Calculating payroll burden is a crucial task for businesses to understand the total cost of employing their workforce. Payroll burden refers to the additional costs associated with hiring employees, beyond their base salaries or wages. These costs can include social security contributions, Medicare taxes, unemployment insurance, workers' compensation insurance, and other benefits or perks provided to employees. To calculate payroll burden, employers need to identify and sum up all these additional costs, then divide the total by the employees' gross wages to obtain a percentage. This percentage represents the payroll burden and can vary significantly depending on factors such as the number of employees, their salaries, and the benefits offered. Understanding payroll burden is essential for businesses to make informed decisions about hiring, budgeting, and financial planning.

| Characteristics | Values |

|---|---|

| Definition | Payroll burden refers to the total cost of employing staff, including salaries, wages, benefits, and taxes. |

| Components | Salaries, wages, benefits (health insurance, retirement plans, etc.), payroll taxes (social security, Medicare, etc.), workers' compensation insurance, unemployment insurance. |

| Calculation Method | To calculate payroll burden, add up all direct labor costs and indirect labor costs. Direct labor costs include salaries and wages, while indirect labor costs include benefits and taxes. |

| Formula | Payroll Burden = (Salaries + Wages) + (Benefits + Payroll Taxes) |

| Importance | Understanding payroll burden is crucial for businesses to manage their finances effectively, ensure compliance with tax laws, and make informed decisions about hiring and compensation. |

| Factors Affecting | Payroll burden can be affected by various factors such as changes in tax laws, increases in minimum wage, and the addition or removal of benefits. |

| Management Strategies | Businesses can manage payroll burden by implementing cost-saving measures such as outsourcing certain functions, automating processes, and negotiating better rates for benefits. |

| Compliance Requirements | Employers must comply with federal, state, and local tax laws, as well as regulations related to benefits and labor practices. |

| Impact on Business | High payroll burden can impact a business's bottom line, limiting its ability to invest in growth and innovation. Conversely, effective payroll management can lead to increased profitability and competitiveness. |

| Tools and Resources | There are various tools and resources available to help businesses calculate and manage payroll burden, including payroll software, calculators, and consulting services. |

Explore related products

What You'll Learn

- Gross Wages Calculation: Sum of all employee wages before deductions, including salaries, hourly pay, and bonuses

- Payroll Taxes: Federal, state, and local taxes withheld from employee wages, such as Social Security and Medicare

- Benefits and Deductions: Health insurance, retirement plans, and other benefits deducted from employee wages

- Overtime and PTO: Calculating additional pay for overtime work and accounting for paid time off

- Payroll Burden Formula: The final calculation to determine the total payroll burden as a percentage of gross wages

![]()

Gross Wages Calculation: Sum of all employee wages before deductions, including salaries, hourly pay, and bonuses

To calculate gross wages, you must first identify all the components that make up an employee's total compensation before any deductions are made. This includes salaries, hourly pay, and bonuses. Salaries are typically fixed amounts paid annually or monthly, while hourly pay is calculated based on the number of hours worked multiplied by the hourly rate. Bonuses can be performance-based, sign-on bonuses, or other types of incentive pay.

Once you have identified these components, you need to sum them up to get the gross wages. For example, if an employee has a salary of $50,000 per year, works 20 hours of overtime at $25 per hour, and receives a $5,000 performance bonus, their gross wages would be calculated as follows: $50,000 (salary) + ($25 x 20) (overtime) + $5,000 (bonus) = $55,500.

It's important to note that gross wages do not include any deductions such as taxes, social security, or health insurance premiums. These deductions are subtracted from the gross wages to arrive at the net wages, which is the amount the employee actually takes home.

When calculating gross wages, it's also important to consider any other forms of compensation that may not be immediately obvious, such as stock options, commissions, or tips. These should be included in the total gross wages calculation to ensure accuracy.

In summary, calculating gross wages involves identifying all the components of an employee's compensation, summing them up, and excluding any deductions. This calculation is crucial for determining the total payroll burden for a company, as it represents the total amount of money that will be paid out to employees before any deductions are made.

