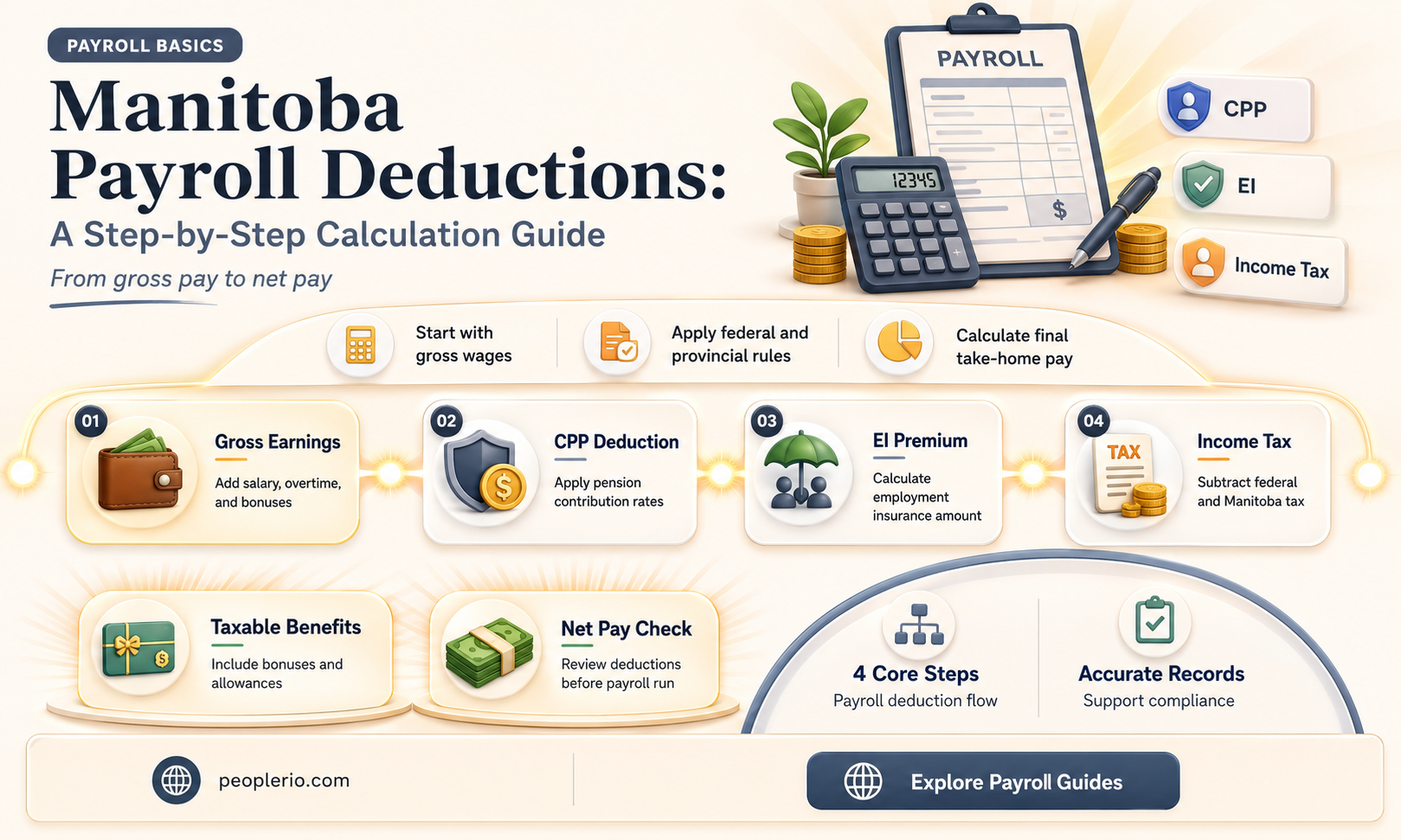

Calculating payroll deductions in Manitoba involves understanding various components that affect an employee's take-home pay. These deductions typically include federal and provincial income taxes, Canada Pension Plan (CPP) contributions, Employment Insurance (EI) premiums, and potentially other deductions such as union dues or garnishments. Employers must accurately calculate these deductions to comply with Canadian tax laws and ensure employees receive the correct net pay. The process involves using the employee's gross earnings, applying the relevant tax rates and contribution percentages, and then subtracting the total deductions from the gross pay to arrive at the net pay. Understanding the nuances of these calculations is crucial for both employers and employees to avoid discrepancies and ensure proper financial planning.

