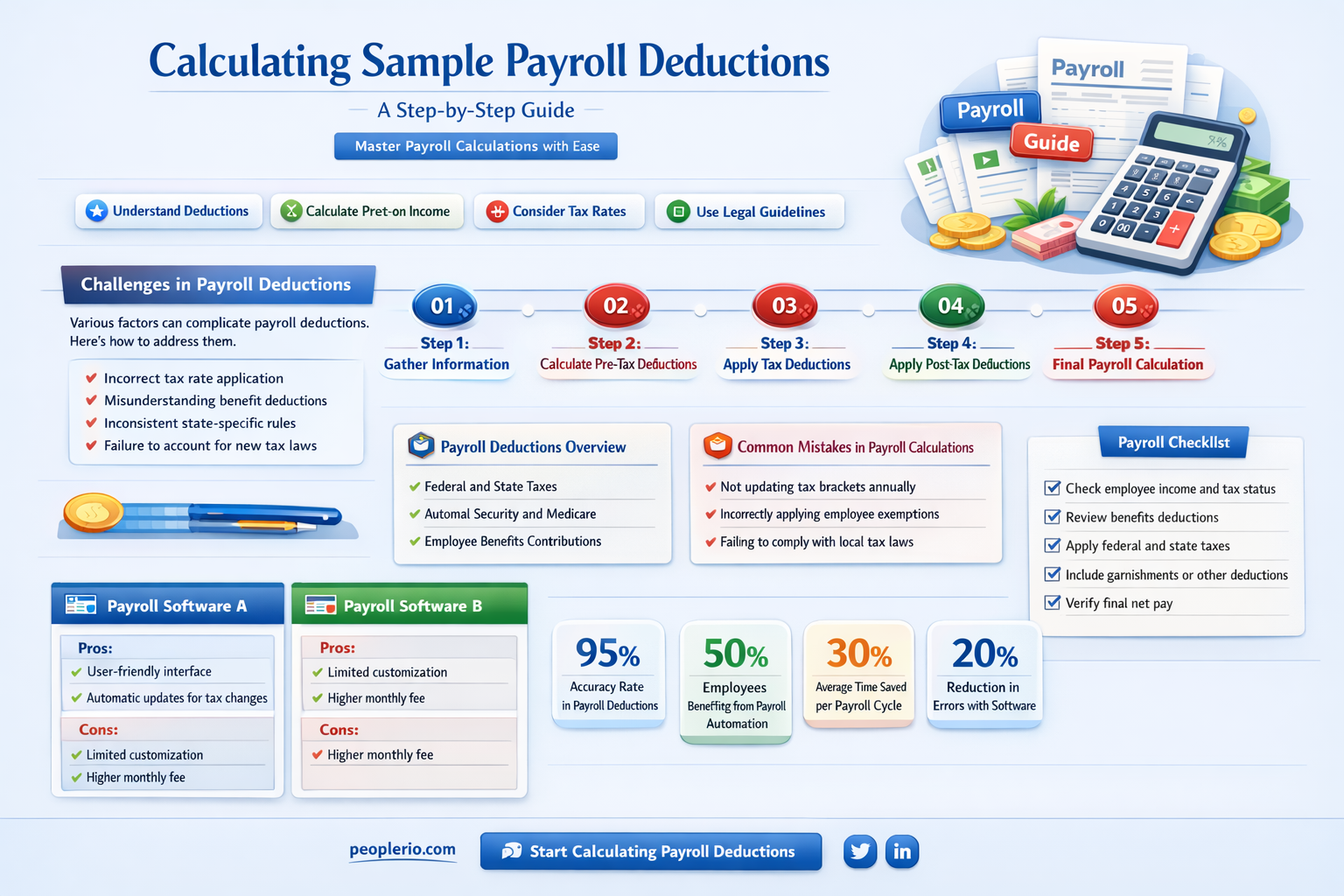

Calculating a sample payroll deduction involves understanding various components of an employee's compensation and the applicable deductions. This process includes identifying the gross pay, which is the total amount earned before deductions, and then subtracting mandatory and voluntary deductions. Mandatory deductions typically include federal, state, and local taxes, as well as Social Security and Medicare contributions. Voluntary deductions might encompass retirement plan contributions, health insurance premiums, and other benefits. To accurately calculate the sample payroll deduction, one must be familiar with the relevant tax rates and deduction limits for the specific jurisdiction and pay period in question. By following a systematic approach and utilizing the appropriate formulas, one can determine the net pay, which is the amount that the employee will receive after all deductions have been made.

| Characteristics | Values |

|---|---|

| Calculation Type | Sample Payroll Deduction |

| Purpose | To estimate the amount to be deducted from an employee's paycheck |

| Required Information | Employee's gross pay, tax withholding rates, other deductions |

| Calculation Steps | 1. Calculate federal income tax withholding, 2. Calculate state income tax withholding, 3. Calculate local income tax withholding, 4. Calculate Social Security tax withholding, 5. Calculate Medicare tax withholding, 6. Subtract all tax withholdings and other deductions from gross pay |

| Tools Needed | Payroll calculator, tax withholding tables, employee's W-4 form |

| Frequency | Typically calculated for each pay period |

| Importance | Ensures accurate payroll processing and compliance with tax laws |

Explore related products

What You'll Learn

- Determine Gross Pay: Calculate the total earnings before any deductions are made

- Identify Deduction Types: Recognize various deduction categories such as taxes, insurance, and retirement

- Calculate Tax Withholdings: Compute the amount to be withheld for federal, state, and local taxes

- Apply Other Deductions: Subtract amounts for health insurance, retirement plans, and other benefits

- Net Pay Calculation: Arrive at the final take-home pay after all deductions have been accounted for

![]()

Determine Gross Pay: Calculate the total earnings before any deductions are made

