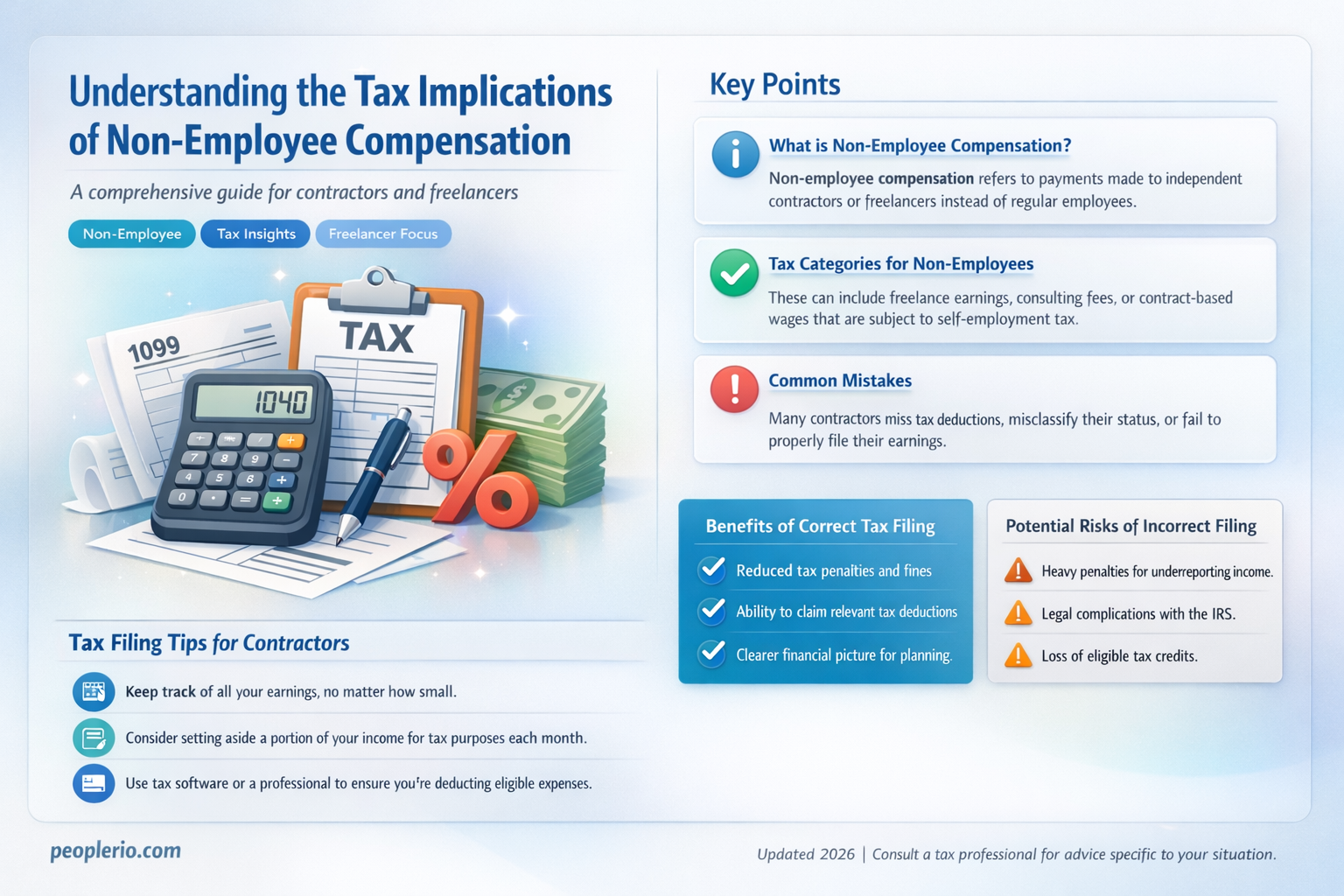

Non-employee compensation refers to payments made to independent contractors, freelancers, or other individuals who are not considered employees of a company. This type of compensation is often subject to different tax rules and regulations compared to employee wages. In many jurisdictions, non-employee compensation is reported on a Form 1099-MISC and is subject to self-employment taxes, which include Social Security and Medicare taxes. The individual receiving the compensation is responsible for paying these taxes, as well as any applicable income taxes. It's important for both the payer and the recipient to understand the tax implications of non-employee compensation to ensure compliance with tax laws and to avoid any potential penalties or fines.

Explore related products

What You'll Learn

- Tax Rates for Non-Employee Compensation: Understand the specific tax rates applied to non-employee income

- Types of Non-Employee Compensation: Explore various forms such as freelance work, consulting fees, and royalties

- Tax Withholding Requirements: Learn about the withholding tax obligations for payers of non-employee compensation

- Reporting Non-Employee Compensation: Discover how to properly report non-employee income on tax returns

- Deductions and Credits Available: Find out about potential tax deductions and credits for non-employee workers

![]()

Tax Rates for Non-Employee Compensation: Understand the specific tax rates applied to non-employee income

Non-employee compensation, such as freelance work or consulting fees, is subject to specific tax rates that differ from those applied to traditional employee wages. Understanding these rates is crucial for both non-employees and the businesses that hire them to ensure proper tax withholding and reporting.

