Reducing taxes as an employee requires a strategic approach to maximize deductions and take advantage of available tax benefits. By understanding your tax bracket, contributing to retirement accounts like a 401(k) or IRA, and utilizing pre-tax deductions for health insurance or dependent care, you can lower your taxable income. Additionally, keeping detailed records of work-related expenses, such as mileage, education, or home office costs, can help you claim valuable deductions. Staying informed about tax credits, like the Earned Income Tax Credit or education credits, and consulting a tax professional can further optimize your tax savings, ensuring you retain more of your hard-earned income.

Explore related products

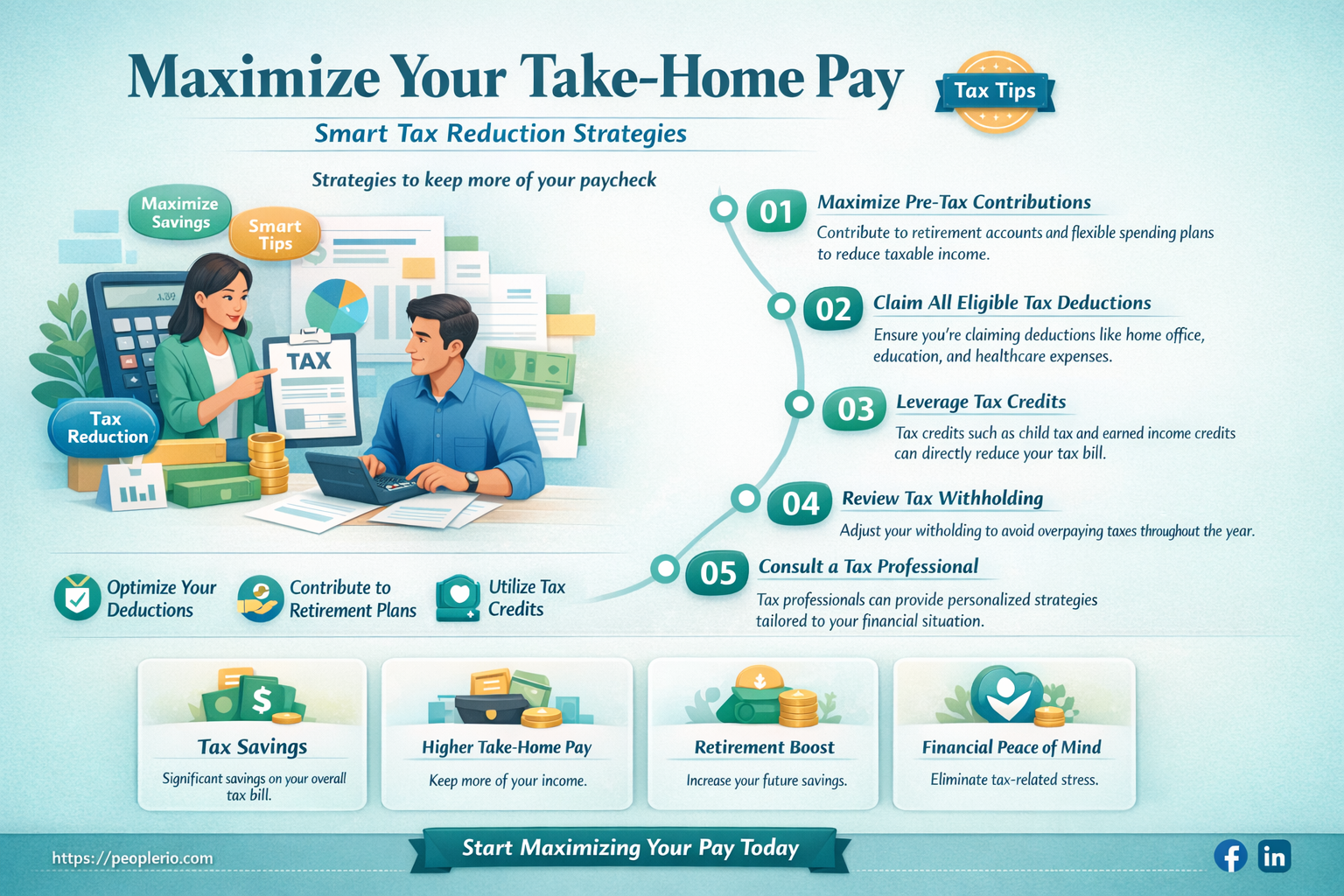

What You'll Learn

- Maximize Retirement Contributions: Contribute to 401(k) or IRA to lower taxable income

