Calculating hourly payroll is a critical task for businesses to ensure employees are compensated accurately and in compliance with labor laws. It involves multiplying an employee's hourly wage by the number of hours worked during a specific pay period, while also accounting for overtime, deductions, and any applicable taxes. Accurate payroll calculations not only maintain employee trust but also help avoid legal penalties and financial discrepancies. Understanding the process, including tracking hours, applying overtime rules, and withholding taxes, is essential for efficient payroll management.

Explore related products

What You'll Learn

- Gathering Employee Data: Collect hours worked, pay rates, and deductions for accurate payroll calculations

- Overtime Calculation: Determine overtime hours and apply the correct multiplier (e.g., 1.5x) to hourly rates

- Deductions and Taxes: Subtract federal, state, and local taxes, as well as benefits or garnishments

- Gross to Net Pay: Calculate gross wages, apply deductions, and compute the final net pay amount

- Payroll Software Tools: Use payroll software to automate calculations, ensure accuracy, and save time

![]()

Gathering Employee Data: Collect hours worked, pay rates, and deductions for accurate payroll calculations

Accurate payroll calculations hinge on meticulous data collection. At the core of this process are three critical elements: hours worked, pay rates, and deductions. Each piece of information must be gathered with precision to ensure employees are compensated fairly and in compliance with labor laws. Hours worked, for instance, should be tracked to the nearest minute or tenth of an hour, depending on your payroll system’s capabilities. This level of detail prevents underpayment or overpayment, both of which can lead to legal and financial complications.

Pay rates, the second pillar, vary widely depending on employee roles, experience, and contractual agreements. For hourly workers, this includes regular rates, overtime rates (typically 1.5 times the regular rate), and any shift differentials. For example, a retail worker earning $15 per hour might receive $22.50 for each hour of overtime. Ensure these rates are documented in employment contracts and updated regularly to reflect changes such as raises or promotions. Missteps here can erode employee trust and result in costly corrections.

Deductions, often overlooked, are equally vital. These include mandatory withholdings like federal and state taxes, Social Security, and Medicare, as well as voluntary deductions such as retirement contributions or health insurance premiums. For instance, a single employee earning $600 weekly might have $78 withheld for federal taxes, $37 for Social Security, and $8.70 for Medicare, leaving them with a net pay of $476.30. Use IRS Publication 15 and state tax guides to determine accurate withholding amounts, and verify employee elections for voluntary deductions annually.

Practical tips can streamline this process. Implement a time-tracking system that integrates with your payroll software to minimize manual entry errors. For pay rates, create a centralized database accessible to HR and payroll teams. For deductions, provide employees with a checklist during onboarding to confirm their withholding preferences. Regular audits of collected data can catch discrepancies early, ensuring payroll runs smoothly. By treating data collection as a strategic function, not a mere administrative task, you safeguard both your organization’s finances and employee satisfaction.

Mastering Payroll Calculations: A Comprehensive Guide to Accurate Compensation

You may want to see also

Explore related products

![]()