Legal Ramifications of Payroll Errors: Employer vs. Employee

You may want to see also

Explore related products

![]()

Payroll Taxes: Federal, state, and local taxes withheld from employee wages, such as Social Security and Medicare

To calculate payroll taxes, you must first understand the different types of taxes that are withheld from employee wages. Federal payroll taxes include Social Security and Medicare, which are mandated by the Federal Insurance Contributions Act (FICA). The current Social Security tax rate is 6.2% of the employee's gross wages, up to a certain wage base limit, while the Medicare tax rate is 1.45% of all gross wages. In addition to federal taxes, states and localities may also impose their own payroll taxes, such as state income tax, local income tax, and unemployment insurance tax.

Once you have identified the applicable tax rates, you can calculate the payroll taxes by multiplying the employee's gross wages by the tax rate. For example, if an employee earns $1,000 per week, the Social Security tax would be $62 ($1,000 x 0.062) and the Medicare tax would be $14.50 ($1,000 x 0.0145). If the state income tax rate is 3%, the state tax would be $30 ($1,000 x 0.03).

It is important to note that payroll taxes are typically withheld from employee wages on a pre-tax basis, meaning that the taxes are deducted before the employee's take-home pay is calculated. This can impact the employee's net pay and should be taken into consideration when calculating payroll burden.

In addition to calculating the payroll taxes, you must also consider the employer's contribution to these taxes. Employers are required to match the employee's Social Security and Medicare tax contributions, and may also be required to contribute to state and local taxes. This can significantly increase the overall payroll burden, so it is important to factor in these costs when calculating payroll taxes.

To avoid errors and ensure compliance with tax laws, it is recommended that employers use payroll software or consult with a payroll professional to calculate payroll taxes accurately. This can help to streamline the process and reduce the risk of penalties or fines for non-compliance.

Mastering Manual Payroll Calculations: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![]()

Benefits and Deductions: Health insurance, retirement plans, and other benefits deducted from employee wages

Calculating payroll burden involves understanding the various benefits and deductions that impact an employee's take-home pay. Health insurance premiums, retirement plan contributions, and other benefits can significantly reduce the amount of money an employee receives in their paycheck. To accurately calculate payroll burden, it's essential to consider these deductions and how they affect the overall compensation package.

Health insurance premiums are a common deduction from employee wages. The amount deducted depends on the type of plan, the employee's salary, and the employer's contribution. For example, if an employer offers a high-deductible health plan (HDHP) with a health savings account (HSA), the employee may have a lower premium but a higher deductible. In contrast, a preferred provider organization (PPO) plan may have a higher premium but lower out-of-pocket costs. Understanding the nuances of health insurance plans is crucial for calculating payroll burden accurately.

Retirement plan contributions, such as 401(k) or 403(b) plans, are another significant deduction from employee wages. These contributions are typically a percentage of the employee's salary, and the employer may match a portion of the contribution. For example, an employer might match 50% of the employee's 401(k) contribution up to 6% of their salary. This means that if an employee contributes 6% of their salary to their 401(k), the employer will contribute an additional 3%. Understanding the employer's matching policy and the employee's contribution rate is essential for calculating payroll burden.

Other benefits, such as life insurance, disability insurance, and flexible spending accounts (FSAs), can also impact payroll burden. These benefits may be paid entirely by the employer, or the employee may be required to contribute a portion of the cost. For example, an employer might offer life insurance equal to one times the employee's salary, with the employee paying 50% of the premium. Understanding the cost-sharing arrangement for these benefits is crucial for calculating payroll burden accurately.

To calculate payroll burden, employers must consider all of these deductions and how they affect the employee's overall compensation package. This involves adding up the employee's gross pay, subtracting the deductions for health insurance, retirement plans, and other benefits, and then dividing the result by the employee's gross pay. This calculation provides a percentage that represents the payroll burden. For example, if an employee's gross pay is $50,000 per year, and their deductions for health insurance, retirement plans, and other benefits total $10,000 per year, their payroll burden would be 20% ($10,000 / $50,000).

In conclusion, calculating payroll burden requires a thorough understanding of the various benefits and deductions that impact an employee's take-home pay. By considering health insurance premiums, retirement plan contributions, and other benefits, employers can accurately calculate payroll burden and ensure that their employees are receiving a fair and competitive compensation package.