To determine gross pay, the first step is to identify the employee's pay rate and the number of hours worked during the pay period. This information is typically found on the employee's timesheet or in the payroll system. For salaried employees, the pay rate is usually an annual amount that needs to be divided by the number of pay periods in a year to get the gross pay per period. For hourly employees, the pay rate is multiplied by the number of hours worked to calculate the gross pay.

Once the pay rate and hours worked are known, the next step is to calculate any additional earnings that need to be included in the gross pay. This could include overtime pay, bonuses, commissions, or other types of compensation. Overtime pay is typically calculated at a higher rate than regular pay and is based on the number of hours worked beyond the standard workweek. Bonuses and commissions are usually calculated based on performance or sales targets and are added to the gross pay as a lump sum.

After calculating the base pay and any additional earnings, the total amount is added together to determine the gross pay. This figure represents the employee's total earnings before any deductions are made for taxes, benefits, or other withholdings. It is important to note that gross pay is not the same as net pay, which is the amount the employee takes home after all deductions have been made.

When calculating gross pay, it is essential to be accurate and thorough to ensure that employees are paid correctly. Any errors in the calculation of gross pay can lead to discrepancies in the employee's paycheck and may result in dissatisfaction or even legal issues. Therefore, it is crucial to double-check all calculations and to use reliable payroll software or systems to help streamline the process and reduce the risk of errors.

In summary, determining gross pay involves identifying the employee's pay rate and hours worked, calculating any additional earnings, and adding these amounts together to get the total earnings before deductions. This process requires attention to detail and accuracy to ensure that employees are paid correctly and to avoid any potential issues.

Mastering Payroll: A Step-by-Step Guide to Calculating Salaries

You may want to see also

Explore related products

![]()

Identify Deduction Types: Recognize various deduction categories such as taxes, insurance, and retirement

To accurately calculate payroll deductions, it's essential to first identify the various types of deductions that may apply. Taxes are a primary category, encompassing federal, state, and local income taxes, as well as Social Security and Medicare taxes. Insurance deductions can include health, dental, vision, life, and disability insurance premiums. Retirement deductions typically involve contributions to 401(k), IRA, or pension plans.