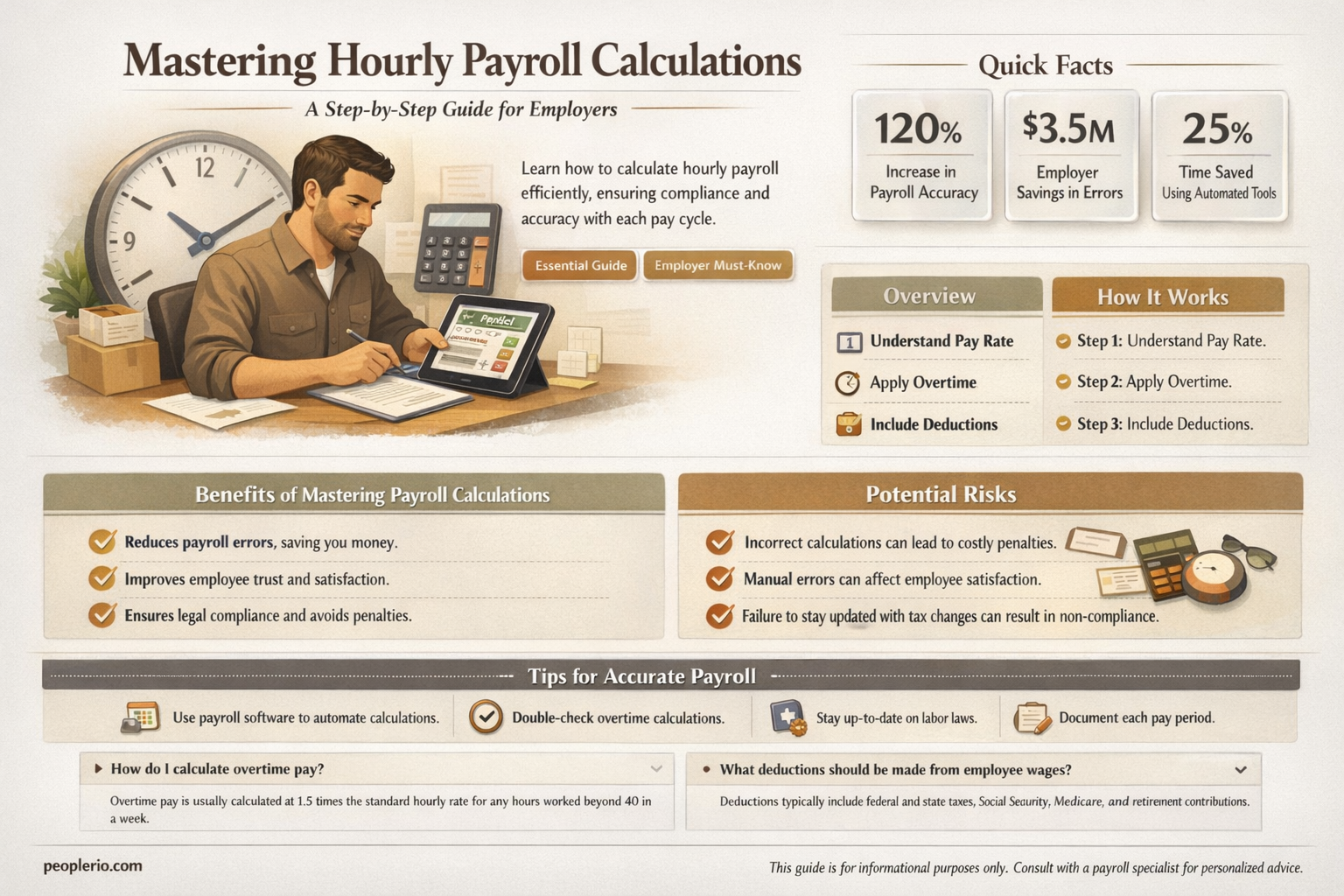

Overtime Calculation: Determine overtime hours and apply the correct multiplier (e.g., 1.5x) to hourly rates

Overtime calculation is a critical component of hourly payroll, ensuring employees are compensated fairly for extra hours worked. To determine overtime hours, start by identifying the standard workweek threshold, typically 40 hours in the United States. Any hours worked beyond this threshold qualify as overtime. For example, if an employee works 47 hours in a week, 7 of those hours are considered overtime. This distinction is essential because overtime hours are paid at a higher rate than regular hours, reflecting the additional effort and time commitment.

Once overtime hours are identified, the next step is to apply the correct multiplier to the employee’s hourly rate. The most common multiplier is 1.5x, meaning overtime pay is one and a half times the regular hourly wage. For instance, if an employee earns $20 per hour, their overtime rate would be $30 per hour. This calculation is straightforward: multiply the regular hourly rate by 1.5. However, some jurisdictions or employment contracts may require a higher multiplier, such as 2x for holidays or specific industries. Always verify the applicable laws or agreements to ensure compliance.

A practical tip for employers is to use payroll software that automates overtime calculations, reducing the risk of errors. Manual calculations can be time-consuming and prone to mistakes, especially in organizations with fluctuating work hours or multiple pay rates. For employees, understanding how overtime is calculated empowers them to verify their paychecks and address discrepancies promptly. For example, if an employee notices their overtime hours were miscalculated, they can reference their timesheet and the agreed-upon rate to correct the issue.

It’s also important to note that overtime rules can vary by state or country. For instance, California requires daily overtime for hours worked beyond 8 in a day, in addition to weekly overtime. In contrast, some countries may have different thresholds or multipliers. Employers operating across multiple regions must stay informed about local labor laws to avoid penalties. Employees should familiarize themselves with these regulations to ensure they receive the compensation they’re entitled to.

