The question of whether the employee paid portion of health insurance is taxable is a common concern for both employees and employers. In general, the portion of health insurance premiums paid by an employee is not considered taxable income. This is because health insurance is typically viewed as a tax-free benefit provided by the employer. However, there are certain situations where the employee's contribution might be subject to taxation, such as if the employee is paying for additional coverage beyond what the employer provides or if the employee is paying for health insurance through a cafeteria plan. It's important for employees to understand the specifics of their health insurance plan and how it impacts their taxes. Employers should also be aware of the tax implications of health insurance contributions to ensure compliance with tax laws and regulations.

Explore related products

$13.11 $19.95

What You'll Learn

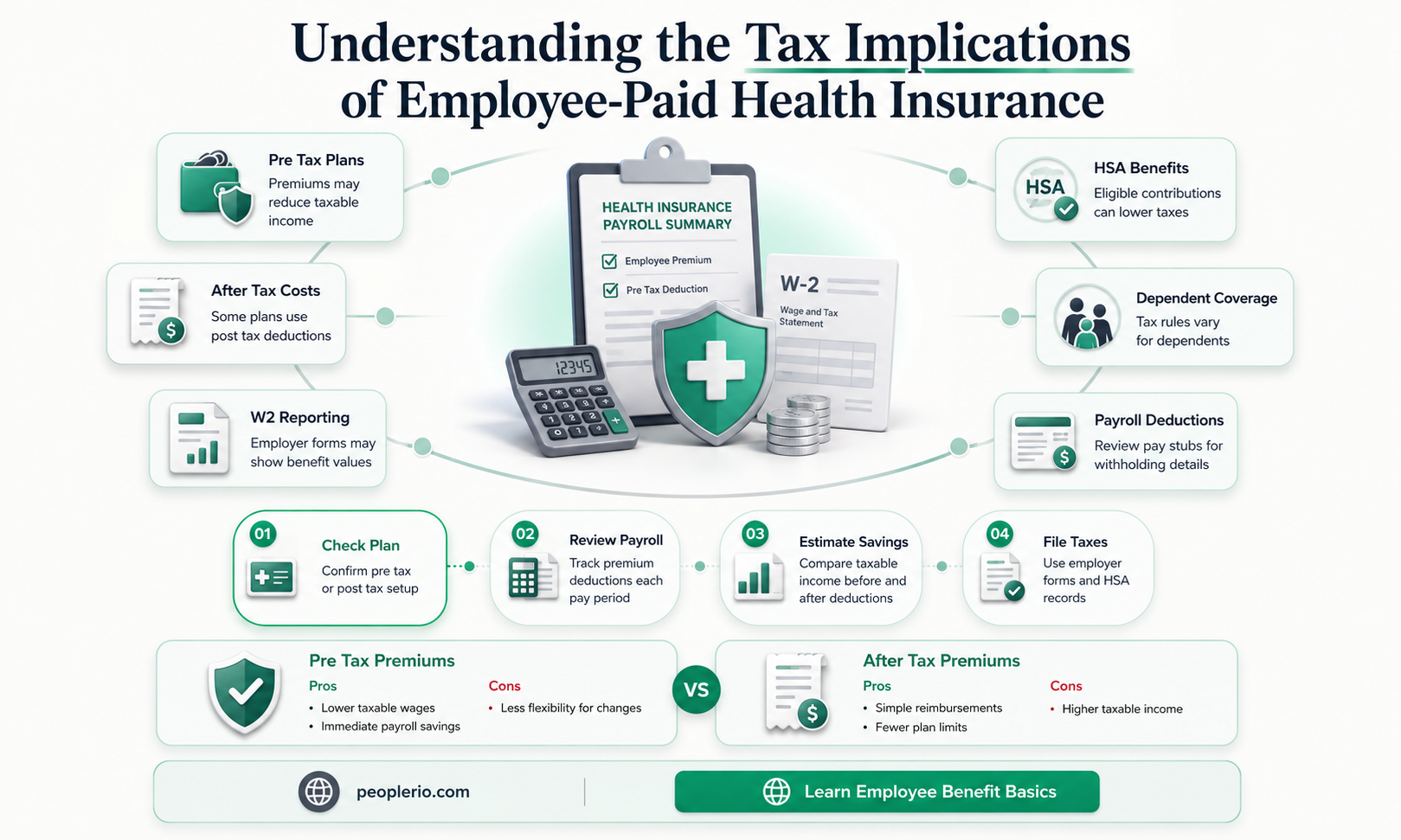

- General Rule: Employee contributions to health insurance are typically tax-deductible, reducing taxable income

- Exceptions: Certain situations, like high-value plans or non-qualified plans, may result in taxable benefits

- Affordable Care Act: ACA-compliant plans usually allow tax-free employee contributions, promoting affordability

- Tax Forms: Employees should check forms like W-2 and 1040 to ensure correct reporting of health insurance contributions

- Consult a Professional: For complex situations, consulting a tax advisor or accountant is recommended to ensure compliance

![]()

General Rule: Employee contributions to health insurance are typically tax-deductible, reducing taxable income

Employee contributions to health insurance are generally considered tax-deductible expenses. This means that the amount an employee pays towards their health insurance premiums can be subtracted from their gross income, reducing the total amount of income that is subject to taxation. This deduction can provide significant tax savings, especially for individuals in higher tax brackets.

