The question of whether employee meals are tax deductible is a common concern for businesses and employees alike, as it directly impacts financial planning and compliance with tax regulations. Generally, the tax deductibility of employee meals depends on the purpose of the meal and the context in which it is provided. For instance, meals provided for the convenience of the employer, such as those consumed during work hours or at a required business meeting, may be partially or fully deductible as a business expense. However, meals considered personal or entertainment-related often face stricter limitations or may not be deductible at all. Understanding the specific IRS guidelines and documentation requirements is crucial to ensure accurate tax reporting and maximize potential deductions while avoiding penalties.

| Characteristics | Values |

|---|---|

| General Rule | Employee meals are generally not tax deductible for employers unless specific conditions are met. |

| 100% Deductible Meals | Meals provided for the convenience of the employer (e.g., on-site meals during work hours) are 100% deductible in the U.S. (as of 2023). |

| 50% Deductible Meals | Business meals with clients, customers, or employees (e.g., dining out for work discussions) are 50% deductible in the U.S. (as of 2023). |

| De Minimis Benefits | Occasional meals (e.g., occasional lunch for employees) may qualify as de minimis benefits, which are tax-free for employees but deductible for employers. |

| On-Site Meals | Meals provided on business premises for the convenience of the employer are fully deductible and tax-free for employees. |

| Travel Meals | Meals during business travel are 50% deductible for employees and employers in the U.S. (as of 2023). |

| Documentation Required | Proper documentation (e.g., receipts, business purpose) is required to claim deductions for meals. |

| Country-Specific Rules | Tax deductibility of employee meals varies by country (e.g., Canada allows 50% deduction for business meals, while the UK has specific rules for employer-provided meals). |

| COVID-19 Temporary Rule (U.S.) | In 2021-2022, the U.S. allowed 100% deduction for restaurant meals to support the hospitality industry, but this rule expired. |

| Employee Taxation | If meals are not deductible, their value may be treated as taxable income for employees unless they qualify as de minimis benefits. |

| Company Policy Impact | Employers should have a clear meal policy to ensure compliance with tax laws and avoid audits. |

Explore related products

$7.47 $7.99

$13.52 $15.95

$22.49

What You'll Learn

- Eligibility Criteria: Rules for employee meals qualifying for tax deductions under IRS guidelines

- Business Meal Deductions: Deducting meals during business travel or client meetings

- On-Site Meal Benefits: Tax implications of providing meals at the workplace

- Documentation Requirements: Records needed to claim meal deductions accurately

- Percentage Limitations: IRS-allowed deduction percentages for employee meal expenses

![]()

Eligibility Criteria: Rules for employee meals qualifying for tax deductions under IRS guidelines

