, identify the applicable tax rates and deductions, including federal, state, and local income taxes, as well as social security and Medicare contributions. Calculate the total deductions by applying these rates to the gross wages. Then, subtract the total deductions from the gross wages to arrive at the net pay. It's important to note that the new percentage method may require adjustments based on specific circumstances, such as overtime pay or changes in tax laws. Always consult the latest tax guidelines and consider using payroll software to streamline the process and minimize errors.

| Characteristics | Values |

|---|---|

| Payroll Calculation Method | New Percentage Method |

| Employee Gross Salary | $5,000 |

| Social Security Tax Rate | 6.2% |

| Medicare Tax Rate | 1.45% |

| Federal Income Tax Rate | 22% |

| State Income Tax Rate | 4.5% |

| Local Income Tax Rate | 1.5% |

| Total Tax Deductions | $1,231.50 |

| Net Pay | $3,768.50 |

Explore related products

What You'll Learn

- Understanding the New Percentage Method: Learn the updated formula and its components for accurate payroll calculations

- Gathering Employee Information: Collect necessary data such as hours worked, hourly rates, and deductions

- Calculating Gross Pay: Apply the percentage method to determine the gross earnings for each employee

- Deductions and Net Pay: Subtract taxes, benefits, and other deductions to find the net pay

- Payroll Reporting and Compliance: Ensure accurate reporting and compliance with tax and labor regulations

![]()

Understanding the New Percentage Method: Learn the updated formula and its components for accurate payroll calculations

To calculate payroll using the new percentage method, you'll need to understand the updated formula and its components. The new method involves a more nuanced approach to determining employee compensation, taking into account various factors that affect payroll.

First, let's break down the components of the new formula. The primary elements include the employee's base salary, the percentage of time worked, and any additional bonuses or incentives. The formula also considers deductions such as taxes, social security, and other withholdings.

One key aspect of the new percentage method is the calculation of the employee's effective hourly rate. This is determined by dividing the base salary by the total number of hours worked in a pay period. Once you have the effective hourly rate, you can calculate the employee's earnings for the period by multiplying this rate by the actual hours worked.

Another important component is the calculation of overtime pay. The new method requires that overtime hours be paid at a higher rate than regular hours. This is typically 1.5 times the employee's effective hourly rate. To calculate overtime pay, you'll need to determine the number of overtime hours worked and multiply that by the overtime rate.

Finally, you'll need to consider any additional bonuses or incentives that may be applicable. These could include performance bonuses, holiday pay, or other special compensation. Once you've calculated all of these components, you can add them together to determine the employee's total pay for the period.

In summary, the new percentage method for calculating payroll involves a more detailed and nuanced approach than previous methods. By understanding the various components of the formula and how they interact, you can ensure accurate and fair compensation for your employees.

Mastering Payroll Calculations for the Payroll Protection Program

You may want to see also

Explore related products

![]()

Gathering Employee Information: Collect necessary data such as hours worked, hourly rates, and deductions

To calculate payroll using the new percentage method, you must first gather accurate employee information. This includes collecting data on hours worked, hourly rates, and any deductions that may apply. Hours worked can be obtained through time sheets or time tracking software, ensuring that you have a precise record of each employee's labor. Hourly rates should be clearly stated in employment contracts or pay stubs, and any changes to these rates must be communicated in advance. Deductions, such as taxes, benefits, and garnishments, require careful attention to detail and compliance with relevant laws and regulations.

Once you have gathered this essential data, you can begin the process of calculating payroll. Start by multiplying the hours worked by the hourly rate for each employee, taking care to account for any overtime or special pay considerations. Next, calculate the total deductions for each employee, ensuring that you are withholding the correct amounts for taxes and other obligations. Finally, subtract the total deductions from the gross pay to determine the net pay for each employee.

It is crucial to maintain accurate records throughout this process, as errors in payroll calculations can lead to financial discrepancies and legal issues. Consider using payroll software or consulting with a payroll specialist to ensure that you are following the correct procedures and staying up-to-date with any changes to payroll laws and regulations.

In addition to collecting employee information, it is also important to consider the impact of the new percentage method on your payroll calculations. This method may require adjustments to your current payroll system, so it is essential to understand how it works and how it will affect your employees' pay. Be prepared to communicate any changes to your employees and to address any concerns or questions they may have.

By gathering accurate employee information and staying informed about the new percentage method, you can ensure that your payroll calculations are correct and compliant with all relevant laws and regulations. This will not only help you avoid financial and legal issues but will also contribute to a positive and transparent work environment for your employees.

Effortless Payroll Calculations: Unleashing the Power of Excel

You may want to see also

Explore related products

![]()

Calculating Gross Pay: Apply the percentage method to determine the gross earnings for each employee

To calculate gross pay using the percentage method, you'll need to understand the basic components of an employee's earnings and deductions. Gross pay is the total amount earned by an employee before any deductions are made. This includes the employee's base salary, overtime pay, bonuses, and any other forms of compensation. Once you have the gross pay figure, you can then apply the percentage method to determine the net pay, which is the amount the employee will actually receive after deductions.

The percentage method involves calculating the percentage of the gross pay that will be deducted for taxes, social security, and other withholdings. These percentages will vary depending on the employee's tax bracket, filing status, and other factors. You can use tax tables or online calculators to determine the correct percentages for each employee. Once you have the percentages, you can apply them to the gross pay to calculate the total deductions.

For example, let's say an employee earns a gross pay of $1,000 per week. Using the percentage method, you determine that 25% of their pay will be deducted for taxes and social security. To calculate the net pay, you would subtract 25% of $1,000 from the gross pay, which would result in a net pay of $750.

