Calculating 401(k) payroll deductions involves understanding the contribution limits, the employee's deferral rate, and any employer matching contributions. The process begins with determining the maximum allowable contribution for the year, which is set by the IRS. For 2023, the limit is $22,500 for individuals under 50 and $30,000 for those 50 and older. Next, you need to know the employee's deferral rate, which is the percentage of their gross income they choose to contribute to their 401(k). This rate is typically expressed as a whole number, such as 5% or 10%. To calculate the deduction, multiply the employee's gross income by their deferral rate. For example, if an employee earns $1,000 per paycheck and defers 5%, the deduction would be $50. Additionally, if the employer offers a matching contribution, you would add that amount to the employee's deduction. It's important to note that these calculations should be made for each pay period and adjusted as necessary based on changes in income or contribution rates.

| Characteristics | Values |

|---|---|

| Contribution Type | Employee contribution, Employer contribution, Roth contribution |

| Contribution Limits | $19,500 (2023), $20,500 (2024) |

| Catch-up Contributions | Additional $6,500 for those 50 and older |

| Deduction Frequency | Per paycheck |

| Tax Treatment | Pre-tax for traditional contributions, After-tax for Roth contributions |

| Vesting Schedule | Immediate vesting for employee contributions, Gradual vesting for employer contributions |

| Investment Options | Mutual funds, Stocks, Bonds, ETFs |

| Fees | Administrative fees, Investment fees |

| Withdrawal Rules | Penalty-free withdrawals after age 59.5, Required minimum distributions starting at age 73 |

