Employee pension contributions are a crucial aspect of retirement planning, and understanding how they are taxed can significantly impact one's financial strategy. In many countries, pension contributions are deducted from an employee's gross salary before income tax is applied, offering a tax-efficient way to save for retirement. This pre-tax deduction reduces the employee's taxable income, potentially lowering their overall tax liability. However, it's important to note that the tax treatment of pension contributions can vary by jurisdiction and may be subject to specific rules and limits. Employees should consult their country's tax laws or a financial advisor to fully understand the implications of their pension contributions on their tax situation.

| Characteristics | Values |

|---|---|

| Deduction Timing | Before tax |

| Contribution Type | Employee pension contributions |

| Tax Treatment | Contributions are tax-deductible |

| Impact on Taxable Income | Reduces taxable income |

| Benefit | Lower tax liability for the employee |

| Employer Involvement | Employer may also contribute |

| Vesting Period | Contributions may have a vesting period |

| Withdrawal Rules | Subject to specific withdrawal rules and penalties |

| Investment Options | May be invested in various financial instruments |

| Retirement Planning | Helps in building retirement savings |

Explore related products

What You'll Learn

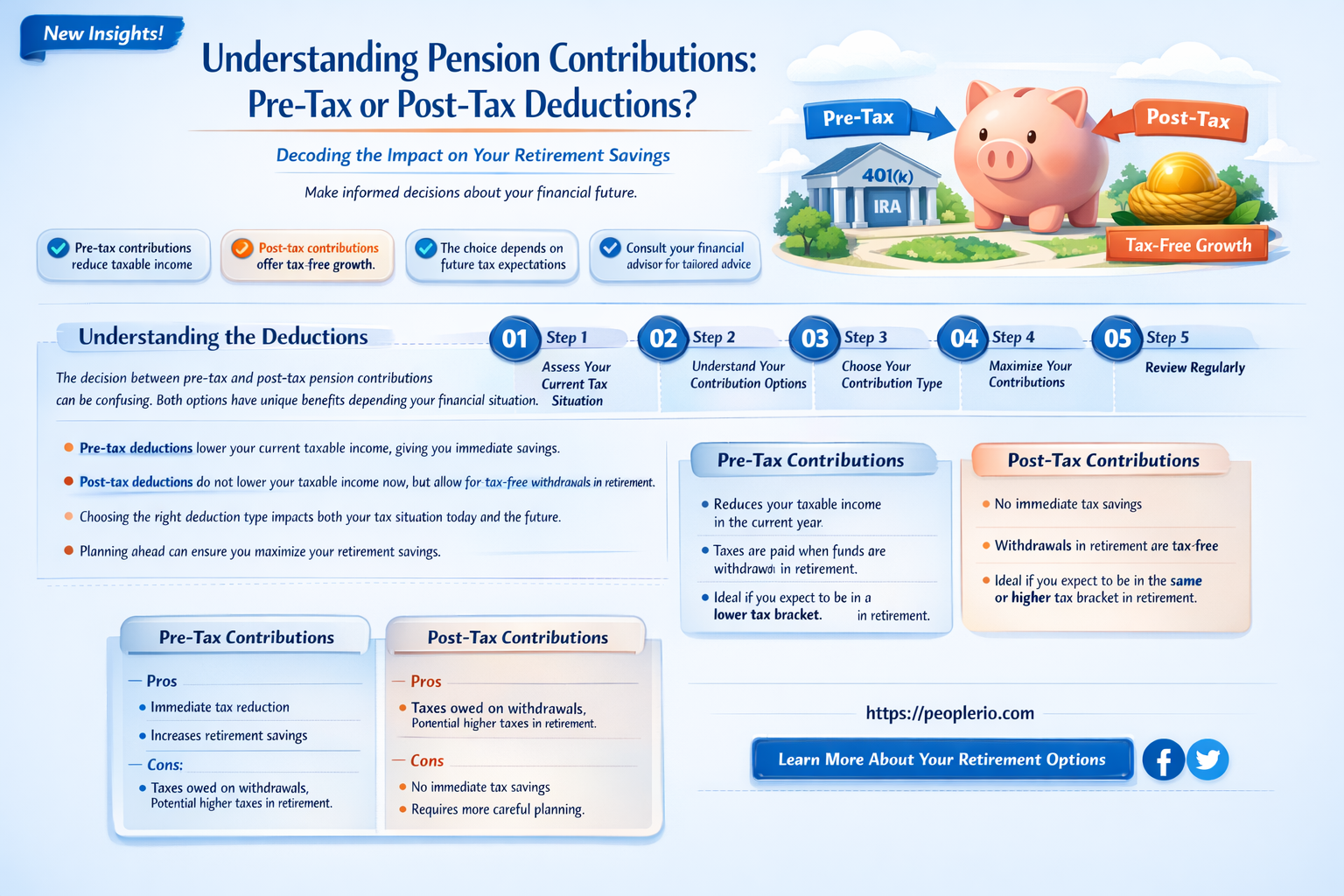

- Pre-tax deductions: Contributions made before taxes, reducing taxable income

- Post-tax deductions: Contributions made after taxes, no impact on taxable income

