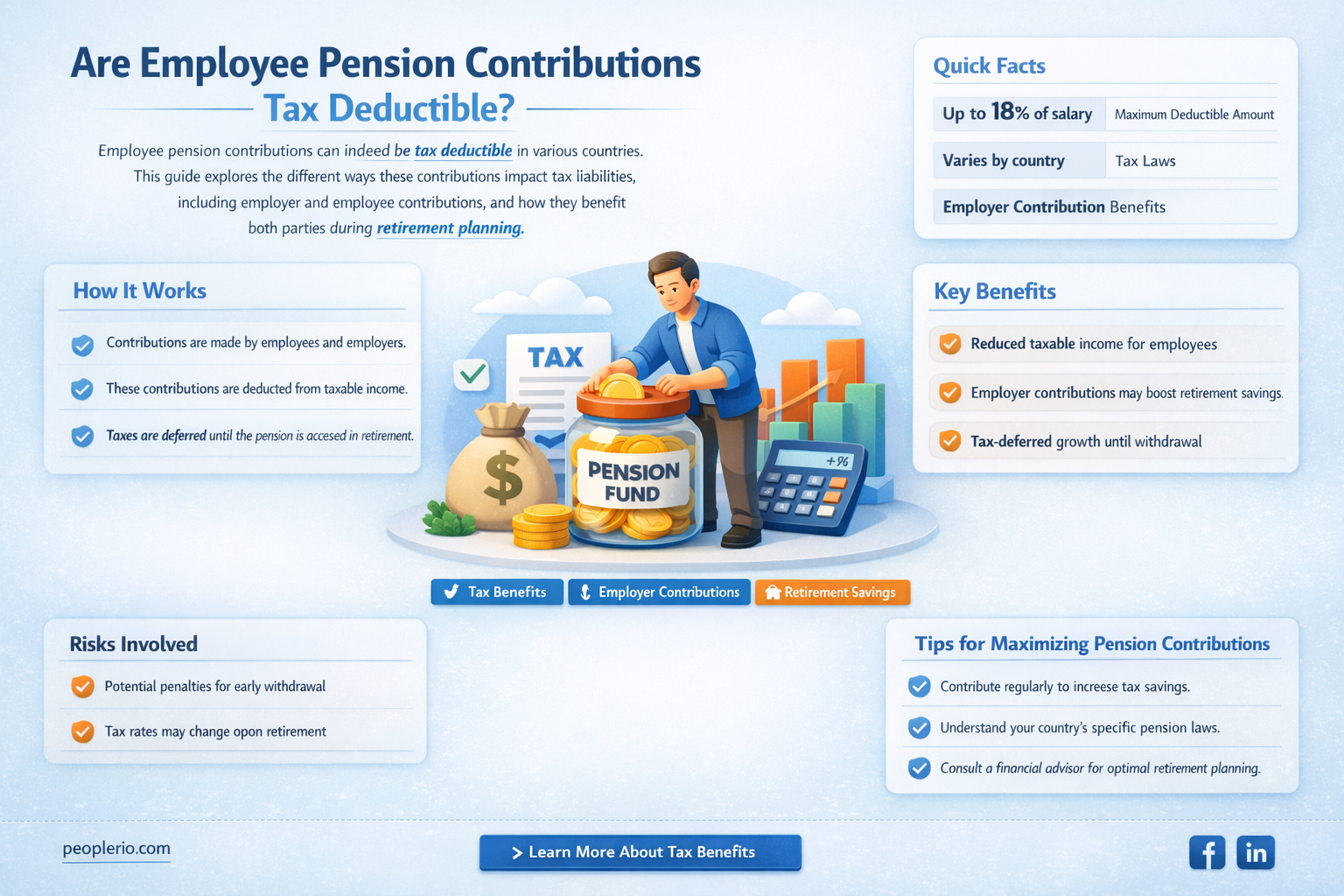

Employee pension contributions are a critical aspect of retirement planning, and understanding their tax implications is essential for maximizing financial benefits. Many countries offer tax incentives to encourage individuals to save for retirement, and one common question is whether employee pension contributions are tax deductible. In several jurisdictions, such as the United States and the United Kingdom, contributions to certain types of pension plans, like 401(k)s or personal pensions, can indeed reduce taxable income, thereby lowering the overall tax burden. However, the extent of deductibility often depends on factors like the type of pension plan, contribution limits, and the individual’s income level. Employees should consult tax laws or financial advisors to ensure they fully leverage these potential tax advantages while planning for their retirement.