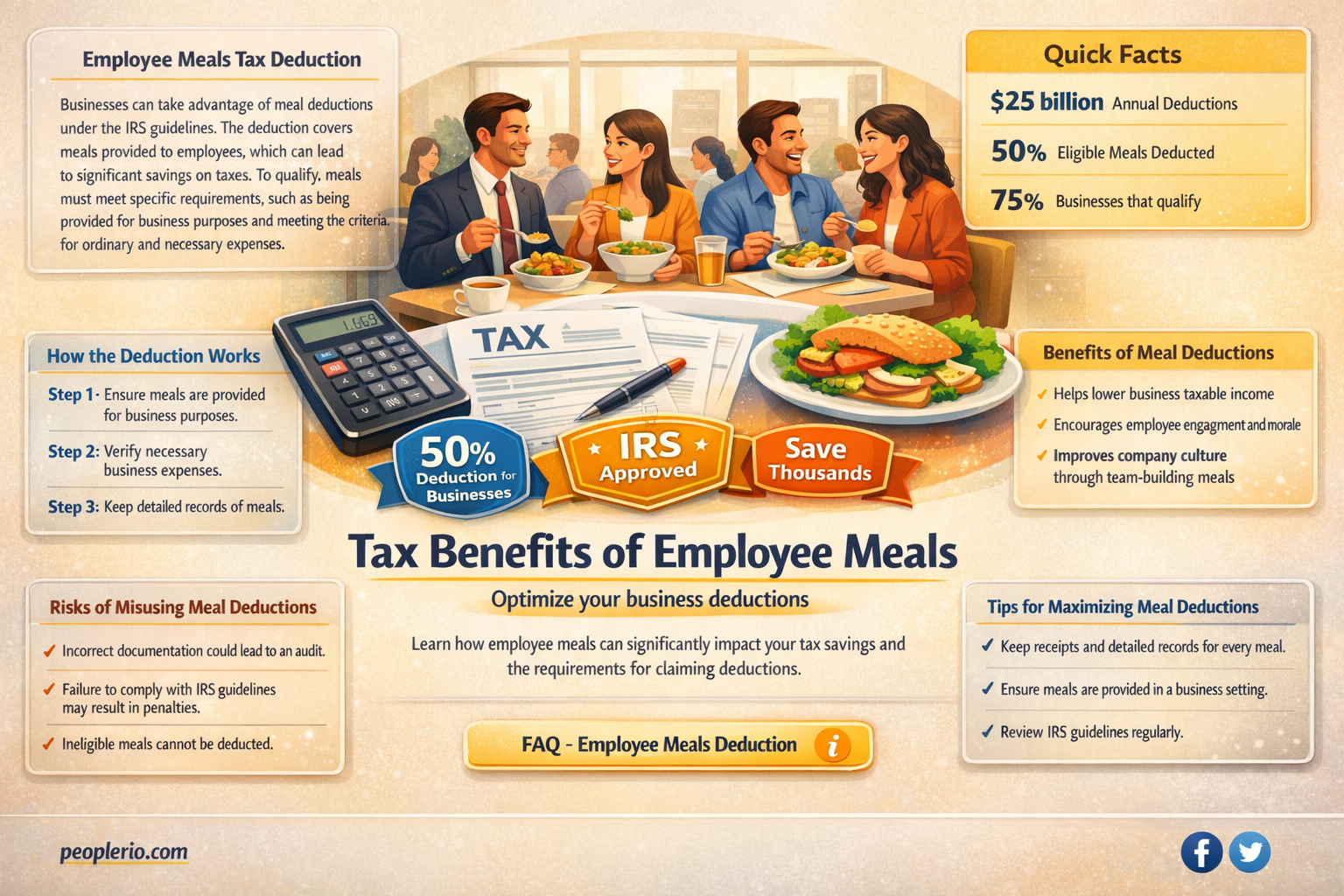

Understanding the eligibility criteria for employee meals to qualify for tax deductions under IRS guidelines is crucial for businesses aiming to maximize their tax benefits while staying compliant. The IRS has specific rules that determine whether a meal expense can be deducted, and these rules hinge on the purpose, timing, and nature of the meal. For instance, meals provided for the convenience of the employer—such as those consumed during overtime work when the employee cannot leave the premises—are generally 50% deductible. However, meals that qualify as de minimis fringe benefits, like occasional snacks or coffee, may be fully deductible if they are provided on the employer’s premises and are not compensatory in nature.

To qualify for a deduction, the meal must serve a legitimate business purpose. This means it should be directly related to the employer’s convenience or necessary for the employee to perform their job effectively. For example, meals provided during business travel or at mandatory training sessions typically meet this criterion. However, meals consumed during social events or personal breaks generally do not qualify unless they are incidental to a business meeting. The IRS also requires detailed record-keeping, including the date, location, business purpose, and amount spent, to substantiate the deduction.

One critical rule is the distinction between meals provided on-premises versus off-premises. Meals consumed on the employer’s premises, such as in a company cafeteria or during overtime shifts, are more likely to qualify for deductions. In contrast, off-premises meals, like those at restaurants, face stricter scrutiny and must be directly tied to business activities, such as client meetings or travel. Additionally, the IRS limits the deduction for meal expenses to 50% of the cost, unless the meal falls under specific exceptions, such as those provided by certain industries like trucking or construction.

Employers must also be cautious about the frequency and nature of meal provisions. Regular, daily meals for employees may not qualify unless they meet the "convenience of the employer" test. For instance, providing lunch every day simply as a perk does not meet this standard. However, occasional meals during extended work hours or in situations where employees cannot leave the workplace are more likely to qualify. It’s essential to evaluate each meal provision on a case-by-case basis to ensure compliance with IRS rules.

In summary, qualifying employee meals for tax deductions requires a clear understanding of IRS guidelines, meticulous record-keeping, and a focus on the business purpose of the meal. By adhering to these eligibility criteria, businesses can optimize their tax benefits while avoiding potential audits or penalties. Always consult IRS Publication 15-B or a tax professional for specific guidance tailored to your situation.

Maximize Your Take-Home Pay: Tax Reduction Strategies for W2 Employees

You may want to see also

Explore related products

![]()

Business Meal Deductions: Deducting meals during business travel or client meetings

Business meals can be a gray area in tax deductions, but understanding the rules can save your company significant money. The IRS allows deductions for meals that are both "ordinary and necessary" in the context of conducting business. For meals during business travel or client meetings, this means the expense must be directly related to the active conduct of your trade or business. For instance, a sales representative dining with a potential client to discuss a contract would qualify, as the meal is integral to the business discussion. However, a team lunch to boost morale, while beneficial, typically does not meet this criterion unless it’s tied to a specific business purpose.