| Loan Provisions | Loans allowed, Interest rates vary |

| Hardship Withdrawals | Allowed for certain financial hardships |

| Beneficiary Designation | Required to designate a beneficiary |

| Portability | Transferable to new employers or IRAs |

| Compliance | Subject to IRS regulations and audits |

Explore related products

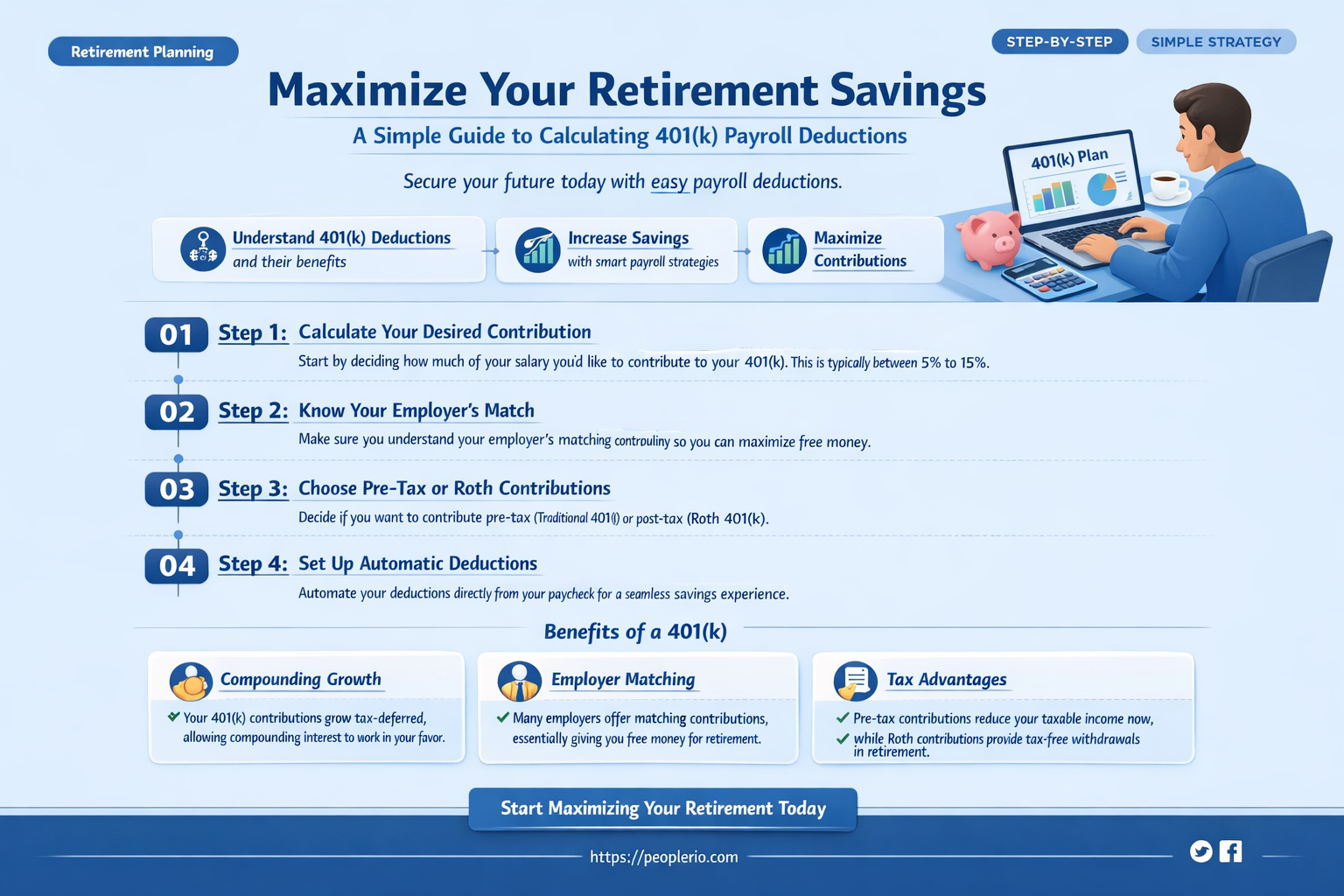

What You'll Learn

- Understanding Contribution Limits: Learn the annual maximum contribution limits for 401(k) plans

- Calculating Contribution Percentage: Decide on the percentage of your salary to contribute

- Determining Pre-Tax Deductions: Understand how pre-tax contributions reduce taxable income

- Estimating Tax Savings: Calculate potential tax savings based on contribution amount

- Setting Up Automatic Contributions: Arrange for automatic payroll deductions to ensure consistent saving

![]()

Understanding Contribution Limits: Learn the annual maximum contribution limits for 401(k) plans

Understanding the contribution limits for 401(k) plans is crucial for optimizing your retirement savings. As of 2023, the annual maximum contribution limit for 401(k) plans is $22,500 for individuals under the age of 50. For those aged 50 and older, an additional catch-up contribution of $7,500 is allowed, bringing the total to $30,000. These limits are subject to change, so it's essential to stay informed about any updates or adjustments made by the IRS.

It's important to note that these contribution limits apply to the total amount you can contribute to all 401(k) plans you participate in, not just a single plan. If you have multiple 401(k) accounts, you'll need to coordinate your contributions to ensure you don't exceed the overall limit. Additionally, employer contributions do not count towards these limits, so you can still receive matching funds from your employer on top of your own contributions.

When calculating your 401(k) payroll deduction, it's essential to consider these contribution limits to avoid over-contributing. You can adjust your payroll deduction amount throughout the year to ensure you're on track to meet your savings goals without exceeding the limits. Many employers offer tools or resources to help you estimate your contributions and make adjustments as needed.

In summary, understanding the contribution limits for 401(k) plans is a key aspect of managing your retirement savings. By staying informed about these limits and coordinating your contributions across multiple plans, you can make the most of your retirement savings opportunities while avoiding potential penalties for over-contributing.

Mastering Manual Payroll: A Step-by-Step Guide for Beginners

You may want to see also

Explore related products

![]()

Calculating Contribution Percentage: Decide on the percentage of your salary to contribute

To calculate your contribution percentage for a 401(k) plan, you need to decide how much of your salary you want to allocate towards your retirement savings. This decision should be based on several factors, including your current financial situation, your retirement goals, and your expected expenses. A common rule of thumb is to contribute at least 10% to 15% of your gross income, but this may not be feasible for everyone. If you're just starting out, you may want to begin with a smaller percentage and gradually increase it over time as your income grows and your financial situation stabilizes.