In conclusion, mastering overtime calculation is essential for accurate hourly payroll processing. By determining overtime hours correctly and applying the appropriate multiplier, employers can maintain compliance and foster trust with their workforce. Employees, on the other hand, benefit from understanding these calculations to safeguard their earnings. Whether through manual computation or automated tools, precision in overtime pay is non-negotiable for fair and lawful compensation.

Mastering Manual Payroll: Calculating Hours and Minutes Step-by-Step

You may want to see also

Explore related products

![]()

Deductions and Taxes: Subtract federal, state, and local taxes, as well as benefits or garnishments

Federal, state, and local taxes are mandatory deductions from an employee's gross pay, and their rates vary based on location and income level. For instance, federal income tax withholding is determined by the employee's W-4 form, which considers factors like marital status, allowances, and additional withholding amounts. State and local taxes, if applicable, are calculated similarly but with region-specific rates. These deductions are non-negotiable and must be accurately computed to avoid penalties.

In addition to taxes, benefits and garnishments further reduce an employee's net pay. Benefits, such as health insurance or retirement contributions, are often shared costs between the employer and employee. For example, a health insurance premium might be $500 per month, with the employee contributing $200 and the employer covering the remaining $300. Garnishments, on the other hand, are court-ordered deductions for debts like child support or tax liens. These can be a fixed amount or a percentage of disposable earnings, typically capped at 25% for consumer debts.

To calculate these deductions, follow a structured approach. First, determine the employee's gross pay by multiplying their hourly rate by hours worked. Next, apply federal tax withholding using IRS Publication 15 and the employee's W-4. Then, subtract state and local taxes based on regional rates. Afterward, deduct benefit contributions and garnishments as per the agreed-upon amounts or court orders. For example, if an employee earns $600 weekly, has federal tax withholding of $75, state tax of $30, health insurance contribution of $50, and a child support garnishment of $100, their net pay would be $345.

A critical caution is to stay updated on tax laws and regulations, as they frequently change. For instance, tax brackets and standard deductions are adjusted annually for inflation. Additionally, ensure compliance with garnishment limits to avoid over-deducting from an employee's wages. Tools like payroll software can automate these calculations, reducing errors and saving time. However, manual checks are still essential to verify accuracy, especially for complex scenarios involving multiple garnishments or varying tax rates.

In conclusion, mastering deductions and taxes is crucial for accurate hourly payroll calculation. By understanding the nuances of federal, state, and local taxes, as well as benefits and garnishments, employers can ensure compliance and fairness. Practical tips include using reliable payroll software, staying informed about tax updates, and double-checking calculations for employees with unique deduction scenarios. This meticulous approach not only avoids legal issues but also builds trust with employees by ensuring they receive the correct net pay.

Efficient Payroll Calculation: Mastering 45-Minute Time Tracking for Accuracy

You may want to see also

Explore related products

![Paycheck (2003) (BD) [Blu-ray]](https://m.media-amazon.com/images/I/91eumTA2u1L._AC_UY218_.jpg)

![]()

Gross to Net Pay: Calculate gross wages, apply deductions, and compute the final net pay amount

Calculating hourly payroll involves more than just multiplying hours worked by the hourly rate. The journey from gross wages to net pay is a critical process that ensures employees receive their rightful earnings after all necessary deductions. Gross wages represent the total earnings before any deductions, while net pay is the amount the employee actually takes home. Understanding this transformation is essential for both employers and employees to ensure accuracy and compliance with tax laws.

To begin, calculate gross wages by multiplying the employee’s hourly rate by the number of hours worked. For example, if an employee works 40 hours at a rate of $15 per hour, their gross wages would be $600. However, this is just the starting point. Deductions such as federal and state taxes, Social Security, Medicare, and voluntary contributions like retirement plans or health insurance must be applied. Each deduction has specific rules and rates, often based on the employee’s income level, marital status, and allowances claimed on their W-4 form.

