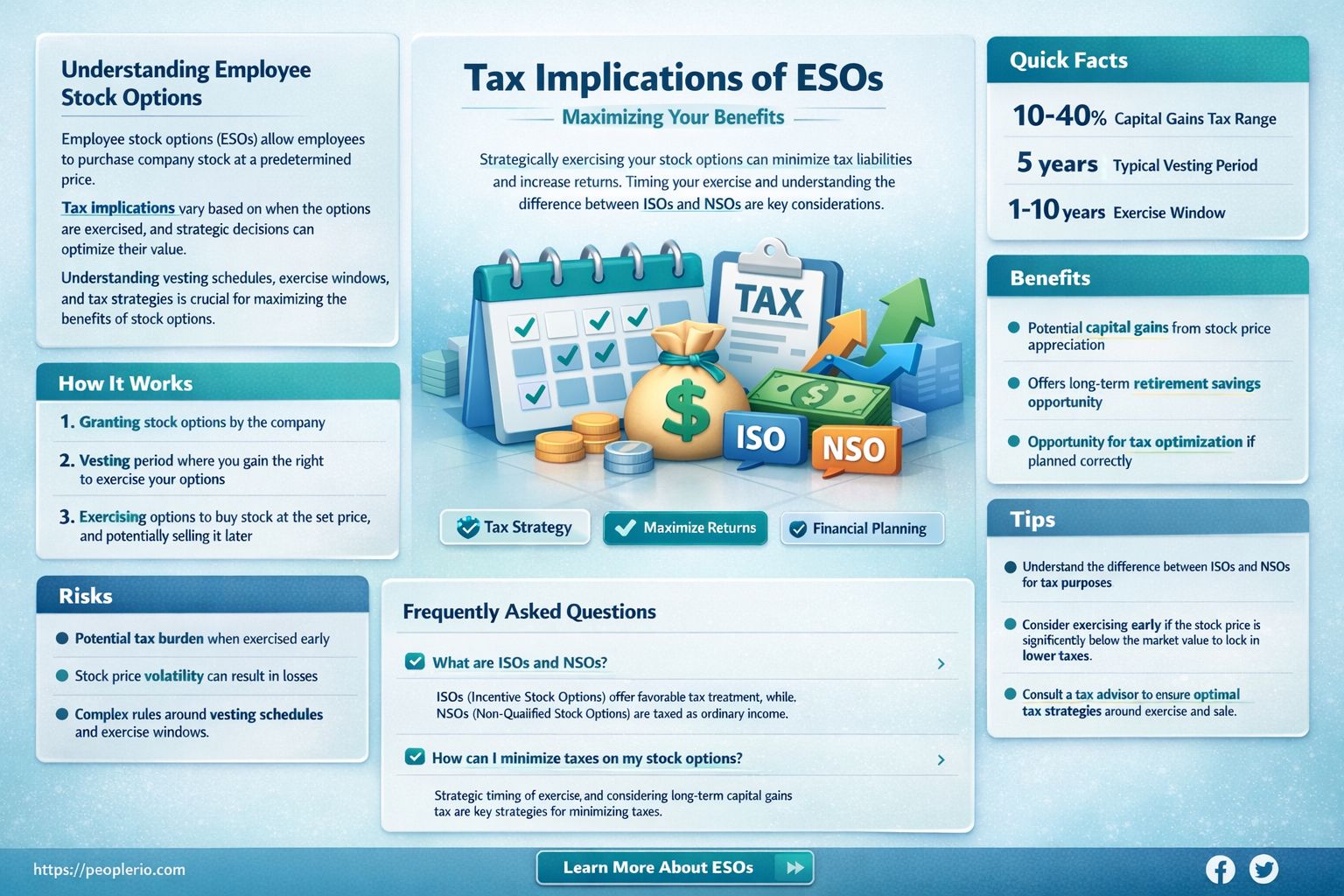

Employee stock options (ESOs) are a popular form of compensation offered by companies to attract and retain talent, allowing employees to purchase company shares at a predetermined price, typically at a discount. However, understanding the tax implications of ESOs is crucial, as they can significantly impact an employee’s financial outcomes. Taxation of ESOs varies depending on the type of option—whether it is an incentive stock option (ISO) or a non-qualified stock option (NSO)—and the timing of when the options are exercised and sold. Generally, ISOs may qualify for more favorable tax treatment, with potential long-term capital gains rates, while NSOs are taxed as ordinary income at the time of exercise. Additionally, the alternative minimum tax (AMT) may apply to ISOs if the spread between the exercise price and the fair market value is substantial. Proper planning and consultation with a tax professional are essential to navigate these complexities and optimize tax efficiency when dealing with employee stock options.

