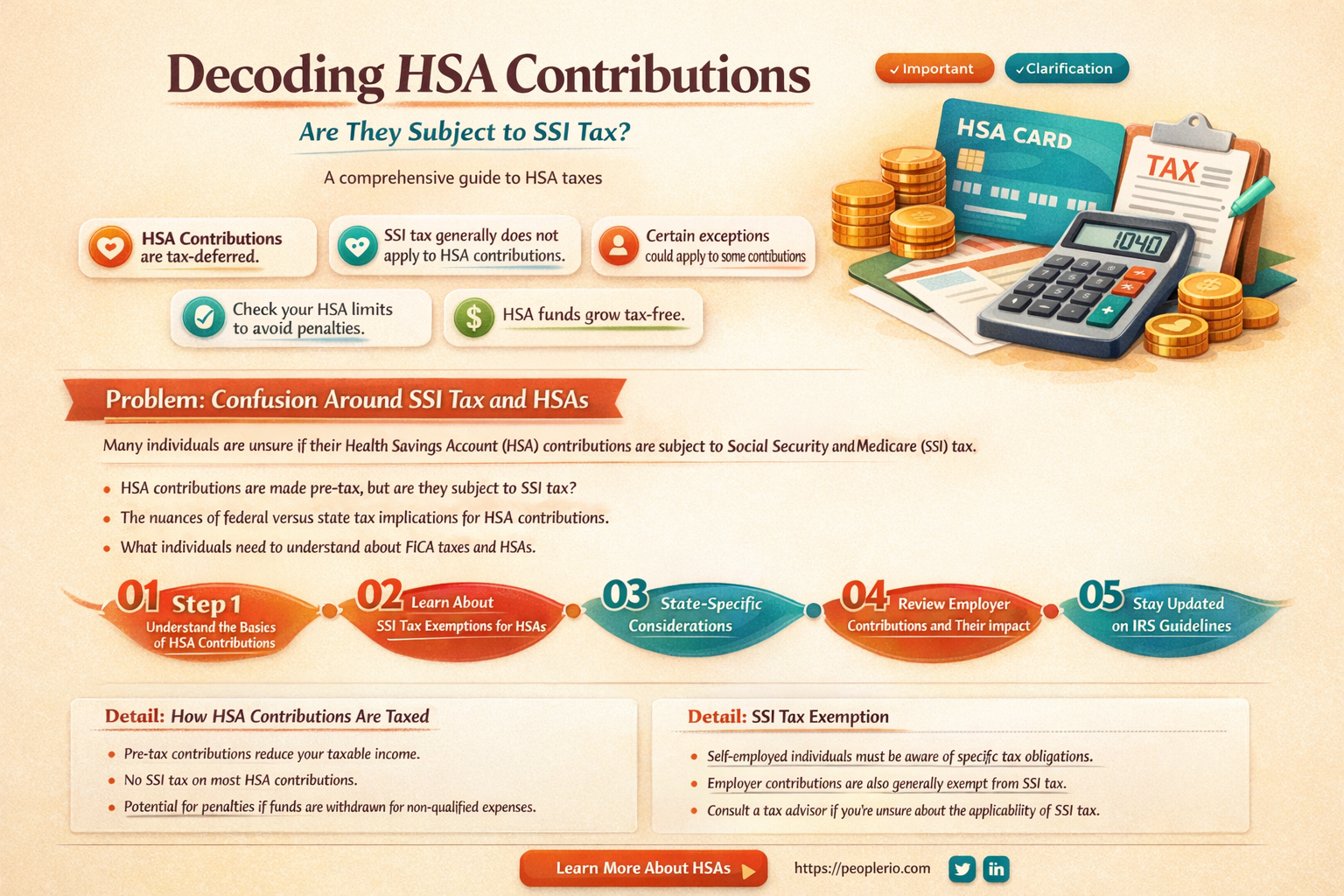

Health Savings Accounts (HSAs) are a popular benefit offered by many employers to help employees save for medical expenses. However, there's often confusion about the tax implications of these accounts, particularly regarding Social Security Income (SSI) tax. The question of whether employee HSA contributions are subject to SSI tax is an important one for both employees and employers to understand. In this article, we'll delve into the specifics of HSA contributions and their relationship with SSI tax, providing clarity on this common financial query.

| Characteristics | Values |

|---|---|

| Tax Type | SSI (Social Security Income) Tax |

| Contributions | Employee HSA (Health Savings Account) Contributions |

| Tax Applicability | Generally not subject to SSI tax |

| Exceptions | If contributions are made by an employer on behalf of the employee, they may be considered taxable income and subject to SSI tax |

| Employee Impact | Employees may need to report HSA contributions on their tax returns, but typically will not pay SSI tax on these contributions |

| Employer Impact | Employers may need to withhold SSI tax on HSA contributions made on behalf of employees |

| IRS Guidance | The IRS provides specific guidance on the tax treatment of HSA contributions, including SSI tax implications |

| State Tax Laws | State tax laws may vary, and some states may impose their own taxes on HSA contributions |

Explore related products

What You'll Learn

- Definition of HSA Contributions: Understand what constitutes HSA contributions and how they are classified for tax purposes

