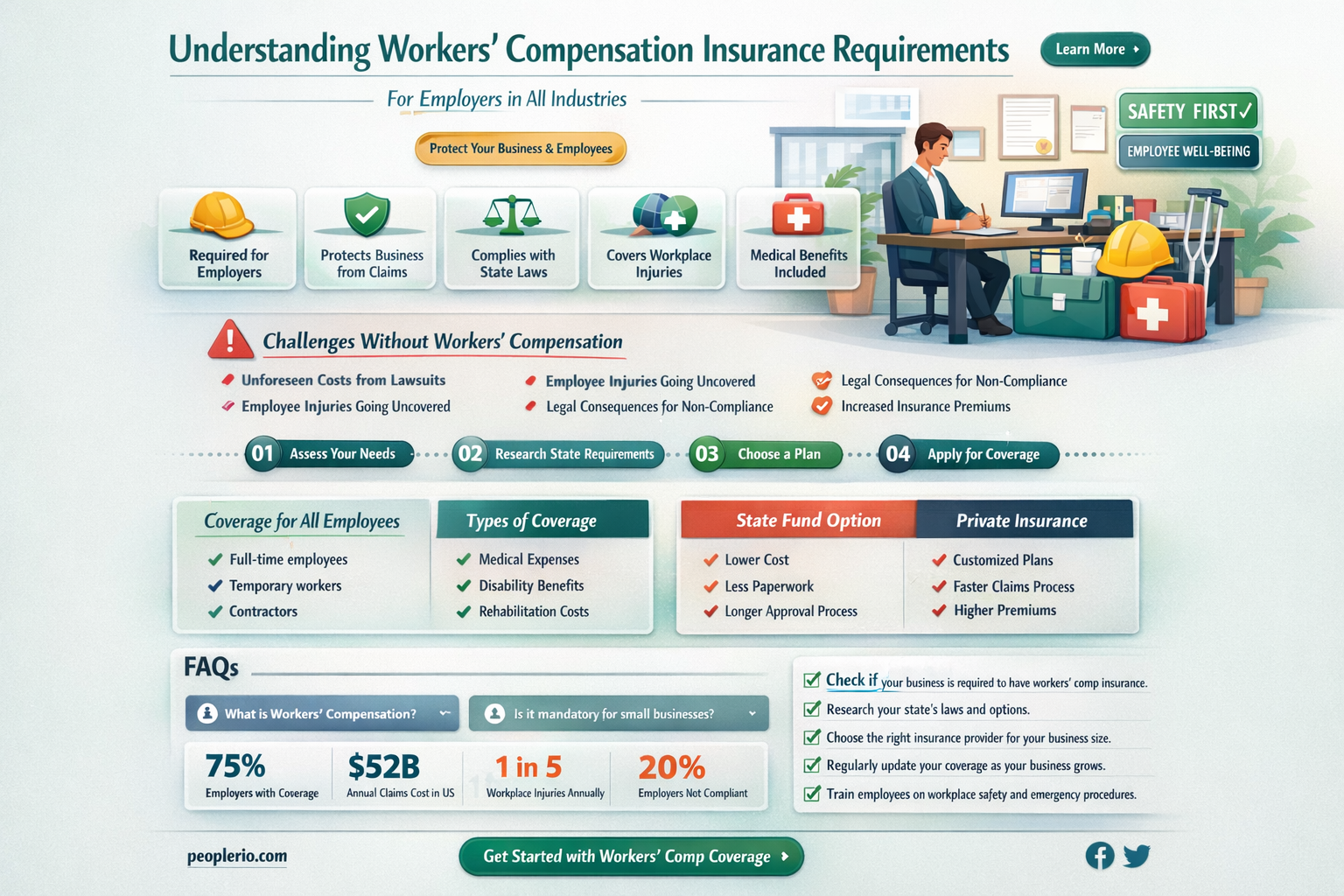

Workers' compensation insurance is a crucial aspect of business operations that provides financial protection to employees who suffer work-related injuries or illnesses. Understanding when this insurance is required is essential for business owners and managers to ensure compliance with legal obligations and to safeguard the well-being of their workforce. Generally, workers' compensation insurance is mandated by state laws and the specific requirements can vary depending on the jurisdiction. In most cases, it is required for businesses that have a certain number of employees, although this threshold can differ from state to state. Additionally, certain high-risk industries may be required to carry this insurance regardless of the number of employees. It is important for business owners to familiarize themselves with the laws and regulations in their state to determine if workers' compensation insurance is necessary for their operations.

