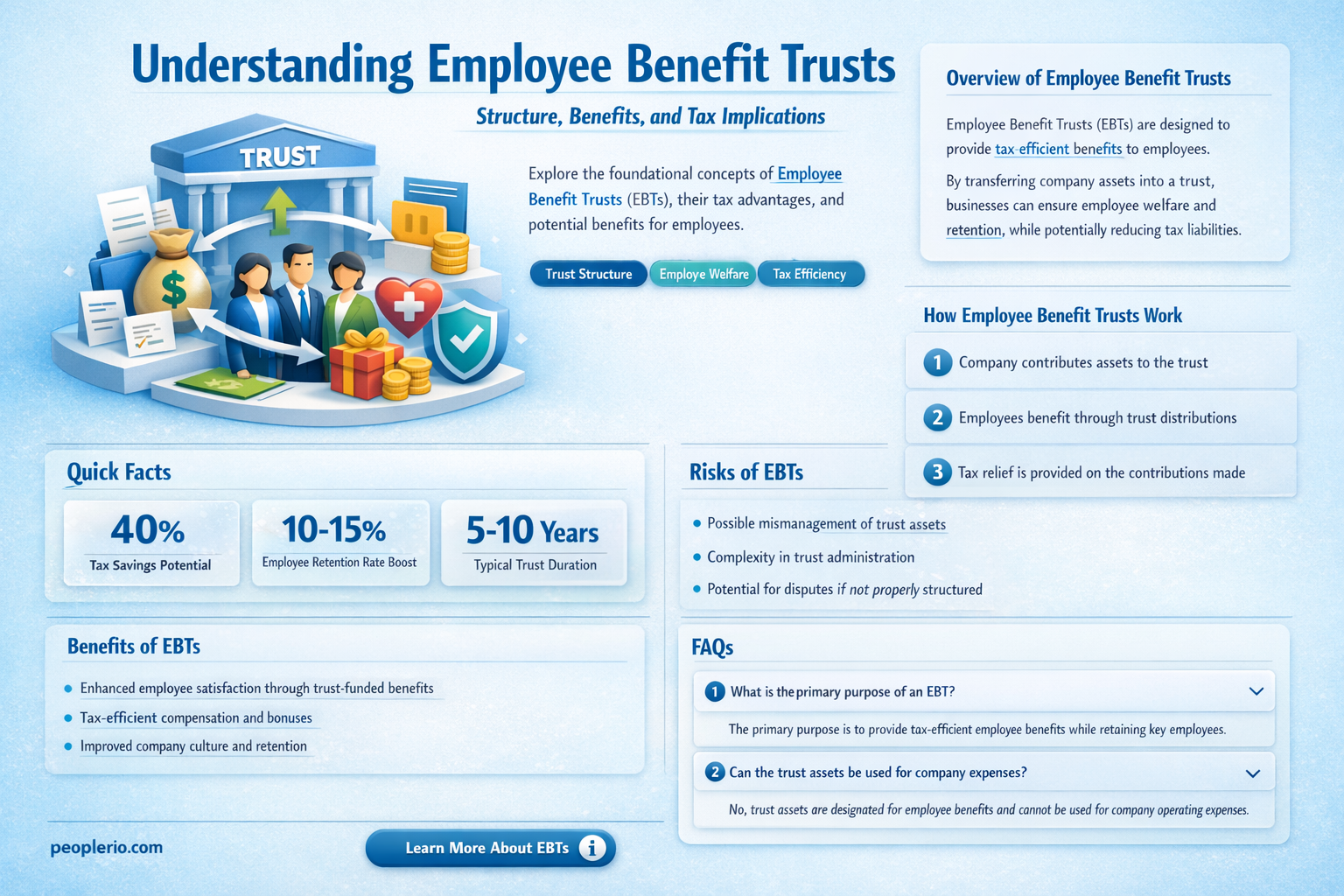

An Employee Benefit Trust (EBT) is a legal arrangement designed to provide benefits to employees, often in the form of shares, bonuses, or other incentives, while offering tax efficiencies for both the employer and the employees. Typically set up by a company, the EBT is managed by trustees who hold assets on behalf of the employees, ensuring that benefits are distributed according to predefined rules. The trust allows employers to reward staff without directly increasing their taxable income, as the benefits are provided through the trust structure. This mechanism can enhance employee motivation and retention while aligning their interests with the company’s long-term success. However, EBTs must comply with strict legal and tax regulations to avoid penalties, making professional advice essential for their effective implementation.

