Certainly! Here's a paragraph introducing the topic:

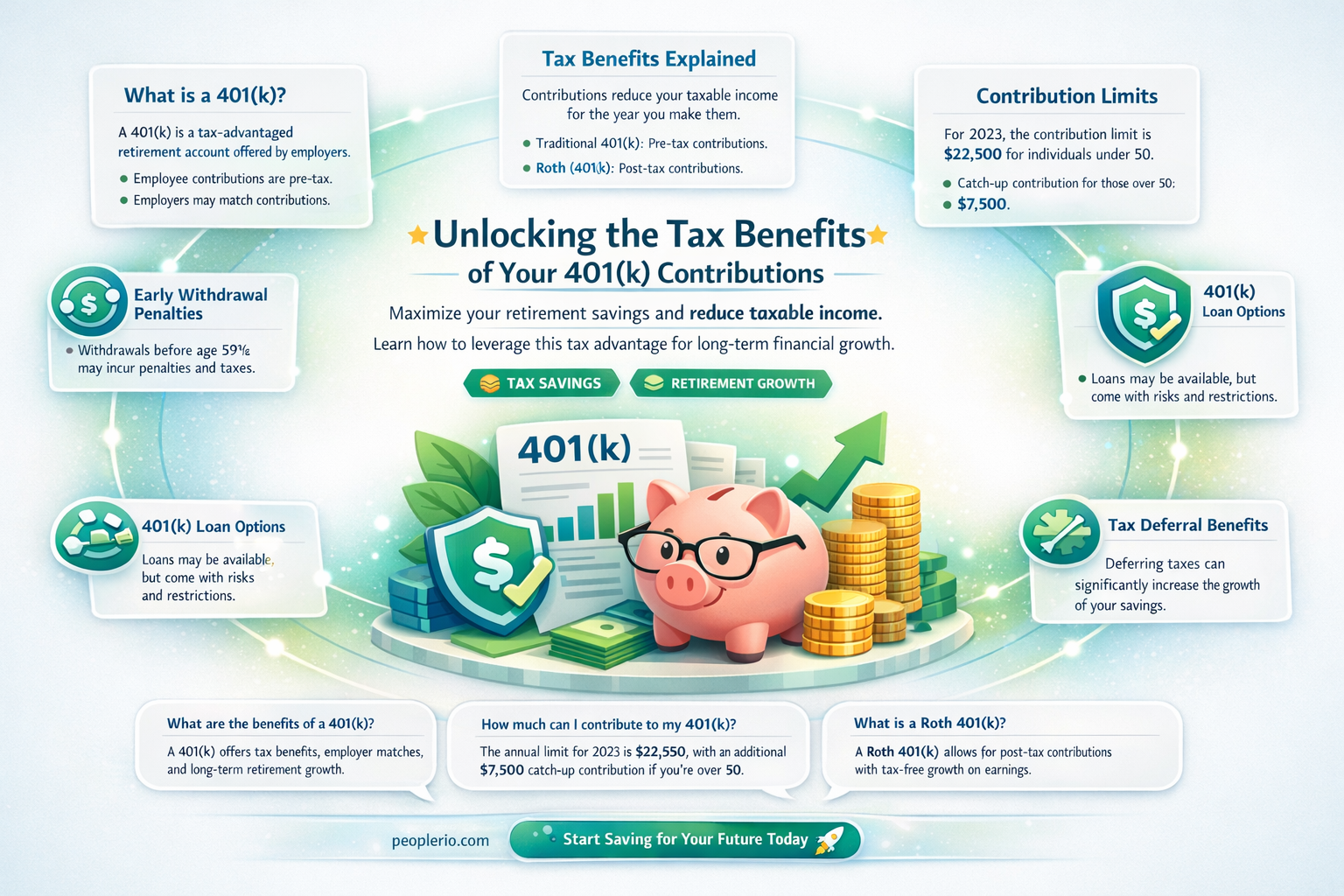

Understanding the tax implications of 401(k) contributions is crucial for employees planning their retirement. A 401(k) plan is a retirement savings plan sponsored by an employer that allows workers to save and invest a piece of their paycheck before taxes are taken out. One of the key benefits of contributing to a 401(k) is the potential for tax deductions. Contributions made by employees to their 401(k) plan are generally tax-deductible, meaning they can reduce the employee's taxable income for the year. This can result in a lower tax bill and more money saved for retirement. However, it's important to note that there are limits to how much can be contributed each year, and the tax benefits may vary depending on individual circumstances and tax laws.

This paragraph provides a clear and concise introduction to the topic, explaining what a 401(k) plan is, the tax benefits of contributing to one, and hinting at the importance of understanding the limits and laws surrounding these contributions.

| Characteristics | Values |

|---|---|

| Tax Deductibility | Contributions are tax-deductible for the employee |

| Contribution Limits | Subject to annual contribution limits |

| Tax Savings | Reduces taxable income for the contribution year |

| Employer Matching | Often matched by employer contributions |

| Investment Options | Offers a variety of investment options |

| Withdrawal Rules | Withdrawals are generally taxed and may incur penalties if taken before age 59.5 |

| Loan Provisions | Allows for loans against the account balance |

| Portability | Can be rolled over to other qualified plans or IRAs |

| Required Minimum Distributions | Mandatory distributions starting at age 72 (as of 2020) |

| Beneficiary Designation | Allows designation of beneficiaries for account balance upon death |

Explore related products

What You'll Learn

- Contribution Limits: Understand the annual contribution limits set by the IRS for 401(k) plans

- Tax Benefits: Explore how 401(k) contributions reduce taxable income and provide tax savings

- Employer Matching: Learn about employer matching contributions and their impact on tax deductions

- Roth vs. Traditional: Compare Roth and Traditional 401(k) contributions regarding tax deductibility