| Characteristics | Values |

|---|---|

| Tax Deductibility | Employee pension contributions are generally tax-deductible in many countries, including the UK, USA, and others, up to certain limits. |

| UK Tax Rules | Contributions are deducted from gross income before tax, reducing taxable income. Relief is given at the highest rate of income tax paid. |

| USA Tax Rules (401(k)) | Contributions to traditional 401(k) plans are tax-deductible up to annual limits set by the IRS ($22,500 in 2023, with an additional $7,500 catch-up for ages 50+). |

| IRA Contributions (USA) | Traditional IRA contributions may be tax-deductible depending on income and participation in employer-sponsored plans. Roth IRA contributions are not tax-deductible. |

| Tax Limits | Deductions are capped annually (e.g., £40,000/year in the UK, $22,500 for 401(k) in the USA). Exceeding limits may result in penalties. |

| Employer Contributions | Employer pension contributions are typically tax-deductible for the employer and not taxable income for the employee. |

| Carry Forward Rules | Unused annual allowances (e.g., UK pension contributions) can sometimes be carried forward for tax relief in future years. |

| Tax Treatment at Withdrawal | Withdrawals from tax-deductible pension plans are generally taxed as income in retirement. |

| Country-Specific Variations | Tax deductibility rules vary by country; always check local tax laws or consult a financial advisor. |

| Self-Employed Individuals | Self-employed individuals may also deduct pension contributions, often through plans like SEP IRAs or self-employed 401(k)s in the USA. |

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for tax deductions on employee pension contributions

- Contribution Limits: Maximum deductible amounts for employee pension contributions annually

- Tax Benefits: How deductions reduce taxable income and overall tax liability

- Retirement Plans: Types of pension plans eligible for tax-deductible contributions

- Reporting Requirements: How to claim deductions on tax returns accurately

![]()

Eligibility Criteria: Who qualifies for tax deductions on employee pension contributions?

Employee pension contributions can indeed be tax-deductible, but not everyone qualifies for this benefit. The eligibility criteria vary by country and specific pension schemes, but there are common themes across jurisdictions. In the United States, for instance, contributions to traditional 401(k) plans or Individual Retirement Accounts (IRAs) may be tax-deductible, depending on factors like income level, marital status, and whether the employee is covered by a workplace retirement plan. Understanding these criteria is crucial for maximizing tax benefits while planning for retirement.

Income Limits and Filing Status: One of the primary determinants of eligibility is the taxpayer’s income. For example, in the U.S., contributions to a traditional IRA are fully deductible if neither the taxpayer nor their spouse is covered by a workplace retirement plan. However, if they are covered, the deduction phases out at higher incomes. For 2023, the phase-out range for single filers covered by a workplace plan starts at $73,000 and ends at $83,000. For married couples filing jointly, where the spouse making the IRA contribution is covered by a workplace plan, the phase-out range is $116,000 to $136,000. These limits highlight the importance of checking current IRS guidelines to ensure eligibility.

Type of Pension Plan: Not all pension plans offer tax-deductible contributions. In the UK, for example, contributions to personal pensions or workplace pensions (like auto-enrolment schemes) are typically tax-deductible at the highest rate of income tax the employee pays. However, contributions to some salary sacrifice schemes may not qualify for tax relief if they exceed annual allowance limits, currently set at £60,000 for most individuals. Similarly, in Canada, contributions to Registered Pension Plans (RPPs) or Registered Retirement Savings Plans (RRSPs) are deductible, but only up to a certain limit based on the employee’s earned income.

Age and Contribution Limits: Age can also play a role in eligibility. In Australia, for instance, individuals under 67 can claim tax deductions for personal superannuation contributions, provided they meet the “work test” or satisfy other conditions. Contribution limits are another critical factor. In the U.S., the maximum deductible contribution to a 401(k) in 2023 is $22,500, with an additional $7,500 catch-up contribution allowed for those aged 50 or older. Exceeding these limits can result in penalties, so careful planning is essential.

