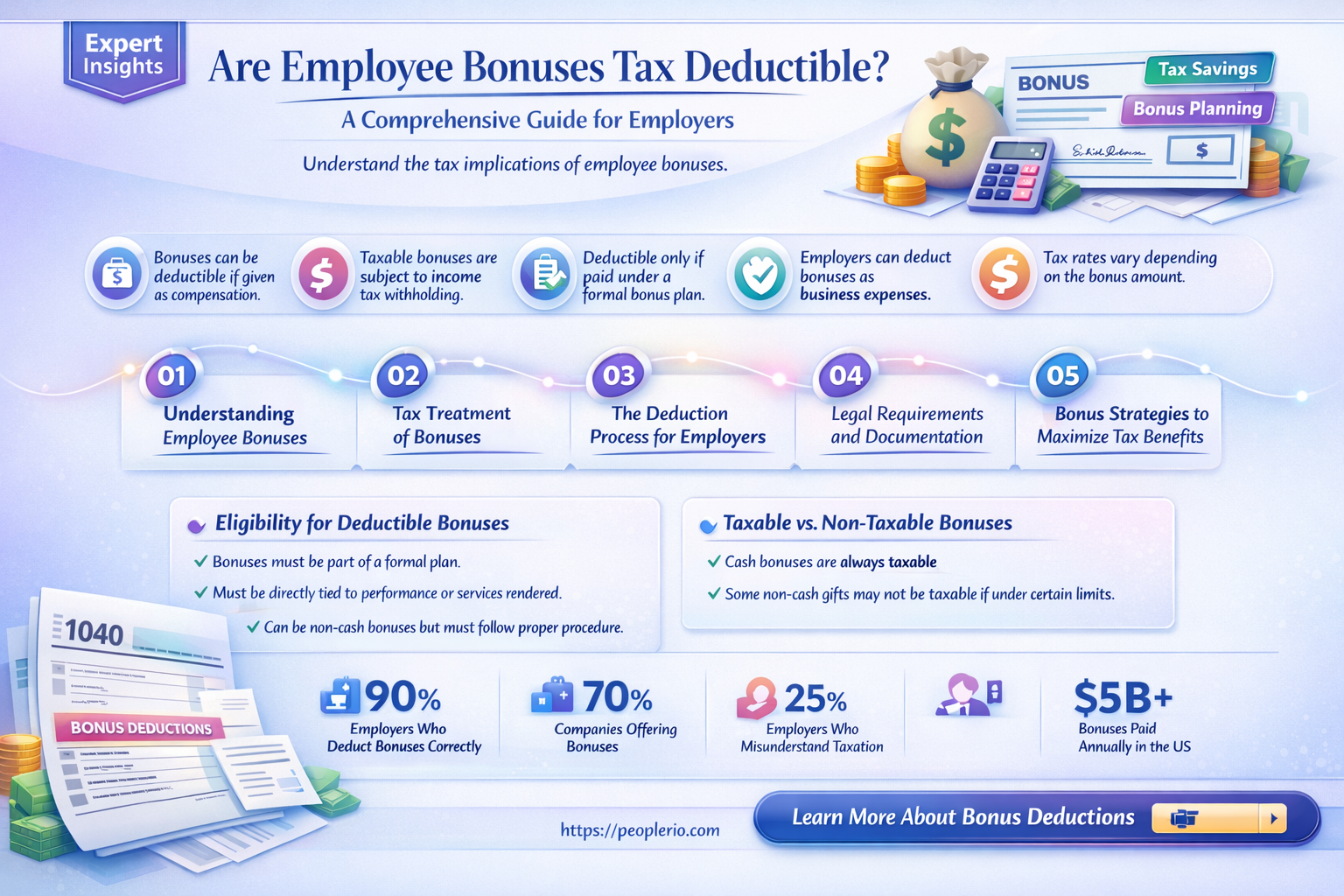

Employee bonuses can be a valuable tool for businesses to reward and motivate their workforce, but understanding the tax implications is crucial for both employers and employees. The question of whether employee bonuses are tax deductible is a common concern, as it directly impacts a company's financial planning and an individual's take-home pay. Generally, bonuses are considered taxable income for employees, meaning they are subject to federal, state, and payroll taxes. However, for employers, bonuses may be tax deductible as a business expense, provided they meet certain criteria, such as being reasonable in amount and directly related to the employee's performance or services rendered. Navigating these rules requires careful consideration of IRS guidelines and can significantly affect a company's bottom line and employee satisfaction.