- Withdrawals and Penalties: Know the rules for withdrawals, including potential taxes and penalties

![]()

Contribution Limits: Understand the annual contribution limits set by the IRS for 401(k) plans

The IRS sets annual contribution limits for 401(k) plans, which are crucial for employees to understand in order to maximize their retirement savings while staying within the legal guidelines. For 2023, the contribution limit for employees is $19,500, with an additional catch-up contribution limit of $6,500 for those aged 50 and older. These limits are subject to change based on inflation and other economic factors, so it's important for employees to stay informed about any updates.

Exceeding these contribution limits can result in penalties, including excise taxes and potential withdrawal of excess contributions. Therefore, it's essential for employees to monitor their contributions throughout the year to ensure they do not surpass the limit. Employers may also impose their own contribution limits or matching contribution limits, which can further impact an employee's overall contribution strategy.

One strategy to consider is front-loading contributions, where an employee contributes as much as possible early in the year to take advantage of compound interest and potential employer matching contributions. However, this approach should be balanced with the need to maintain liquidity and avoid penalties for early withdrawals.

Another important aspect to consider is the impact of contribution limits on overall retirement planning. Employees should assess their contribution limits in conjunction with other retirement savings vehicles, such as IRAs or Roth IRAs, to ensure they are on track to meet their retirement goals. Consulting with a financial advisor can help employees develop a comprehensive retirement plan that takes into account contribution limits, investment strategies, and long-term financial objectives.

In summary, understanding and adhering to the annual contribution limits set by the IRS for 401(k) plans is a critical component of effective retirement planning. By staying informed about these limits and developing a strategic approach to contributions, employees can maximize their retirement savings while minimizing potential penalties and risks.