In the United States, non-employee compensation is generally taxed at a flat rate of 30% for federal income tax purposes. This rate applies to the total amount of compensation paid, without any deductions for expenses or allowances. However, non-employees may be able to deduct certain business expenses on their personal tax returns, which can help offset the higher tax rate.

For state tax purposes, the rates for non-employee compensation vary depending on the state. Some states, such as California and New York, have higher tax rates for non-employee income, while others, such as Florida and Texas, have lower rates or no state income tax at all.

Non-employees are also responsible for paying self-employment taxes, which include Social Security and Medicare taxes. The self-employment tax rate is 15.3% for 2023, with a maximum taxable earnings limit of $147,000. This tax is in addition to the federal and state income taxes owed on non-employee compensation.

To avoid underpayment penalties, non-employees are required to make estimated tax payments throughout the year. These payments should be based on the expected tax liability for the year, taking into account the flat tax rate for non-employee compensation and any deductions or credits that may be available.

In conclusion, understanding the specific tax rates applied to non-employee compensation is essential for both non-employees and businesses. By being aware of these rates and making proper tax payments, non-employees can avoid penalties and ensure compliance with tax laws.

Understanding Employee Tax Deductions: A Comprehensive Guide for Workers

You may want to see also

Explore related products

![]()

Types of Non-Employee Compensation: Explore various forms such as freelance work, consulting fees, and royalties

Non-employee compensation encompasses a wide range of payments made to individuals who are not considered employees under tax law. This includes freelancers, independent contractors, consultants, and others who provide services or intellectual property to businesses. Understanding the different types of non-employee compensation is crucial for both payers and recipients to ensure proper tax reporting and compliance.

Freelance work is one of the most common forms of non-employee compensation. Freelancers offer their skills and services to multiple clients on a project-by-project basis. They are responsible for reporting their income and paying self-employment taxes. Consulting fees are another form of non-employee compensation, where individuals provide expert advice or services to businesses. These fees are typically paid on an hourly or project basis and are subject to self-employment taxes as well.

Royalties represent payments made to individuals for the use of their intellectual property, such as patents, trademarks, copyrights, or trade secrets. Royalties can be earned from licensing agreements, book sales, music streaming, or other forms of intellectual property usage. Unlike freelance work or consulting fees, royalties are generally not subject to self-employment taxes but may be taxed as ordinary income.

Other forms of non-employee compensation include commissions, bonuses, and stock options. Commissions are payments made to individuals based on the sales or services they generate, often seen in real estate or insurance industries. Bonuses can be awarded to non-employees for meeting specific performance goals or targets. Stock options allow non-employees to purchase company stock at a predetermined price, which can be a valuable form of compensation if the company's stock value increases.

It is important for businesses to correctly classify and report non-employee compensation to avoid potential tax penalties. The IRS has specific guidelines for determining whether a worker is an employee or an independent contractor, based on factors such as the level of control the business has over the worker's activities, the worker's financial investment in their work, and the degree of permanence in the relationship.

In conclusion, non-employee compensation comes in various forms, each with its own tax implications. Freelancers, consultants, and royalty recipients must be aware of their tax responsibilities and report their income accordingly. Businesses must also ensure they are properly classifying and reporting non-employee compensation to comply with tax laws and avoid penalties.

Understanding California Disability Employee Tax: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Tax Withholding Requirements: Learn about the withholding tax obligations for payers of non-employee compensation

Payers of non-employee compensation must understand their tax withholding obligations to comply with IRS regulations. This involves determining the correct amount of tax to withhold from payments made to independent contractors, freelancers, and other non-employees. The withholding requirements vary depending on the type of compensation and the payee's tax status.

For example, if a payer is making payments to a non-employee who is a U.S. citizen or resident, they may need to withhold federal income tax, Social Security tax, and Medicare tax. The payer must also consider any state or local tax withholding requirements that may apply. To determine the correct amount of tax to withhold, the payer can use the payee's Form W-9, which provides information about the payee's tax identification number and any applicable exemptions or deductions.

In some cases, payers may be required to withhold tax even if the payee does not provide a Form W-9. For instance, if the payer knows or has reason to know that the payee is subject to backup withholding, they must withhold tax at a rate of 24% of the payment. Backup withholding may apply if the payee has not provided their correct tax identification number, has been notified by the IRS that they are subject to backup withholding, or has failed to report all interest or dividends on their tax return.

Payers must also be aware of the reporting requirements for non-employee compensation. They are required to report payments of $600 or more to non-employees on Form 1099-MISC, which must be filed with the IRS and sent to the payee by January 31st of the year following the payment. Failure to comply with these reporting requirements can result in penalties and fines.

To ensure compliance with tax withholding and reporting requirements, payers should consult with a tax professional or use tax software that can help them accurately calculate and report non-employee compensation. By understanding and fulfilling their tax obligations, payers can avoid costly penalties and ensure that their non-employee workers are properly taxed on their earnings.

