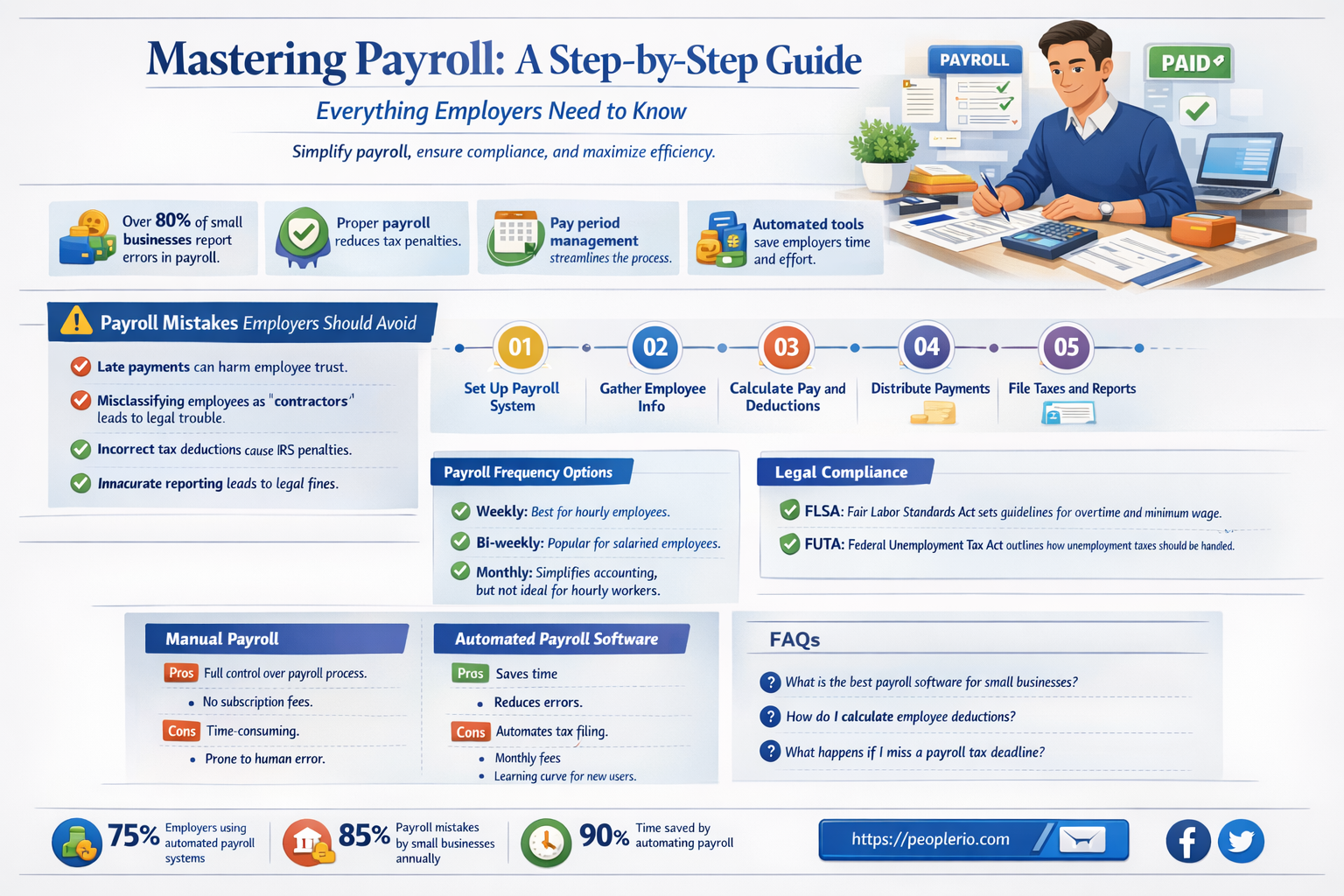

Calculating employee payroll is a critical task for any business, ensuring that workers are compensated accurately and on time. This process involves several key steps: determining the number of hours worked, applying the appropriate hourly rate or salary, accounting for overtime, and deducting necessary taxes and other withholdings. Additionally, payroll calculations must comply with various federal, state, and local regulations, making it essential for employers to stay informed about current laws and standards. By understanding these fundamental aspects, businesses can maintain efficient payroll operations and foster a positive work environment.