| Characteristics | Values |

|---|---|

| Type of Business | Businesses with employees |

| Industry | All industries, though requirements may vary by state |

| Number of Employees | Typically required for businesses with a certain number of employees, which varies by state (commonly 3-5 employees) |

| Coverage | Medical expenses, lost wages, rehabilitation costs, and death benefits for work-related injuries or illnesses |

| Legal Requirement | Mandated by state laws, with specific requirements differing by jurisdiction |

| Exemptions | Some states may exempt certain types of businesses or employees, such as independent contractors or those in specific industries |

| Premiums | Premiums are typically paid by the employer and are based on factors such as the number of employees, industry, and claims history |

| Reporting Requirements | Employers are required to report work-related injuries and illnesses to the insurance provider and relevant state agencies |

| Compliance | Failure to maintain workers' compensation insurance can result in legal penalties and fines |

Explore related products

What You'll Learn

- Employee Eligibility: Understand who qualifies as an employee under workers' compensation laws

- Types of Coverage: Explore different types of workers' compensation insurance policies available

- State Requirements: Learn about specific state mandates regarding workers' compensation insurance

- Exemptions: Discover which employers might be exempt from carrying workers' compensation insurance

- Penalties for Non-Compliance: Understand the consequences of not having required workers' compensation insurance

![]()

Employee Eligibility: Understand who qualifies as an employee under workers' compensation laws

To determine employee eligibility for workers' compensation, it's crucial to understand the legal definitions and criteria. Generally, an employee is considered eligible if they are hired for a specific job, work on a regular basis, and receive payment for their services. This includes full-time, part-time, and seasonal workers. However, independent contractors, volunteers, and certain types of gig workers may not be eligible for workers' compensation benefits.

One key factor in determining eligibility is the level of control the employer has over the worker's job duties and schedule. If the employer has significant control over the worker's tasks, hours, and work environment, the worker is more likely to be considered an employee. On the other hand, if the worker has more autonomy and freedom to choose their own projects and work schedule, they may be classified as an independent contractor.

Another important consideration is the nature of the work being performed. Workers who perform manual labor or work in hazardous conditions are typically more likely to be eligible for workers' compensation benefits. This is because these types of jobs carry a higher risk of injury or illness, and workers' compensation is designed to provide financial protection in such cases.

It's also worth noting that some states have specific laws and regulations regarding employee eligibility for workers' compensation. For example, some states may require employers to provide workers' compensation coverage for all employees, regardless of their classification. In other states, employers may have more flexibility in determining which workers are eligible for coverage.

In conclusion, understanding employee eligibility for workers' compensation is essential for both employers and employees. By knowing the legal definitions and criteria, employers can ensure they are providing the necessary coverage for their workers, while employees can be aware of their rights and benefits under the law.

Understanding Workers' Compensation Insurance Premiums: Who's Responsible?

You may want to see also

Explore related products

![]()

Types of Coverage: Explore different types of workers' compensation insurance policies available

Workers' compensation insurance is a critical component of risk management for businesses, providing financial protection against work-related injuries or illnesses. Understanding the different types of coverage available is essential for employers to ensure they have the appropriate policy in place. This section will delve into the various workers' compensation insurance policies, highlighting their unique features and benefits.

One common type of workers' compensation insurance is the Guaranteed Cost program. This policy provides a fixed premium for the duration of the policy term, typically one year. The insurer assumes the risk of fluctuating claim costs, which can be beneficial for employers looking for predictable budgeting. However, this type of policy may not offer much flexibility in terms of premium adjustments based on actual claim experience.

Another option is the Retrospective Rating program, which allows for premium adjustments based on the actual loss experience of the insured. This can be advantageous for employers with a strong safety record, as they may be able to secure lower premiums over time. However, it also means that employers with higher claim frequencies could face increased premiums, making it a more variable option compared to Guaranteed Cost programs.

Large employers may opt for a Self-Insurance program, where they assume the financial risk for providing workers' compensation benefits directly. This can be a cost-effective solution for companies with the financial strength and risk tolerance to handle potential claims. Self-insured employers often work with a third-party administrator (TPA) to manage claims and ensure compliance with regulatory requirements.

For smaller businesses or those in high-risk industries, a Captive Insurance program may be a viable option. This involves a group of employers pooling their resources to form a captive insurance company, which then provides workers' compensation coverage to its members. Captive programs can offer more control over premium rates and claims handling, as well as potential profit sharing for members with good loss experience.

Employers should carefully consider their business needs, risk profile, and budget constraints when selecting a workers' compensation insurance policy. Consulting with an experienced insurance broker or advisor can help navigate the complexities of different coverage options and ensure that the chosen policy aligns with the company's overall risk management strategy.

Understanding Exemptions: Who Doesn't Need Workers' Compensation Insurance in Florida?

You may want to see also

Explore related products

![]()

State Requirements: Learn about specific state mandates regarding workers' compensation insurance

Workers' compensation insurance is a critical aspect of business operations in the United States, and each state has its own set of mandates and regulations governing this type of insurance. Understanding these state-specific requirements is essential for business owners and HR professionals to ensure compliance and protect their employees.