Maximizing Your Retirement Savings: The Tax Benefits of Employer 401(k) Matches

You may want to see also

![]()

Reporting Non-Employee Compensation: Discover how to properly report non-employee income on tax returns

Non-employee compensation, such as freelance work or consulting fees, is subject to specific tax reporting requirements. Unlike employee wages, which are often withheld and reported by the employer, non-employee compensation typically requires the recipient to report and pay taxes on the income. This can include self-employment taxes, income taxes, and in some cases, estimated taxes.

One of the key aspects of reporting non-employee compensation is understanding the difference between Form 1099-MISC and Form W-2. Form 1099-MISC is used to report miscellaneous income, including non-employee compensation, while Form W-2 is used for employee wages. Non-employee compensation is generally reported in Box 7 of Form 1099-MISC, and the recipient is responsible for paying self-employment taxes on this income.

When reporting non-employee compensation, it's important to keep accurate records of all income received, as well as any expenses related to the work. This can include receipts for equipment, travel expenses, and other business-related costs. These expenses may be deductible on Schedule C of Form 1040, which is used to report business income and expenses.

In addition to federal taxes, non-employee compensation may also be subject to state and local taxes. The specific requirements vary by location, so it's important to check with the relevant state and local tax authorities to ensure compliance.

To avoid potential penalties and interest, it's crucial to report non-employee compensation accurately and on time. This may involve making estimated tax payments throughout the year, as well as filing the appropriate tax forms by the required deadlines. Consulting with a tax professional can help ensure that all reporting requirements are met and that any potential deductions are maximized.

Overall, reporting non-employee compensation requires careful attention to detail and an understanding of the specific tax laws and regulations that apply. By keeping accurate records and staying informed about the latest tax requirements, non-employees can minimize their tax liability and avoid potential issues with the IRS and other tax authorities.

Employee Gifts and Taxes: What's Deductible for Your Business?

You may want to see also

![]()

Deductions and Credits Available: Find out about potential tax deductions and credits for non-employee workers

Non-employee workers, such as freelancers and independent contractors, often face unique tax challenges. One key aspect of managing their tax liability is understanding the deductions and credits available to them. Unlike traditional employees, non-employee workers are responsible for paying both the employer and employee portions of Social Security and Medicare taxes, which can significantly impact their overall tax burden. However, there are several deductions and credits that can help offset these costs and reduce their taxable income.

One important deduction for non-employee workers is the home office deduction. This deduction allows them to deduct a portion of their home expenses, such as rent, utilities, and insurance, if they use a dedicated space in their home for business purposes. To qualify, the space must be used regularly and exclusively for business activities. Additionally, non-employee workers may be able to deduct the cost of equipment, supplies, and other business expenses necessary for their work.

Another valuable credit for non-employee workers is the Earned Income Tax Credit (EITC). This credit is designed to help low- to moderate-income individuals and families reduce their tax liability. To qualify, non-employee workers must meet certain income and eligibility requirements, such as having a valid Social Security number and being a U.S. citizen or resident alien. The amount of the credit varies based on income and family size, and it can be a significant boost for those who qualify.

Non-employee workers may also be able to take advantage of retirement savings plans, such as Individual Retirement Accounts (IRAs) or Simplified Employee Pension (SEP) plans. Contributions to these plans are often tax-deductible, and they can help non-employee workers save for their future while reducing their current tax liability. Additionally, non-employee workers may be eligible for health insurance deductions if they purchase their own health insurance or have a Health Savings Account (HSA).

It's important for non-employee workers to keep accurate records of their business expenses and income throughout the year. This will help them maximize their deductions and credits when filing their tax return. Consulting with a tax professional can also be beneficial, as they can provide guidance on the specific deductions and credits available to non-employee workers and help them navigate the complexities of the tax code.

In conclusion, non-employee workers have access to a variety of deductions and credits that can help reduce their tax burden. By understanding these options and keeping accurate records, they can effectively manage their tax liability and save money.

Are Employee Salaries Tax Deductible? A Business Owner's Guide

You may want to see also

Frequently asked questions

Non-employee compensation refers to payments made to individuals who are not considered employees of a company, such as independent contractors, freelancers, or consultants. This type of compensation is often subject to different tax rules than employee wages.

Non-employee compensation is typically taxed as self-employment income. In the United States, for example, non-employees are required to pay self-employment taxes, which include Social Security and Medicare taxes. The payer may also need to issue a Form 1099-MISC to report the payments to the IRS.

Employee compensation is subject to payroll taxes, including Social Security, Medicare, and federal income tax withholding. Non-employee compensation, on the other hand, is not subject to payroll taxes. Instead, non-employees are responsible for paying self-employment taxes on their net earnings.

Yes, there can be tax benefits to classifying workers as non-employees. For example, non-employees are not subject to payroll taxes, which can save both the worker and the payer money. Additionally, non-employees may be able to deduct business expenses on their tax returns, which can further reduce their tax liability.

Misclassifying an employee as a non-employee can lead to significant tax consequences, including penalties and interest. The IRS may also require the payer to retroactively pay payroll taxes, as well as any unpaid self-employment taxes owed by the worker. Additionally, misclassification can lead to legal issues, such as disputes over worker rights and benefits.