Explore related products

$47.82 $62.99

What You'll Learn

- Gross Pay Calculation: Determine the total earnings before deductions, including base salary and overtime pay

- Tax Withholdings: Calculate federal, state, and local income taxes to be withheld from the employee's paycheck

- Social Security and Medicare: Deduct the appropriate amounts for Social Security and Medicare taxes

- Other Deductions: Account for any additional deductions such as health insurance, retirement contributions, or garnishments

- Net Pay Determination: Subtract all deductions from the gross pay to arrive at the employee's take-home pay

![]()

Gross Pay Calculation: Determine the total earnings before deductions, including base salary and overtime pay

To calculate an employee's gross pay, you must first determine their base salary and any additional earnings from overtime work. The base salary is the fixed amount of money an employee receives for their regular work hours, typically expressed as an annual, monthly, or hourly rate. Overtime pay, on the other hand, is the compensation for hours worked beyond the standard workweek, usually calculated at a higher rate than the base salary.

The first step in calculating gross pay is to determine the employee's total hours worked during the pay period. This includes both regular hours and overtime hours. Regular hours are typically the first 40 hours worked in a week, while overtime hours are any hours worked beyond that. It's important to note that some jurisdictions may have different regulations regarding overtime, so it's essential to be familiar with local labor laws.

Once you have the total hours worked, you can calculate the base salary by multiplying the regular hours by the employee's hourly rate. For example, if an employee works 40 hours at an hourly rate of $15, their base salary would be $600 (40 hours x $15 per hour).

Next, you need to calculate the overtime pay. Overtime is usually paid at a higher rate than the base salary, often 1.5 times the regular hourly rate. Using the same example, if the employee works 10 hours of overtime at $15 per hour, their overtime pay would be $225 (10 hours x $15 per hour x 1.5).

Finally, to determine the gross pay, you add the base salary and the overtime pay together. In our example, the gross pay would be $825 ($600 base salary + $225 overtime pay). This amount represents the total earnings before any deductions, such as taxes, social security, or health insurance premiums, are taken out.

It's crucial to accurately calculate gross pay to ensure that employees are fairly compensated for their work. Additionally, proper calculation of gross pay is essential for compliance with tax laws and other regulations. By following these steps and staying informed about local labor laws, you can ensure that your payroll calculations are accurate and up-to-date.

Mastering Payroll Expense Calculations: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Tax Withholdings: Calculate federal, state, and local income taxes to be withheld from the employee's paycheck

To calculate tax withholdings for an employee's paycheck, you must first understand the different types of taxes that are typically withheld. These include federal income tax, state income tax, and local income tax. The amount withheld for each type of tax will depend on the employee's earnings, tax filing status, and the tax rates in effect for the current year.

Federal income tax withholdings are calculated using the employee's gross wages and the federal tax withholding tables provided by the Internal Revenue Service (IRS). The tables are updated annually and take into account the employee's filing status (single, married, head of household, etc.) and the number of allowances claimed on their W-4 form. To calculate the federal income tax withholding, you would first determine the employee's taxable wages by subtracting any pre-tax deductions (such as 401(k) contributions or health insurance premiums) from their gross wages. You would then use the IRS withholding tables to find the amount of tax to withhold based on the employee's taxable wages and filing status.

State income tax withholdings are calculated in a similar manner to federal income tax withholdings, but the rates and tables vary by state. Some states have a flat tax rate, while others have a progressive tax rate that increases as the employee's earnings increase. To calculate the state income tax withholding, you would need to obtain the state tax withholding tables and follow the instructions provided by the state tax authority.

Local income tax withholdings are less common, but some cities and counties impose a local income tax on top of the state and federal taxes. The rates and rules for local income tax withholdings vary widely, so you would need to check with the local tax authority for specific instructions.

Once you have calculated the federal, state, and local income tax withholdings, you would subtract the total amount from the employee's gross wages to determine their net pay. It is important to note that tax withholdings are only an estimate of the employee's tax liability for the year. The actual amount of tax owed may be higher or lower, depending on the employee's total earnings and tax deductions for the year.

Decoding Payroll: How Worker Classification Shapes Your Earnings

You may want to see also

Explore related products

![]()

Social Security and Medicare: Deduct the appropriate amounts for Social Security and Medicare taxes

To calculate employee payroll accurately, it's crucial to deduct the appropriate amounts for Social Security and Medicare taxes. These deductions are mandated by law and play a significant role in funding social security benefits and healthcare for the elderly.

The first step is to determine the employee's gross wages, which include all forms of compensation such as salary, tips, and bonuses. Once you have the gross wages, you can calculate the Social Security tax deduction. As of 2023, the Social Security tax rate is 6.2% for both employees and employers. This means you'll deduct 6.2% of the employee's gross wages for Social Security.