Railroad Employee Tax Filing Guide: Simplify Your Tax Process

You may want to see also

Explore related products

![]()

Tax Benefits: Explore how 401(k) contributions reduce taxable income and provide tax savings

K) contributions offer a significant tax advantage by reducing an employee's taxable income. When an employee contributes to their 401(k), the amount contributed is deducted from their gross income before taxes are calculated. This means that the employee is taxed on a lower income, resulting in a smaller tax bill. For example, if an employee contributes $5,000 to their 401(k) and their gross income is $50,000, they will only be taxed on $45,000. This reduction in taxable income can lead to substantial tax savings, especially for those in higher tax brackets.

The tax benefits of 401(k) contributions are further enhanced by the fact that the money grows tax-deferred. This means that the investment earnings on the contributions are not taxed until the money is withdrawn, typically in retirement. This allows the investments to grow more quickly, as the earnings are reinvested and compound over time. For instance, if an employee contributes $5,000 to their 401(k) and it grows at an average annual rate of 7%, after 30 years, the investment would be worth approximately $29,000. If the employee had been taxed on the earnings each year, the final amount would be significantly lower.

Another important aspect of the tax benefits of 401(k) contributions is that they can help employees avoid or reduce the impact of certain tax penalties. For example, if an employee's income is high enough, they may be subject to the Alternative Minimum Tax (AMT). However, 401(k) contributions can help reduce their taxable income below the AMT threshold, thereby avoiding or minimizing the impact of this tax. Additionally, 401(k) contributions can help employees qualify for other tax benefits, such as the Earned Income Tax Credit (EITC) or the Child Tax Credit, by reducing their taxable income.

It is also worth noting that the tax benefits of 401(k) contributions are not limited to federal taxes. Many states also offer tax deductions or credits for 401(k) contributions. This means that employees can enjoy tax savings at both the federal and state levels. However, it is important to check the specific tax laws of one's state to determine the exact benefits available.

In conclusion, 401(k) contributions provide employees with a valuable tax-saving opportunity. By reducing taxable income, allowing for tax-deferred growth, and potentially avoiding or reducing certain tax penalties, 401(k) contributions can help employees save money on taxes both now and in the future. This makes them an attractive option for those looking to maximize their retirement savings while also minimizing their tax burden.

Understanding Medicare Employee Additional Tax: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Employer Matching: Learn about employer matching contributions and their impact on tax deductions

Employer matching contributions are a crucial aspect of 401(k) plans that can significantly impact an employee's tax deductions. When an employer offers a matching contribution, it means they will contribute a certain percentage of the employee's contribution to their 401(k) account. This not only helps the employee save more for retirement but also reduces their taxable income.

For example, if an employer matches 50% of the employee's contribution up to 6% of their salary, and the employee contributes $2,000, the employer will contribute an additional $1,000. This $1,000 is not taxable to the employee, reducing their taxable income by that amount.

It's important to note that employer matching contributions are subject to certain limits. The total contribution limit for 2023 is $22,500 for employees under 50 and $30,000 for those 50 and older. This includes both the employee's and employer's contributions. Therefore, if an employer's matching contribution pushes the total over these limits, the excess may be taxable to the employee.

Employer matching contributions can also impact the employee's tax deductions in other ways. For instance, if the employee's income is reduced due to the matching contribution, they may be eligible for lower tax brackets or additional tax credits. This can further increase the tax savings for the employee.

In conclusion, employer matching contributions are a valuable benefit that can enhance an employee's retirement savings while also providing tax advantages. By understanding how these contributions work and their impact on tax deductions, employees can make informed decisions about their 401(k) contributions and maximize their retirement savings.

Maximizing Tax Benefits: The Truth About Employee Wage Deductions

You may want to see also

Explore related products

![]()

Roth vs. Traditional: Compare Roth and Traditional 401(k) contributions regarding tax deductibility

Roth vs. Traditional 401(k) contributions offer different tax advantages. Traditional 401(k) contributions are made pre-tax, reducing taxable income for the contribution year. This can lower tax liability and increase take-home pay. However, withdrawals in retirement are taxed as ordinary income. Roth 401(k) contributions, on the other hand, are made after-tax, providing no immediate tax deduction. The advantage lies in tax-free growth and withdrawals in retirement, assuming certain conditions are met.