- SSI Tax Overview: Learn about Social Security Income (SSI) tax and how it applies to various types of income

- Tax Exemption Status: Explore whether HSA contributions are exempt from SSI tax under current tax laws

- Impact on Employees: Analyze how SSI tax on HSA contributions affects employees' overall tax liability and financial planning

- Employer Considerations: Examine the implications for employers in terms of payroll taxes and compliance with tax regulations

![]()

Definition of HSA Contributions: Understand what constitutes HSA contributions and how they are classified for tax purposes

HSA contributions refer to the amounts of money that individuals or employers deposit into a Health Savings Account (HSA). These contributions are a key component of HSA functionality, designed to help individuals save for qualified medical expenses on a tax-advantaged basis. Understanding what constitutes HSA contributions and how they are classified for tax purposes is crucial for maximizing the benefits of an HSA while ensuring compliance with IRS regulations.

Contributions to an HSA can be made by both the account holder and their employer, as well as by other individuals on behalf of the account holder. These contributions are generally considered tax-deductible, meaning they can reduce the contributor's taxable income for the year in which they are made. However, the tax treatment of HSA contributions can vary depending on the contributor's relationship to the account holder and the source of the funds.

Employer contributions to an employee's HSA are typically excluded from the employee's gross income, meaning they are not subject to federal income tax, Social Security tax, or Medicare tax. This exclusion applies whether the contributions are made as a direct deposit from the employer's payroll system or as a separate payment. Additionally, employer contributions are not considered taxable wages for purposes of calculating the employee's Social Security and Medicare taxes.

Individual contributions to one's own HSA are tax-deductible, but they are subject to certain limits. As of 2023, the annual contribution limit for individuals is $3,850, while the limit for families is $7,750. Contributions made by individuals who are 55 years old or older are eligible for an additional "catch-up" contribution of up to $1,000 per year. It is important to note that these limits are subject to change and may be adjusted for inflation in future years.

Contributions made by other individuals on behalf of the account holder, such as family members or friends, are also tax-deductible for the contributor, provided they are made directly to the HSA and not as a reimbursement for expenses already incurred. However, these contributions are subject to the same annual limits as individual contributions.

In summary, HSA contributions are a valuable tool for saving on healthcare expenses, and understanding their tax implications is essential for making the most of this benefit. By knowing the rules and limits associated with HSA contributions, individuals can optimize their savings while minimizing their tax liability.

Understanding 401k Deferrals: Are They Subject to Payroll Taxes?

You may want to see also

![]()

SSI Tax Overview: Learn about Social Security Income (SSI) tax and how it applies to various types of income

Social Security Income (SSI) tax is a federal tax that funds the Social Security program, providing financial support to retirees, disabled individuals, and children of deceased workers. Unlike Social Security taxes, which are typically withheld from wages, SSI taxes are not withheld from income but are instead calculated and paid by individuals when filing their tax returns. This tax applies to various types of income, including wages, self-employment income, and certain types of passive income.

When considering whether employee Health Savings Account (HSA) contributions are subject to SSI tax, it's important to understand the nature of HSA contributions. HSAs are tax-advantaged accounts used for saving and paying for qualified medical expenses. Contributions to an HSA are generally made on a pre-tax basis, reducing the employee's taxable income for the year. However, since SSI taxes are calculated based on income after certain deductions and adjustments, the question arises as to whether these pre-tax HSA contributions are considered when determining SSI tax liability.

The good news is that, according to the IRS, employee HSA contributions are not considered taxable income for SSI purposes. This means that when calculating SSI taxes, individuals do not need to include the amount of their HSA contributions in their income. This exclusion applies regardless of whether the HSA contributions are made by the employee or their employer, as long as they are properly reported on Form W-2.

It's worth noting that while HSA contributions are not subject to SSI tax, they can still impact other aspects of an individual's tax situation. For example, HSA contributions can affect the calculation of other taxes, such as federal income tax and state taxes, depending on the specific tax laws in the individual's state. Additionally, HSA contributions can also impact the individual's eligibility for certain tax credits and deductions.

In conclusion, employee HSA contributions are not subject to SSI tax, providing a tax advantage for individuals who contribute to these accounts. However, it's important to consider the broader tax implications of HSA contributions and to consult with a tax professional for personalized advice on how these contributions may affect an individual's overall tax situation.

Decoding Employee Tax IDs: A Comprehensive Guide for Employers

You may want to see also

![]()

Tax Exemption Status: Explore whether HSA contributions are exempt from SSI tax under current tax laws

Under current tax laws, Health Savings Account (HSA) contributions made by employees are generally not subject to Social Security Income (SSI) tax. This exemption is a significant benefit for employees who contribute to HSAs, as it reduces their overall tax liability. However, it's important to note that this exemption applies only to contributions made by the employee themselves, not to any contributions made by their employer.

The tax exemption status of HSA contributions is outlined in the Internal Revenue Code (IRC). Specifically, Section 223 of the IRC states that contributions to an HSA made by an individual are deductible from their gross income, and therefore not subject to SSI tax. This is because HSA contributions are considered a form of tax-advantaged savings, similar to contributions to a 401(k) or IRA.