- Utilize Pretax Benefits: Leverage FSA/HSA for medical/dependent care expenses

- Claim All Deductions: Track work-related expenses, student loan interest, and charitable donations

- Adjust Withholding: Update W-4 to avoid overpaying taxes throughout the year

- Education Credits: Use Lifetime Learning or American Opportunity Credits for tuition costs

![]()

Maximize Retirement Contributions: Contribute to 401(k) or IRA to lower taxable income

One of the most effective ways to reduce your taxable income as an employee is by maximizing your retirement contributions. By funneling money into a 401(k) or IRA, you not only build a nest egg for the future but also lower your current tax burden. This strategy leverages the tax-deferred nature of these accounts, allowing you to pay taxes on the contributions later, when you’re likely in a lower tax bracket during retirement. For example, contributing $10,000 to a 401(k) could reduce your taxable income by the same amount, potentially saving you thousands in taxes depending on your marginal tax rate.

To implement this strategy, start by understanding your employer’s 401(k) plan. Many companies offer matching contributions, which is essentially free money. Aim to contribute at least enough to max out this match—typically 3% to 6% of your salary. For 2023, the maximum 401(k) contribution limit is $22,500, with an additional $7,500 catch-up contribution allowed for those aged 50 or older. If your employer doesn’t offer a 401(k), or if you’ve maxed it out, consider opening a traditional IRA. The contribution limit for an IRA is $6,500 in 2023, with an additional $1,000 catch-up contribution for those over 50.

While maximizing contributions is beneficial, it’s crucial to balance this strategy with your current financial needs. Over-contributing to retirement accounts can leave you short on cash for immediate expenses or emergencies. A practical approach is to automate your contributions, starting with a percentage of your income that aligns with your budget. Gradually increase this percentage as your salary grows or as you pay off debts. For instance, if you currently contribute 5% of your salary, aim to increase it by 1% every six months until you reach the maximum allowed.

One common misconception is that contributing to a 401(k) or IRA locks your money away until retirement. While early withdrawals generally incur penalties, there are exceptions, such as using IRA funds for a first-time home purchase or certain education expenses. Additionally, some 401(k) plans allow for loans against your balance, though this should be a last resort. The primary goal is long-term growth, so focus on consistent contributions rather than viewing these accounts as accessible funds.

In conclusion, maximizing retirement contributions through a 401(k) or IRA is a powerful tool for reducing taxable income while securing your financial future. By understanding contribution limits, leveraging employer matches, and automating your savings, you can optimize this strategy without compromising your current financial stability. Start small if necessary, but start now—the compounding benefits of early and consistent contributions cannot be overstated.

Smart Tax Strategies: How a W2 Employee Reduced His Taxes

You may want to see also

Explore related products

$12.49 $21.99

![]()

Utilize Pretax Benefits: Leverage FSA/HSA for medical/dependent care expenses

One of the most effective ways to reduce your taxable income as an employee is by taking advantage of pretax benefits like Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs). These accounts allow you to set aside pretax dollars for qualified medical and dependent care expenses, directly lowering your taxable income. For instance, if you contribute $2,000 to an FSA, that amount is deducted from your gross income before taxes are calculated, potentially saving you hundreds of dollars depending on your tax bracket.

To maximize these benefits, start by estimating your annual eligible expenses carefully. FSAs typically cover out-of-pocket medical costs like prescriptions, copays, and even over-the-counter medications with a doctor’s note. For dependent care FSAs, expenses like daycare, after-school programs, or summer camps for children under 13 qualify. HSAs, available only with high-deductible health plans, offer broader flexibility, including investment options and no "use-it-or-lose-it" rule, unlike FSAs. For example, if you have predictable medical expenses like annual prescriptions or braces for a child, an FSA can be a smart choice.

However, caution is key. FSAs often have a "use-it-or-lose-it" policy, meaning any unspent funds at the end of the plan year are forfeited. To avoid this, track your expenses throughout the year and adjust contributions if necessary. For HSAs, while there’s no immediate forfeiture risk, contributions should align with your healthcare needs and long-term financial goals. For instance, if you’re generally healthy but want to save for future medical expenses, an HSA’s investment feature can grow your savings tax-free.