When identifying deduction types, it's crucial to consider the specific circumstances of each employee. For instance, an employee's marital status, number of dependents, and state of residence can all impact the amount of taxes withheld. Similarly, the type of insurance coverage an employee elects will determine the corresponding deductions.

To streamline the identification process, employers can utilize payroll deduction tables or calculators provided by the IRS and state tax authorities. These resources can help determine the correct amount of taxes to withhold based on an employee's earnings and personal information. Additionally, employers should maintain open communication with employees to ensure they are aware of any changes in their deduction elections or personal circumstances that may affect their payroll deductions.

In conclusion, accurately identifying deduction types is a critical step in the payroll deduction process. By understanding the various categories of deductions and considering individual employee circumstances, employers can ensure compliance with tax laws and provide accurate paychecks to their employees.

Mastering Payroll: A Guide to Calculating Fringe Benefits for Certified Payroll

You may want to see also

Explore related products

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UY218_.jpg)

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UY218_.jpg)

![]()

Calculate Tax Withholdings: Compute the amount to be withheld for federal, state, and local taxes

To calculate tax withholdings for payroll deductions, you must first understand the different types of taxes that are typically withheld. These include federal income tax, state income tax, and local income tax. The amount withheld for each type of tax will depend on the employee's earnings, tax filing status, and the tax rates applicable to their location.

For federal income tax, the withholding amount is determined by the employee's gross wages and the federal tax withholding tables provided by the Internal Revenue Service (IRS). These tables are updated annually and take into account the employee's filing status (single, married, head of household, etc.) and the number of allowances they have claimed on their W-4 form. To calculate the federal tax withholding, you would look up the employee's gross wages in the appropriate tax table and find the corresponding withholding amount based on their filing status and allowances.

State income tax withholding is similar to federal withholding, but the rates and tables vary by state. Some states have a flat tax rate, while others have progressive tax rates that increase as income levels rise. To calculate state tax withholding, you would need to refer to the tax withholding tables or formulas provided by the state's tax authority.

Local income tax withholding is less common, but some cities and counties impose their own income taxes. The rates and withholding methods for local taxes can vary widely, so it's important to check with the local tax authority for specific instructions.

Once you have calculated the withholding amounts for federal, state, and local taxes, you would subtract these amounts from the employee's gross wages to determine their net pay. It's important to note that tax withholding is an estimate, and the actual taxes owed may differ when the employee files their tax return. Therefore, it's crucial to review and adjust withholding amounts periodically to ensure accuracy and avoid underpayment or overpayment of taxes.

Mastering Payroll with Quicken: A Comprehensive Guide

You may want to see also

Explore related products

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe + State 2022 with Refund Bonus Offer (Amazon Exclusive) [PC Download] (Old Version)](https://m.media-amazon.com/images/I/71L-QsTnZhL._AC_UY218_.jpg)

![(Old Version) H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY218_.jpg)

![H&R Block Tax Software Premium & Business 2022 with Refund Bonus Offer (Amazon Exclusive) [PC Download] (Old Version)](https://m.media-amazon.com/images/I/712wnjKatGL._AC_UY218_.jpg)

![]()

Apply Other Deductions: Subtract amounts for health insurance, retirement plans, and other benefits

To accurately calculate payroll deductions, it's essential to consider various factors beyond just taxes. Health insurance, retirement plans, and other benefits can significantly impact an employee's take-home pay. When processing payroll, employers must subtract these amounts from the gross salary to arrive at the net pay.

Health insurance deductions are typically based on the employee's coverage level and the cost of the plan. Employers may offer multiple health insurance options, each with different premiums and coverage levels. It's crucial to deduct the correct amount based on the employee's plan selection. Additionally, employers may need to consider any flexible spending accounts (FSAs) or health savings accounts (HSAs) that employees have elected to contribute to.