Applying deductions requires careful attention to detail. Federal income tax, for instance, is calculated using progressive tax brackets, meaning higher earnings are taxed at higher rates. State taxes vary widely, with some states having no income tax at all. Social Security and Medicare taxes are fixed percentages (6.2% and 1.45%, respectively, as of 2023) applied to gross wages up to certain limits. Voluntary deductions, like 401(k) contributions, are subtracted based on the employee’s elected amount. It’s crucial to use the latest tax tables and guidelines to ensure compliance.

Once all deductions are applied, compute the final net pay by subtracting the total deductions from the gross wages. For example, if an employee has $600 in gross wages and $150 in total deductions, their net pay would be $450. This final amount is what the employee receives in their paycheck. Employers must also keep detailed records of these calculations for tax reporting purposes, such as filing Form 941 for federal taxes and state-specific forms.

In practice, automating this process with payroll software can reduce errors and save time. However, understanding the manual calculation ensures transparency and helps identify discrepancies. For instance, if an employee notices their net pay is lower than expected, reviewing the deductions can reveal whether too much tax was withheld or if a voluntary contribution was incorrectly applied. By mastering the gross-to-net calculation, employers and employees alike can ensure fairness and accuracy in every paycheck.

Efficient Payroll Calculations: Mastering 15-Minute Time Entries for Accuracy

You may want to see also

Explore related products

![]()

Payroll Software Tools: Use payroll software to automate calculations, ensure accuracy, and save time

Calculating hourly payroll manually is prone to errors, especially when factoring in overtime, deductions, and varying tax rates. Payroll software tools eliminate this risk by automating complex calculations, ensuring every paycheck is accurate down to the cent. For instance, if an employee works 45 hours in a week with a base rate of $15 per hour and time-and-a-half for overtime, the software automatically computes the regular pay ($675) and overtime pay ($112.50), totaling $787.50—no manual math required. This precision not only builds trust with employees but also protects your business from costly compliance penalties.

Beyond accuracy, payroll software saves time by streamlining repetitive tasks. Instead of manually entering hours, rates, and deductions into spreadsheets, these tools integrate with time-tracking systems to import data seamlessly. For example, if your team clocks in via a digital platform like Clockify or TSheets, the software pulls the hours directly, reducing data entry time by up to 70%. Additionally, automated tax filings and direct deposit setups free up hours each pay period, allowing you to focus on strategic tasks rather than administrative chores.

The benefits of payroll software extend to scalability and adaptability. Whether you’re managing 10 employees or 1,000, these tools grow with your business, handling multiple pay rates, schedules, and locations effortlessly. For instance, Gusto and QuickBooks Payroll offer tiered pricing plans starting at $40/month for small businesses, with features like unlimited payroll runs, tax filings, and employee self-service portals. Larger enterprises can leverage platforms like ADP or Paychex, which include advanced reporting, benefits administration, and global payroll capabilities.

However, choosing the right payroll software requires careful consideration. Start by evaluating your specific needs—do you require multi-state tax compliance, PTO tracking, or integration with accounting software? Next, compare user reviews and demo the platforms to ensure they’re intuitive for your team. For example, Rippling stands out for its all-in-one HR and payroll solution, while Patriot Software is budget-friendly for startups. Finally, factor in hidden costs like setup fees or per-employee charges to avoid surprises.

In conclusion, payroll software is not just a tool but a strategic investment in efficiency and accuracy. By automating calculations, saving time, and scaling with your business, it transforms payroll from a tedious chore into a seamless process. With the right platform, you can ensure compliance, boost productivity, and focus on what truly matters—growing your business.

Mastering Payroll Time Calculations: A Step-by-Step Guide for Accuracy

You may want to see also

Frequently asked questions

Multiply the employee's hourly rate by the number of hours worked during the pay period. For example, if an employee works 40 hours at $15 per hour, the calculation is 40 * $15 = $600.

Overtime is typically paid at 1.5 times the regular hourly rate for hours worked beyond 40 in a week. For example, if an employee works 45 hours at $20 per hour, calculate overtime as 5 hours * $20 * 1.5 = $150, then add it to the regular pay.

Calculate the pay for each rate separately. For example, if an employee works 20 hours at $12/hour and 10 hours at $18/hour, calculate as (20 * $12) + (10 * $18) = $240 + $180 = $420.

Apply tax rates and deductions based on the employee’s W-4 form and applicable laws. Subtract federal, state, and local taxes, as well as deductions like insurance or retirement contributions, from the gross pay to determine net pay.