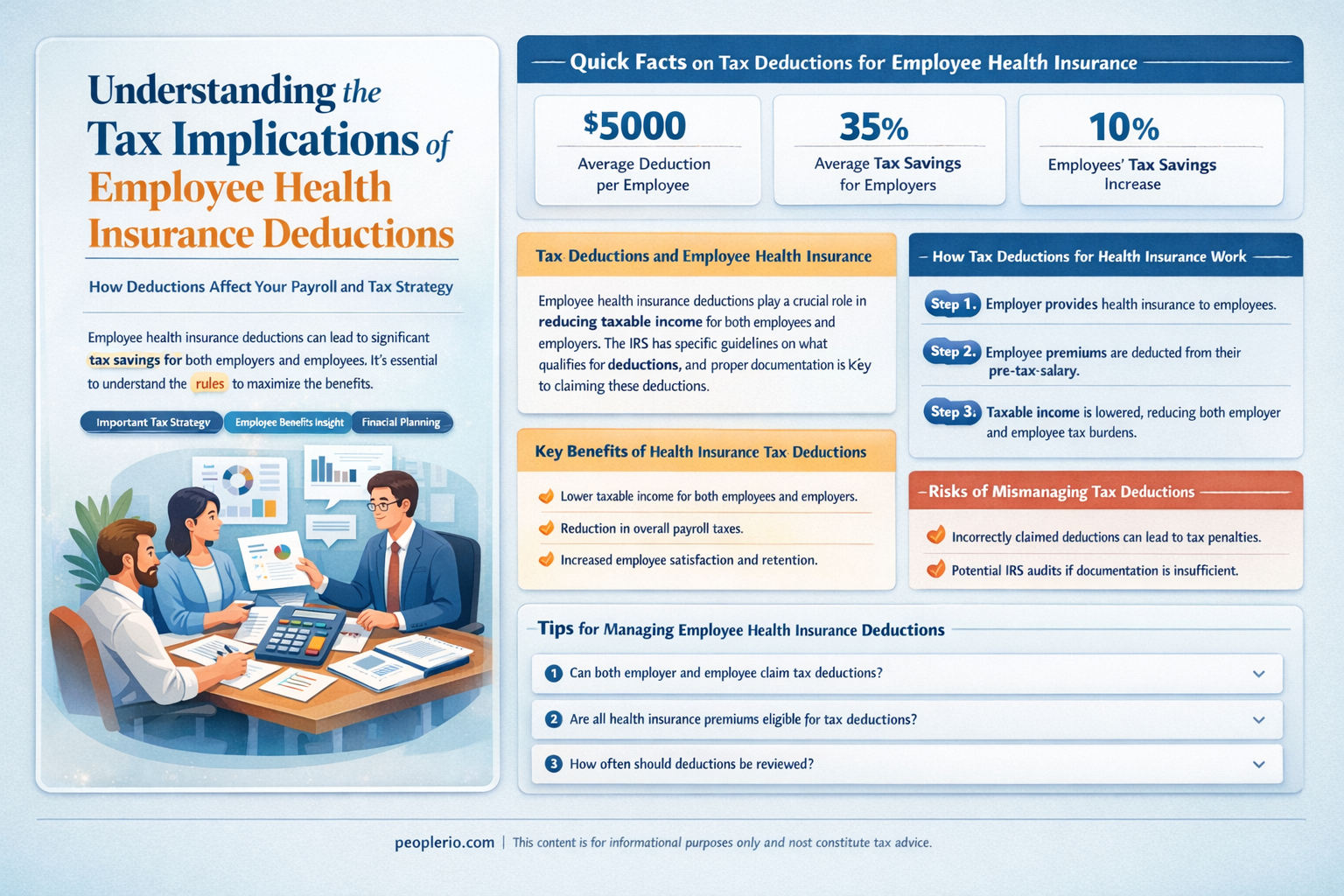

Employee deductions for health insurance are a common practice in many companies, but the tax implications of these deductions can be complex. In general, health insurance premiums paid by employees through payroll deductions are considered tax-free, as long as they are for a qualified health plan. This means that the deductions are not subject to federal income tax, Social Security tax, or Medicare tax. However, there are some exceptions and nuances to this rule, such as the requirement that the health plan must be a qualified health plan under the Affordable Care Act, and that the employer must properly report the deductions on the employee's W-2 form. Additionally, state tax laws may vary, and some states may tax health insurance premiums. It is important for employees and employers to understand the tax implications of health insurance deductions to ensure compliance with tax laws and to make informed decisions about health insurance coverage.

| Characteristics | Values |

|---|---|

| Taxability | Generally not taxable |

| Conditions | Must be for health insurance premiums paid by the employee |

| Exclusions | Premiums paid for non-health insurance plans |

| Limitations | Only applies to premiums paid during the tax year |

| Documentation | Employees should keep records of premiums paid |

| Reporting | Premiums may need to be reported on Form W-2 |

Explore related products

What You'll Learn

- General Rule: Employee deductions for health insurance are generally not taxable under certain conditions