Practical Tips for Maximizing Deductions: To ensure eligibility, employees should regularly review their pension plan’s rules and consult tax professionals. For instance, if an employee’s income is near the phase-out threshold, they might consider contributing to a Roth IRA instead, which offers tax-free withdrawals in retirement. Additionally, keeping detailed records of contributions and staying informed about annual changes to tax laws can help avoid errors. Employers can assist by providing clear guidance on eligible plans and contribution limits, fostering a culture of informed financial planning.

In summary, eligibility for tax deductions on employee pension contributions hinges on factors like income, filing status, plan type, age, and contribution limits. By understanding these criteria and staying proactive, employees can optimize their retirement savings while minimizing tax liabilities.

Smart Tax Strategies: How a W2 Employee Reduced His Taxes

You may want to see also

Explore related products

![]()

Contribution Limits: Maximum deductible amounts for employee pension contributions annually

Employee pension contributions are a cornerstone of retirement planning, but understanding the tax implications can be complex. One critical aspect is the contribution limit—the maximum amount you can deduct annually. For 2023, the IRS allows individuals to contribute up to $22,500 to their 401(k) plans, with an additional $7,500 catch-up contribution for those aged 50 or older. These limits apply to both employee and employer contributions combined, but knowing your deductible portion is key to maximizing tax benefits. Exceeding these limits can result in penalties, so staying informed is essential.

Analyzing these limits reveals a strategic opportunity for tax optimization. For instance, if your employer matches contributions, ensure your personal contributions don’t push the total over the $22,500 threshold. For self-employed individuals, the rules differ slightly. Solo 401(k) plans allow a combined employee and employer contribution of up to $66,000 in 2023, with the same $7,500 catch-up provision. This higher limit reflects the dual role of the self-employed as both employee and employer, offering a broader scope for tax-deductible savings.

A comparative look at other retirement plans highlights the importance of these limits. For example, IRA contributions max out at $6,500 annually ($7,500 for those 50+), significantly lower than 401(k) limits. This disparity underscores the advantage of employer-sponsored plans for those seeking to maximize deductions. However, IRAs offer flexibility in investment choices, making them a viable alternative for those who’ve reached their 401(k) limits but still wish to save more.

Practical tips can help you navigate these limits effectively. First, automate your contributions to ensure consistency and avoid last-minute scrambling. Second, monitor your total contributions throughout the year, especially if you have multiple retirement accounts. Finally, consult a tax advisor to tailor your strategy to your financial situation. By staying within the limits, you can optimize your tax deductions while building a robust retirement fund.

In conclusion, understanding contribution limits is crucial for maximizing the tax benefits of employee pension contributions. Whether you’re contributing to a 401(k), Solo 401(k), or IRA, knowing the annual caps and how they apply to your situation can make a significant difference in your retirement savings strategy. Stay informed, plan strategically, and leverage these limits to secure your financial future.

Employee Gifts and Taxes: What's Deductible for Your Business?

You may want to see also

Explore related products

![]()

Tax Benefits: How deductions reduce taxable income and overall tax liability

Employee pension contributions often qualify as tax-deductible expenses, providing a direct reduction in taxable income. When an employee contributes to a pension plan, the amount contributed is typically subtracted from their gross income before taxes are calculated. For instance, if an employee earns $70,000 annually and contributes $5,000 to their pension, their taxable income drops to $65,000. This reduction can lower the individual’s tax bracket, resulting in significant savings. In the U.S., contributions to traditional 401(k) or IRA plans exemplify this benefit, while in the UK, pension contributions are treated similarly under the Pension Tax Relief scheme. This mechanism ensures that saving for retirement not only secures future income but also provides immediate financial relief through reduced tax liability.

The tax benefits of pension contributions extend beyond lowering taxable income; they also reduce overall tax liability by deferring taxation to a potentially lower-income period. Contributions to tax-deferred retirement accounts, such as 401(k)s or traditional IRAs, grow tax-free until withdrawal, typically during retirement when the individual may be in a lower tax bracket. For example, a high-earning professional in the 32% tax bracket might contribute $10,000 to their pension, saving $3,200 in taxes today. If they withdraw the funds in retirement at a 22% tax rate, they pay $2,200 in taxes, effectively saving $1,000. This strategy not only reduces current tax obligations but also maximizes the growth of retirement savings through compounding interest.