When deciding on your contribution percentage, it's important to consider any employer matching contributions. Many employers will match a certain percentage of your contributions, which can significantly boost your retirement savings. For example, if your employer matches 50% of your contributions up to 6% of your salary, you should aim to contribute at least 6% to take full advantage of the match. This means that for every dollar you contribute, your employer will contribute an additional 50 cents, effectively doubling your savings.

Another factor to consider is your tax situation. Contributions to a traditional 401(k) plan are made on a pre-tax basis, which means they can reduce your taxable income and potentially lower your tax bill. If you're in a high tax bracket, contributing more to your 401(k) can be a tax-efficient way to save for retirement. However, if you're in a low tax bracket, you may want to consider contributing to a Roth 401(k) plan instead, which allows you to contribute after-tax dollars in exchange for tax-free growth and withdrawals in retirement.

Once you've decided on your contribution percentage, you'll need to set up your payroll deductions accordingly. This typically involves filling out a form with your employer's human resources department, specifying the percentage of your salary you want to contribute and selecting the appropriate investment options for your contributions. It's important to review your payroll deductions regularly to ensure they're accurate and to make any necessary adjustments based on changes in your income or financial situation.

In conclusion, calculating your contribution percentage for a 401(k) plan involves careful consideration of your financial situation, retirement goals, employer matching contributions, and tax implications. By taking the time to make an informed decision and setting up your payroll deductions correctly, you can maximize your retirement savings and achieve your long-term financial objectives.

Mastering Payroll Expense Calculations: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Determining Pre-Tax Deductions: Understand how pre-tax contributions reduce taxable income

Pre-tax deductions, such as contributions to a 401(k) plan, are a crucial aspect of payroll deductions because they can significantly reduce an employee's taxable income. This reduction occurs before federal, state, and local taxes are calculated, which can lead to substantial savings. For instance, if an employee contributes $5,000 to their 401(k) plan annually, this amount is deducted from their gross income before taxes are applied. Assuming the employee is in a 25% tax bracket, this deduction would save them $1,250 in taxes annually.

To determine pre-tax deductions, employees need to understand the contribution limits set by the IRS for 401(k) plans. As of 2023, the contribution limit for employees under 50 years old is $22,500, while those 50 and older can contribute an additional $7,500 as a catch-up contribution. It's essential to note that these limits may change over time due to inflation adjustments, so employees should stay informed about any updates.

Employers may also offer matching contributions to their employees' 401(k) plans, which can further enhance the tax-saving benefits. For example, if an employer matches 50% of the employee's contribution up to 6% of their salary, and the employee earns $100,000 and contributes 6% ($6,000), the employer will match $3,000. This additional contribution is also tax-deductible, reducing the employee's taxable income even further.

When calculating pre-tax deductions, it's important to consider other factors that may affect taxable income, such as health insurance premiums, flexible spending accounts (FSAs), and dependent care flexible spending accounts (DCFSAs). These deductions can also reduce taxable income, providing additional tax savings. Employees should review their payroll deductions regularly to ensure they are maximizing their tax-saving opportunities and adjust their contributions as needed to take full advantage of pre-tax deductions.

In summary, understanding pre-tax deductions and how they reduce taxable income is essential for employees looking to optimize their tax savings. By contributing to a 401(k) plan, taking advantage of employer matching contributions, and considering other pre-tax deductions, employees can significantly lower their tax liability and increase their overall financial well-being.

Understanding Payroll Workers' Comp Reports: A Calculation Guide

You may want to see also

Explore related products

![]()

Estimating Tax Savings: Calculate potential tax savings based on contribution amount

To estimate tax savings based on your 401(k) contribution amount, you'll need to understand how these contributions impact your taxable income. Contributions to a traditional 401(k) plan are made pre-tax, which means they reduce your taxable income for the year. This reduction can lead to significant tax savings, depending on your contribution amount and tax bracket.