In practice, consider these steps: first, review your employer’s benefits package to confirm FSA/HSA availability. Next, calculate your expected eligible expenses—for medical FSAs, factor in deductibles, prescriptions, and routine care; for dependent care, estimate childcare costs. Finally, contribute strategically, keeping in mind the "use-it-or-lose-it" rule for FSAs and the long-term advantages of HSAs. By leveraging these pretax accounts, you not only reduce your tax liability but also ensure your healthcare and dependent care expenses are more manageable.

Are Employee Bonuses Tax Deductible? A Comprehensive Guide for Employers

You may want to see also

Explore related products

![]()

Claim All Deductions: Track work-related expenses, student loan interest, and charitable donations

Every dollar you spend on work-related expenses is a potential tax deduction. From the mileage on your car for work trips to the cost of a home office setup, these expenses add up. The key is meticulous record-keeping. Use a dedicated app or spreadsheet to log every expense, including dates, amounts, and purposes. For example, if you’re a salesperson driving to client meetings, track your mileage using an app like MileIQ, which automatically calculates deductions based on IRS rates (currently 65.5 cents per mile for 2023). Without proper documentation, these deductions are worthless, so make tracking a habit.

Student loan interest is another often-overlooked deduction. If you’re repaying federal or private student loans, you may deduct up to $2,500 in interest annually, depending on your income. For instance, single filers with a modified adjusted gross income (MAGI) below $70,000 in 2023 can claim the full deduction, while those earning between $70,000 and $85,000 qualify for a partial deduction. Married couples filing jointly have a MAGI threshold of $145,000 to $175,000. Even if you don’t itemize deductions, this one is available to you. Check Form 1098-E from your loan servicer to confirm the interest paid and claim it on Schedule 1 of your tax return.

Charitable donations are a powerful way to reduce taxable income while supporting causes you care about. Cash donations to qualified organizations can be deducted up to 60% of your adjusted gross income (AGI), while donations of appreciated assets like stocks or mutual funds can be deducted at fair market value, bypassing capital gains tax. For example, if you donate $10,000 worth of stock that you purchased for $5,000, you deduct $10,000 and avoid tax on the $5,000 gain. Always obtain a receipt or acknowledgment letter from the charity, especially for donations over $250, as the IRS requires written documentation for larger contributions.

The takeaway? Deductions are a taxpayer’s best friend, but they require proactive effort. Work-related expenses, student loan interest, and charitable donations are three areas where many employees leave money on the table. By tracking expenses diligently, understanding eligibility thresholds, and keeping proper documentation, you can maximize your deductions and minimize your tax liability. It’s not just about saving money—it’s about reclaiming what’s rightfully yours.

Railroad Employee Tax Filing Guide: Simplify Your Tax Process

You may want to see also

Explore related products

![]()

Adjust Withholding: Update W-4 to avoid overpaying taxes throughout the year

Overpaying taxes throughout the year is a common pitfall for employees, often resulting in a large refund at tax time. While a refund might feel like a windfall, it’s essentially an interest-free loan to the government. Adjusting your withholding by updating your W-4 form can help you keep more of your money in your paycheck throughout the year, rather than waiting for a lump sum in April. This strategy requires understanding your tax situation and making proactive changes to align your withholding with your actual tax liability.

To begin, gather your most recent tax return and recent pay stubs. Use the IRS Tax Withholding Estimator, a free online tool, to calculate the ideal number of allowances or additional withholding you should claim on your W-4. For example, if you’re single with no dependents and earn $60,000 annually, claiming two allowances might be appropriate, but adding extra withholding could prevent overpayment. Conversely, if you have multiple income streams or significant deductions, reducing allowances or specifying an additional dollar amount to withhold per paycheck could be more accurate.

Updating your W-4 is straightforward but requires attention to detail. Access the form through your employer’s HR portal or request a physical copy. On the new W-4, you’ll find steps to account for multiple jobs, dependents, and other income sources. For instance, if you’re married filing jointly and both spouses work, using the "Two-Earners/Multiple Jobs Worksheet" can help you avoid under-withholding. Be cautious not to reduce withholding too much, as this could lead to a tax bill at year-end. Aim for a balance where your total tax liability is covered without significant overpayment.