What You'll Learn

- Taxation at Grant: Generally, no tax is due when options are granted, unless the options have a readily ascertainable fair market value

- Taxation at Exercise: Tax treatment depends on whether the options are incentive stock options (ISOs) or non-qualified stock options (NSOs)

- Alternative Minimum Tax (AMT): Exercising ISOs can trigger AMT, requiring additional tax calculations and potential payments

- Taxation at Sale: Capital gains tax applies when shares are sold, based on holding period and profit

- Withholding Requirements: Employers may withhold taxes at exercise or sale, depending on the option type and jurisdiction

![]()

Taxation at Grant: Generally, no tax is due when options are granted, unless the options have a readily ascertainable fair market value

Employee stock options are a common form of compensation, yet their tax implications can be complex. At the grant stage, the general rule is straightforward: no tax is due. This principle hinges on the fact that the options themselves do not yet represent realized income. However, this rule is not absolute. If the options have a "readily ascertainable fair market value," an exception arises, and taxation may apply immediately. This scenario is rare but critical to understand, as it can significantly impact an employee’s financial planning.

To grasp this exception, consider the nature of "readily ascertainable fair market value." This term refers to situations where the value of the options can be determined with reasonable accuracy at the time of grant. For instance, if the options are for publicly traded stock, their value is easily calculated based on the current market price. Similarly, if the options are for stock in a company with a recent, arm’s-length transaction (e.g., a funding round), the value may be ascertainable. In such cases, the difference between the option’s exercise price and its fair market value is treated as taxable income at grant, subject to ordinary income tax and payroll taxes.

The practical takeaway is that most employees need not worry about taxation at grant, as their options typically lack a readily ascertainable fair market value. However, caution is warranted for employees of publicly traded companies or startups with recent valuations. For example, if an employee receives options in a private company that just completed a Series A round at a $50 million valuation, the options’ value might be considered ascertainable. Consulting a tax professional in such cases is advisable to ensure compliance and avoid unexpected tax liabilities.

From a strategic perspective, understanding this rule allows employees to focus on long-term financial planning rather than immediate tax concerns. By deferring taxation until the options are exercised or sold, employees can align their tax obligations with potential gains. This deferral is particularly beneficial for those in high tax brackets, as it allows them to manage their income recognition over time. However, it also underscores the importance of tracking the options’ value and staying informed about changes in tax laws that could alter this treatment.

In summary, while taxation at grant is generally not an issue for employee stock options, the exception for options with a readily ascertainable fair market value demands attention. Employees, especially those in companies with recent valuations or publicly traded stock, should remain vigilant. By understanding this nuance, individuals can navigate the complexities of stock option taxation more effectively, ensuring they maximize their financial benefits while remaining compliant with tax regulations.

Tax-Free Employee Gifts: What Employers Need to Know

You may want to see also

![]()

Taxation at Exercise: Tax treatment depends on whether the options are incentive stock options (ISOs) or non-qualified stock options (NSOs)

The tax implications of exercising employee stock options hinge critically on whether they are classified as Incentive Stock Options (ISOs) or Non-Qualified Stock Options (NSOs). At the moment of exercise, ISOs generally do not trigger immediate taxation, provided the employee adheres to specific holding period requirements. This means no ordinary income tax or payroll taxes are due when the option is exercised, offering a potential tax advantage. Conversely, NSOs are taxed at exercise as ordinary income, based on the difference between the exercise price and the fair market value of the stock at that time. This distinction underscores the importance of understanding the type of options held before making any decisions.

Consider a scenario where an employee exercises ISOs to purchase 1,000 shares at $10 each, with the current market value at $50 per share. Despite the $40,000 spread between the exercise price and market value, no tax is owed at exercise. However, if the same scenario involved NSOs, the employee would face ordinary income tax on $40,000, plus payroll taxes, significantly impacting their immediate tax liability. This example highlights the stark difference in tax treatment between the two types of options at the exercise stage.

While ISOs offer a tax deferral at exercise, they come with a trade-off known as the Alternative Minimum Tax (AMT). If the spread between the exercise price and market value exceeds certain thresholds, it may trigger AMT liability in the year of exercise. For instance, if the spread is $50,000 and the employee’s income places them in a higher tax bracket, they could face AMT, effectively reducing the immediate tax benefit of ISOs. NSOs, on the other hand, avoid AMT complications but require careful planning to manage the ordinary income tax burden.