- Conditions for Exemption: The insurance must be a qualified health plan, and the deduction must be for the employee's share

- Taxable Situations: If the employer pays for the health insurance, it may be considered taxable income to the employee

- Reporting Requirements: Employers must report the amount of health insurance deductions on the employee's W-2 form

- State Tax Considerations: Some states may have different rules regarding the taxability of health insurance deductions

![]()

General Rule: Employee deductions for health insurance are generally not taxable under certain conditions

Employee deductions for health insurance are generally not taxable under certain conditions, which can provide significant tax savings for individuals. This rule applies when the deductions are made under a qualified health plan, such as a group health plan provided by an employer or a health insurance exchange plan. The key condition is that the premiums must be paid with after-tax dollars, meaning they are not deducted from the employee's gross income.

One important aspect to consider is the type of health plan. For instance, if an employee is enrolled in a Health Savings Account (HSA) or a Flexible Spending Account (FSA), the contributions made to these accounts are typically tax-deductible. However, the rules can vary depending on the specific plan and the employee's individual circumstances. It's crucial to consult with a tax professional or the plan administrator to understand the tax implications of health insurance deductions.

Another factor that can impact the taxability of health insurance deductions is the employee's income level. In some cases, higher-income individuals may be subject to taxes on their health insurance premiums if they exceed certain thresholds. This is often related to the Affordable Care Act's (ACA) individual mandate, which requires individuals to maintain minimum essential coverage or pay a penalty.

To ensure compliance with tax regulations, employees should keep accurate records of their health insurance deductions and any related documentation. This includes maintaining records of premium payments, plan enrollment, and any correspondence with the plan administrator or tax authorities. By doing so, employees can substantiate their deductions and avoid potential tax penalties or audits.

In conclusion, while employee deductions for health insurance are generally not taxable under certain conditions, it's essential to understand the specific rules and requirements that apply to individual situations. Consulting with a tax professional and keeping accurate records can help employees maximize their tax savings while ensuring compliance with tax regulations.

Navigating Spousal Coverage: Employee Health Insurance Obligations Explained

You may want to see also

Explore related products

![]()

Conditions for Exemption: The insurance must be a qualified health plan, and the deduction must be for the employee's share

To qualify for tax exemption, the health insurance plan must meet specific criteria set by the IRS. Firstly, it must be a qualified health plan, which generally means it provides minimum essential coverage and adheres to the Affordable Care Act's standards. This ensures that the plan offers a comprehensive level of care, including preventive services, without imposing lifetime limits on coverage.

Secondly, the deduction must be for the employee's share of the premiums. This means that the portion of the health insurance cost that the employer covers is not eligible for tax exemption. The employee must pay their share of the premiums out-of-pocket to qualify for the deduction. This distinction is crucial as it prevents employers from taking advantage of tax benefits intended for employees.

The IRS has strict guidelines on what constitutes a qualified health plan. For instance, the plan must cover at least 60% of healthcare costs, known as the actuarial value, and must not have an annual deductible exceeding a certain threshold. Additionally, the plan must offer coverage for essential health benefits, such as maternity care, mental health services, and prescription drugs.

Employees should also be aware that the tax exemption applies only to premiums paid during the tax year. Any premiums paid in advance or arrears do not qualify for the current year's deduction. Furthermore, the deduction is limited to the amount of the employee's taxable income for the year. This means that if an employee's income is low, their deduction may be limited or even zero.

In conclusion, understanding the conditions for tax exemption on health insurance premiums is essential for both employers and employees. By ensuring that the plan meets the IRS's criteria and that the deduction is properly calculated, employees can take advantage of this valuable tax benefit while employers can provide a competitive compensation package.

Understanding FICA: Are Employee Paid Health Insurance Premiums Subject to FICA?

You may want to see also

Explore related products

![]()

Taxable Situations: If the employer pays for the health insurance, it may be considered taxable income to the employee

In the realm of employee benefits, the tax implications of health insurance can be complex. When an employer pays for an employee's health insurance, this benefit may be considered taxable income to the employee. This scenario often arises when the employer provides a health insurance plan as part of the employee's compensation package. The value of this benefit is typically included in the employee's gross income, which can have significant tax consequences.

To understand the tax implications, it's essential to consider the specifics of the situation. For instance, if the employer pays for a health insurance plan that covers both the employee and their dependents, the entire premium may be taxable to the employee. However, if the employee contributes a portion of the premium, only the employer's contribution is considered taxable income. Additionally, the tax treatment may vary depending on whether the health insurance plan is fully insured, self-insured, or a hybrid model.