| Characteristics | Values |

|---|---|

| Definition | A legal arrangement where an employer sets aside assets in a trust to provide benefits to employees. |

| Purpose | To fund employee benefits such as pensions, healthcare, life insurance, or retirement plans. |

| Trustee Role | An independent trustee manages the trust assets in the best interest of the beneficiaries (employees). |

| Funding Source | Employer contributions, often tax-deductible, are used to fund the trust. |

| Tax Advantages | Contributions may be tax-deductible for the employer, and assets grow tax-free until distributed. |

| Employee Benefits | Benefits can include retirement plans, health insurance, disability coverage, or death benefits. |

| Legal Structure | Governed by trust law and regulated by relevant authorities (e.g., IRS in the U.S.). |

| Irrevocability | Once assets are placed in the trust, they cannot be reclaimed by the employer for non-benefit purposes. |

| Transparency | Employees are informed about the trust and its benefits through regular disclosures. |

| Portability | Benefits may be transferable if an employee changes jobs, depending on the trust terms. |

| Cost Efficiency | Employers may save on administrative costs compared to managing benefits directly. |

| Employee Retention | Enhances employee satisfaction and retention by providing secure and valuable benefits. |

| Compliance | Must comply with local laws and regulations governing employee benefits and trusts. |

| Flexibility | Can be tailored to meet specific employer and employee needs, including diverse benefit options. |

| Long-Term Security | Provides long-term financial security for employees through guaranteed benefits. |

What You'll Learn

- Trust Structure: Legal framework, trustee roles, and how the trust is established and managed

- Funding Mechanisms: Sources of funds, employer contributions, and investment strategies for trust assets

- Benefit Distribution: Eligibility criteria, types of benefits, and how employees access trust funds

- Tax Implications: Tax treatment for employers, employees, and the trust itself

- Compliance & Regulation: Legal requirements, reporting obligations, and oversight to ensure trust integrity

![]()

Trust Structure: Legal framework, trustee roles, and how the trust is established and managed

An employee benefit trust (EBT) operates within a stringent legal framework designed to safeguard the interests of beneficiaries while providing tax efficiencies for employers. In jurisdictions like the UK, EBTs are governed by trust law and regulated by bodies such as HM Revenue & Customs (HMRC). The legal structure requires clear documentation, including a trust deed or declaration, which outlines the trust’s purpose, rules, and the rights of beneficiaries. This framework ensures transparency and compliance with tax laws, such as those related to employee benefits and pensions. For instance, an EBT must adhere to anti-avoidance rules to prevent misuse, such as the Disguised Remuneration Rules, which target arrangements designed to avoid income tax and National Insurance contributions.

Establishing an EBT involves several critical steps, beginning with the appointment of trustees who act as fiduciaries responsible for managing the trust’s assets. Trustees are typically independent professionals or corporate entities with expertise in trust administration and tax law. Their roles include ensuring the trust operates within legal boundaries, making discretionary decisions about benefit distributions, and maintaining detailed records for audit purposes. For example, trustees must decide how to allocate funds among beneficiaries, such as whether to provide lump-sum payments, pension contributions, or other benefits. The trust is formally established when the settlor (usually the employer) transfers assets into the trust, creating a legally binding arrangement that separates the assets from the employer’s balance sheet.

Managing an EBT requires ongoing diligence to balance legal compliance with the trust’s objectives. Trustees must regularly review the trust’s performance, ensure investments align with beneficiary needs, and file annual reports with regulatory authorities. Practical tips for effective management include setting clear investment policies, conducting periodic risk assessments, and engaging legal counsel to navigate complex tax regulations. For instance, trustees should be cautious of triggering tax liabilities by ensuring benefits are provided in accordance with HMRC guidelines. Additionally, communication with beneficiaries is crucial; regular updates about the trust’s status and their entitlements foster transparency and trust.

Comparatively, the structure of an EBT differs from other employee benefit schemes, such as pension plans or share incentive plans, in its flexibility and discretionary nature. While pension plans have rigid contribution and distribution rules, an EBT allows trustees to tailor benefits to individual or group needs. However, this flexibility comes with increased administrative complexity and regulatory scrutiny. Employers considering an EBT should weigh these factors against the potential tax advantages and the need for professional trustee management. For example, an EBT can be particularly beneficial for companies with fluctuating profits, as it allows them to set aside funds for employee benefits during prosperous periods without committing to fixed contributions.

