Calculating the annual insurance premium for payroll deductions involves understanding the various components that contribute to the total cost. This includes the base premium, which is the fixed cost of the insurance policy, as well as any additional charges or fees that may apply. To accurately determine the annual premium, you'll need to consider factors such as the employee's salary, the percentage of the premium that will be deducted from their paycheck, and the frequency of the deductions. Additionally, it's important to be aware of any applicable taxes or regulations that may impact the calculation. By breaking down the process into smaller steps and using the appropriate formulas, you can ensure that the annual insurance premium is calculated correctly and efficiently.

Explore related products

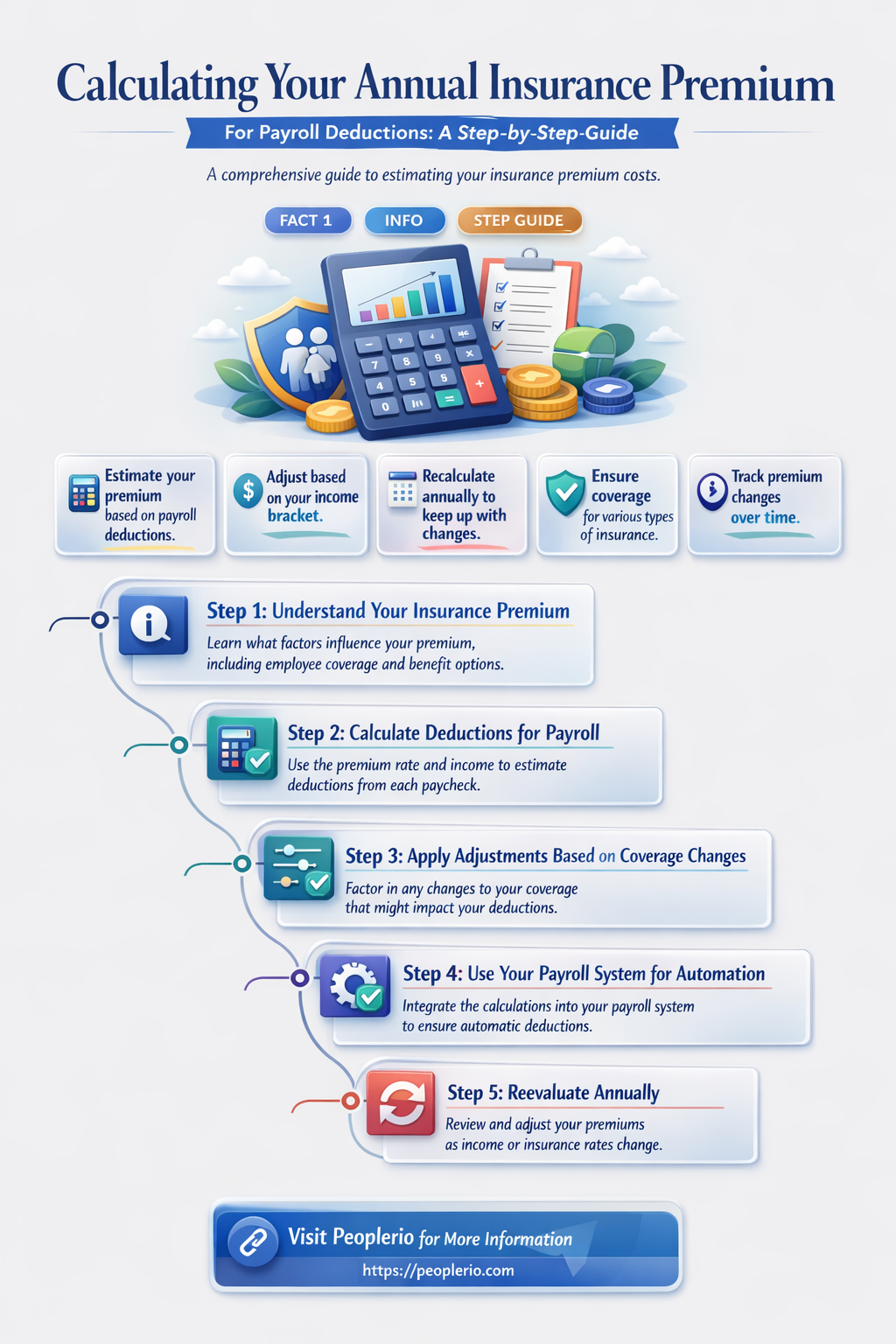

What You'll Learn

- Determine Gross Salary: Calculate the annual gross salary by multiplying the monthly gross salary by 12

- Identify Insurance Types: Recognize the types of insurance to be deducted, such as health, dental, and life insurance