One practical tip is to review your W-4 annually or after major life changes, such as marriage, divorce, the birth of a child, or a significant income shift. For example, if you had a child during the year, you might qualify for additional credits, reducing your overall tax burden. Adjusting your withholding promptly ensures your paycheck reflects these changes. Additionally, if you receive a large bonus or commission, consider asking your employer to withhold at a higher rate for that paycheck to avoid a surprise tax bill.

In conclusion, adjusting your withholding via the W-4 form is a proactive way to manage your cash flow and avoid overpaying taxes. By taking the time to understand your tax situation and make informed adjustments, you can keep more of your earnings throughout the year. This approach not only improves your financial flexibility but also ensures you’re not inadvertently subsidizing the government with your hard-earned money.

Employee Gifts and Taxes: What's Deductible for Your Business?

You may want to see also

Explore related products

![]()

Education Credits: Use Lifetime Learning or American Opportunity Credits for tuition costs

Employees seeking to reduce their tax burden often overlook the power of education credits, specifically the Lifetime Learning Credit (LLC) and the American Opportunity Credit (AOC). These credits can significantly offset the costs of higher education, whether you're pursuing a degree, taking classes to improve job skills, or even enrolling in courses for personal development. Unlike deductions, which reduce taxable income, credits directly reduce the amount of tax you owe, dollar for dollar. This makes them a valuable tool for anyone looking to minimize their tax liability while investing in their education.

The American Opportunity Credit is particularly generous, offering up to $2,500 per eligible student per year for the first four years of post-secondary education. To qualify, the student must be pursuing a degree or other recognized credential, and the credit covers 100% of the first $2,000 in tuition and fees, plus 25% of the next $2,000. Notably, 40% of the AOC is refundable, meaning if the credit exceeds your tax liability, you can receive up to $1,000 back as a refund. This makes it an especially attractive option for lower-income individuals or families. To claim the AOC, the student must be enrolled at least half-time for at least one academic period during the tax year, and the credit phases out for single filers with modified adjusted gross incomes (MAGI) between $80,000 and $90,000, or joint filers with MAGI between $160,000 and $180,000.

In contrast, the Lifetime Learning Credit is more flexible, catering to a broader range of students, including those taking just one course or pursuing non-degree programs. The LLC provides up to $2,000 per tax return (not per student) for eligible tuition and fees, covering 20% of the first $10,000 spent on qualified education expenses. Unlike the AOC, the LLC is not refundable, but it can be used for an unlimited number of years, making it ideal for part-time students, graduate students, or individuals seeking to update their job skills. The income limits for the LLC are also higher, phasing out for single filers with MAGI between $59,000 and $69,000, or joint filers with MAGI between $118,000 and $138,000.

When deciding between the two credits, consider your educational goals, enrollment status, and income level. For instance, if you’re a full-time undergraduate student in the first four years of higher education, the AOC’s higher maximum credit and refundable portion make it the better choice. However, if you’re taking a single course to enhance your resume or pursuing a graduate degree, the LLC’s flexibility and lack of enrollment restrictions may be more advantageous. Keep in mind that you cannot claim both credits for the same student in the same year, so strategic planning is key.

To maximize these credits, maintain detailed records of tuition payments, fees, and any required course materials. While books, supplies, and equipment are no longer eligible expenses for the AOC, they may qualify for the LLC if purchased from an outside vendor. Additionally, coordinate with family members if claiming credits for dependents, as the credits can only be claimed by one taxpayer per student. By leveraging the Lifetime Learning or American Opportunity Credits, employees can not only advance their education but also significantly reduce their tax liability, making these credits a smart financial move for lifelong learners.

Maximize Your Take-Home Pay: Tax Reduction Strategies for W2 Employees

You may want to see also

Frequently asked questions

Yes, contributing to tax-advantaged retirement accounts like a 401(k) or Traditional IRA can lower your taxable income. These contributions are often made pre-tax, reducing the amount of income subject to federal and state taxes.

As of recent tax law changes, unreimbursed employee expenses are no longer deductible for most taxpayers. However, certain professions (e.g., educators) may still claim limited deductions for qualified expenses. Check IRS guidelines for eligibility.

Tax credits directly reduce the amount of tax you owe, unlike deductions. Common credits include the Child Tax Credit, Earned Income Tax Credit (EITC), and education credits like the American Opportunity Tax Credit (AOTC). Ensure you meet eligibility requirements to claim these.