To maximize deductions, documentation is key. Keep detailed records of the date, location, attendees, business purpose, and cost of each meal. For example, a receipt from a restaurant with a handwritten note like "Discussed Q3 marketing strategy with Client X" can provide the necessary context to satisfy IRS scrutiny. Additionally, ensure the expense is reasonable. A $500 dinner for two might raise red flags unless it’s justified by the business context, such as entertaining a high-value client in a premium setting. The IRS generally allows 50% of the meal cost as a deduction, so plan accordingly.

One common pitfall is confusing social meals with business meals. While taking a client to a baseball game and dinner afterward might seem like a good idea, the IRS distinguishes between entertainment and business meals. The meal portion may be deductible if it’s clearly separated from the entertainment activity and has a specific business purpose. For example, discussing a deal over dinner before the game would qualify, but snacks during the game would not. This distinction requires careful planning and documentation to ensure compliance.

For business travel, meals are often easier to deduct because the travel itself establishes a business purpose. However, the rules differ for same-day trips versus overnight stays. If an employee travels to another city for a conference and dines with colleagues to discuss industry trends, the meal is deductible. But if the travel is local—say, a commute to a nearby client site—the meal might not qualify unless it’s directly tied to a specific business activity. Always consider the context and purpose to ensure eligibility.

Finally, stay updated on tax law changes, as regulations can shift. For example, the Tax Cuts and Jobs Act of 2017 eliminated deductions for entertainment expenses but retained them for business meals. Consulting a tax professional can provide clarity, especially for complex scenarios. By understanding these nuances, businesses can confidently deduct eligible meals, turning what might seem like an expense into a strategic investment in growth.

Smart Tax Strategies: How a W2 Employee Reduced His Taxes

You may want to see also

Explore related products

![]()

On-Site Meal Benefits: Tax implications of providing meals at the workplace

Providing on-site meals to employees can be a valuable perk, but it’s not as simple as setting up a cafeteria. From a tax perspective, the deductibility of these meals hinges on whether they qualify as a business expense or a taxable fringe benefit. The IRS has clear guidelines: meals provided for the convenience of the employer—such as those enabling employees to work through lunch or stay late—are generally 50% deductible. However, if meals are offered as a fringe benefit (e.g., free lunches for all employees regardless of work demands), they may be fully taxable to the employer and included in employees’ wages. Understanding this distinction is critical to avoid unexpected tax liabilities.

For employers, structuring meal programs to maximize tax benefits requires careful planning. For instance, if employees are required to be on-site during meals due to the nature of their work (e.g., manufacturing or healthcare), the meals are more likely to qualify as a deductible business expense. Documentation is key: maintain records showing that meals are provided primarily for business convenience, not as a general perk. Additionally, consider timing and accessibility. Meals served during mandatory shifts or in areas where employees cannot easily leave the premises strengthen the case for deductibility.

A comparative analysis reveals that industries with 24/7 operations, like tech or healthcare, often benefit most from on-site meal deductions. For example, a hospital providing meals to nurses during 12-hour shifts can likely deduct 50% of the cost, as the meals enable uninterrupted patient care. In contrast, a tech startup offering free lunches as a recruitment tool may face taxable fringe benefit treatment. The takeaway? Align meal programs with operational needs, not just employee satisfaction, to optimize tax outcomes.

Practical tips can further enhance compliance and savings. First, consult a tax professional to tailor your meal program to your industry and workforce. Second, track meal expenses separately and ensure they are reasonable in cost—lavish meals may trigger additional scrutiny. Finally, communicate the purpose of the meal program to employees. Framing it as a business necessity rather than a perk can reinforce its tax-deductible status. By strategically designing and documenting on-site meal benefits, employers can provide value to employees while minimizing tax exposure.

Are Employee Salaries Tax Deductible? A Business Owner's Guide

You may want to see also

Explore related products

![]()

Documentation Requirements: Records needed to claim meal deductions accurately

To claim meal deductions accurately, meticulous record-keeping is non-negotiable. The IRS requires detailed documentation to substantiate each expense, ensuring it meets the criteria of being ordinary, necessary, and directly related to business. Without proper records, deductions can be disallowed, leading to penalties or audits. This isn’t merely about saving receipts; it’s about creating a clear, audit-proof trail that links every meal expense to a legitimate business purpose.