To navigate these complexities, employees should consult a tax advisor to strategize around the timing of exercise and potential tax liabilities. For ISOs, holding the shares for at least one year post-exercise and two years post-grant can qualify the gain for long-term capital gains treatment, further optimizing tax efficiency. For NSOs, coordinating exercise with other income sources or utilizing tax-advantaged accounts can mitigate the immediate tax impact. Understanding these nuances ensures employees maximize the value of their stock options while minimizing unexpected tax consequences.

Are Employee Salaries Tax Deductible? A Business Owner's Guide

You may want to see also

![]()

Alternative Minimum Tax (AMT): Exercising ISOs can trigger AMT, requiring additional tax calculations and potential payments

Exercising Incentive Stock Options (ISOs) can feel like a financial windfall, but it also opens a Pandora’s box of tax complexities, particularly the Alternative Minimum Tax (AMT). Unlike regular income tax, AMT operates as a parallel system designed to ensure high earners pay a minimum amount of tax, regardless of deductions. When you exercise ISOs, the difference between the strike price and the fair market value (the "bargain element") isn’t taxed for regular income purposes, but it’s treated as an AMT adjustment, potentially pushing you into AMT territory.

Here’s how it works: Suppose you exercise 10,000 ISOs with a strike price of $10 each, and the current market value is $50. The bargain element is $400,000 ($40 x 10,000). This amount increases your AMT income, and if the resulting AMT liability exceeds your regular tax liability, you owe the difference. For example, if your regular tax is $50,000 and your AMT calculation yields $70,000, you’d owe an additional $20,000 in AMT. This can be a shock, especially if you haven’t sold the shares and don’t have cash on hand to cover the tax bill.

To mitigate AMT risk, consider exercising ISOs in smaller batches or in years with lower income. Alternatively, if you’re confident the stock will appreciate further, you might exercise and immediately sell enough shares to cover the AMT liability (a "same-day sale"). However, this disqualifies the sale from ISO tax treatment, subjecting it to ordinary income tax instead of the more favorable long-term capital gains rate. Weighing these options requires careful planning and often consultation with a tax professional.

A critical takeaway is that AMT doesn’t disappear when you eventually sell the ISO shares. If you hold them long enough to qualify for long-term capital gains treatment, the spread at sale is taxed at a lower rate, but the AMT credit you may have accumulated from the exercise year can offset future tax liabilities. For instance, if you paid $20,000 in AMT upon exercise and later sell the shares, you could claim this credit in subsequent years, effectively recouping some of the tax paid.

In essence, while ISOs offer significant upside, their AMT implications demand proactive strategy. Ignoring this parallel tax system can lead to unexpected liabilities, but with careful planning, you can navigate its complexities and maximize your financial gains. Always model different scenarios with a tax advisor to understand the full impact of exercising ISOs on your tax situation.

Are Employee Bonuses Tax Deductible? A Comprehensive Guide for Employers

You may want to see also

![]()

Taxation at Sale: Capital gains tax applies when shares are sold, based on holding period and profit

When employees exercise stock options and eventually sell the acquired shares, the tax implications shift to capital gains tax, a critical aspect often overlooked in the excitement of potential profits. This tax is not a flat rate but a nuanced calculation based on two key factors: the holding period of the shares and the profit realized from the sale. Understanding this mechanism is essential for anyone looking to maximize their after-tax gains from employee stock options.

The holding period, or how long the shares are held after exercise, determines whether the capital gain is classified as short-term or long-term. Short-term capital gains apply to shares held for one year or less and are taxed at ordinary income tax rates, which can be as high as 37% in the U.S., depending on the taxpayer’s income bracket. In contrast, long-term capital gains, for shares held over one year, benefit from reduced tax rates, typically ranging from 0% to 20%, depending on taxable income. For instance, a single taxpayer with a taxable income of $40,000 would pay 0% on long-term capital gains, while someone earning $450,000 could face a 20% rate. This distinction highlights the importance of timing in selling shares to optimize tax efficiency.

