To calculate the workers' compensation rate for payroll calculation, you need to understand the basics of workers' compensation insurance and how it relates to your payroll. Workers' compensation is a type of insurance that provides wage replacement and medical benefits to employees who are injured or become ill as a result of their job. The rate at which you calculate workers' compensation is typically expressed as a percentage of your total payroll. This rate can vary depending on factors such as the nature of your business, your claims history, and the state in which you operate. To determine your workers' compensation rate, you'll need to obtain this information from your insurance provider. Once you have the rate, you can calculate the amount to be deducted from each employee's paycheck by multiplying their gross wages by the workers' compensation rate. It's important to note that workers' compensation rates can change over time, so it's crucial to stay updated with the latest rates to ensure accurate payroll calculations.

| Characteristics | Values |

|---|---|

| Calculation Basis | Employee's average weekly wage |

| Maximum Weekly Benefit | Varies by state, typically a percentage of the average weekly wage |

| Waiting Period | Usually 3 to 7 days, varies by state |

| Duration of Benefits | Temporary, varies by state and injury severity |

| Medical Benefits | Covered, extent varies by state |

| Vocational Rehabilitation | Available in some states |

| Death Benefits | Provided to dependents in case of work-related death |

| Statute of Limitations | Time limit to file a claim, varies by state |

| Appeals Process | Available for denied claims, varies by state |

| Employer's Responsibility | Provide insurance, report injuries, cooperate with claims |

| Employee's Responsibility | Report injury promptly, cooperate with claims |

| Insurance Coverage | Employers must carry workers' compensation insurance |

| Premium Calculation | Based on payroll, industry risk factors, and claims history |

| Compliance Requirements | Regular audits, proper documentation, timely reporting |

| Penalties for Non-Compliance | Fines, legal action, increased premiums |

| Resources for Assistance | State labor departments, insurance companies, legal counsel |