Step 1: Capture the Essentials

For each meal, record the date, amount spent, location, and type of expense (e.g., lunch, dinner). Include the names and titles of attendees if the meal involves clients, vendors, or employees. For example, a receipt for a $45 dinner should be accompanied by a note stating, “Discussed Q4 marketing strategy with client John Doe, Marketing Director.” This level of detail ensures the expense is tied to a specific business activity, not personal consumption.

Step 2: Prove the Business Purpose

Beyond receipts, maintain a log or journal that explains the business reason for the meal. For instance, if an employee travels for work and purchases a $12 lunch, the record should note, “Lunch during site visit to resolve equipment malfunction at Chicago branch.” This documentation bridges the gap between the expense and its business necessity, a critical requirement for deductions.

Step 3: Leverage Digital Tools

Modern expense-tracking apps like Expensify or QuickBooks can streamline documentation. These tools allow employees to upload receipts, add notes, and categorize expenses in real time. For example, a manager attending a conference could snap a photo of a $30 dinner receipt, tag it as “business travel,” and add a memo about networking with industry peers. Such digital records are not only efficient but also reduce the risk of lost paper receipts.

Caution: Avoid Common Pitfalls

Incomplete or vague records are red flags. For instance, a receipt labeled “Dinner – $60” without context fails to demonstrate business intent. Similarly, lumping multiple expenses into one entry (e.g., combining meals with entertainment) complicates the audit process. Always separate meal expenses from other costs and ensure each entry is standalone and clear.

Accurate meal deductions hinge on thorough, organized documentation. By combining detailed receipts, descriptive logs, and digital tools, businesses can confidently claim eligible expenses while minimizing audit risks. Remember, the goal isn’t just to save money—it’s to maintain compliance and transparency in every financial decision.

Understanding Household Employees: Tax Implications and Responsibilities Explained

You may want to see also

Explore related products

![]()

Percentage Limitations: IRS-allowed deduction percentages for employee meal expenses

The IRS imposes strict percentage limitations on deductible employee meal expenses, a critical detail for businesses aiming to maximize tax benefits while staying compliant. These limits, currently set at 50% for most meal expenses, mean that only half of the cost qualifies for deduction. This rule applies whether the meals are provided during business travel, at company events, or as part of employee benefits. For instance, if a company spends $10,000 on employee meals annually, only $5,000 can be deducted, reducing taxable income by that amount. Understanding this limitation is essential for accurate financial planning and tax reporting.

Analyzing the rationale behind the 50% rule reveals the IRS’s intent to balance legitimate business deductions with potential personal benefits. Meals inherently serve both business and personal purposes, and the percentage limitation ensures taxpayers don’t exploit the deduction for non-business-related expenses. For example, a company lunch meeting clearly serves a business purpose, but the IRS acknowledges that employees also derive personal value from the meal. The 50% cap reflects this duality, encouraging businesses to document expenses carefully and allocate costs appropriately.

One exception to the 50% rule is worth noting: meals provided for the convenience of the employer. If meals are furnished on business premises and meet specific IRS criteria, they may qualify for a 100% deduction under de minimis fringe benefits. This exception often applies to industries like manufacturing or healthcare, where employees work long shifts and on-site meals enhance productivity. For instance, a hospital providing meals for nurses during 12-hour shifts could deduct the full cost, provided the meals are consumed on-site and during work hours.

To navigate these percentage limitations effectively, businesses should adopt practical strategies. First, maintain detailed records distinguishing meal expenses by purpose (e.g., travel vs. on-site meals). Second, leverage accounting software that automatically applies the 50% limitation to eligible expenses, reducing errors. Third, consult a tax professional to identify opportunities for 100% deductions under specific circumstances. For example, a tech startup hosting a weekend hackathon could deduct meals at 100% if they meet the IRS’s “convenience of the employer” criteria.

In conclusion, mastering the IRS’s percentage limitations on employee meal deductions requires a blend of awareness, documentation, and strategic planning. By understanding the 50% rule, its exceptions, and practical compliance tips, businesses can optimize their tax savings while avoiding penalties. Whether deducting travel meals or on-site employee lunches, precision in expense categorization and reporting is key to unlocking the full potential of this tax benefit.

Understanding California Disability Employee Tax: A Comprehensive Guide

You may want to see also

Frequently asked questions

Employee meals may be tax deductible if they meet specific IRS criteria, such as being ordinary and necessary for the business, directly related to business activities, and not considered a personal expense.

Yes, meals provided during work hours, such as those for employees working overtime or at a remote job site, can often be deducted as a business expense, typically up to 50% of the cost.

Yes, meals provided at company events or holiday parties are generally 100% tax deductible as long as they are primarily for the benefit of employees and not lavish or extravagant.