One key difference is the timing of tax benefits. Traditional 401(k)s provide an upfront tax break, which can be beneficial for those in higher tax brackets or seeking to lower their current tax burden. Roth 401(k)s, while offering no immediate tax relief, provide a long-term benefit by allowing tax-free withdrawals, which can be advantageous for those expecting to be in a higher tax bracket in retirement or desiring a predictable income stream.

Another consideration is the impact on retirement planning. Traditional 401(k)s require careful planning to manage tax liabilities in retirement, as withdrawals are taxed. Roth 401(k)s simplify retirement income planning by eliminating taxes on qualified withdrawals, allowing for more flexibility in managing retirement finances.

In summary, the choice between Roth and Traditional 401(k) contributions depends on individual financial goals, tax expectations, and retirement planning strategies. While Traditional 401(k)s offer immediate tax benefits, Roth 401(k)s provide long-term tax advantages and simplified retirement income management.

Are Employee Pension Contributions Tax Deductible? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Withdrawals and Penalties: Know the rules for withdrawals, including potential taxes and penalties

Understanding the rules for withdrawals from a 401(k) plan is crucial for employees who wish to avoid unnecessary taxes and penalties. Generally, withdrawals made before the age of 59½ are subject to a 10% early withdrawal penalty, in addition to being taxed as ordinary income. However, there are several exceptions to this rule, such as withdrawals made for certain medical expenses, to pay for health insurance premiums while unemployed, or to cover the cost of higher education tuition.

One important exception to the early withdrawal penalty is the Substantially Equal Periodic Payments (SEPP) rule, which allows individuals to withdraw a certain amount from their 401(k) plan each year without incurring the 10% penalty. To qualify for SEPP, the withdrawals must be made over the individual's life expectancy, and the amount withdrawn each year must be substantially equal. This option can be particularly useful for individuals who need to access their retirement funds early but want to minimize the tax and penalty implications.

Another consideration for employees is the impact of withdrawals on their overall retirement savings strategy. Withdrawing funds early can significantly reduce the amount of money available for retirement, as well as the potential for investment growth. Therefore, it is important for employees to carefully weigh the benefits and drawbacks of making early withdrawals from their 401(k) plan.

In addition to the federal tax implications, employees should also be aware of any state taxes that may apply to their 401(k) withdrawals. Some states have their own income tax rates and rules for retirement plan withdrawals, which can further complicate the decision-making process.

To avoid unexpected penalties and taxes, employees should consult with a financial advisor or tax professional before making any withdrawals from their 401(k) plan. These experts can help individuals understand the specific rules and exceptions that apply to their situation, and can provide guidance on how to minimize the impact of withdrawals on their overall financial goals.

Employee Gifts and Taxes: What's Deductible for Your Business?

You may want to see also

Frequently asked questions

Yes, 401(k) contributions are tax-deductible for employees. This means that the amount you contribute to your 401(k) plan is subtracted from your taxable income, reducing your overall tax liability.

In 2023, employees can contribute up to $19,500 to a 401(k) plan. If you are age 50 or older, you may also be eligible to make an additional catch-up contribution of up to $6,500.

Yes, in addition to the tax deduction for contributions, 401(k) plans also offer tax-deferred growth. This means that the earnings on your investments grow tax-free until you withdraw the funds in retirement.

If you change jobs, you have several options for your 401(k) contributions. You can leave the funds in your former employer's plan, roll them over to your new employer's plan, or roll them over to an individual retirement account (IRA).

Yes, if you withdraw 401(k) funds before age 59 1/2, you may be subject to a 10% early withdrawal penalty. Additionally, you will owe income tax on the withdrawn funds. There are some exceptions to this penalty, such as withdrawals for medical expenses or to purchase a first home.