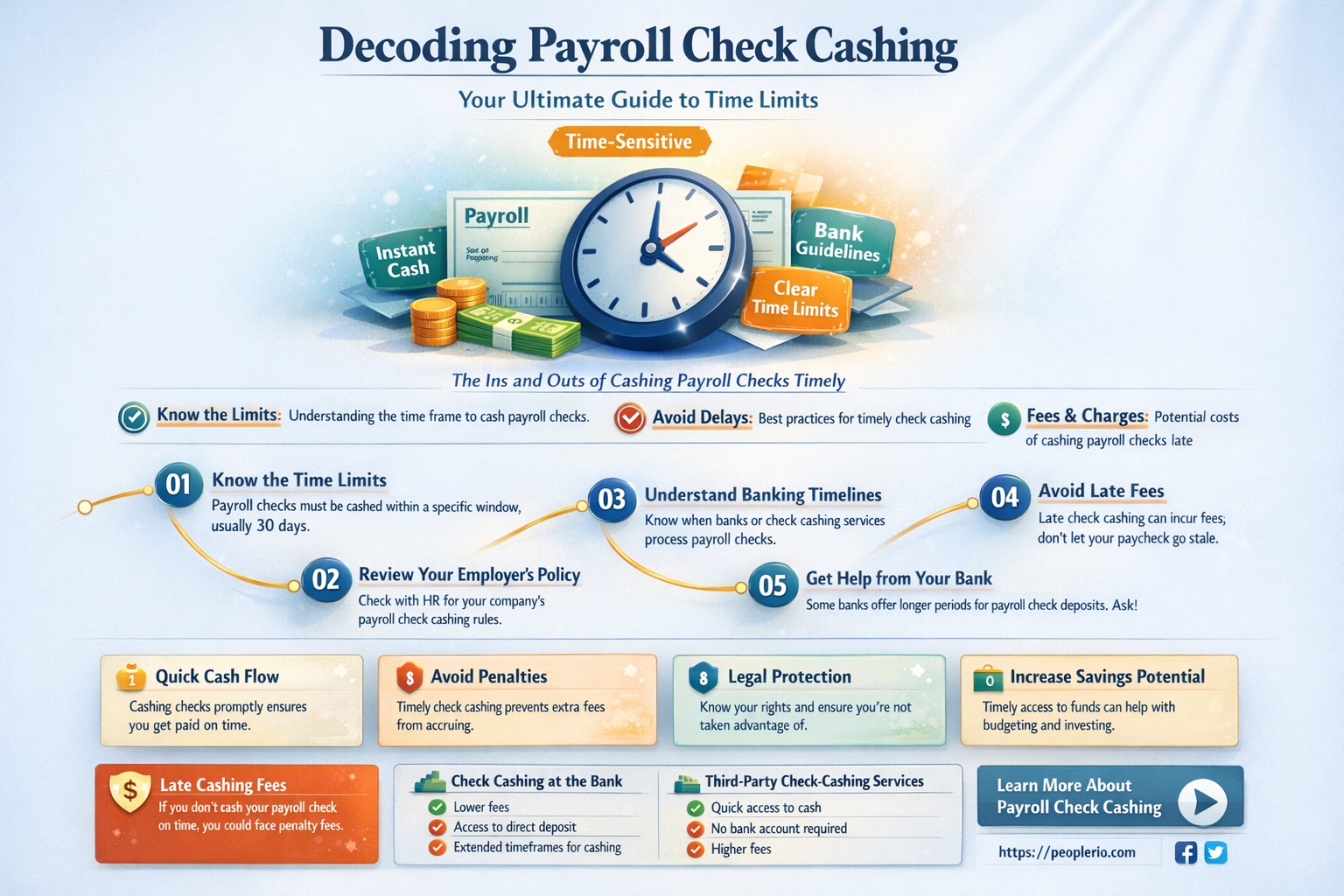

When it comes to cashing a payroll check, understanding the time frame is crucial to avoid any inconvenience or financial setbacks. Generally, payroll checks are valid for a specific period, after which they may become stale and difficult to cash. This duration varies depending on the issuing bank's policies and the state laws where the check was issued. Typically, checks are valid for six months, but some banks may extend this period to a year or more. It's essential to verify the validity period with your bank or employer to ensure you cash your check within the stipulated time. Failing to do so might result in the need to request a reissued check, which could lead to delays in accessing your hard-earned money.