| Characteristics | Values |

|---|---|

| Province | Manitoba |

| Topic | Payroll deductions |

| Calculation | Based on income and deductions |

| Income Types | Salary, wages, commissions, bonuses |

| Deduction Types | Federal income tax, provincial income tax, CPP, EI |

| Tax Rates | Federal: up to 33%, Provincial: up to 17.4% |

| CPP Rate | 5.25% (employee contribution) |

| EI Rate | 1.62% (employee contribution) |

| Thresholds | Basic personal amount: $13,242 (2023) |

| Forms | T4, T4A, T4E, T4RIF, T4RSP, T4SA |

| Filing | Annually by employer |

| Penalties | Late filing: $25 per day, up to $2,500 |

| Resources | Canada Revenue Agency, Manitoba Finance |

| Software | QuickBooks, ADP, Paychex |

| Updates | Annual updates to tax rates and thresholds |

| Compliance | Subject to CRA audits and penalties |

| Record Keeping | Maintain records for 6 years |

Explore related products

What You'll Learn

- Understanding Provincial Tax Rates: Learn about Manitoba's income tax brackets and rates for accurate payroll deductions

- Calculating CPP Contributions: Determine employee and employer Canada Pension Plan contribution rates and amounts

- EI Premiums: Calculate Employment Insurance premiums for both employees and employers based on earnings

- Health and Dental Benefits: Understand how to deduct health and dental benefit premiums from employee wages

- Union Dues and Other Deductions: Learn about deducting union dues, garnishments, and other court-ordered deductions from employee pay

![]()

Understanding Provincial Tax Rates: Learn about Manitoba's income tax brackets and rates for accurate payroll deductions

Manitoba's income tax system is structured into several brackets, each with its own rate. Understanding these brackets and rates is crucial for accurate payroll deductions. The tax rates increase progressively as income rises, ensuring that higher earners contribute a larger percentage of their income towards taxes.

For the 2023 tax year, Manitoba's income tax brackets and rates are as follows:

- 10.8% on the first $37,470 of taxable income

- 12.75% on taxable income between $37,471 and $74,940

- 14.75% on taxable income between $74,941 and $112,410

- 16.75% on taxable income between $112,411 and $149,880

- 17.75% on taxable income between $149,881 and $187,350

- 19.75% on taxable income between $187,351 and $224,820

- 20.75% on taxable income between $224,821 and $262,290

- 21.75% on taxable income between $262,291 and $299,760

- 22.75% on taxable income between $299,761 and $337,230

- 23.75% on taxable income between $337,231 and $374,700

- 24.75% on taxable income between $374,701 and $412,170

- 25.75% on taxable income between $412,171 and $449,640

- 26.75% on taxable income between $449,641 and $487,110

- 27.75% on taxable income between $487,111 and $524,580

- 28.75% on taxable income between $524,581 and $562,050

- 29.75% on taxable income between $562,051 and $599,520

- 30.75% on taxable income between $599,521 and $637,000

- 31.75% on taxable income between $637,001 and $674,470

- 32.75% on taxable income between $674,471 and $711,940

- 33.75% on taxable income between $711,941 and $749,410

- 34.75% on taxable income between $749,411 and $786,880

- 35.75% on taxable income between $786,881 and $824,350

- 36.75% on taxable income between $824,351 and $861,820

- 37.75% on taxable income between $861,821 and $899,290

- 38.75% on taxable income between $899,291 and $936,760

- 39.75% on taxable income between $936,761 and $974,230

- 40.75% on taxable income between $974,231 and $1,011,700

- 41.75% on taxable income between $1,011,701 and $1,049,170

- 42.75% on taxable income between $1,049,171 and $1,086,640

- 43.75% on taxable income between $1,086,641 and $1,124,110

- 44.75% on taxable income between $1,124,111 and $1,161,580

- 45.75% on taxable income between $1,161,581 and $1,199,050

- 46.75% on taxable income between $1,199,051 and $1,236,520

- 47.75% on taxable income between $1,236,521 and $1,274,000

To calculate payroll deductions, employers must first determine the employee's taxable income for the pay period. This includes wages, salaries, commissions, and any other taxable benefits. Once the taxable income is determined, the employer applies the appropriate tax rate based on the income bracket to calculate the tax deduction.