| Characteristics | Values |

|---|---|

| Tax Deductibility for Employers | Yes, employee bonuses are generally tax-deductible for employers as a business expense, provided they are reasonable and meet IRS criteria. |

| Conditions for Deductibility | Bonuses must be ordinary and necessary business expenses, paid for services rendered, and not personal or lavish. |

| Employee Taxation | Bonuses are taxable income for employees and subject to federal, state, and payroll taxes (e.g., Social Security, Medicare). |

| Withholding Requirements | Employers must withhold applicable taxes from bonuses, including income tax, Social Security, and Medicare. |

| Timing of Deduction | Employers can claim the deduction in the tax year the bonuses are paid or accrued, depending on accounting methods. |

| Documentation Required | Proper documentation, such as payroll records and bonus policies, is necessary to support the deduction. |

| Exclusions | Bonuses paid to independent contractors or non-employees are not deductible under employee bonus rules. |

| IRS Guidelines | Must comply with IRS rules under Section 162(a) of the Internal Revenue Code for deductibility. |

| State Tax Variations | State tax treatment of bonuses may vary; employers should check state-specific regulations. |

| Reasonableness Test | Bonuses must be reasonable in amount; excessive bonuses may be disallowed by the IRS. |

Explore related products

What You'll Learn

- Eligibility Criteria: Rules for qualifying bonuses as deductible expenses under tax regulations

- Reasonable Compensation: Ensuring bonuses align with employee roles and industry standards

- Documentation Requirements: Proper records needed to claim deductions for employee bonuses

- Timing of Payments: Impact of bonus payment timing on tax deductibility in specific years

- IRS Guidelines: Adherence to IRS rules for classifying bonuses as deductible business expenses

![]()

Eligibility Criteria: Rules for qualifying bonuses as deductible expenses under tax regulations

To qualify employee bonuses as deductible expenses under tax regulations, businesses must navigate a strict set of eligibility criteria. These rules ensure that bonuses are genuinely performance-based and not merely disguised compensation. For instance, the IRS requires that bonuses be tied to specific, measurable achievements or company goals, such as meeting sales targets or completing projects ahead of schedule. Vague or arbitrary bonuses, like those given as holiday gifts without clear justification, are unlikely to pass scrutiny. This distinction is critical because only bonuses that meet these criteria can be deducted as ordinary and necessary business expenses.

One key eligibility rule is that bonuses must be reasonable in amount. Tax authorities evaluate whether the bonus is proportionate to the employee’s contribution and the company’s financial health. For example, a small business with modest profits awarding a six-figure bonus to an employee would raise red flags. To avoid this, businesses should document the rationale behind the bonus, linking it to specific achievements and their impact on the company’s bottom line. This not only strengthens the case for deductibility but also provides a clear audit trail if questioned.

Another critical factor is the timing of the bonus. Bonuses must be paid within a specific timeframe to qualify as deductible in a given tax year. For instance, in the U.S., bonuses must be paid within 2.5 months after the end of the tax year to be deductible for that year. Late payments may result in the deduction being deferred to the following year, disrupting cash flow planning. Businesses should therefore align their bonus payment schedules with tax deadlines to maximize deductions.

Finally, eligibility criteria often require that bonuses be consistently applied across similar roles or performance levels. Inconsistent bonus practices, such as awarding bonuses to favored employees without clear performance metrics, can disqualify the expense. For example, if sales team members receive bonuses for hitting targets but customer service staff do not, despite comparable contributions, the deduction may be denied. Fair and uniform application of bonus policies not only ensures compliance but also fosters employee morale and trust.

In summary, qualifying employee bonuses as deductible expenses hinges on clear performance linkage, reasonableness, timely payment, and consistent application. Businesses that meticulously adhere to these eligibility criteria can confidently claim deductions while avoiding potential audits or penalties. Practical steps include documenting performance metrics, aligning bonuses with company goals, and staying informed about tax deadlines. By treating bonuses as strategic rewards rather than discretionary gifts, companies can optimize their tax benefits while rewarding employees effectively.