- Tax benefits: Pre-tax contributions offer immediate tax relief, lowering tax liability

- Net pay impact: Pre-tax deductions reduce net pay less than post-tax deductions

- Employer contributions: Employers may also contribute, often matching employee pre-tax contributions

![]()

Pre-tax deductions: Contributions made before taxes, reducing taxable income

Pre-tax deductions are a critical component of employee pension contributions, as they allow individuals to reduce their taxable income before taxes are applied. This can result in significant savings over time, as the contributions are not subject to income tax. For example, if an employee contributes $5,000 to their pension plan before taxes, their taxable income would be reduced by $5,000, resulting in a lower tax bill.

One of the key benefits of pre-tax deductions is that they can help employees save more for retirement without feeling the pinch in their take-home pay. Since the contributions are deducted before taxes, the employee does not have to pay income tax on the contributed amount, which can add up to substantial savings over the course of their career. Additionally, pre-tax deductions can help employees reach their retirement savings goals more quickly, as the contributions are not subject to the same tax rates as regular income.

However, it is important to note that pre-tax deductions are not without their limitations. For instance, there are typically caps on the amount that can be contributed to a pension plan on a pre-tax basis. In the United States, for example, the contribution limit for 2022 is $19,500 for individuals under the age of 50, and $26,000 for those 50 and older. Additionally, pre-tax deductions may not be available to all employees, as some employers may not offer this benefit.

Another consideration is that pre-tax deductions can impact an employee's eligibility for certain government benefits, such as Social Security and Medicare. Since these benefits are based on an individual's taxable income, reducing taxable income through pre-tax deductions may result in lower benefit payments. Therefore, it is essential for employees to carefully consider the implications of pre-tax deductions on their overall financial situation before making contributions.

In conclusion, pre-tax deductions can be a valuable tool for employees looking to save for retirement, as they allow individuals to reduce their taxable income and save more without feeling the impact in their take-home pay. However, it is crucial to be aware of the limitations and potential implications of pre-tax deductions on government benefits and overall financial planning. By understanding these factors, employees can make informed decisions about their pension contributions and maximize their savings for retirement.

Understanding Tax Rates for 1099 Employees: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Post-tax deductions: Contributions made after taxes, no impact on taxable income

Contributions made after taxes, such as certain types of employee pension contributions, do not reduce taxable income. This is in contrast to pre-tax deductions, which are subtracted from gross income before taxes are calculated. Post-tax deductions are subtracted from after-tax income, meaning they do not affect the amount of income subject to taxation.

One example of a post-tax deduction is the employee contribution to a traditional IRA (Individual Retirement Account). These contributions are made with after-tax dollars, and while they do not reduce taxable income, they can still provide tax benefits in the form of tax-deferred growth and potential tax deductions for the contributions themselves.

Another example is the employee contribution to a Roth 401(k) plan. Similar to a Roth IRA, contributions to a Roth 401(k) are made with after-tax dollars and do not reduce taxable income. However, the earnings on these contributions grow tax-free, and qualified distributions can be made tax-free as well.

It's important to note that while post-tax deductions do not reduce taxable income, they can still be beneficial for retirement savings and other financial goals. By understanding the differences between pre-tax and post-tax deductions, individuals can make informed decisions about their retirement contributions and overall financial planning.

Decoding Employee Tax IDs: A Comprehensive Guide for Employers

You may want to see also

Explore related products

![]()

Tax benefits: Pre-tax contributions offer immediate tax relief, lowering tax liability

Pre-tax contributions to employee pension plans offer a significant advantage by reducing taxable income. This immediate tax relief can lower an individual's tax liability, resulting in higher take-home pay. For instance, if an employee contributes $5,000 pre-tax to their pension plan, their taxable income is reduced by the same amount, potentially saving them hundreds or even thousands of dollars in taxes, depending on their tax bracket.

One of the key benefits of pre-tax contributions is the ability to defer taxes until retirement. When the funds are withdrawn during retirement, they are taxed at the retiree's current tax rate, which is often lower than their working-age tax rate. This tax deferral can lead to substantial savings over time. Additionally, pre-tax contributions can help individuals maximize their retirement savings by allowing them to contribute more to their pension plans without feeling the immediate tax impact.