For example, if an employee earns $50,000 annually, their taxable income for a bi-weekly pay period would be approximately $1,923.08 ($50,000 / 26 pay periods). Based on the tax brackets, this income falls within the 12.75% tax rate. Therefore, the tax deduction for this pay period would be $245.19 ($1,923.08 * 0.1275).

It's important to note that these tax rates are subject to change, and employers should always refer to the latest information provided by the Manitoba government to ensure accurate payroll deductions. Additionally, employers must also consider other deductions such as Canada Pension Plan (CPP) contributions, Employment Insurance (EI) premiums, and any other applicable deductions when calculating total payroll deductions.

Decoding Payroll: The Simple Guide to Gross from Net

You may want to see also

Explore related products

![]()

Calculating CPP Contributions: Determine employee and employer Canada Pension Plan contribution rates and amounts

To calculate CPP contributions, you need to determine the contribution rates for both employees and employers. As of 2023, the employee contribution rate is 5.25% of gross earnings, while the employer contribution rate is 5.25% of the employee's gross earnings. These rates are subject to change, so it's essential to check the latest rates with the Canada Revenue Agency (CRA).

Once you have the contribution rates, you can calculate the CPP contribution amounts. For example, if an employee earns $50,000 per year, their CPP contribution would be $50,000 x 5.25% = $2,625. The employer's CPP contribution would also be $2,625.

It's important to note that CPP contributions are only required on earnings up to the CPP contribution limit. For 2023, the CPP contribution limit is $61,500. If an employee earns more than this amount, their CPP contributions will be capped at $61,500.

When calculating CPP contributions, it's also important to consider any CPP contribution exemptions that may apply. For example, if an employee is a member of a pension plan that is exempt from CPP, they may not be required to make CPP contributions.

In summary, calculating CPP contributions involves determining the contribution rates, calculating the contribution amounts based on gross earnings, and considering any CPP contribution exemptions that may apply. By following these steps, you can ensure that you are accurately calculating CPP contributions for your employees.

Decoding Payroll: A Simple Guide to Calculating Your Hourly Rate

You may want to see also

Explore related products

$6.54 $7.99

![]()

EI Premiums: Calculate Employment Insurance premiums for both employees and employers based on earnings

To calculate Employment Insurance (EI) premiums for both employees and employers in Manitoba, you need to follow specific guidelines set by the federal government. The first step is to determine the employee's insurable earnings, which are generally the total wages, salaries, and commissions earned during the pay period, up to a maximum annual limit. For 2023, the maximum insurable earnings are $56,300.

Once you have the insurable earnings, you can calculate the EI premiums. The employee's premium rate is 1.62% of their insurable earnings, while the employer's premium rate is 1.4 times the employee's rate, which equates to 2.27%. These rates are subject to change, so it's essential to check the latest rates on the Government of Canada's website.

Let's use an example to illustrate the calculation. Suppose an employee earns $1,000 in a pay period. The employee's EI premium would be $1,000 x 1.62% = $16.20. The employer's EI premium would be $1,000 x 2.27% = $22.70.

It's important to note that EI premiums are typically deducted from the employee's gross pay and remitted to the Canada Revenue Agency (CRA) by the employer. Employers must also pay their portion of the EI premiums. These premiums contribute to the EI program, which provides financial assistance to eligible workers who lose their jobs or need to take time off work due to illness, pregnancy, or other reasons.

In addition to EI premiums, employers in Manitoba must also deduct other payroll taxes, such as Canada Pension Plan (CPP) contributions and income tax. It's crucial to stay up-to-date with the latest payroll tax rates and regulations to ensure compliance and avoid penalties.

