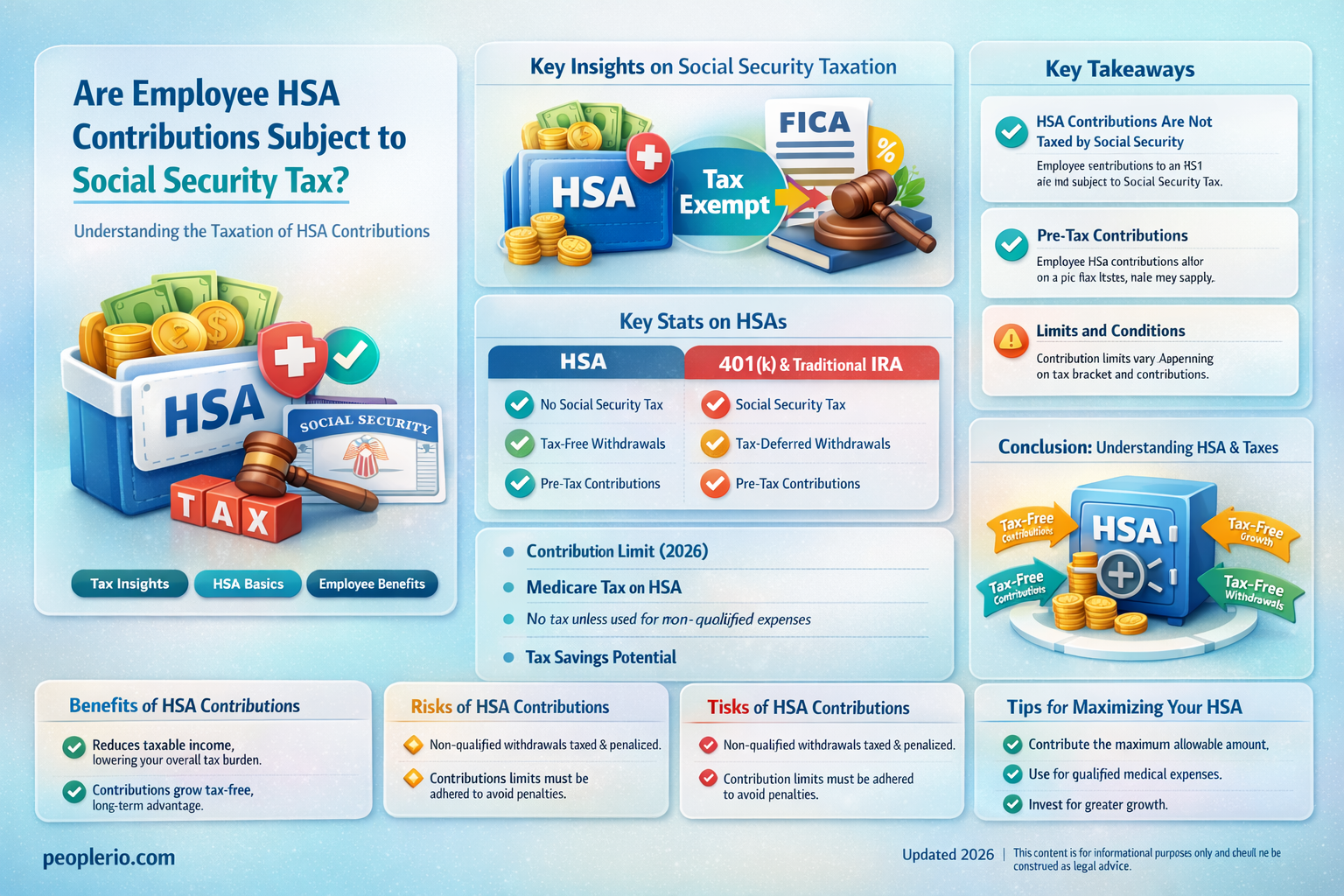

Employee contributions to a Health Savings Account (HSA) are generally not subject to Social Security tax. According to IRS guidelines, these contributions are considered tax-deductible and are not included in the employee's gross income for Social Security tax purposes. This means that when an employee contributes to their HSA, the amount contributed is not taxed by Social Security, providing a financial benefit to the employee. However, it's important to note that there are limits to how much an employee can contribute to their HSA each year, and these limits may vary depending on factors such as the employee's age and the type of health insurance plan they have. Additionally, while HSA contributions are not subject to Social Security tax, they may still be subject to other types of taxes, such as federal income tax, depending on the employee's tax situation.

| Characteristics | Values |

|---|---|

| Subject | Are employee HSA contributions subject to social security tax? |

| Source | TurboTax |

| Category | Tax-related |

| Type | Question |

| Language | English |

| Date | June 2024 |

Explore related products

What You'll Learn

- HSA Basics: Understanding Health Savings Accounts, their purpose, and how they benefit employees and employers