In addition to being exempt from SSI tax, HSA contributions are also not subject to federal income tax, and in many cases, state income tax as well. This triple tax advantage makes HSAs a powerful tool for saving for healthcare expenses. However, it's crucial for employees to understand the rules and regulations surrounding HSA contributions to ensure they are maximizing their tax benefits while remaining compliant with the law.

One important consideration is the contribution limit. For 2023, the maximum contribution limit for individuals is $3,650, and for families, it's $7,300. Contributions above these limits are subject to a 6% excise tax. Additionally, employees should be aware that they cannot contribute to an HSA if they are enrolled in Medicare, as this would disqualify them from the tax exemption.

In conclusion, the tax exemption status of HSA contributions provides a significant benefit for employees looking to save for healthcare expenses. By understanding the rules and regulations surrounding HSA contributions, employees can make the most of this tax-advantaged savings tool while avoiding potential pitfalls.

Maximizing Deductions: Understanding Business Expenses on State Tax Returns

You may want to see also

![]()

Impact on Employees: Analyze how SSI tax on HSA contributions affects employees' overall tax liability and financial planning

The impact of SSI tax on HSA contributions can significantly affect an employee's overall tax liability and financial planning. When employees contribute to their Health Savings Accounts (HSAs), these contributions are generally considered tax-deductible, reducing their taxable income. However, the application of SSI tax to these contributions can complicate this benefit.

SSI tax, which funds Social Security and Medicare, is typically applied to wages and other forms of income. If HSA contributions are subject to SSI tax, this means that employees will need to pay an additional 6.2% (for Social Security) and 1.45% (for Medicare) on their HSA contributions, as of the current tax rates. This additional tax burden can reduce the net benefit of contributing to an HSA, as employees will need to factor in these taxes when planning their contributions.

To mitigate the impact of SSI tax on HSA contributions, employees may need to adjust their contribution strategies. For example, they might consider contributing less to their HSA to minimize the tax burden, or they might look for other tax-advantaged savings options that are not subject to SSI tax. Additionally, employees may need to consult with a tax professional to understand how SSI tax on HSA contributions interacts with other aspects of their tax situation, such as their income tax bracket and other deductions.

In terms of financial planning, the impact of SSI tax on HSA contributions can also affect employees' long-term savings goals. HSAs are often used as a retirement savings vehicle, as they offer tax-free growth and withdrawals for qualified medical expenses. However, if SSI tax is applied to contributions, this can reduce the overall growth potential of the HSA. Employees may need to reassess their retirement savings strategies and consider alternative investment options to achieve their long-term financial goals.

Overall, the application of SSI tax to HSA contributions can have a significant impact on employees' tax liability and financial planning. It is essential for employees to understand this impact and adjust their contribution strategies and financial plans accordingly to maximize their tax benefits and achieve their long-term savings goals.

Unlocking the Tax Benefits of Your 401(k) Contributions

You may want to see also

![]()

Employer Considerations: Examine the implications for employers in terms of payroll taxes and compliance with tax regulations

Employers must carefully consider the implications of employee HSA contributions on their payroll tax obligations and overall compliance with tax regulations. The IRS has specific guidelines regarding the taxability of HSA contributions, and employers need to ensure they are accurately following these rules to avoid penalties and legal issues.

One key consideration is the distinction between employer and employee contributions to HSAs. Employer contributions are generally considered taxable income to the employee, subject to federal income tax withholding and FICA taxes (Social Security and Medicare). However, employee contributions made through payroll deductions are treated differently. These contributions are made on a pre-tax basis, reducing the employee's taxable income and, consequently, the amount of payroll taxes owed.

Employers must also be aware of the annual contribution limits for HSAs, which are set by the IRS and adjusted for inflation each year. For 2023, the maximum contribution limit for individuals is $3,850, while families can contribute up to $7,750. Employers should ensure their payroll systems are updated to reflect these limits and prevent over-contributions, which could result in tax penalties for both the employer and employee.

Another important aspect is the reporting of HSA contributions on Form W-2. Employers are required to report the total HSA contributions made by both the employer and employee on the employee's W-2 form at the end of the year. This information is used by the IRS to determine the taxability of the contributions and ensure compliance with the tax code.

To maintain compliance, employers should regularly review their payroll tax filings and HSA contribution records. They should also stay informed about any changes to tax laws and regulations that may impact their obligations. By taking a proactive approach to managing HSA contributions, employers can minimize the risk of tax penalties and ensure a smooth payroll tax filing process.

Maximize Your Take-Home Pay: Tax Reduction Strategies for W2 Employees

You may want to see also

Frequently asked questions

No, employee contributions to a Health Savings Account (HSA) are not subject to Social Security Income (SSI) tax.

Employee HSA contributions are made on a pre-tax basis, which means they reduce the employee's taxable income for the year.

Yes, there are annual contribution limits for HSAs. For 2023, the limit is $3,600 for individuals and $7,200 for families.

HSA funds are portable, meaning they belong to the employee and can be taken to a new job. The employee can continue to use the funds for qualified medical expenses or save them for future use.