Calculating Average Payroll for PPP Round 2: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Health and Dental Benefits: Understand how to deduct health and dental benefit premiums from employee wages

To accurately deduct health and dental benefit premiums from employee wages in Manitoba, employers must first ensure they are complying with the province's specific regulations and standards. This includes understanding the tax implications and any applicable provincial laws that govern such deductions. Employers should consult the Manitoba Labour Board or a professional payroll service to confirm the correct procedures.

Once compliance is confirmed, the next step is to calculate the total premium cost for each employee. This will typically involve adding together the premiums for health and dental coverage, which may vary depending on the employee's plan and coverage level. Employers should provide employees with a detailed breakdown of these costs to ensure transparency and understanding.

After calculating the total premium cost, employers must then determine the appropriate deduction frequency. In most cases, health and dental benefit premiums are deducted on a bi-weekly or monthly basis, coinciding with the employee's pay schedule. Employers should clearly communicate the deduction schedule to employees to avoid any confusion or disputes.

When making the deductions, employers must ensure they are using the correct formula and calculations. This may involve using a percentage-based deduction or a fixed dollar amount, depending on the employee's plan and the employer's policies. Employers should double-check their calculations to avoid any errors or discrepancies.

Finally, employers must maintain accurate records of all health and dental benefit premium deductions. This includes keeping track of the total amount deducted, the deduction frequency, and any changes to the employee's plan or coverage level. These records will be essential for both compliance purposes and for resolving any potential disputes or inquiries from employees.

By following these steps and maintaining accurate records, employers can ensure they are properly deducting health and dental benefit premiums from employee wages in Manitoba. This will help to maintain compliance with provincial regulations and promote transparency and understanding between employers and employees.

Illinois Payroll Deductions: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![]()

Union Dues and Other Deductions: Learn about deducting union dues, garnishments, and other court-ordered deductions from employee pay

Union dues are a common payroll deduction in Manitoba, and employers must understand their obligations when it comes to withholding these amounts. In this province, union dues are typically deducted pre-tax from an employee's gross pay, which means they are not subject to income tax, CPP, or EI deductions. Employers must ensure they are deducting the correct amount as specified by the union and the employee's collective agreement. Failure to do so could result in penalties or legal action.

Garnishments are another type of court-ordered deduction that employers in Manitoba may need to process. These are typically used to satisfy debts or financial obligations that an employee has not met voluntarily. Employers must receive a garnishment order from the court before they can begin deducting the specified amount from the employee's pay. It's important to note that garnishments can only be used for certain types of debts, such as unpaid child support or tax arrears. Employers should consult with legal counsel if they are unsure about their obligations regarding garnishments.

Other court-ordered deductions may include alimony or spousal support payments, which are also deducted pre-tax from an employee's gross pay. Employers must ensure they are following the terms of the court order and deducting the correct amount. In some cases, employers may need to prioritize certain deductions over others, depending on the specific circumstances and legal requirements.

When processing payroll deductions in Manitoba, employers must also be aware of the province's Employment Standards Code, which outlines the rules and regulations surrounding wage deductions. Employers should familiarize themselves with these regulations to ensure they are compliant and avoid any potential legal issues. Additionally, employers should maintain clear and accurate records of all deductions made, including the amounts and dates, to facilitate transparency and accountability.

In conclusion, understanding and processing union dues, garnishments, and other court-ordered deductions is a critical aspect of payroll management in Manitoba. Employers must stay informed about their obligations and ensure they are following the correct procedures to avoid penalties and legal complications. By prioritizing accuracy and compliance, employers can maintain a smooth and efficient payroll process while upholding their responsibilities to their employees and the law.

Understanding Payroll Deductions in Jamaica: A Comprehensive Guide

You may want to see also

Frequently asked questions

Payroll deductions in Manitoba typically include federal and provincial income taxes, Canada Pension Plan (CPP) contributions, Employment Insurance (EI) premiums, and health insurance premiums.

To calculate CPP contributions in Manitoba, you need to multiply the employee's gross earnings by the CPP contribution rate, which is 5.1% for 2023. The maximum annual CPP contribution for 2023 is $3,720.00.

Employers in Manitoba must remit payroll deductions to the Canada Revenue Agency (CRA) on a regular basis, typically monthly or quarterly. This can be done online through the CRA's My Business Account service or by mail using Form PD7A.