Retirement plan deductions are another important aspect of payroll processing. Employers may offer 401(k), 403(b), or other retirement plans, and employees may choose to contribute a percentage of their salary to these plans. Employers must deduct these contributions from the employee's gross pay and ensure that they are properly invested in the chosen retirement plan.

Other benefits, such as life insurance, disability insurance, and employee assistance programs, may also require deductions from the employee's salary. Employers must carefully review the terms of these benefits and deduct the appropriate amounts from the employee's pay.

When calculating payroll deductions, it's essential to follow a systematic approach to ensure accuracy. Employers should start by determining the employee's gross salary for the pay period, then subtract any pre-tax deductions, such as health insurance and retirement plan contributions. Next, they should calculate and subtract any post-tax deductions, such as garnishments or child support payments. Finally, employers should review the employee's net pay to ensure that all deductions have been properly accounted for.

By carefully considering and accurately subtracting amounts for health insurance, retirement plans, and other benefits, employers can ensure that employees receive the correct net pay and that all payroll deductions are properly processed.

Understanding IRA Calculations in Payroll: A Comprehensive Guide

You may want to see also

Explore related products

![[Old Version] TurboTax Deluxe 2022 Tax Software, Federal and State Tax Return, [Amazon Exclusive] [PC/MAC Download]](https://m.media-amazon.com/images/I/71IgMkror-L._AC_UY218_.jpg)

![[Old Version] TurboTax Home & Business 2022 Tax Software, Federal and State Tax Return, [Amazon Exclusive] [PC/MAC Download]](https://m.media-amazon.com/images/I/71SKL1biC-L._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UY218_.jpg)

![]()

Net Pay Calculation: Arrive at the final take-home pay after all deductions have been accounted for

To calculate the net pay, which is the final take-home pay after all deductions, you must first understand the various components that affect it. The process begins with the gross pay, which is the total amount earned before any deductions. From this, you subtract federal income tax, which is calculated based on the employee's W-4 form and the tax tables provided by the IRS. Next, you deduct Social Security and Medicare taxes, which are typically 6.2% and 1.45% of the gross pay, respectively.

In addition to these federal deductions, you must also account for state and local taxes, which vary depending on the location. Some states have no income tax, while others have rates that can exceed 5%. Local taxes can also include city or county taxes, which are usually a small percentage of the gross pay.

Other deductions that may affect the net pay include health insurance premiums, retirement contributions, and any other voluntary deductions such as life insurance or flexible spending accounts. These deductions are typically subtracted from the gross pay before taxes are calculated, which can lower the taxable income and thus reduce the tax liability.

Once all of these deductions have been accounted for, you can calculate the net pay by subtracting the total deductions from the gross pay. This will give you the final amount that the employee will take home. It's important to note that the net pay can vary significantly depending on the individual's circumstances, such as their tax bracket, number of dependents, and the deductions they have chosen.

To ensure accuracy in calculating the net pay, it's crucial to have a thorough understanding of the tax laws and regulations, as well as the specific deductions that apply to each employee. This can be a complex process, but it's essential for ensuring that employees receive the correct amount of pay and that the company is in compliance with tax laws.

Mastering Off-Cycle Payroll: A Step-by-Step Guide

You may want to see also

Frequently asked questions

The first step is to determine the employee's gross pay for the period.

To calculate total deductions, sum up all individual deductions such as taxes, insurance, and retirement contributions.

Typical deductions include federal and state taxes, Social Security, Medicare, health insurance premiums, and retirement plan contributions.

The amount deducted for federal income tax is determined using the employee's W-4 form, which specifies the number of allowances and any additional withholding requested.

The final step is to subtract the total deductions from the employee's gross pay to arrive at the net pay amount.

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UY218_.jpg)