The taxability of employer-paid health insurance also depends on the employee's tax filing status and the state in which they reside. For example, some states may exempt employer-paid health insurance from state income tax, while others may tax it as ordinary income. Furthermore, the Affordable Care Act (ACA) has introduced additional complexities, such as the requirement for employers to report the value of health insurance benefits on employees' W-2 forms.

To navigate these complexities, employees should consult with a tax professional or their employer's human resources department to understand the specific tax implications of their health insurance benefits. They may also need to adjust their tax withholding or estimated tax payments to account for the additional taxable income. By doing so, employees can avoid unexpected tax liabilities and ensure compliance with tax laws.

In conclusion, the taxability of employer-paid health insurance is a nuanced issue that requires careful consideration of various factors, including the type of plan, the employee's tax filing status, and state tax laws. Employees should take the time to understand the tax implications of their health insurance benefits to avoid potential pitfalls and make informed decisions about their finances.

Boosting Employee Wellness: Strategies for a Healthier, Happier Workforce

You may want to see also

Explore related products

![]()

Reporting Requirements: Employers must report the amount of health insurance deductions on the employee's W-2 form

Employers are required to report the amount of health insurance deductions on an employee's W-2 form. This is a crucial aspect of tax reporting that ensures transparency and accuracy in the calculation of taxable income. The W-2 form, officially known as the Wage and Tax Statement, is a document that employers must send to their employees and the Internal Revenue Service (IRS) at the end of the year. It details the employee's annual wages, the amount of taxes withheld from their paycheck, and other relevant information, including health insurance deductions.

The reporting of health insurance deductions on the W-2 form is significant because it helps employees determine their taxable income. The amount deducted for health insurance is generally not considered taxable income, which means it can reduce the employee's overall tax liability. By accurately reporting these deductions, employers help their employees avoid overpaying taxes and ensure that they are in compliance with federal tax laws.

To report health insurance deductions on the W-2 form, employers must follow specific guidelines set by the IRS. The deductions should be reported in Box 12 of the W-2 form, using the appropriate code from the IRS's list of W-2 codes. Employers must also ensure that the deductions are calculated correctly and that they reflect the actual amounts withheld from the employee's wages for health insurance premiums.

Failure to report health insurance deductions on the W-2 form can result in penalties for the employer and may lead to employees facing unexpected tax liabilities. It is therefore essential for employers to understand their reporting obligations and to take the necessary steps to comply with federal tax laws. By doing so, they can help their employees make informed decisions about their taxes and ensure that they are not subject to unnecessary financial burdens.

Understanding Employee-Sponsored Health Insurance: Benefits, Costs, and Coverage Explained

You may want to see also

Explore related products

![]()

State Tax Considerations: Some states may have different rules regarding the taxability of health insurance deductions

While federal tax laws provide a general framework for the taxability of health insurance deductions, state tax laws can introduce significant variations. Some states may fully conform to federal rules, while others may have distinct regulations that can impact how employees and employers approach health insurance deductions.

For instance, certain states may allow for additional deductions or credits for health insurance premiums beyond what is permitted under federal law. This could be particularly beneficial for employees who are responsible for a significant portion of their health insurance costs. Conversely, some states may impose stricter rules on the taxability of health insurance deductions, potentially increasing the tax burden on employees.

To navigate these complexities, it is essential for employees and employers to be aware of the specific state tax laws that apply to them. This may involve consulting with a tax professional or reviewing state tax publications to ensure compliance and optimize tax planning strategies.

Moreover, changes in state tax laws can occur frequently, so it is crucial to stay informed about any updates or amendments that may affect health insurance deductions. This could involve monitoring state tax websites, subscribing to tax newsletters, or attending tax seminars to stay abreast of the latest developments.

Ultimately, understanding state tax considerations is a critical component of effective tax planning for employees and employers alike. By being aware of the unique rules and regulations that apply at the state level, individuals can make informed decisions about their health insurance deductions and minimize their tax liabilities.

Understanding Employee Health: Key Factors for Workplace Well-Being

You may want to see also

Frequently asked questions

Generally, employee deductions for health insurance are not taxable if they meet certain conditions. The premiums must be for a qualified health plan, and the employee must not be able to deduct the premiums as a medical expense on their tax return.

A qualified health plan is a health insurance plan that meets the requirements of the Affordable Care Act (ACA). These plans must cover essential health benefits, have a minimum actuarial value, and meet certain cost-sharing requirements.

Yes, self-employed individuals can deduct health insurance premiums as a business expense on their tax return. However, they cannot deduct the premiums as a medical expense on Schedule A.

Yes, there are some exceptions. For example, if an employee's health insurance premiums are paid with pre-tax dollars through a flexible spending account (FSA) or a health savings account (HSA), the premiums may be taxable. Additionally, if an employee receives a subsidy from their employer to help pay for health insurance, the subsidy may be taxable.