For example, if you contribute $10,000 to your 401(k) and you're in the 24% tax bracket, you would save $2,400 in taxes for that year. This is because the $10,000 contribution reduces your taxable income by the same amount, and 24% of $10,000 is $2,400.

To calculate your potential tax savings, you can use the following formula:

\[ \text{Tax Savings} = \text{Contribution Amount} \times \text{Tax Rate} \]

Where the tax rate is the percentage of your income that goes towards taxes. You can find your tax rate by referring to the IRS tax brackets for the current year.

Keep in mind that this calculation only provides an estimate of your tax savings. Other factors, such as changes in tax laws, your overall income, and deductions, can affect your actual tax liability. It's always a good idea to consult with a tax professional or use tax preparation software to get a more accurate estimate of your tax savings.

Additionally, it's important to note that while contributing to a 401(k) can provide immediate tax benefits, the primary purpose of these plans is to save for retirement. The tax savings should be viewed as a bonus on top of the long-term investment benefits.

Effortless Payroll Management: Discover the Aren Payroll Calculator

You may want to see also

Explore related products

![]()

Setting Up Automatic Contributions: Arrange for automatic payroll deductions to ensure consistent saving

To set up automatic contributions for your 401(k), you'll need to coordinate with your employer's payroll department. Start by determining the maximum contribution limit for your 401(k) plan, which is typically a percentage of your gross income. For example, if your employer allows you to contribute up to 15% of your salary and you earn $5,000 per month, your maximum monthly contribution would be $750. Decide on a contribution percentage that fits your budget and savings goals, keeping in mind that it's generally advisable to contribute at least enough to take full advantage of any employer match.

Once you've chosen your contribution percentage, fill out the necessary paperwork to authorize automatic payroll deductions. This usually involves completing a 401(k) enrollment form, which you can obtain from your employer's human resources or payroll department. Be sure to specify the exact percentage or dollar amount you wish to contribute each pay period. If your employer offers a Roth 401(k) option, you'll also need to decide whether to make your contributions on a pre-tax or after-tax basis.

After submitting your enrollment form, it may take a few pay cycles for the deductions to begin. Keep an eye on your pay stubs to ensure that the correct amount is being deducted and deposited into your 401(k) account. If you notice any discrepancies, contact your employer's payroll department to resolve the issue.

One of the benefits of setting up automatic contributions is that it helps to ensure consistent saving without the need for manual intervention each pay period. This can be particularly helpful for individuals who may struggle with saving regularly or who want to avoid the temptation to spend their paycheck before saving. By automating your 401(k) contributions, you can build a solid foundation for your retirement savings and make it easier to reach your long-term financial goals.

Understanding Payroll Costs Calculation for PPP Loans

You may want to see also

Frequently asked questions

To calculate your 401(k) payroll deduction, you'll need to decide on a percentage of your gross income that you want to contribute. Many employers suggest contributing at least enough to take full advantage of their matching contribution, if they offer one. You can also consider your financial goals and budget to decide on an appropriate amount.

The IRS sets annual contribution limits for 401(k) plans. As of 2023, the maximum amount you can contribute as an employee is $19,500 per year, or $26,000 if you're age 50 or older and eligible for catch-up contributions. These limits may change over time, so it's a good idea to check the IRS website for the most current information.

Many employers offer a matching contribution to your 401(k) plan, which means they'll contribute a certain percentage of your contributions, up to a specified limit. For example, your employer might match 50% of your contributions up to 6% of your gross income. This is essentially free money, so it's important to contribute enough to take full advantage of the match.

Yes, you can typically change your 401(k) contribution amount at any time during the year. You'll need to contact your employer's payroll department or log in to your 401(k) plan's website to make the change. Keep in mind that any changes you make will only affect future paychecks, so if you want to increase your contributions, it's best to do so as soon as possible.

When you leave your job, you have several options for your 401(k) contributions. You can leave the money in your former employer's plan, roll it over to a new employer's plan, or roll it over to an individual retirement account (IRA). You may also be able to cash out your contributions, but this is generally not recommended as it can result in penalties and taxes. It's important to carefully consider your options and consult with a financial advisor if needed.