In conclusion, the trust structure of an EBT hinges on a robust legal framework, the fiduciary duties of trustees, and meticulous establishment and management processes. By adhering to these principles, employers can create a valuable tool for rewarding employees while optimizing tax efficiency. However, the complexity of EBTs underscores the importance of expert guidance to navigate legal and regulatory challenges. Whether for a small business or a multinational corporation, an EBT can be a strategic component of an employee benefits package, provided it is structured and managed with precision and care.

Dismissing Employees for Workplace Intoxication: Legal Boundaries and Best Practices

You may want to see also

![]()

Funding Mechanisms: Sources of funds, employer contributions, and investment strategies for trust assets

Employee benefit trusts (EBTs) rely on a robust funding mechanism to fulfill their purpose of providing long-term benefits to employees. At the heart of this mechanism lies the source of funds, which can vary widely depending on the organization's structure and goals. Common sources include employer contributions, which are typically tax-deductible for the company and can be structured as a fixed percentage of payroll or a lump sum. For instance, a mid-sized tech firm might allocate 5% of its annual profits to the EBT, ensuring a steady influx of capital. Additionally, some trusts may receive funds from employee contributions, though this is less common and often supplementary. External sources, such as grants or donations, can also play a role, particularly in nonprofit or charitable contexts.

Employer contributions are a cornerstone of EBT funding, but their structure and frequency require careful consideration. Companies often adopt a hybrid approach, combining regular monthly contributions with discretionary top-ups based on annual performance. For example, a retail company might contribute $50 per employee monthly, with an additional $10,000 year-end contribution if profit targets are met. This dual strategy ensures consistency while incentivizing organizational success. However, employers must balance these contributions with other financial obligations, such as operational costs and shareholder returns. A rule of thumb is to cap EBT contributions at 10–15% of total employee compensation to maintain fiscal responsibility.

Once funds are secured, the focus shifts to investment strategies, which are critical for growing trust assets and ensuring long-term sustainability. Trustees often adopt a diversified portfolio approach, blending low-risk assets like government bonds with higher-yield options such as equities or real estate. For younger EBTs with a longer time horizon, a 70/30 split between equities and fixed-income securities can maximize growth potential. Conversely, mature trusts nearing payout phase may prioritize capital preservation, shifting to a 30/70 split. Active management by financial advisors is recommended, as they can adjust allocations based on market conditions and the trust’s evolving needs.

A lesser-known but effective strategy is the use of alternative investments, such as private equity or infrastructure funds, which can offer higher returns but come with increased risk and liquidity constraints. For instance, a trust with a 10-year horizon might allocate 10% of its portfolio to private equity, targeting an annual return of 8–10%. However, trustees must ensure these investments align with the trust’s risk tolerance and regulatory requirements. Regular reviews—at least biannual—are essential to assess performance and rebalance the portfolio as needed.

In conclusion, the funding mechanism of an EBT is a multifaceted process that demands strategic planning and adaptability. By diversifying funding sources, structuring employer contributions thoughtfully, and employing dynamic investment strategies, organizations can ensure their trusts remain solvent and effective. Whether through traditional or alternative approaches, the goal remains the same: to create a sustainable financial foundation that benefits employees for years to come.

Unlocking Disney Magic: Understanding Employee Guest Pass Benefits & Usage

You may want to see also

![]()

Benefit Distribution: Eligibility criteria, types of benefits, and how employees access trust funds

Employee benefit trusts (EBTs) are structured to provide a range of benefits to employees, but not all workers automatically qualify. Eligibility criteria are the gatekeepers, ensuring fairness and alignment with the trust’s objectives. Typically, these criteria include tenure (e.g., completing a probationary period of 3–6 months), employment status (full-time vs. part-time), and sometimes performance metrics tied to company goals. For instance, a tech firm might require employees to meet quarterly innovation targets to access certain benefits. Age or role-specific thresholds may also apply; a retirement savings benefit could be limited to employees over 30. Employers must clearly communicate these criteria to avoid confusion and ensure transparency, often through detailed employee handbooks or annual benefit enrollment sessions.