- Calculate Insurance Rates: Find the rates for each insurance type, which may vary based on age, health, and other factors

- Apply Rates to Salary: Multiply the annual gross salary by the rates for each insurance type to find the annual premiums

- Sum Premiums: Add up the annual premiums for all insurance types to get the total annual insurance premium for payroll deductions

![]()

Determine Gross Salary: Calculate the annual gross salary by multiplying the monthly gross salary by 12

To determine the annual gross salary, you must first understand the components that make up the gross salary. Gross salary is the total amount of money an employee earns before any deductions, such as taxes, insurance premiums, and other withholdings, are taken out. It includes the base salary, any bonuses, overtime pay, and other forms of compensation. Once you have identified the monthly gross salary, you can calculate the annual gross salary by multiplying it by 12. This is because there are 12 months in a year, and assuming the employee is paid monthly, the annual gross salary is simply the monthly amount multiplied by the number of months in a year.

For example, if an employee's monthly gross salary is $5,000, the annual gross salary would be $5,000 multiplied by 12, which equals $60,000. This calculation is crucial when determining the annual insurance premium for payroll deductions because the insurance premium is often calculated as a percentage of the employee's gross salary. Therefore, having an accurate annual gross salary figure is essential for calculating the correct insurance premium amount.

It's important to note that if an employee's salary changes during the year, you would need to recalculate the annual gross salary based on the new monthly amount. Additionally, if the employee is not paid monthly, you would need to adjust the calculation accordingly. For instance, if the employee is paid bi-weekly, you would multiply the bi-weekly gross salary by 26 (the number of bi-weekly pay periods in a year) to get the annual gross salary.

In some cases, employees may receive additional compensation that is not included in their regular paychecks, such as bonuses or commissions. These amounts should also be included in the annual gross salary calculation to ensure accuracy. Furthermore, it's essential to consider any changes in the employee's work status, such as promotions, demotions, or changes in work hours, as these can impact the gross salary and, consequently, the insurance premium calculations.

By accurately determining the annual gross salary, you can ensure that the payroll deductions for insurance premiums are calculated correctly, avoiding any potential discrepancies or issues with the employee's insurance coverage. This process requires attention to detail and a thorough understanding of the employee's compensation structure to ensure that all components of the gross salary are accounted for in the calculation.

Understanding California Payroll: A Guide to Calculating PIT

You may want to see also

Explore related products

![]()

Identify Insurance Types: Recognize the types of insurance to be deducted, such as health, dental, and life insurance

To accurately calculate annual insurance premiums for payroll deductions, it's crucial to first identify the types of insurance that will be deducted. This typically includes health insurance, which covers medical expenses; dental insurance, which covers dental care costs; and life insurance, which provides financial protection to beneficiaries in the event of the insured person's death. Each type of insurance has its own premium amount that needs to be considered in the overall calculation.

When identifying the types of insurance, it's important to note the specific coverage details and limitations of each policy. For example, health insurance may have different tiers of coverage, such as bronze, silver, gold, and platinum, each with varying levels of deductibles, copays, and coinsurance. Dental insurance may cover preventive care, basic procedures, and major procedures, but with different annual maximums and waiting periods. Life insurance may come in the form of term life or whole life, with different premium rates and coverage periods.

Once the types of insurance have been identified, the next step is to determine the premium amounts for each. This information can typically be found on the insurance policy documents or by contacting the insurance provider directly. It's important to note any changes in premium rates that may occur due to factors such as age, health status, or changes in coverage levels.

After determining the premium amounts, the final step is to calculate the total annual premium by adding up the premiums for each type of insurance. This total amount can then be divided by the number of pay periods in a year to determine the amount that needs to be deducted from each paycheck.

In summary, identifying the types of insurance to be deducted is a critical first step in calculating annual insurance premiums for payroll deductions. By carefully reviewing the coverage details and premium amounts for health, dental, and life insurance, individuals can ensure that they are accurately calculating their insurance costs and making informed decisions about their coverage options.

Calculating Payroll Minutes: A Quick 20-Minute Guide

You may want to see also

Explore related products

![]()

Calculate Insurance Rates: Find the rates for each insurance type, which may vary based on age, health, and other factors

To calculate insurance rates accurately, it's essential to understand the various factors that influence them. Age is a primary determinant, with younger individuals typically facing lower premiums due to their reduced risk profile. Conversely, older individuals may encounter higher rates as their likelihood of requiring medical attention increases. Health status is another critical factor; individuals with pre-existing conditions or a history of health issues may be subject to higher premiums or even exclusions for certain types of coverage.