Explore related products

$13.52 $15.95

What You'll Learn

- Check Validity Period: Understand the standard time frame during which a payroll check remains valid for cashing

- Bank Policies: Familiarize yourself with specific bank policies regarding the cashing of payroll checks, including any exceptions

- State Laws: Learn about state-specific laws that may affect the validity and cashing of payroll checks

- Employer Guidelines: Check if your employer has any particular guidelines or restrictions on cashing payroll checks

- Alternatives to Cashing: Explore alternative methods of receiving your pay, such as direct deposit, which may offer more convenience

![]()

Check Validity Period: Understand the standard time frame during which a payroll check remains valid for cashing

The validity period of a payroll check is a crucial aspect that both employers and employees need to be aware of. This period dictates the timeframe within which a check can be cashed or deposited without any issues. Typically, payroll checks are valid for a period of six months from the date of issue. This standard duration is implemented by most banks and financial institutions to ensure that checks are processed within a reasonable time frame, minimizing the risk of fraud or outdated transactions.

However, it's important to note that this validity period can vary depending on the specific policies of the bank or the employer's payroll processing system. Some banks may have a shorter validity period, such as three months, while others might extend it to a year. Employers should clearly communicate the validity period of their payroll checks to employees to avoid any confusion or potential issues with cashing or depositing the checks.

In cases where a payroll check is not cashed or deposited within the validity period, it is considered stale-dated. Stale-dated checks may still be processed by some banks, but they often require additional verification and may incur extra fees. If an employee misses the validity period, they should contact their employer's payroll department to request a reissued check.

Understanding the validity period of a payroll check is essential for employees to manage their finances effectively. It ensures that they can cash or deposit their checks in a timely manner, avoiding any delays in accessing their earned income. Additionally, being aware of this timeframe helps employees plan their financial transactions and budget accordingly.

In conclusion, the standard validity period for a payroll check is six months from the date of issue, but this can vary depending on the bank or employer's policies. Employees should be informed about the validity period of their checks and take necessary actions to cash or deposit them within the specified timeframe to avoid any complications or additional fees.

Does Food Lion Cash Payroll Checks? Your Payment Options Explained

You may want to see also

Explore related products

![]()

Bank Policies: Familiarize yourself with specific bank policies regarding the cashing of payroll checks, including any exceptions

Understanding bank policies is crucial when it comes to cashing payroll checks. Each bank has its own set of rules and regulations that govern the process, including the time frame within which a check must be cashed. Familiarizing yourself with these policies can help you avoid potential issues and ensure a smooth transaction.

One key aspect of bank policies is the validity period of a check. Typically, banks have a cutoff date by which a check must be cashed or deposited. This period can vary, but it's common for banks to require checks to be processed within 6 months from the date of issue. Some banks may have shorter periods, such as 30 or 90 days, so it's essential to check with your specific financial institution.

Exceptions to these policies do exist. For instance, certain types of checks, like government-issued checks, may have different validity periods. Additionally, banks may make exceptions for customers with special circumstances, such as those who are away on extended travel or have other valid reasons for not being able to cash their checks within the standard time frame.

To ensure you're in compliance with your bank's policies, it's a good idea to review their guidelines regularly. You can usually find this information on the bank's website, in their mobile app, or by contacting their customer service department directly. Staying informed about any changes or updates to these policies can help you avoid potential fees or other penalties associated with cashing checks outside of the designated time period.

In summary, familiarizing yourself with your bank's specific policies regarding the cashing of payroll checks is an important step in managing your finances effectively. By understanding the validity period of checks and any exceptions that may apply, you can ensure that you're able to cash your checks without any issues and avoid potential complications down the line.

Understanding Your Payroll Check: A Detailed Look at Its Components

You may want to see also

Explore related products

![]()

State Laws: Learn about state-specific laws that may affect the validity and cashing of payroll checks

State laws play a crucial role in determining the validity and cashing of payroll checks. While federal law sets a general standard, individual states have the authority to enact their own regulations, which can significantly impact the process. For instance, some states may impose shorter time limits for cashing checks, while others may offer more lenient terms.

One key aspect to consider is the statute of limitations for cashing payroll checks. This varies widely from state to state, with some states allowing up to six months or more, while others may limit the timeframe to as little as 30 days. It's essential for employees and employers alike to be aware of these deadlines to avoid potential legal issues or financial losses.

Another important factor is the requirement for proper identification when cashing a payroll check. Some states may have stricter ID requirements than others, and failure to meet these standards could result in the check being returned or the transaction being denied. Additionally, certain states may have specific rules regarding the cashing of checks from out-of-state employers, which could further complicate the process.