Employers also benefit from pre-tax contributions, as they can deduct the contributions from their taxable income, reducing their corporate tax liability. This can lead to cost savings for employers, which may be passed on to employees in the form of higher wages or better benefits. Furthermore, pre-tax contributions can help attract and retain top talent, as employees often view pension plans as a valuable part of their compensation package.

However, it is important to note that pre-tax contributions are subject to certain limits and regulations. For example, the IRS imposes annual contribution limits on pension plans, and exceeding these limits can result in penalties. Additionally, pre-tax contributions may not be available to all employees, particularly those in certain industries or job categories. It is essential for employees to consult with their employer or a financial advisor to understand the specific rules and limitations that apply to their situation.

In conclusion, pre-tax contributions to employee pension plans offer immediate tax relief and can lead to significant long-term savings for both employees and employers. By reducing taxable income and deferring taxes until retirement, pre-tax contributions can help individuals maximize their retirement savings and achieve their financial goals. However, it is crucial to be aware of the limits and regulations that govern pre-tax contributions to ensure compliance and avoid potential penalties.

Understanding Pre-Tax Employee Health Care Payments: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Net pay impact: Pre-tax deductions reduce net pay less than post-tax deductions

The impact of pre-tax deductions on net pay is a crucial aspect to consider when evaluating the overall compensation package for employees. Pre-tax deductions, such as those for pension contributions, reduce the amount of gross income subject to taxation, thereby lowering the tax liability and increasing the net pay. This is in contrast to post-tax deductions, which are subtracted from the already taxed income, resulting in a smaller net pay.

To illustrate this concept, let's consider an example. Suppose an employee has a gross income of $50,000 per year and contributes $5,000 to their pension plan as a pre-tax deduction. Their taxable income would be reduced to $45,000, and assuming a tax rate of 20%, their tax liability would be $9,000. This results in a net pay of $36,000. On the other hand, if the pension contribution were a post-tax deduction, the employee would first pay tax on the full $50,000, amounting to $10,000, and then subtract the $5,000 pension contribution from the after-tax income, resulting in a net pay of $35,000.

The difference in net pay between pre-tax and post-tax deductions may seem small in this example, but it can add up significantly over time. Additionally, pre-tax deductions can have other benefits, such as reducing the amount of income subject to Social Security and Medicare taxes, further increasing the net pay.

Employers should carefully consider the structure of their employee benefit plans to maximize the net pay for their employees. By offering pre-tax deductions for pension contributions, employers can provide a more attractive compensation package while also encouraging employees to save for retirement.

In conclusion, understanding the impact of pre-tax deductions on net pay is essential for both employees and employers. By leveraging pre-tax deductions, employees can increase their take-home pay and save for the future, while employers can create a more competitive and appealing benefits package.

Understanding Pre-Tax Employee Benefits: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Employer contributions: Employers may also contribute, often matching employee pre-tax contributions

Employers often play a significant role in pension contributions by matching the amounts deducted from employees' pre-tax income. This practice not only encourages employees to save for retirement but also helps in reducing the overall tax burden. When employers match pre-tax contributions, they essentially provide additional funds that can grow tax-deferred within the pension plan. This can lead to substantial savings over time, as the matched contributions benefit from compound interest and investment returns.

For example, if an employee contributes 5% of their salary to a pension plan and the employer matches this contribution, the total amount going into the plan is 10% of the employee's salary. This matched amount is also deducted from the employee's gross income before taxes are calculated, which lowers the taxable income and, consequently, the amount of tax owed.

Employer matching can vary widely among different companies and industries. Some employers may match a fixed percentage of contributions, while others might offer a variable match based on factors such as the employee's length of service or contribution amount. It's essential for employees to understand their employer's matching policy to maximize their retirement savings.

In addition to the direct financial benefits, employer matching can also have a positive impact on employee morale and retention. When employees see that their employer is invested in their financial future, they may feel more valued and motivated to stay with the company. This can lead to increased loyalty and reduced turnover, which are valuable for any organization.

Overall, employer contributions to pension plans, especially when matching employee pre-tax contributions, are a crucial aspect of retirement savings. They provide additional funds that can significantly enhance an employee's future financial security and also offer tax advantages. Understanding and leveraging these contributions effectively is key to making the most out of pension plans.

Maximizing Tax Benefits: Employee Health Insurance Contributions Explained

You may want to see also

Frequently asked questions

Employee pension contributions are typically deducted before tax.

Since pension contributions are deducted before tax, they reduce the employee's taxable income, potentially lowering their tax liability.

Contributing to a pension plan before tax can lead to immediate tax savings and help in accumulating retirement funds more efficiently.

In some cases, such as with Roth 401(k) contributions in the United States, contributions are made after tax, offering different tax advantages.

Employees can maximize tax benefits by contributing as much as possible to their pension plan, up to the allowable limits, and by understanding the specific tax implications of their contributions based on their income and tax bracket.