In addition to age and health, other factors such as occupation, lifestyle, and geographic location can also impact insurance rates. For instance, individuals working in high-risk occupations may face higher premiums for life insurance, while those living in areas prone to natural disasters might encounter increased rates for property insurance. Understanding these variables is crucial for accurately calculating insurance rates and ensuring that you're adequately covered.

When calculating insurance rates, it's also important to consider the different types of insurance available and how they may vary in cost. For example, term life insurance is generally less expensive than whole life insurance, but it only provides coverage for a specified period. Similarly, health insurance plans with higher deductibles and co-pays may have lower monthly premiums, but they could result in higher out-of-pocket expenses in the event of a medical emergency.

To calculate insurance rates effectively, it's necessary to gather accurate information about the individual or entity being insured. This may include medical records, driving history, credit reports, and other relevant data. Insurance companies use this information to assess risk and determine appropriate premiums. It's also important to shop around and compare rates from different insurance providers, as this can help you find the most affordable and comprehensive coverage options.

In conclusion, calculating insurance rates requires a thorough understanding of the various factors that influence them, including age, health, occupation, lifestyle, and geographic location. By gathering accurate information and comparing rates from different providers, you can ensure that you're getting the best possible coverage at the most affordable price. Remember to review your insurance policies regularly and adjust your coverage as needed to account for changes in your circumstances.

Understanding H1B Payroll Calculations: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Apply Rates to Salary: Multiply the annual gross salary by the rates for each insurance type to find the annual premiums

To calculate the annual insurance premium for payroll deductions, you need to apply the insurance rates to the employee's annual gross salary. This process involves multiplying the salary by the specific rate for each type of insurance. For instance, if an employee's annual gross salary is $50,000 and the health insurance rate is 5%, the annual premium for health insurance would be $2,500 ($50,000 x 0.05).

It's important to note that different types of insurance may have different rates. For example, life insurance rates are typically lower than health insurance rates. Additionally, rates can vary based on factors such as the employee's age, gender, and health status. Employers often provide a breakdown of the rates for each insurance type in the employee benefits package.

When calculating the premiums, ensure that you are using the correct rates for each insurance type. Mistakes in applying the rates can lead to inaccuracies in payroll deductions, which can cause issues for both the employer and the employee. Double-checking the rates and the calculations can help prevent these errors.

In some cases, employers may offer multiple insurance plans with different rates and coverage levels. Employees should carefully review the options and choose the plan that best fits their needs and budget. Once the plan is selected, the employer will use the corresponding rates to calculate the annual premiums.

Finally, it's worth mentioning that annual premiums can be paid in various ways. Some employers may require the premiums to be paid in full at the beginning of the year, while others may allow for monthly or quarterly payments. Understanding the payment schedule is crucial for budgeting and financial planning.

Understanding STRS Payroll Withholding: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Sum Premiums: Add up the annual premiums for all insurance types to get the total annual insurance premium for payroll deductions

To calculate the total annual insurance premium for payroll deductions, you need to sum up the annual premiums for all insurance types. This involves adding together the premiums for health insurance, dental insurance, vision insurance, life insurance, and any other types of insurance that are deducted from employees' paychecks.

The first step in this process is to gather all of the necessary information. This includes the annual premium amounts for each type of insurance, as well as the number of employees who are enrolled in each plan. Once you have this information, you can begin to add up the premiums.

It's important to note that the premiums for different types of insurance may be calculated differently. For example, health insurance premiums may be based on a percentage of the employee's salary, while life insurance premiums may be based on a flat rate. Make sure you understand how each type of premium is calculated before you begin to add them up.

Once you have added up all of the annual premiums, you will have the total annual insurance premium for payroll deductions. This amount can then be divided by the number of pay periods in a year to determine the amount that needs to be deducted from each paycheck.

It's also important to consider any changes that may occur during the year, such as employees enrolling or dropping insurance plans, or changes in premium rates. These changes will need to be accounted for when calculating the total annual insurance premium for payroll deductions.

By following these steps, you can ensure that the total annual insurance premium for payroll deductions is calculated accurately and efficiently. This will help to ensure that employees are paying the correct amount for their insurance coverage, and that the company is able to manage its payroll deductions effectively.

Calculating Hourly Rates for Semi-Monthly Payroll: A Step-by-Step Guide

You may want to see also

Frequently asked questions

To calculate the annual insurance premium for payroll deductions, you need to multiply the employee's annual salary by the insurance premium rate. The formula is: Annual Premium = Annual Salary × Premium Rate.

The premium rate for payroll deductions is typically provided by the insurance company or determined by the employer based on the insurance plan selected. It is usually expressed as a percentage of the employee's salary.

Yes, the annual insurance premium for payroll deductions can change over time due to various factors such as changes in the employee's salary, adjustments in the insurance plan, or modifications in the premium rate by the insurance company.