Mastering Payroll Calculations: A Comprehensive Guide to Accurate Compensation

You may want to see also

Explore related products

![]()

Overtime and PTO: Calculating additional pay for overtime work and accounting for paid time off

Calculating additional pay for overtime work involves understanding the regulations set forth by labor laws, which often mandate time-and-a-half pay for hours worked beyond the standard 40-hour workweek. To determine the overtime rate, multiply the employee's regular hourly wage by 1.5. For example, if an employee earns $20 per hour, their overtime rate would be $30 per hour. It's crucial to accurately track all hours worked to ensure proper compensation.

Accounting for paid time off (PTO) requires a clear understanding of the company's PTO policy, including accrual rates, maximum balances, and usage rules. PTO can include vacation time, sick leave, and personal days. Employers must track PTO usage and ensure that employees are paid for any unused PTO upon termination, as required by law in some jurisdictions.

When calculating payroll burden, it's essential to consider the impact of overtime and PTO on overall labor costs. Overtime can significantly increase payroll expenses, especially during peak business periods. Conversely, PTO can reduce labor costs when employees take time off without pay. Employers should regularly review and adjust their overtime and PTO policies to optimize labor costs while maintaining compliance with legal requirements and fostering a positive work environment.

To effectively manage overtime and PTO, employers can implement time-tracking systems and establish clear communication channels with employees regarding their work schedules and PTO usage. This can help prevent disputes and ensure that both employers and employees are aware of their rights and responsibilities.

In summary, calculating additional pay for overtime work and accounting for PTO are critical components of payroll management. Employers must stay informed about labor laws and company policies to accurately calculate payroll burden and maintain a compliant and efficient workforce.

Mastering Monthly Payroll: A Step-by-Step Calculation Guide for Employers

You may want to see also

Explore related products

![]()