To maximize these tax benefits, employees should contribute strategically, considering both annual limits and employer matching programs. In the U.S., the 2023 contribution limit for 401(k)s is $22,500, with an additional $7,500 catch-up contribution for individuals aged 50 or older. Contributing up to these limits can significantly reduce taxable income while building a robust retirement fund. Additionally, employees should take full advantage of employer matching programs, as these essentially provide free money that further enhances retirement savings. For instance, if an employer matches 50% of contributions up to 6% of salary, an employee earning $60,000 should contribute at least $3,600 annually to receive the full $1,800 match.

While pension contributions offer substantial tax benefits, employees must navigate potential pitfalls to avoid unintended consequences. For example, exceeding contribution limits can result in penalties and additional taxes. Similarly, withdrawing funds early from tax-deferred accounts typically incurs a 10% penalty and immediate taxation, negating the benefits of tax deferral. Employees should also consider their overall financial situation, including current tax bracket, expected retirement income, and other savings goals. Consulting a financial advisor or tax professional can provide personalized guidance to optimize pension contributions and maximize tax savings while aligning with long-term financial objectives.

In summary, employee pension contributions serve as a powerful tool for reducing taxable income and overall tax liability. By lowering current tax obligations, deferring taxation, and leveraging employer matching programs, individuals can enhance their retirement savings while achieving immediate financial benefits. However, careful planning and adherence to contribution limits are essential to avoid penalties and ensure the strategy aligns with broader financial goals. Whether through a 401(k), IRA, or other pension plan, understanding and utilizing these tax benefits can pave the way for a more secure and prosperous retirement.

Maximize Your Take-Home Pay: Smart Tax Reduction Strategies for Employees

You may want to see also

Explore related products

![]()

Retirement Plans: Types of pension plans eligible for tax-deductible contributions

Employee pension contributions can indeed be tax-deductible, but the eligibility depends on the type of retirement plan and the specific rules governing it. Understanding which pension plans qualify for tax deductions is crucial for maximizing retirement savings while minimizing tax liabilities. Here’s a breakdown of the key plans and their tax advantages.

K) Plans: A Popular Choice for Tax-Deductible Contributions

One of the most widely recognized retirement plans, the 401(k), allows employees to contribute pre-tax dollars, reducing their taxable income for the year. For example, if an employee earns $70,000 annually and contributes $10,000 to their 401(k), their taxable income drops to $60,000. In 2023, the contribution limit is $22,500, with an additional $7,500 catch-up contribution for individuals aged 50 or older. This plan is employer-sponsored, and many companies offer matching contributions, effectively providing free money toward retirement. However, withdrawals before age 59½ typically incur penalties, so it’s essential to plan contributions with long-term goals in mind.

Traditional IRAs: Flexibility with Tax Deductions

For those without access to a 401(k) or seeking additional savings options, a Traditional IRA offers tax-deductible contributions, depending on income and participation in an employer-sponsored plan. In 2023, the contribution limit is $6,500, with a $1,000 catch-up provision for individuals over 50. For example, a single filer earning under $73,000 (or a joint filer earning under $116,000) can deduct the full contribution if they’re not covered by a workplace retirement plan. Even if deductions are phased out due to income, contributions can still be made, though they won’t be tax-deductible. This flexibility makes the Traditional IRA a versatile option for tax-efficient retirement planning.

SEP IRAs and SIMPLE IRAs: Options for Self-Employed and Small Businesses

Self-employed individuals and small business owners often turn to SEP IRAs or SIMPLE IRAs for tax-deductible contributions. A SEP IRA allows contributions of up to 25% of net earnings, capped at $66,000 in 2023. For instance, a self-employed individual with $100,000 in net earnings can contribute $25,000, all of which is tax-deductible. SIMPLE IRAs, on the other hand, have lower contribution limits ($15,500 in 2023, with a $3,500 catch-up option) but are easier to set up and maintain. Both plans offer significant tax advantages, making them ideal for those looking to save aggressively for retirement while reducing taxable income.