The profit realized from the sale, calculated as the selling price minus the exercise price and any associated costs, directly influences the capital gains tax amount. For example, if an employee exercises options at $10 per share, holds them for over a year, and sells them at $50, the long-term capital gain is $40 per share. At a 15% long-term capital gains rate, the tax would be $6 per share, leaving a net gain of $34. Conversely, if sold within a year, the gain might be taxed at a 32% ordinary income rate, reducing the net gain to $27.20 per share. This example underscores how holding period and profit interplay to shape the final tax liability.

Practical tips for managing capital gains tax include strategic timing of sales to qualify for long-term rates, especially for high-income earners. Additionally, taxpayers can offset capital gains with capital losses from other investments, reducing overall tax liability. For those with complex financial situations, consulting a tax advisor can provide tailored strategies, such as tax-loss harvesting or charitable donations of appreciated stock, to further minimize taxes. By proactively planning for the sale of shares, employees can retain more of their hard-earned profits and align their financial goals with tax efficiency.

Employee Gifts and Taxes: What's Deductible for Your Business?

You may want to see also

![]()

Withholding Requirements: Employers may withhold taxes at exercise or sale, depending on the option type and jurisdiction

Employers face a critical decision when it comes to withholding taxes on employee stock options: whether to deduct taxes at the time of exercise or upon sale. This choice hinges on the type of option—incentive stock options (ISOs) or non-qualified stock options (NSOs)—and the jurisdiction’s tax laws. For NSOs, taxation occurs at exercise, making withholding at that point mandatory in many countries, including the U.S., where employers must withhold income and payroll taxes. ISOs, however, are more complex; while no tax is due at exercise, employers may still choose to withhold taxes at sale to avoid future complications. Understanding these nuances is essential for compliance and employee clarity.

Consider the U.S. scenario: if an employee exercises NSOs and the fair market value of the shares exceeds the exercise price, the difference is taxed as ordinary income. Employers are required to withhold federal income tax (up to 37% as of 2023), Social Security (6.2%), and Medicare (1.45%), totaling up to 44.65% in federal withholdings alone. State and local taxes may further increase this burden. For ISOs, while no tax is due at exercise, a disqualifying disposition (selling shares before meeting holding period requirements) triggers ordinary income tax at sale, necessitating careful withholding strategies to avoid underpayment penalties.

Internationally, withholding requirements vary dramatically. In the UK, employers must withhold income tax and National Insurance contributions (NICs) at exercise for NSOs, with rates ranging from 20% to 45% for income tax and 13.8% for NICs. In contrast, Canada treats stock options more favorably, allowing a 50% deduction on the benefit realized at exercise, effectively halving the taxable amount. Employers in these jurisdictions must navigate local laws to ensure accurate withholding, often consulting tax advisors to avoid costly errors.

A practical tip for employers is to communicate withholding policies clearly to employees. For instance, if withholding occurs at exercise, employees should be informed of the potential tax impact on their take-home pay. If withholding is deferred to sale, employers should emphasize the need for employees to set aside funds to cover future tax liabilities. Tools like tax calculators or partnerships with financial advisors can help employees plan effectively. Transparency not only fosters trust but also reduces administrative headaches related to tax disputes.

Ultimately, withholding requirements are a balancing act between compliance and employee satisfaction. Employers must weigh the administrative burden of withholding at exercise against the risk of underpayment penalties if deferred to sale. For ISOs, proactive withholding at sale can mitigate risks, especially in jurisdictions with strict tax enforcement. By staying informed and adopting a strategic approach, employers can navigate this complex landscape, ensuring both legal adherence and employee financial well-being.

Understanding Household Employees: Tax Implications and Responsibilities Explained

You may want to see also

Frequently asked questions

Employee stock options are generally taxed at two points: when you exercise the options (if they are non-qualified stock options, or NSOs) and when you sell the shares. Incentive stock options (ISOs) may trigger a tax event at the time of sale, depending on how long you hold the shares.

NSOs are taxed as ordinary income at the time of exercise, based on the difference between the fair market value of the stock and the exercise price. This amount is also subject to payroll taxes (Social Security and Medicare).

ISOs are not taxed at the time of exercise, but the difference between the fair market value and the exercise price may trigger an alternative minimum tax (AMT) liability. If you hold the shares for at least one year from exercise and two years from grant (qualifying disposition), the gain is taxed as long-term capital gains when sold.

If you sell the shares immediately after exercising, it’s considered a disqualifying disposition for ISOs, and the gain is taxed as ordinary income. For NSOs, selling immediately doesn’t change the tax treatment since they’re already taxed at exercise, but any additional gain or loss is taxed as short-term capital gains or losses.