The types of benefits distributed through an EBT are as diverse as the workforce they serve. Common offerings include health insurance, retirement plans, and education stipends, but some trusts go further. For example, a wellness benefit might cover gym memberships or mental health apps, while a parental support benefit could provide subsidized childcare or paid leave extensions. Less conventional perks, like travel vouchers or pet insurance, are gaining traction in competitive industries. The key is tailoring benefits to employee needs, often determined through surveys or focus groups. For instance, a company with a young workforce might prioritize student loan repayment assistance over pension contributions.

Accessing trust funds is a process designed to be straightforward yet secure. Employees typically log into a dedicated portal, where they can view available benefits, track usage, and submit claims. For instance, a worker seeking reimbursement for a medical expense would upload receipts and receive approval within 5–7 business days. Some trusts issue prepaid benefit cards for immediate access to funds, while others integrate with payroll systems for automatic deductions. Employers should provide training or tutorials to ensure employees understand how to navigate the system, especially for older workers less familiar with digital platforms. Regular reminders about unused benefits can also maximize utilization and employee satisfaction.

One critical aspect often overlooked is the role of trustees in benefit distribution. Trustees, who can be internal or external, act as stewards of the trust, ensuring funds are allocated according to legal and ethical standards. They review claims, resolve disputes, and periodically audit the trust to prevent misuse. For example, if an employee submits a fraudulent claim for a nonexistent expense, trustees have the authority to investigate and deny payment. This oversight builds trust among employees, who know the system is fair and sustainable. Employers should emphasize the trustee’s role during onboarding to reinforce the integrity of the EBT.

Finally, the success of an EBT hinges on adaptability. As workforce demographics and priorities shift, so too should the benefits offered. A company with an aging workforce might transition from focusing on career development to prioritizing long-term care benefits. Similarly, in response to economic downturns, trusts may introduce hardship funds to cover unexpected expenses like car repairs or utility bills. Employers must stay attuned to employee feedback and industry trends, adjusting the trust’s offerings annually or biannually. This proactive approach not only enhances employee retention but also positions the company as an employer of choice in a competitive market.

Working During FMLA Leave: Risks, Consequences, and Legal Implications Explained

You may want to see also

![]()

Tax Implications: Tax treatment for employers, employees, and the trust itself

Employers establishing an Employee Benefit Trust (EBT) must navigate a complex tax landscape to ensure compliance and maximize benefits. Contributions to an EBT are generally tax-deductible for the employer as a business expense, provided they are made for the benefit of employees and meet specific regulatory criteria. However, HMRC scrutinizes these contributions to prevent tax avoidance schemes, such as those where benefits are disproportionately directed to company directors. For instance, in the UK, EBTs must adhere to the "wholly and exclusively" rule, ensuring payments are solely for business purposes. Employers should consult tax advisors to structure contributions effectively, avoiding penalties for misclassification or excessive benefits.

Employees receiving benefits from an EBT face varying tax treatments depending on the nature of the benefit. Cash payments or easily convertible assets are typically subject to income tax and National Insurance Contributions (NICs), treated as earnings. In contrast, non-cash benefits, like private medical insurance or childcare vouchers, may qualify for tax exemptions or reduced rates under specific schemes. For example, in the UK, employer-provided pensions through an EBT are tax-free up to certain limits, while gym memberships may be taxable as a perk. Employees should review their benefit packages annually to understand their tax liabilities and plan accordingly.

The trust itself operates as a separate legal entity, subject to its own tax rules. In many jurisdictions, EBTs are taxed on investment income, such as dividends or interest, at standard corporate rates. However, distributions to beneficiaries (employees) are often taxed at the individual level, creating a potential double taxation scenario. Trustees must file annual tax returns and maintain detailed records to demonstrate compliance. For instance, in the US, an EBT may be classified as a grantor trust, where the employer retains certain powers, shifting the tax burden back to the employer. Trustees should prioritize transparency and regular audits to mitigate risks.

Comparing tax treatments across jurisdictions highlights the importance of localization in EBT structuring. In the UK, EBTs are often used for discretionary bonuses, while in the US, they may focus on deferred compensation plans. For multinational employers, aligning EBT strategies with local tax laws is critical. For example, a UK-based company with US employees must ensure compliance with IRS rules on employee benefits, which differ significantly from HMRC guidelines. Leveraging cross-border tax expertise can optimize benefits while avoiding unintended tax consequences.