Explore related products

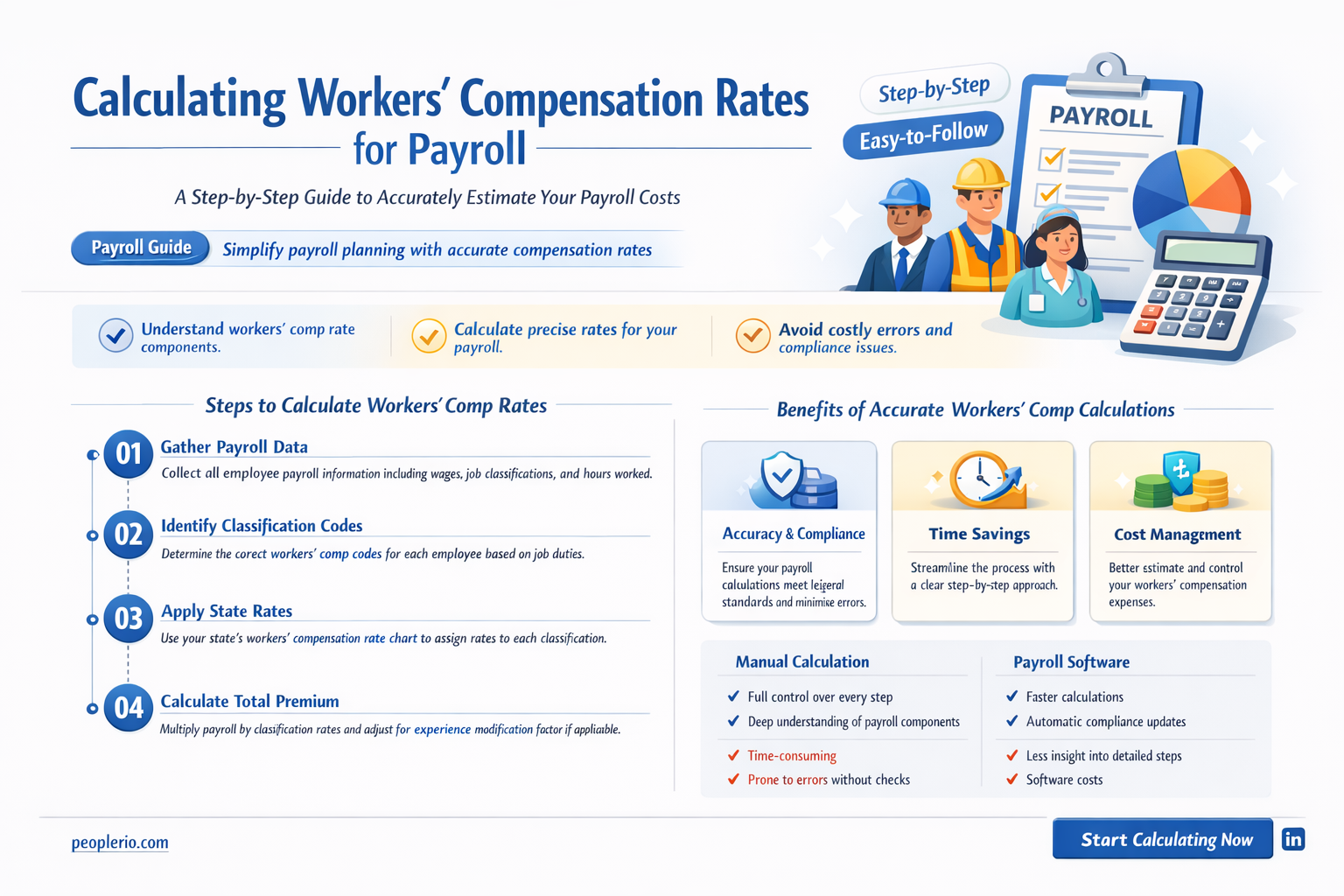

What You'll Learn

- Determine the Base Payroll: Calculate the total payroll amount before any deductions or adjustments

- Identify the Compensation Rate: Find the workers' compensation insurance rate specific to your industry and state

- Apply the Rate to Payroll: Multiply the base payroll by the workers' compensation rate to get the premium amount

- Consider Additional Factors: Adjust the calculation based on factors like employee classification, exemptions, and state-specific rules

- Review and Verify: Double-check the calculations and ensure compliance with all applicable laws and regulations

![]()

Determine the Base Payroll: Calculate the total payroll amount before any deductions or adjustments

To determine the base payroll, you must first calculate the total payroll amount before any deductions or adjustments. This involves summing up the gross wages of all employees for the pay period in question. Gross wages include the total compensation paid to employees, such as salaries, hourly wages, overtime pay, and any other forms of remuneration.

The process of calculating the base payroll typically involves the following steps:

- Identify the Pay Period: Determine the specific time frame for which you are calculating the payroll. This could be weekly, bi-weekly, monthly, or any other frequency used by your organization.

- Collect Employee Data: Gather information on each employee's gross wages for the pay period. This data may come from time sheets, salary records, or other payroll documentation.

- Sum Gross Wages: Add up the gross wages of all employees to arrive at the total payroll amount. This figure represents the base payroll before any deductions or adjustments are made.

- Verify Accuracy: Double-check your calculations to ensure accuracy. This may involve reviewing individual employee records or using payroll software to automate the process and reduce the risk of errors.

Once you have determined the base payroll, you can then proceed to calculate the workers' compensation rate, which will be applied to this total amount to determine the workers' compensation premium. It is crucial to have an accurate base payroll figure, as this will directly impact the amount of workers' compensation insurance you need to purchase.

In summary, determining the base payroll is a critical step in the payroll calculation process. By accurately summing up the gross wages of all employees for the specified pay period, you can ensure that your workers' compensation rate is calculated correctly, ultimately helping to protect your employees and your business.

Effortlessly Calculate Your Payroll Hours in Excel: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Identify the Compensation Rate: Find the workers' compensation insurance rate specific to your industry and state

To accurately calculate workers' compensation rates for payroll, it's essential to first identify the specific compensation rate applicable to your industry and state. Workers' compensation insurance rates vary significantly depending on the type of business, the state in which it operates, and the specific risks associated with the industry. For instance, construction companies typically face higher rates due to the increased risk of workplace injuries compared to office-based businesses.

The process of identifying the correct compensation rate involves several steps. Initially, business owners should consult the relevant state's workers' compensation commission or insurance department to obtain the most current rate information. These rates are often updated annually and can change based on legislative adjustments, economic factors, and shifts in industry risk profiles. Additionally, employers may need to consider the specific classification codes assigned to their business activities, as these codes directly influence the applicable insurance rates.

Once the appropriate rate is determined, employers can then proceed to calculate the workers' compensation premium. This calculation typically involves multiplying the total payroll by the applicable rate. However, it's crucial to note that different states may have varying formulas and additional factors to consider, such as the number of employees, the average weekly wage, and the business's claims history. Employers should also be aware of any minimum or maximum premium limits set by the state.

In some cases, businesses may be able to reduce their workers' compensation rates by implementing safety measures, maintaining a low claims history, or participating in industry-specific risk management programs. Regularly reviewing and updating safety protocols can not only lower insurance costs but also create a safer work environment for employees.

Ultimately, understanding and accurately applying the correct workers' compensation rate is a critical aspect of payroll management. By staying informed about the latest rate changes and industry-specific requirements, business owners can ensure compliance with state regulations and make informed decisions about their workers' compensation insurance coverage.

Calculating Average Monthly Payroll for SBA Loans: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Apply the Rate to Payroll: Multiply the base payroll by the workers' compensation rate to get the premium amount

To calculate the workers' compensation premium, you must first understand the concept of applying the rate to the payroll. This involves multiplying the base payroll amount by the workers' compensation rate, which is a percentage determined by various factors such as the industry, the employer's claims history, and the state regulations. The base payroll is the total amount of wages paid to employees during a specific period, usually a year.

The workers' compensation rate is typically expressed as a percentage, and it represents the cost of providing workers' compensation insurance for every dollar of payroll. For example, if the rate is 2.5%, it means that for every $100 of payroll, the employer needs to pay $2.50 in workers' compensation premiums.