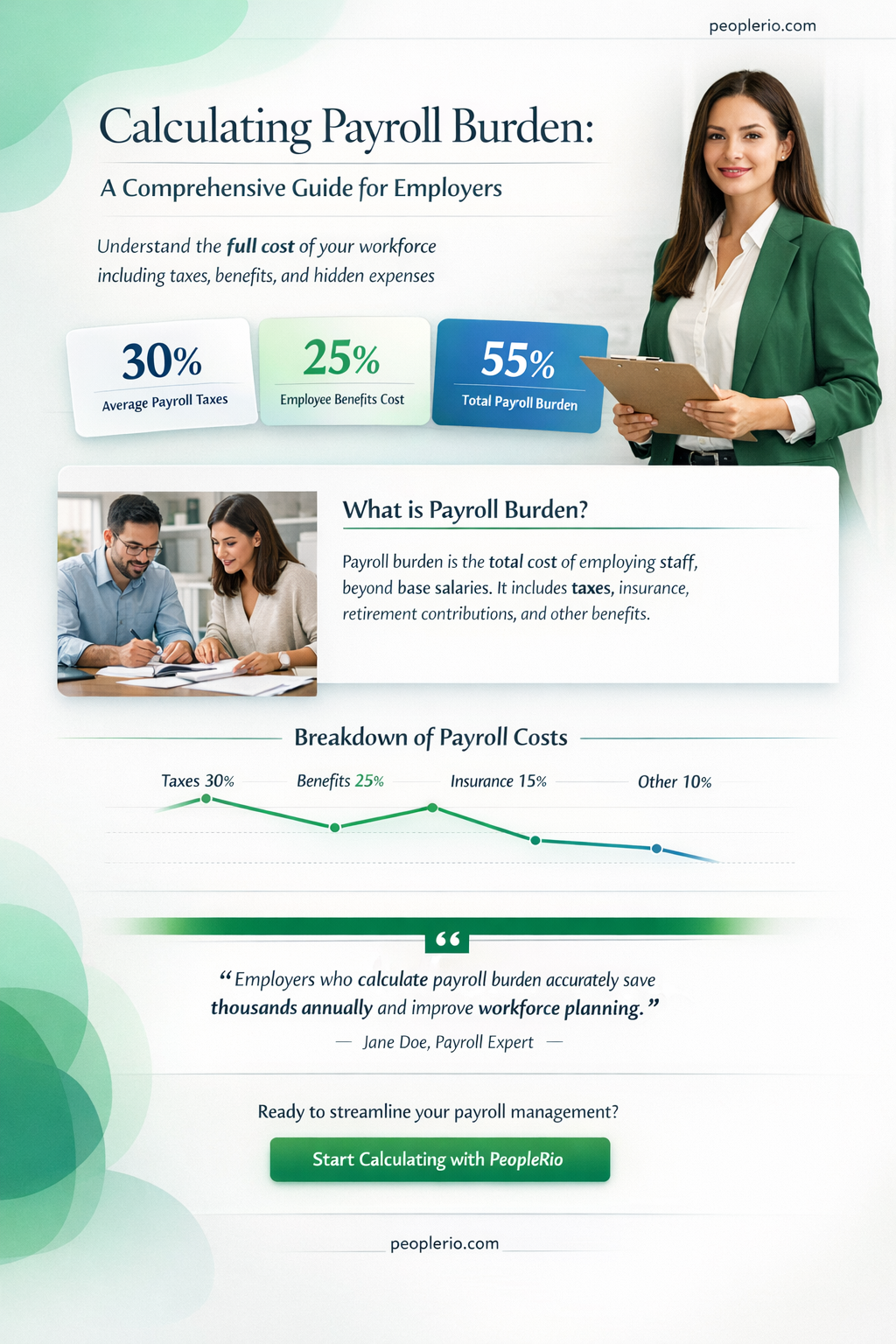

Payroll Burden Formula: The final calculation to determine the total payroll burden as a percentage of gross wages

The Payroll Burden Formula represents the culmination of a series of calculations aimed at determining the total cost of employing staff, expressed as a percentage of gross wages. This formula is critical for businesses to understand the true cost of their workforce beyond just the base salaries or hourly wages paid out. It encompasses all the additional costs associated with employment, such as taxes, benefits, and other mandatory contributions.

To calculate the payroll burden, you first need to identify and sum up all the components that contribute to it. These typically include federal and state income taxes, Social Security and Medicare contributions, unemployment insurance, workers' compensation insurance, and any other legally required payments. Once these are totaled, they are divided by the gross wages paid to employees to arrive at the payroll burden percentage.

For instance, if a company pays out $100,000 in gross wages and incurs an additional $30,000 in payroll taxes and benefits, the payroll burden would be calculated as ($30,000 / $100,000) * 100%, resulting in a 30% payroll burden. This means that for every dollar the company pays in gross wages, an additional 30 cents is spent on payroll-related costs.

Understanding the payroll burden is essential for businesses to accurately forecast their labor costs and make informed decisions about hiring, compensation, and benefits. It also helps in benchmarking against industry standards to ensure competitive positioning in the market. By meticulously calculating the payroll burden, companies can identify areas for cost savings and optimize their payroll processes to improve overall financial efficiency.

Effortless Payroll Calculations: Unleashing the Power of Excel

You may want to see also

Frequently asked questions

Payroll burden refers to the total cost of employing staff, including salaries, wages, benefits, and taxes. It's important to calculate payroll burden to understand the true cost of labor, ensure compliance with tax and employment laws, and make informed decisions about hiring and compensation.

To calculate payroll burden, you need to add up all the direct and indirect costs associated with employing staff. This includes salaries, wages, bonuses, benefits, payroll taxes, and any other expenses related to employment. You can use the following formula: Payroll Burden = Direct Labor Costs + Indirect Labor Costs.

Some common mistakes to avoid when calculating payroll burden include:

- Forgetting to include benefits and taxes in the calculation

- Misclassifying employees as independent contractors

- Not accounting for overtime pay

- Failing to update the calculation when laws or regulations change

Payroll burden can help you make better business decisions by providing insight into the true cost of labor. You can use this information to:

- Determine the optimal staffing levels for your business

- Evaluate the cost-effectiveness of outsourcing certain functions

- Develop a more accurate budget and financial forecast

- Identify areas where you can reduce costs without compromising employee satisfaction