- Tax Advantages: Exploring the tax benefits of HSAs, including deductions and tax-free growth

- Social Security Tax: Overview of Social Security tax implications on HSA contributions and distributions

- Employer Contributions: Insights on how employer contributions to HSAs are treated for tax purposes

- TurboTax Guidance: Specific instructions and tips for reporting HSA contributions and distributions on TurboTax

![]()

HSA Basics: Understanding Health Savings Accounts, their purpose, and how they benefit employees and employers

Health Savings Accounts (HSAs) are a type of savings account that allows individuals to save money on a tax-advantaged basis for qualified medical expenses. HSAs are only available to people who have a high-deductible health plan (HDHP) and are not enrolled in Medicare. The purpose of an HSA is to help individuals save money for future medical expenses, while also reducing their taxable income.

HSAs offer several benefits to both employees and employers. For employees, HSAs provide a way to save money on taxes and to have a dedicated fund for medical expenses. For employers, HSAs can help to reduce health insurance premiums and to provide a more attractive benefits package to employees.

One of the key benefits of HSAs is that the contributions are made on a pre-tax basis, which means that the money is not subject to federal income tax. Additionally, the earnings on the HSA investments grow tax-free, and the withdrawals are also tax-free when used for qualified medical expenses. This makes HSAs a powerful tool for saving money on taxes and for managing healthcare costs.

Another benefit of HSAs is that they are portable, which means that the account can be taken with the individual if they change jobs or retire. This portability makes HSAs a valuable long-term savings vehicle for healthcare expenses.

In order to open an HSA, an individual must first have a high-deductible health plan (HDHP). The HDHP must meet certain requirements, such as having a minimum deductible and a maximum out-of-pocket limit. Once the HDHP is in place, the individual can open an HSA with a qualified financial institution.

When it comes to contributing to an HSA, there are several options available. Employees can contribute a portion of their paycheck directly to the HSA, and employers can also make contributions on behalf of their employees. Additionally, individuals can make lump-sum contributions to their HSA at any time during the year.

In conclusion, HSAs are a valuable tool for saving money on taxes and for managing healthcare costs. They offer several benefits to both employees and employers, and they are a portable savings vehicle that can be taken with the individual if they change jobs or retire. By understanding the basics of HSAs, individuals can make informed decisions about how to use these accounts to their advantage.

Smart Tax Strategies: How a W2 Employee Reduced His Taxes

You may want to see also

Explore related products

![]()

Tax Advantages: Exploring the tax benefits of HSAs, including deductions and tax-free growth

Health Savings Accounts (HSAs) offer significant tax advantages, making them an attractive option for individuals looking to save on healthcare costs. One of the primary benefits is the ability to deduct HSA contributions from your taxable income, reducing your overall tax liability. This deduction is available to both individuals and families, and the amount varies based on the type of health insurance coverage you have.

Another key tax advantage of HSAs is the tax-free growth of the funds within the account. Unlike other types of savings accounts, the interest and investment earnings in an HSA grow tax-free, allowing your savings to compound more quickly. This can be particularly beneficial for long-term healthcare savings, as the tax-free growth can significantly increase the value of your account over time.

Additionally, HSAs offer tax-free withdrawals for qualified medical expenses. This means that you can use the funds in your HSA to pay for a wide range of healthcare costs, including doctor visits, prescriptions, and medical procedures, without incurring any taxes on the withdrawals. This can be a major advantage, especially for individuals with high-deductible health insurance plans.

It's important to note that while HSA contributions are not subject to Social Security tax, they may be subject to other taxes, such as state and local income taxes. Additionally, if you withdraw funds from your HSA for non-qualified expenses, you may be subject to a penalty tax. Therefore, it's crucial to understand the tax implications of HSAs and to use them in a way that maximizes their benefits while minimizing any potential tax liabilities.

In summary, HSAs offer several tax advantages, including deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. By understanding and leveraging these benefits, individuals can save significantly on healthcare costs and build a more secure financial future.

Are Employee HSA Contributions Subject to Medicare Tax?

You may want to see also

![]()

Social Security Tax: Overview of Social Security tax implications on HSA contributions and distributions

Employee contributions to a Health Savings Account (HSA) are generally not subject to Social Security tax. This is because HSAs are designed to provide a tax-advantaged way for individuals to save for qualified medical expenses. When you contribute to an HSA, the funds are deducted from your gross income, reducing your taxable income for the year. This results in a lower Social Security tax liability, as Social Security tax is calculated based on your gross income.