To navigate tax implications effectively, employers, employees, and trustees should adopt a proactive approach. Employers should regularly review EBT structures to align with evolving tax laws and business goals. Employees must stay informed about the tax treatment of their benefits, potentially seeking advice to minimize personal liabilities. Trustees should prioritize governance and documentation, ensuring the trust operates within legal boundaries. By fostering collaboration between legal, tax, and HR teams, organizations can maximize the value of EBTs while maintaining compliance in a dynamic regulatory environment.

Voluntary Work During FMLA Leave: Legal Considerations for Employees

You may want to see also

![]()

Compliance & Regulation: Legal requirements, reporting obligations, and oversight to ensure trust integrity

Compliance with legal requirements is the bedrock of any employee benefit trust, ensuring that the structure operates within the bounds of the law and maintains its integrity. In the United States, for instance, the Employee Retirement Income Security Act (ERISA) sets forth stringent rules for the establishment, management, and reporting of such trusts. Trustees must adhere to fiduciary standards, acting solely in the best interest of beneficiaries, and avoid conflicts of interest that could compromise the trust’s purpose. Failure to comply can result in severe penalties, including fines and legal action, making it imperative for administrators to stay abreast of regulatory changes.

Reporting obligations are a critical component of compliance, serving as a transparency mechanism for both regulators and beneficiaries. Trusts are typically required to file annual reports, such as Form 5500 in the U.S., which detail financial activities, investments, and administrative practices. These reports must be accurate and timely, as they provide a snapshot of the trust’s health and ensure accountability. Additionally, beneficiaries have the right to access certain documents, fostering trust and confidence in the system. Neglecting these obligations not only risks legal repercussions but also erodes the credibility of the trust.

Oversight mechanisms play a pivotal role in safeguarding the integrity of employee benefit trusts. External auditors, regulatory bodies, and internal compliance teams work in tandem to monitor operations and identify potential issues. For example, the Department of Labor (DOL) in the U.S. conducts audits to ensure compliance with ERISA, while independent auditors verify financial statements for accuracy. Internal oversight may include regular reviews of investment strategies, beneficiary communications, and administrative processes. This multi-layered approach minimizes the risk of fraud, mismanagement, and other malpractices, ensuring the trust fulfills its intended purpose.

A comparative analysis of global practices reveals varying degrees of regulatory rigor. In the UK, the Pensions Regulator enforces strict governance standards, including a focus on long-term sustainability and member protection. Conversely, some jurisdictions may have less stringent regulations, highlighting the importance of aligning trust structures with local legal frameworks. Trustees operating internationally must navigate these differences, ensuring compliance across multiple jurisdictions while maintaining a consistent standard of integrity.

Practical tips for maintaining compliance include establishing a robust governance framework, investing in ongoing education for trustees and administrators, and leveraging technology for accurate record-keeping and reporting. Regular internal audits and external reviews can preempt issues before they escalate. Additionally, fostering a culture of transparency and accountability ensures that all stakeholders, from trustees to beneficiaries, understand their roles and responsibilities. By prioritizing compliance and regulation, employee benefit trusts can operate effectively, providing long-term value to their beneficiaries while mitigating legal and reputational risks.

Per Diem Work Hours: Understanding Limits for Part-Time Employees

You may want to see also

Frequently asked questions

An Employee Benefit Trust (EBT) is a legal arrangement where a company sets up a trust to hold assets for the benefit of its employees. The trust is managed by trustees who distribute benefits, such as bonuses, shares, or pensions, to employees based on predefined rules. The EBT operates independently of the company, ensuring benefits are provided in a tax-efficient manner and in compliance with legal requirements.

Employees of the company, including current and former staff, as well as their dependents, can benefit from an EBT. The trust can also be structured to include specific groups, such as executives or long-term employees, depending on the company’s objectives and the terms of the trust deed.

An EBT can offer tax advantages by allowing benefits to be provided in a tax-efficient manner. For example, contributions to the trust may be tax-deductible for the company, and employees may receive benefits with reduced tax liabilities. However, tax rules vary by jurisdiction, so professional advice is essential to ensure compliance.

An EBT is typically funded by the employer through contributions of cash, shares, or other assets. The trust is managed by appointed trustees who are responsible for administering the trust in accordance with its terms. Trustees must act in the best interests of the beneficiaries and ensure the trust complies with legal and regulatory requirements.