One key aspect of state requirements is the definition of who qualifies as an employee. Some states, like California, have broad definitions that include independent contractors, while others, like Texas, have more narrow definitions. This distinction is crucial because it determines who is eligible for workers' compensation benefits.

Another important factor is the minimum number of employees required to mandate workers' compensation insurance. For instance, in Florida, businesses with four or more employees must carry this insurance, while in New York, it's required for all businesses with one or more employees.

The types of injuries or illnesses covered under workers' compensation also vary by state. While most states cover work-related injuries, some, like Illinois, also include coverage for occupational diseases. Additionally, some states, such as Georgia, have specific provisions for mental health conditions related to work.

Business owners should also be aware of the reporting and filing requirements in their state. In Ohio, for example, employers must report all work-related injuries within eight days, while in Pennsylvania, the deadline is 120 days for certain types of injuries.

Finally, the penalties for non-compliance with workers' compensation insurance requirements can be severe. In Michigan, employers who fail to carry the required insurance may face fines of up to $10,000 and even criminal charges. Therefore, it's crucial for businesses to stay informed about their state's specific mandates and ensure they have the appropriate coverage in place.

Understanding Exemptions: Who Doesn't Need Workers' Compensation Insurance in California?

You may want to see also

Explore related products

![]()

Exemptions: Discover which employers might be exempt from carrying workers' compensation insurance

Certain employers may be exempt from carrying workers' compensation insurance based on specific criteria. For instance, if an employer has fewer than a certain number of employees, they might not be required to carry this type of insurance. This exemption can vary by state, with some states setting the threshold at three employees, while others may set it at five or more. It's crucial for employers to check their state's specific regulations to determine if they fall under this exemption.

Another exemption could apply to employers who hire independent contractors rather than full-time employees. Since independent contractors are not considered employees, employers may not be obligated to provide workers' compensation insurance for them. However, this exemption can be tricky, as misclassifying an employee as an independent contractor can lead to legal issues and penalties. Employers should ensure they are correctly classifying their workers according to state laws and regulations.

Employers in certain industries might also be exempt from carrying workers' compensation insurance. For example, some states may exempt employers in the agricultural sector or those who hire seasonal workers for short periods. Additionally, employers who provide alternative forms of injury coverage, such as a private insurance plan that meets certain standards, might be exempt from the workers' compensation requirement.

It's important to note that exemptions from workers' compensation insurance are not automatic and often require employers to take specific steps, such as filing a form with the state or providing proof of alternative coverage. Employers should carefully review their state's laws and consult with an insurance professional to determine if they qualify for any exemptions and to ensure they are in compliance with all applicable regulations.

Essential Guide to Determining Your Workers' Compensation Insurance Needs

You may want to see also

Explore related products

![]()

Penalties for Non-Compliance: Understand the consequences of not having required workers' compensation insurance

Failing to secure the required workers' compensation insurance can lead to severe penalties for employers. These consequences are designed to protect employees and ensure that they receive the necessary benefits in the event of a workplace injury or illness. Employers who neglect this crucial aspect of business operation may face financial fines, legal action, and damage to their reputation.

The specific penalties for non-compliance vary depending on the jurisdiction and the severity of the offense. In some cases, employers may be subject to hefty fines, which can range from a few hundred to several thousand dollars. Repeat offenders may face even higher fines or more stringent penalties. Additionally, employers may be required to pay back wages and benefits to injured employees who were not properly covered.

Legal action is another potential consequence of failing to maintain workers' compensation insurance. Employees who are injured on the job and find that their employer does not have the required insurance may sue for damages. This can lead to lengthy and costly legal battles, which can further harm the employer's financial stability and reputation.

Beyond financial and legal repercussions, non-compliance with workers' compensation insurance requirements can also damage an employer's reputation. This can lead to a loss of trust among employees, potential clients, and the wider community. In some cases, employers may even face criminal charges, particularly if their negligence results in severe harm to an employee.

To avoid these penalties, it is essential for employers to understand their obligations regarding workers' compensation insurance. This includes knowing when such insurance is required, the types of coverage that must be provided, and the steps necessary to maintain compliance with relevant laws and regulations. By taking these precautions, employers can protect both their employees and their business from the consequences of non-compliance.

Understanding Workers' Compensation Insurance Funding: A State Fund Overview

You may want to see also

Frequently asked questions

Workers' compensation insurance is required when a business has employees, as it provides coverage for work-related injuries or illnesses.

Failure to have workers' compensation insurance when required can result in legal penalties, fines, and potential lawsuits from injured employees.

Workers' compensation insurance benefits employers by protecting them from lawsuits and providing a structured system for handling work-related injuries. It benefits employees by ensuring they receive medical care and wage replacement if they are injured on the job.