Maximize Your Take-Home Pay: Tax Reduction Strategies for W2 Employees

You may want to see also

Explore related products

![]()

Reasonable Compensation: Ensuring bonuses align with employee roles and industry standards

Employee bonuses can be a powerful tool for motivating staff and driving business success, but their tax deductibility hinges on a critical factor: reasonableness. The IRS scrutinizes bonus payments to ensure they align with employee roles, industry standards, and overall compensation practices. A bonus deemed excessive or disproportionate to an employee's responsibilities may be reclassified as a dividend or personal expense, disqualifying it from tax deductions.

This underscores the importance of structuring bonuses with careful consideration of both financial and legal implications.

Determining reasonable compensation requires a multi-faceted approach. Start by benchmarking against industry norms. Research salary surveys, compensation reports, and job descriptions for similar roles within your sector. This provides a baseline for understanding typical bonus structures and ranges. For instance, a sales executive in the tech industry might expect a bonus tied to revenue targets, while a customer service representative may receive a smaller, performance-based incentive. Quantifying the impact of an employee's role on company performance is crucial. A bonus for a CEO should reflect their strategic leadership and overall business growth, while a bonus for a production line worker might be linked to efficiency improvements or quality control metrics.

Documenting the rationale behind each bonus decision is essential. Clearly outline the criteria used to determine the bonus amount, including specific performance metrics, achievements, and their contribution to company goals. This transparency not only strengthens your case for tax deductibility but also fosters trust and understanding among employees.

While aligning bonuses with industry standards is crucial, it's equally important to consider internal equity. A bonus structure should be fair and consistent across comparable roles within your organization. Avoid creating disparities that could lead to morale issues and potential legal challenges. For example, if two employees hold similar positions with comparable responsibilities and performance, their bonuses should reflect this parity.

Remember, reasonable compensation is a dynamic concept. Regularly review and adjust your bonus structure to reflect changing market conditions, company performance, and individual contributions. This proactive approach ensures your bonus program remains effective, motivating, and compliant with tax regulations. By carefully considering employee roles, industry benchmarks, and internal equity, you can design a bonus system that rewards performance, drives business success, and maximizes tax benefits.

Railroad Employee Tax Filing Guide: Simplify Your Tax Process

You may want to see also

Explore related products

![]()

Documentation Requirements: Proper records needed to claim deductions for employee bonuses

To claim deductions for employee bonuses as a business expense, meticulous documentation is non-negotiable. The IRS requires proof that bonuses are both ordinary and necessary business expenses, directly tied to employee performance or company goals. Without proper records, these payments could be reclassified as constructive dividends or personal gifts, triggering penalties and back taxes.

Step 1: Establish Clear Bonus Criteria

Before disbursing bonuses, document the criteria used to determine eligibility and amounts. This includes performance metrics, sales targets, or profit-sharing formulas. For example, if a bonus is tied to achieving 120% of quarterly sales goals, outline this in a written policy or employee handbook. Retain signed acknowledgments from employees confirming their understanding of these terms.

Step 2: Maintain Contemporaneous Records

Record bonus decisions as they occur, not retroactively. For instance, if a $5,000 bonus is awarded for exceeding a $500,000 sales target, document the achievement and approval process in real time. Include emails, meeting minutes, or performance reviews that justify the payout. Avoid vague descriptions like "year-end bonus"; specify the rationale (e.g., "Q4 sales exceeded target by 25%").

Step 3: Link Bonuses to Business Purpose

Ensure every bonus payment is traceable to a legitimate business purpose. For example, if a bonus is part of a retention strategy, include retention rates or turnover data in your documentation. Use payroll records to show bonuses are reported as taxable wages, not personal gifts. Cross-reference bonus amounts with Form W-2 and 941 filings to maintain consistency.

Caution: Avoid Common Pitfalls

Be wary of irregular or disproportionate bonuses, which may raise red flags. For instance, a $20,000 bonus to a part-time employee without clear justification could be questioned. Similarly, bonuses paid to owners or family members require stricter scrutiny. Always consult IRS Publication 15-B for compliance with employer tax responsibilities.