Comparing Plans: Which One Fits Your Needs?

Choosing the right tax-deductible pension plan depends on individual circumstances. For employees with access to a 401(k), this is often the best starting point due to higher contribution limits and potential employer matching. Self-employed individuals or small business owners may find SEP or SIMPLE IRAs more suitable, given their flexibility and higher contribution ceilings. Traditional IRAs are a solid option for those without workplace plans or seeking additional savings. By evaluating income, employment status, and retirement goals, individuals can select a plan that maximizes tax benefits while aligning with their financial objectives.

Practical Tips for Maximizing Tax-Deductible Contributions

To make the most of tax-deductible pension plans, consider contributing the maximum allowable amount annually. Automating contributions through payroll deductions or bank transfers ensures consistency. Additionally, monitor income levels to avoid missing out on deductions, especially with Traditional IRAs. Finally, consult a financial advisor or tax professional to tailor a strategy that optimizes tax savings while building a robust retirement fund. With the right plan and approach, tax-deductible contributions can significantly enhance long-term financial security.

Railroad Employee Tax Filing Guide: Simplify Your Tax Process

You may want to see also

Explore related products

![]()

Reporting Requirements: How to claim deductions on tax returns accurately

Employee pension contributions can indeed be tax-deductible, but the devil is in the details—specifically, in how you report them. Accurate reporting is crucial to ensure you claim the maximum allowable deductions without triggering audits or penalties. The first step is understanding which contributions qualify. Generally, contributions to workplace pension schemes like 401(k)s in the U.S. or personal pension plans in the U.K. are eligible, but limits apply. For instance, in the U.S., the 2023 contribution limit for a 401(k) is $22,500, with an additional $7,500 catch-up contribution for those aged 50 or older. Exceeding these limits can invalidate your deductions, so stay within the thresholds.

Once you’ve confirmed eligibility, the next step is to identify the correct tax forms. In the U.S., contributions to traditional 401(k)s or IRAs are reported on Form 1040, while self-employed individuals use Schedule 1 to claim deductions for SEP IRA or Solo 401(k) contributions. In the U.K., pension contributions are typically reported via your self-assessment tax return or through your employer’s payroll system. Ensure you have all necessary documentation, such as contribution statements from your pension provider or payroll records, to support your claims. Missing or incomplete documentation can delay processing or lead to disallowed deductions.

A common pitfall is misunderstanding the difference between tax-deductible and non-deductible contributions. For example, Roth IRA contributions are made with after-tax dollars and are not deductible, whereas traditional IRA contributions may be deductible depending on your income and whether you’re covered by a workplace retirement plan. Similarly, in the U.K., relief at source pension contributions are topped up by the government, but you must still report them accurately to avoid overclaiming. Always double-check the type of contribution you’re making and its tax treatment to avoid errors.

Finally, timing matters. Contributions must be made by the tax year deadline to qualify for deductions in that year. For example, in the U.S., 2023 contributions must be made by December 31, 2023, to be claimed on that year’s tax return. Late contributions, even if made in the following year, cannot be backdated. If you’re self-employed or making last-minute contributions, plan ahead to meet these deadlines. Additionally, consider using tax software or consulting a tax professional to ensure accuracy, especially if your financial situation is complex.

In summary, claiming deductions for pension contributions requires careful attention to eligibility, documentation, and deadlines. By understanding the rules, using the correct forms, and staying organized, you can maximize your tax benefits while avoiding common pitfalls. Accurate reporting not only ensures compliance but also helps you build a secure retirement fund efficiently.

Are Employee Bonuses Tax Deductible? A Comprehensive Guide for Employers

You may want to see also

Frequently asked questions

Yes, employee pension contributions are often tax deductible, depending on the country and specific tax laws. In many jurisdictions, contributions to approved pension schemes reduce taxable income, lowering overall tax liability.

Tax relief on pension contributions is typically applied automatically through your payroll if you contribute via a workplace pension scheme. For personal pension contributions, you may need to claim relief through your annual tax return or notify your tax authority.

Yes, most countries have annual or lifetime contribution limits for tax-deductible pension contributions. Exceeding these limits may result in the excess contributions not qualifying for tax relief. Check your local tax regulations for specific thresholds.