To qualify for this deduction, the health insurance plan must meet certain criteria. Typically, the plan must be a qualified health plan under the Affordable Care Act (ACA), and the employee must not be eligible for other health coverage, such as through a spouse or parent. Additionally, the deduction is only available for the portion of the premium that the employee pays out-of-pocket; employer contributions are not tax-deductible.

The process of claiming this deduction can vary depending on the individual's tax situation. For some, it may be as simple as entering the total amount of their health insurance premiums on their tax return. However, for others, especially those who are self-employed or have complex tax situations, it may be necessary to itemize deductions or use specific tax forms to claim the deduction.

One important consideration is the impact of this deduction on other tax credits and benefits. For example, if an individual claims the health insurance premium deduction, they may not be eligible for the premium tax credit, which is a separate tax benefit available to those who purchase health insurance through the ACA marketplace. Therefore, it is important to carefully evaluate all available tax benefits and choose the option that provides the greatest overall tax savings.

In conclusion, the general rule that employee contributions to health insurance are tax-deductible can provide significant tax savings for many individuals. However, it is important to understand the specific criteria and requirements for claiming this deduction, as well as the potential impact on other tax benefits. By carefully evaluating all available options, individuals can maximize their tax savings and ensure compliance with tax laws.

Nurturing Workforce Wellness: Strategies for Optimal Employee Health

You may want to see also

Explore related products

![]()

Exceptions: Certain situations, like high-value plans or non-qualified plans, may result in taxable benefits

In the realm of health insurance taxation, exceptions play a crucial role in determining whether the employee-paid portion of health insurance is taxable. High-value plans, for instance, are a significant exception. According to the Affordable Care Act (ACA), a high-value plan is one that has an annual premium cost exceeding a certain threshold, which is adjusted annually for inflation. For 2024, the threshold is set at $10,200 for individual coverage and $27,500 for family coverage. When an employer-sponsored health plan surpasses these limits, the portion of the premium paid by the employee becomes taxable.

Another notable exception is non-qualified plans. These plans do not meet the requirements set forth by the ACA and, as a result, do not enjoy the same tax benefits as qualified plans. Non-qualified plans can include certain types of health reimbursement arrangements (HRAs) or health savings accounts (HSAs) that are not properly structured or do not comply with ACA regulations. In such cases, the employee's contributions to these plans may be considered taxable income.

It is also important to consider the impact of these exceptions on the overall tax landscape. For employees, understanding these exceptions can help them make informed decisions about their health insurance choices and potential tax liabilities. Employers, on the other hand, must navigate these exceptions carefully to ensure compliance with tax laws and to provide the most beneficial health insurance options to their employees.

To illustrate these exceptions in practice, consider the following scenario: An employer offers a health insurance plan with an annual premium of $12,000 for individual coverage. Since this exceeds the 2024 threshold of $10,200, the portion of the premium paid by the employee would be taxable. However, if the employer were to offer a qualified HSA that meets ACA requirements, the employee's contributions to this HSA would be tax-free, providing a more favorable tax outcome.

In conclusion, exceptions such as high-value plans and non-qualified plans can significantly impact the taxability of the employee-paid portion of health insurance. By understanding these exceptions and their implications, both employees and employers can make more informed decisions regarding health insurance and tax planning.

Nurturing Workforce Well-being: A Guide to Employee Health and Wellness

You may want to see also

Explore related products

![]()

Affordable Care Act: ACA-compliant plans usually allow tax-free employee contributions, promoting affordability

Under the Affordable Care Act (ACA), one of the key provisions aimed at increasing the accessibility of health insurance is the allowance of tax-free employee contributions. This means that when employees contribute to their health insurance premiums, these contributions are often excluded from their taxable income. This exclusion can significantly reduce the overall cost of health insurance for employees, making it more affordable and encouraging higher participation rates in employer-sponsored health plans.

To understand how this works, it's important to note that the ACA sets certain standards for health insurance plans. Plans that meet these standards are considered ACA-compliant. One of the requirements for compliance is that the plan must allow for tax-free contributions from employees. This is typically achieved through mechanisms such as pre-tax deductions from an employee's paycheck, which are then used to pay for health insurance premiums.

The benefit of tax-free contributions is twofold. First, it reduces the immediate financial burden on employees by lowering their taxable income. This can result in lower federal and state income taxes, leaving more money in the employee's pocket. Second, it incentivizes employers to offer health insurance plans that are ACA-compliant, as these plans are more attractive to employees due to the tax advantages.

For example, consider an employee who earns $50,000 per year and contributes $5,000 annually to their health insurance premiums. If these contributions are tax-free, the employee's taxable income would be $45,000 instead of $50,000. Depending on their tax bracket, this could result in significant tax savings.