Next, you'll calculate the Medicare tax deduction. The Medicare tax rate is 1.45% for both employees and employers. Therefore, you'll deduct 1.45% of the employee's gross wages for Medicare. It's important to note that there is no wage base limit for Medicare tax, meaning all wages are subject to this tax.

In addition to these standard deductions, there's an additional Medicare tax for high-income earners. If an employee's wages exceed $200,000 in a year, you'll need to deduct an extra 0.9% for Medicare. This additional tax is only paid by the employee, not the employer.

Once you've calculated the deductions, you'll subtract them from the employee's gross wages to determine their net pay. It's essential to keep accurate records of these deductions for both reporting and compliance purposes. The IRS requires employers to report Social Security and Medicare wages and taxes on Form W-2 at the end of each year.

In summary, calculating Social Security and Medicare deductions is a critical part of payroll processing. By following these steps and staying up-to-date with current tax rates and regulations, you can ensure accurate payroll calculations and compliance with federal tax laws.

Florida Payroll Calculation: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![]()

Other Deductions: Account for any additional deductions such as health insurance, retirement contributions, or garnishments

To accurately calculate employee payroll, it's crucial to account for various deductions beyond just taxes. Health insurance premiums, retirement contributions, and garnishments are common examples of additional deductions that can significantly impact an employee's take-home pay. When processing payroll, employers must ensure they're deducting the correct amounts for each of these categories.

Health insurance premiums are typically deducted pre-tax, reducing the employee's taxable income. Employers must verify the premium amounts with the insurance provider and deduct them accordingly. Retirement contributions, such as 401(k) or IRA deductions, are also pre-tax and can vary based on the employee's election or the employer's matching contribution. Garnishments, on the other hand, are post-tax deductions that can include child support, alimony, or creditor payments. Employers must have proper documentation and court orders to process garnishments accurately.

When calculating these deductions, employers should follow a systematic approach. First, determine the employee's gross pay for the period. Next, calculate the pre-tax deductions, such as health insurance and retirement contributions, and subtract them from the gross pay to arrive at the taxable income. Then, calculate the post-tax deductions, like garnishments, and subtract them from the net pay. It's essential to maintain accurate records of all deductions and to communicate any changes or updates to employees promptly.

Failure to account for these additional deductions can lead to errors in payroll processing, resulting in financial discrepancies and potential legal issues. Employers should regularly review and update their payroll systems to ensure compliance with changing regulations and employee elections. By doing so, they can maintain accurate payroll records and provide employees with the correct take-home pay.

Understanding Medicare Payroll Deductions: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Net Pay Determination: Subtract all deductions from the gross pay to arrive at the employee's take-home pay

To determine an employee's net pay, you must subtract all deductions from their gross pay. This is the final step in the payroll calculation process and is crucial for ensuring that employees receive the correct amount of take-home pay. Deductions can include federal and state taxes, social security, Medicare, health insurance premiums, retirement contributions, and any other withholdings required by law or agreed upon by the employee.

The process of subtracting deductions from gross pay can be complex, as it requires careful consideration of each deduction type and its corresponding amount. For example, federal income tax withholdings are calculated based on the employee's income, marital status, and number of dependents, while social security and Medicare taxes are typically withheld at a flat rate. Health insurance premiums and retirement contributions may vary depending on the employee's plan selections and the employer's contribution policies.

To avoid errors in net pay determination, it's essential to have a thorough understanding of the various deduction types and their calculation methods. Employers should also regularly review and update their payroll systems to ensure compliance with changing tax laws and regulations. Additionally, providing employees with clear explanations of their pay stubs can help them understand how their net pay is calculated and identify any potential discrepancies.

In summary, net pay determination is a critical aspect of payroll calculation that requires careful attention to detail and a comprehensive understanding of the various deduction types. By following the proper procedures and staying up-to-date with tax laws and regulations, employers can ensure that their employees receive the correct amount of take-home pay.

Decoding Fed Unemployment Payroll: A Step-by-Step Guide

You may want to see also

Frequently asked questions

The first step in calculating employee payroll is to determine the total hours worked by each employee during the pay period.

To calculate the gross pay for an employee, multiply the total hours worked by the employee's hourly wage or salary.

Deductions from an employee's gross pay typically include federal income tax, Social Security tax, Medicare tax, state income tax (if applicable), and any other voluntary deductions such as retirement contributions or health insurance premiums.

To calculate the net pay for an employee, subtract all deductions from the gross pay.

Accurate payroll calculations are crucial to ensure that employees are paid correctly and on time, to comply with tax laws and regulations, and to maintain accurate financial records for the business.