Employers must also be mindful of state laws when issuing payroll checks. For example, some states may require employers to provide a written statement detailing the amount and purpose of the check, while others may have specific formatting or disclosure requirements. Failure to comply with these regulations could lead to legal repercussions or disputes with employees.

In conclusion, understanding state-specific laws is crucial for both employees and employers when it comes to the validity and cashing of payroll checks. By staying informed about these regulations, individuals can ensure that they are in compliance with the law and can avoid potential issues or complications.

Direct Deposit Dilemmas: Can You Deposit Your Payroll Check Into Someone Else's Account?

You may want to see also

Explore related products

![]()

Employer Guidelines: Check if your employer has any particular guidelines or restrictions on cashing payroll checks

Employers often have specific guidelines or restrictions on cashing payroll checks to ensure financial security and compliance with banking regulations. These guidelines may include stipulations on the maximum amount that can be cashed, the frequency of cashing checks, or requirements for identification and verification. It is essential for employees to be aware of and adhere to these guidelines to avoid any potential issues or delays in receiving their wages.

To understand the employer's guidelines on cashing payroll checks, employees should first review their employment contract or employee handbook. These documents typically outline the company's policies and procedures regarding payroll, including any restrictions on cashing checks. If the information is not readily available, employees can also consult with their human resources department or payroll administrator to obtain clarification on the guidelines.

In some cases, employers may require employees to cash their payroll checks within a specific timeframe to ensure timely processing and avoid any potential accounting discrepancies. This timeframe may vary depending on the company's payroll schedule and banking arrangements. Employees should be aware of these deadlines and plan accordingly to avoid any delays in receiving their wages.

Employers may also have guidelines in place to prevent fraudulent activities, such as requiring employees to present identification when cashing checks or limiting the number of checks that can be cashed in a single transaction. These measures are designed to protect both the employer and the employee from potential financial losses due to fraud or misuse of payroll funds.

In conclusion, it is crucial for employees to familiarize themselves with their employer's guidelines and restrictions on cashing payroll checks to ensure a smooth and hassle-free payroll process. By understanding and adhering to these guidelines, employees can avoid potential issues and delays in receiving their wages, while also contributing to the overall financial security and compliance of the company.

Does Tops Cash Payroll Checks on Sundays? Your Weekend Guide

You may want to see also

Explore related products

![]()

Alternatives to Cashing: Explore alternative methods of receiving your pay, such as direct deposit, which may offer more convenience

Direct deposit has become an increasingly popular alternative to cashing payroll checks, offering employees a more convenient and secure way to receive their earnings. This method eliminates the need to physically cash a check, which can save time and reduce the risk of lost or stolen checks. With direct deposit, funds are automatically transferred into the employee's bank account on payday, making it immediately available for use.

Another alternative to cashing payroll checks is using a prepaid debit card. Employers can load the employee's earnings onto the card, which can then be used for purchases or withdrawn as cash from ATMs. This option is particularly beneficial for those who do not have a bank account or prefer not to use one for payroll purposes. Prepaid debit cards often come with additional features, such as online account management and mobile banking apps, providing employees with greater control over their finances.

Some employers also offer the option of receiving pay via digital wallets or peer-to-peer payment services, such as PayPal or Venmo. These platforms allow for instant transfers and can be a convenient way to receive and manage funds. However, it is essential to ensure that the employer is reputable and that the payment method is secure to avoid potential scams or fraud.

In addition to these alternatives, employees may also consider setting up an automatic transfer from their checking account to a savings or investment account. This can help promote financial savings and reduce the temptation to spend the entire paycheck immediately. By automating the transfer, employees can ensure that a portion of their earnings is consistently set aside for future goals or emergencies.

When exploring alternative methods of receiving pay, it is crucial to consider factors such as convenience, security, and cost. Employees should evaluate their individual financial needs and preferences to determine the best option for their situation. By understanding the various alternatives available, employees can make informed decisions about how to receive their pay and better manage their finances.

Does Food City Cash Payroll Checks? A Complete Guide for Shoppers

You may want to see also

Frequently asked questions

Typically, payroll checks are valid for six months from the date issued. However, this can vary depending on your employer's policy or state laws.

If you don't cash your payroll check within the specified period, it may become void. You would then need to contact your employer to request a new check.

Yes, you can deposit a payroll check into your bank account. This usually extends the validity period, as banks often hold checks for a longer duration before processing.

Some banks or check-cashing services may charge a fee to cash a payroll check. However, many banks offer free check-cashing services for their customers.

To verify the validity of your payroll check, you can contact your employer's payroll department or check the check's date to ensure it's within the valid period.