It's also worth noting that the ACA's emphasis on tax-free contributions aligns with its broader goal of expanding health insurance coverage. By making health insurance more affordable, the ACA aims to reduce the number of uninsured individuals and improve overall public health outcomes.

In summary, the ACA's provision for tax-free employee contributions to health insurance premiums is a critical component of its strategy to promote affordability and accessibility. This provision not only benefits employees by reducing their tax burden but also encourages employers to offer ACA-compliant plans, ultimately contributing to the expansion of health insurance coverage.

Unlocking Educational Opportunities: Advent Health's Tuition Reimbursement Program

You may want to see also

Explore related products

![]()

Tax Forms: Employees should check forms like W-2 and 1040 to ensure correct reporting of health insurance contributions

Employees should diligently review their W-2 and 1040 tax forms to verify the accurate reporting of their health insurance contributions. This is crucial because any discrepancies can impact their tax liability and potential refunds. The W-2 form, provided by the employer, details the employee's earnings and the amounts withheld for taxes, including health insurance premiums. The 1040 form, filed by the employee with the IRS, reports their income and deductions, including health insurance contributions. By cross-referencing these forms, employees can ensure that their health insurance payments are correctly accounted for and potentially reduce their taxable income.

Analyzing the W-2 form, employees should focus on Box 1, which shows their total earnings, and Box 6, which indicates the amount withheld for health insurance. They should then compare these figures with their actual health insurance payments to identify any inconsistencies. If the employer has over- or under-reported the health insurance contributions, the employee may need to adjust their 1040 form accordingly. This involves reporting the correct amount on Line 25 of the 1040, which is designated for health insurance premiums.

Furthermore, employees should be aware of the tax implications of their health insurance contributions. Generally, the employee paid portion of health insurance is not taxable, as it is considered a tax-deductible expense. However, if the employer provides a health insurance premium reimbursement arrangement (HRA), the reimbursed amounts may be taxable. In such cases, employees should consult with a tax professional to understand the specific tax consequences and ensure proper reporting on their 1040 form.

To avoid common mistakes, employees should keep detailed records of their health insurance payments and any related communications with their employer or insurance provider. This documentation can be invaluable in case of an IRS audit or if there are discrepancies between the W-2 and 1040 forms. Additionally, employees should stay informed about changes in tax laws and regulations that may affect the reporting of health insurance contributions, as these can vary from year to year.

In conclusion, by carefully reviewing their W-2 and 1040 tax forms and understanding the tax implications of their health insurance contributions, employees can ensure accurate reporting and potentially reduce their tax liability. This proactive approach not only helps in avoiding penalties but also maximizes their potential tax savings.

Accessing Your Immunization Records as an Orlando Health Employee

You may want to see also

Explore related products

![]()

Consult a Professional: For complex situations, consulting a tax advisor or accountant is recommended to ensure compliance

Navigating the complexities of health insurance taxation can be a daunting task for employees and employers alike. While some aspects may seem straightforward, such as the tax-free status of employer-provided health insurance premiums, the nuances can quickly become overwhelming. This is particularly true when dealing with situations that involve multiple factors, such as varying state laws, different types of health plans, or unique employment arrangements.

In such cases, it is highly recommended to consult a tax advisor or accountant to ensure compliance with all applicable tax laws and regulations. These professionals have the expertise and experience to analyze complex situations, identify potential issues, and provide tailored guidance to minimize tax liabilities and avoid penalties.

For instance, consider an employee who works for a company that offers a high-deductible health plan (HDHP) and contributes to a health savings account (HSA). While the employer's contributions to the HSA are generally tax-free, there may be implications if the employee also has other health coverage or if the HSA is not properly administered. A tax advisor can help navigate these intricacies and ensure that the employee is taking full advantage of the tax benefits available to them.

Similarly, employers may need to consult a professional to ensure that they are correctly reporting and withholding taxes on employee health insurance premiums. This is especially important for companies that operate in multiple states or have employees with complex employment arrangements, such as those who work remotely or are classified as independent contractors.

Ultimately, the cost of consulting a tax professional is often outweighed by the potential savings and peace of mind that come with knowing that all tax obligations are being met. By seeking expert guidance, employees and employers can avoid costly mistakes and ensure that they are making the most of the tax benefits available to them.

California Workers' Health Insurance: Legal Requirements and Options

You may want to see also

Frequently asked questions

Generally, the employee paid portion of health insurance is not taxable. This is because it is considered a tax-free benefit provided by the employer.

If the employee is paying for additional coverage, such as dental or vision insurance, out of their own pocket, then this amount is typically taxable as it is not considered a tax-free benefit.

Yes, there are some exceptions. For example, if the employee is a highly compensated individual, the value of the health insurance benefit may be taxable under certain circumstances.

The taxability of health insurance benefits is typically reported on an employee's W-2 form. The employer will provide this form to the employee at the end of the year, and it will show the total value of the health insurance benefits provided, as well as any amounts that are taxable.