However, it's important to note that while the contributions themselves are not taxed, the earnings on the investments within the HSA may be subject to Social Security tax if they are not used for qualified medical expenses. Additionally, if you withdraw funds from your HSA for non-qualified expenses before the age of 65, you may be subject to a 20% penalty tax, which includes Social Security tax.

Employer contributions to an employee's HSA are also not subject to Social Security tax. This is because employer contributions are considered a fringe benefit and are not included in the employee's gross income. However, employer contributions may be subject to other taxes, such as Medicare tax.

When it comes to distributions from an HSA, if the funds are used for qualified medical expenses, they are generally not subject to Social Security tax. However, if the distributions are used for non-qualified expenses, they may be subject to Social Security tax, as well as other taxes and penalties.

In summary, while employee HSA contributions are not subject to Social Security tax, it's important to be aware of the potential tax implications of investment earnings and distributions from the account. Understanding these implications can help you make informed decisions about your HSA contributions and distributions.

Understanding Employee Taxes: A Comprehensive Guide for Workers

You may want to see also

![]()

Employer Contributions: Insights on how employer contributions to HSAs are treated for tax purposes

Employer contributions to Health Savings Accounts (HSAs) are a valuable benefit for employees, but understanding their tax implications is crucial. Unlike employee contributions, which are generally made on a pre-tax basis and reduce taxable income, employer contributions are treated differently for tax purposes.

Firstly, employer contributions to an HSA are considered taxable income to the employee. This means that the amount contributed by the employer will be reported on the employee's W-2 form and included in their gross income when filing taxes. However, there is a silver lining: these contributions are not subject to Social Security or Medicare taxes. This exemption can result in significant savings for both the employer and the employee, as these taxes typically amount to 7.65% of the employee's income.

It's important to note that employer contributions are subject to federal income tax withholding, unless the employee specifically requests that they be excluded from withholding. This can be done by submitting a Form W-4 to the employer. Additionally, some states may require state income tax withholding on employer contributions, so it's essential to check state tax laws for specific requirements.

One strategic consideration for employers is the timing of their contributions. Contributions made early in the year can provide employees with more time to utilize the funds for qualified medical expenses, potentially reducing their taxable income further. Employers may also choose to make contributions in a lump sum or spread them out over the year, depending on their payroll schedules and the needs of their employees.

In summary, while employer contributions to HSAs are taxable, they offer a unique advantage by being exempt from Social Security and Medicare taxes. This can make them an attractive benefit for both employers and employees, especially when managed strategically to maximize tax savings and healthcare spending efficiency.

Essential Tax Forms for Employees: A Comprehensive Guide

You may want to see also

![]()

TurboTax Guidance: Specific instructions and tips for reporting HSA contributions and distributions on TurboTax

To accurately report HSA contributions and distributions on TurboTax, follow these specific instructions and tips:

- Identify the correct forms: You'll need to use Form 1040 and Form 8889 to report your HSA contributions and distributions. Form 1040 is the standard tax return form, while Form 8889 is specifically for reporting HSA information.

- Report contributions: On Form 8889, you'll find a section to report your HSA contributions. Enter the total amount you contributed to your HSA during the tax year. Remember to include any employer contributions as well.

- Report distributions: In the same form, you'll need to report any distributions you took from your HSA. Distributions are withdrawals you made from your HSA to pay for qualified medical expenses. Be sure to have supporting documentation for these expenses in case of an audit.

- Calculate the tax impact: TurboTax will automatically calculate the tax impact of your HSA contributions and distributions. However, it's essential to review these calculations to ensure accuracy. HSA contributions are generally tax-deductible, while distributions are tax-free if used for qualified medical expenses.

- Common mistakes to avoid: One common mistake is failing to report HSA contributions or distributions accurately. This can lead to incorrect tax calculations and potential penalties. Another mistake is not keeping proper records of medical expenses paid with HSA funds. Always maintain detailed records to support your tax filings.

- Seek professional guidance if needed: If you're unsure about how to report your HSA information on TurboTax, consider consulting a tax professional. They can provide personalized guidance and help you navigate any complex tax situations related to your HSA.

By following these instructions and tips, you can ensure that your HSA contributions and distributions are reported accurately on TurboTax, helping you avoid potential tax issues and maximize the benefits of your HSA.

Tax Savings Guide for 1099 Employees: Smart Strategies for Financial Peace

You may want to see also

Frequently asked questions

No, employee HSA contributions are not subject to Social Security tax. TurboTax confirms that these contributions are excluded from Social Security taxation.

TurboTax allows users to report their HSA contributions on Form 1040, Schedule A, which is used for itemizing deductions. The software ensures that these contributions are properly accounted for and excluded from taxable income.

TurboTax highlights that one of the benefits of using an HSA is that the contributions made by employees are not only tax-deductible but also exempt from Social Security tax, which can lead to significant tax savings over time.