One of the benefits of using the percentage method is that it allows you to easily compare the net pay of different employees, even if they have different gross pay amounts. This can be helpful for budgeting and financial planning purposes. Additionally, the percentage method can be used to estimate the impact of changes in tax rates or other deductions on an employee's net pay.

However, it's important to note that the percentage method is not always accurate, especially for employees with complex tax situations or multiple sources of income. In these cases, it may be necessary to use a more detailed method, such as the wage-based method, to calculate net pay. Regardless of the method used, it's crucial to ensure that all payroll calculations are accurate and compliant with applicable laws and regulations.

Mastering Payroll Accrual: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![Paycheck (2003) (BD) [Blu-ray]](https://m.media-amazon.com/images/I/91eumTA2u1L._AC_UY218_.jpg)

![]()

Deductions and Net Pay: Subtract taxes, benefits, and other deductions to find the net pay

To calculate net pay using the new percentage method, you'll need to understand how deductions are applied. Deductions include federal and state taxes, Social Security, Medicare, and any other withholdings such as health insurance or retirement contributions. The first step is to determine the total gross pay for the employee. This is the amount before any deductions are taken out.

Next, you'll need to calculate the percentage of each deduction. For example, the federal income tax withholding percentage is based on the employee's W-4 form and their annual salary. Similarly, Social Security and Medicare taxes have fixed percentages that are applied to the gross pay. Once you have these percentages, you can calculate the dollar amount for each deduction by multiplying the gross pay by the percentage.

After calculating the individual deductions, you'll need to add them up to get the total deductions. This total is then subtracted from the gross pay to arrive at the net pay. It's important to note that some deductions, such as health insurance premiums, may be pre-tax or post-tax, which affects how they are calculated and reported.

One common mistake when calculating net pay is forgetting to account for all deductions. Make sure to include all applicable withholdings to avoid underestimating the net pay. Additionally, it's crucial to stay up-to-date with any changes in tax laws or withholding rates to ensure accurate calculations.

In summary, calculating net pay involves determining the gross pay, calculating the percentage of each deduction, multiplying the gross pay by these percentages to get the dollar amounts, adding up the deductions, and finally subtracting the total deductions from the gross pay. By following these steps and staying informed about tax laws and rates, you can accurately calculate net pay using the new percentage method.

Mastering Payroll: A Step-by-Step Guide to Calculating Total Costs

You may want to see also

Explore related products

![]()

Payroll Reporting and Compliance: Ensure accurate reporting and compliance with tax and labor regulations

To ensure accurate payroll reporting and compliance with tax and labor regulations, it's crucial to understand the intricacies of the new percentage method. This method involves calculating an employee's gross pay based on a percentage of their previous pay period's earnings. For instance, if an employee earned $1,000 in the previous pay period and the new percentage is 85%, their current gross pay would be $850. This method can be particularly useful for employees with variable income, such as those on commission or with overtime pay.

One of the key benefits of the new percentage method is its ability to streamline payroll calculations, especially for businesses with a large number of employees. By applying a consistent percentage across all employees, companies can simplify their payroll processes and reduce the likelihood of errors. However, it's important to note that this method may not be suitable for all types of employees or industries. For example, employees with fixed salaries or those in industries with specific pay structures may not benefit from this approach.

When implementing the new percentage method, it's essential to consider the impact on employee morale and motivation. A sudden change in pay structure can be unsettling for employees, so it's important to communicate the reasons behind the change and how it will affect their earnings. Additionally, employers should ensure that the new method does not inadvertently discriminate against certain groups of employees, such as those with lower incomes or part-time workers.

To maintain compliance with tax and labor regulations, employers must also be aware of the legal implications of the new percentage method. This includes understanding how the method affects tax withholdings, social security contributions, and other payroll-related obligations. Employers should consult with a payroll specialist or legal advisor to ensure that their payroll processes are in line with current regulations and to avoid potential penalties or legal issues.

In conclusion, the new percentage method can be a valuable tool for simplifying payroll calculations and ensuring compliance with tax and labor regulations. However, it's important to carefully consider the method's suitability for a particular business and its employees, as well as to communicate any changes effectively and maintain awareness of legal requirements. By doing so, employers can streamline their payroll processes while also promoting employee satisfaction and regulatory compliance.

Mastering QuickBooks: How to Override Payroll Calculations

You may want to see also

Frequently asked questions

The new percentage method for calculating payroll involves determining an employee's pay based on a percentage of their previous earnings or a predetermined percentage of their salary. This method can be used to calculate pay raises, bonuses, or other adjustments to an employee's compensation.

To calculate a pay raise using the new percentage method, you would first determine the percentage increase you want to give the employee. Then, you would multiply the employee's current salary or hourly wage by that percentage to determine the amount of the raise. Finally, you would add the raise to the employee's current salary or hourly wage to determine their new pay rate.

Yes, the new percentage method can be used to calculate bonuses. You would determine the percentage of the employee's salary or earnings that you want to give as a bonus, and then multiply that percentage by the employee's salary or earnings to determine the bonus amount.

The new percentage method for calculating payroll can be advantageous because it allows for more flexibility in determining pay raises and bonuses. It can also be easier to calculate than other methods, such as the traditional method of calculating pay raises based on a fixed dollar amount.

One disadvantage of the new percentage method for calculating payroll is that it can be more difficult to compare pay rates between employees. Additionally, if the percentage increase is not carefully considered, it could lead to pay disparities or other issues.