Proper documentation transforms employee bonuses from potential liabilities into defensible deductions. By systematically recording criteria, decisions, and business purpose, businesses can confidently claim these expenses while minimizing audit risks. Treat bonus documentation with the same rigor as payroll or tax filings—it’s not just a formality but a safeguard for your financial integrity.

Smart Tax Strategies: How a W2 Employee Reduced His Taxes

You may want to see also

Explore related products

![]()

Timing of Payments: Impact of bonus payment timing on tax deductibility in specific years

The timing of bonus payments can significantly influence their tax deductibility, offering businesses a strategic lever to optimize financial outcomes. For instance, a company with a fiscal year-end of December 31 can ensure bonuses are tax-deductible in the current year by paying them before January 1, provided the bonuses are fixed and determinable before year-end. This requires clear documentation, such as board resolutions or employee notifications, to establish the liability before the cutoff date.

Consider a scenario where a business owner decides to reward employees with a $50,000 bonus pool in December. If the bonuses are paid in December, the business can claim the deduction in the current tax year, reducing taxable income accordingly. However, if the payment is delayed until January, the deduction shifts to the following year, potentially altering cash flow and tax planning strategies. This highlights the importance of aligning payment timing with fiscal year-ends to maximize immediate tax benefits.

From a strategic perspective, businesses should evaluate their cash flow and tax liabilities when deciding on bonus timing. For companies operating on a calendar year, accelerating bonuses into December instead of January can provide a tax shield in the current year, especially if the business anticipates higher profits. Conversely, delaying bonuses into the next year may be advantageous if the business expects lower profits or higher tax rates in the following period. This approach requires careful forecasting and consultation with tax professionals to avoid penalties for late deductions.

Practical tips include setting internal deadlines for bonus decisions, such as finalizing amounts and notifying employees by mid-December. Additionally, businesses should ensure payroll systems are prepared to process payments before year-end to avoid administrative delays. For accrual-basis taxpayers, the key is establishing a fixed liability before year-end, even if the payment is made later, as long as it occurs within 2.5 months of the fiscal year-end to qualify for the deduction in the intended year.

In conclusion, the timing of bonus payments is a critical factor in tax deductibility, offering businesses a tool to manage tax liabilities effectively. By understanding the rules and planning strategically, companies can align bonus payments with their financial goals, ensuring deductions are claimed in the most advantageous tax year. This requires proactive decision-making, clear documentation, and coordination with payroll and tax advisors to navigate the complexities of tax regulations.

Employee Gifts and Taxes: What's Deductible for Your Business?

You may want to see also

Explore related products

![]()

IRS Guidelines: Adherence to IRS rules for classifying bonuses as deductible business expenses

The IRS allows businesses to deduct employee bonuses as a business expense, but only if they meet specific criteria. This classification hinges on whether the bonus is considered compensation for services rendered or a gift. Understanding these distinctions is crucial for accurate tax reporting and maximizing deductions.

Example: A year-end bonus tied to company performance and individual employee contributions is more likely to be deductible than a holiday gift card given to all employees regardless of performance.

Analysis: The IRS scrutinizes the purpose and structure of bonuses. Deductible bonuses must be:

- Reasonable in amount: Excessive bonuses disproportionate to an employee's role or company profits may raise red flags.

- Based on performance or profit: Bonuses should be tied to measurable criteria like sales targets, project completion, or overall company profitability.

- Documented: Clear documentation outlining the bonus structure, eligibility criteria, and payout calculations is essential.

Takeaway: Businesses can leverage bonuses as a tax-advantaged way to reward employees, but careful planning and adherence to IRS guidelines are paramount.

Frequently asked questions

Yes, employee bonuses are generally tax deductible for businesses as a business expense, provided they meet IRS criteria for reasonableness and are tied to performance or services rendered.

Bonuses that are performance-based, profit-sharing, or tied to specific achievements typically qualify for tax deductions, as long as they are not considered gifts or personal expenses.

Yes, bonuses must be reported on employee W-2 forms and included in payroll taxes, and the business must also report them as an expense on their tax return to claim the deduction.

While there’s no specific dollar limit, bonuses must be considered "reasonable" in amount and directly related to the employee’s services. Excessive bonuses may be scrutinized by the IRS.

Yes, holiday or year-end bonuses can be tax deductible if they are treated as compensation, reported on payroll, and meet the IRS requirements for business expenses.