To apply the rate to the payroll, follow these steps:

- Determine the base payroll amount by adding up the total wages paid to employees during the specified period.

- Obtain the workers' compensation rate from the insurance carrier or the state workers' compensation board.

- Multiply the base payroll amount by the workers' compensation rate to get the premium amount.

For instance, if the base payroll is $500,000 and the workers' compensation rate is 2.5%, the premium amount would be $12,500 ($500,000 x 0.025).

It's essential to note that the workers' compensation rate can vary significantly depending on the factors mentioned earlier. Employers with a history of frequent claims or those operating in high-risk industries may face higher rates. Conversely, employers with a good safety record and low claims history may be eligible for lower rates.

In conclusion, applying the rate to the payroll is a crucial step in calculating the workers' compensation premium. By understanding the base payroll amount and the workers' compensation rate, employers can accurately determine the cost of providing this essential insurance coverage for their employees.

Allowances vs. Exemptions: Understanding Payroll Calculation Differences

You may want to see also

Explore related products

![]()

Consider Additional Factors: Adjust the calculation based on factors like employee classification, exemptions, and state-specific rules

When calculating workers' compensation rates for payroll, it's crucial to consider additional factors that can significantly impact the final calculation. Employee classification plays a key role, as different classes of employees may be subject to varying rates. For instance, clerical workers might have a lower rate compared to construction workers due to the differences in job hazards. Exemptions also need to be taken into account; certain employees, such as those in managerial or professional roles, might be exempt from workers' compensation coverage altogether.

State-specific rules add another layer of complexity to the calculation. Each state has its own workers' compensation laws and regulations, which can dictate the calculation method, the types of injuries covered, and the benefits provided. For example, some states might require employers to use a specific formula to calculate the rate, while others might allow for more flexibility. Additionally, states may have different requirements for reporting and paying workers' compensation premiums.

To accurately calculate workers' compensation rates, employers must first determine the employee's classification and any applicable exemptions. This involves reviewing job descriptions, duties, and other relevant factors. Once this information is gathered, employers can consult their state's workers' compensation guidelines to determine the appropriate calculation method. This might involve using a state-provided formula or working with an insurance carrier to determine a rate based on the company's specific risk factors.

Employers should also be aware of any state-specific reporting requirements. This might include submitting annual payroll reports, providing proof of workers' compensation coverage, or maintaining detailed records of employee injuries and claims. Failure to comply with these requirements can result in penalties or fines.

In conclusion, calculating workers' compensation rates for payroll requires careful consideration of employee classification, exemptions, and state-specific rules. By taking these factors into account, employers can ensure they are accurately calculating rates and complying with all relevant laws and regulations. This not only helps to protect employees but also minimizes the risk of legal and financial consequences for the employer.

Calculating Sales-to-Payroll Percentage: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Review and Verify: Double-check the calculations and ensure compliance with all applicable laws and regulations

After calculating the workers' compensation rate for payroll, it's crucial to review and verify the figures to ensure accuracy and compliance with legal requirements. This involves a meticulous process of double-checking the calculations and cross-referencing them with the relevant laws and regulations.

The first step in this process is to review the calculations for any mathematical errors. This includes checking the addition, subtraction, multiplication, and division used to determine the workers' compensation rate. It's also important to ensure that the correct formulas have been applied and that the calculations are consistent with the payroll period in question.

In addition to reviewing the calculations, it's essential to verify that the workers' compensation rate complies with all applicable laws and regulations. This includes federal, state, and local laws, as well as any industry-specific regulations. Employers should consult with legal counsel or a qualified professional to ensure that they are meeting all of their legal obligations.

Another important aspect of the review and verification process is to ensure that the workers' compensation rate is accurate for each individual employee. This includes taking into account any changes in an employee's job duties, salary, or work status that may affect their workers' compensation rate. Employers should also verify that they are using the correct classification codes for each employee, as these codes can impact the workers' compensation rate.

Finally, employers should document their review and verification process to demonstrate compliance with legal requirements. This documentation should include a record of the calculations, the laws and regulations that were consulted, and any changes that were made to the workers' compensation rate. By maintaining thorough documentation, employers can protect themselves from potential legal issues and ensure that they are meeting their obligations to their employees.

Simplifying Payroll: Does Payroll Mate Handle 941 Quarterly Reports?

You may want to see also

Frequently asked questions

The workers' compensation rate is typically calculated as a percentage of the employee's gross wages. The formula is: Workers' Compensation Rate = (Gross Wages x State-Specific Rate) / 100.

The state-specific workers' compensation rate can be determined by contacting your state's workers' compensation insurance provider or by visiting the official website of your state's labor department. Rates vary by state and may also depend on the industry and the employer's claims history.

Generally, gross wages include all earnings before taxes and other deductions. However, certain states may have specific exclusions or deductions, such as overtime pay, bonuses, or certain types of fringe benefits. It's essential to check your state's regulations for any applicable exclusions or deductions.

![Compensation (The Criterion Collection) [Blu-ray]](https://m.media-amazon.com/images/I/71yx5jd1XCL._AC_UL320_.jpg)