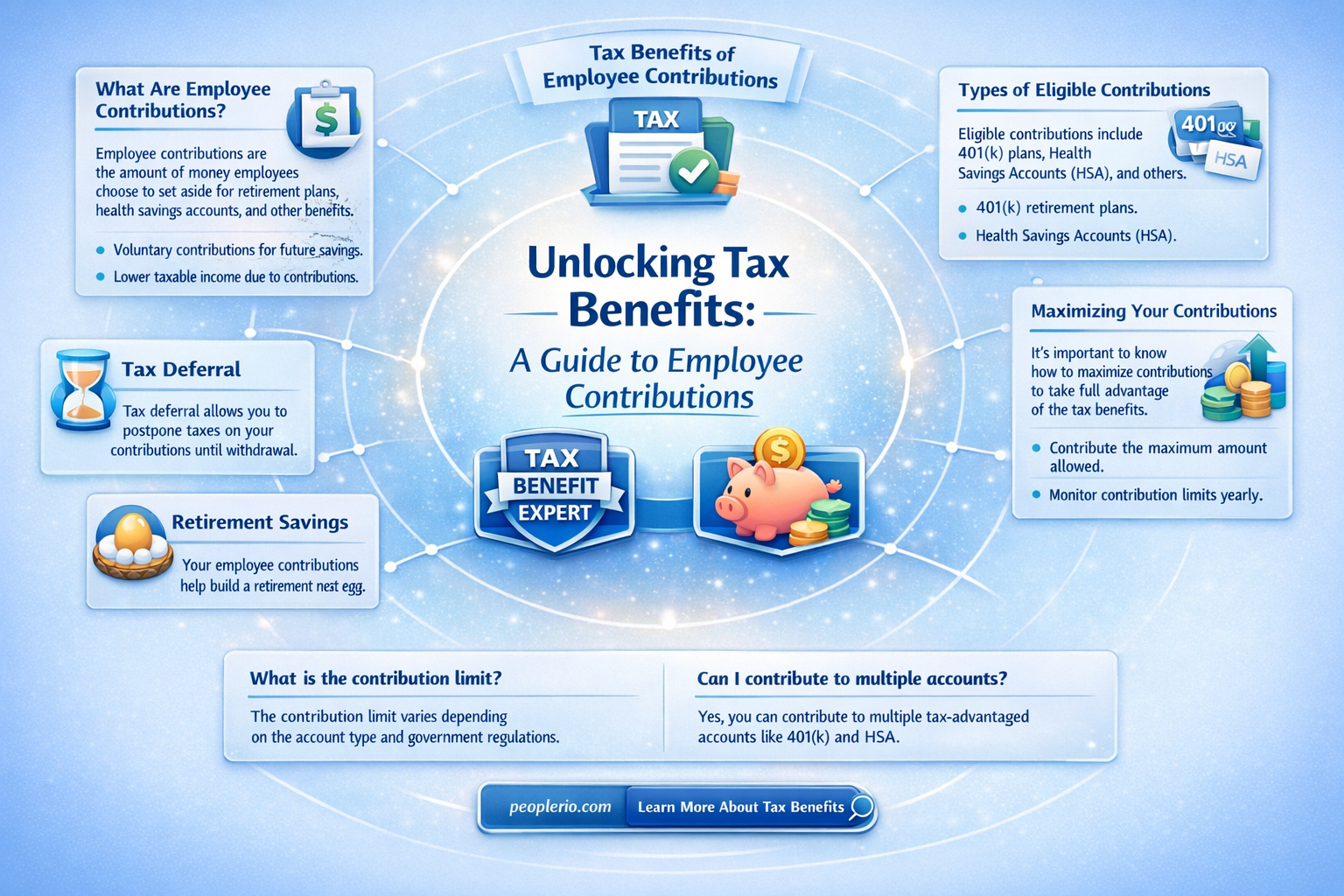

Employee required contributions, such as those towards retirement plans or health insurance, are often a topic of interest when it comes to tax deductions. In many jurisdictions, these contributions are indeed tax-deductible, meaning they can reduce an employee's taxable income. This deduction can provide significant tax savings, especially for those in higher tax brackets. However, the specifics of these deductions can vary widely depending on the country, the type of contribution, and the employee's individual circumstances. It's essential for employees to understand their local tax laws and consult with a financial advisor to maximize their tax benefits while ensuring compliance with all applicable regulations.

| Characteristics | Values |

|---|---|

| Deductibility | Contributions are tax-deductible |

| Contribution Type | Required contributions |

| Contributor | Employee |

| Tax Benefit | Reduces taxable income |

| Limit | Subject to contribution limits |

| Vesting | Immediate vesting |

| Reporting | Reported on Form W-2 |

| Employer Match | May be matched by employer contributions |

| Investment Options | Limited to employer-provided options |

| Withdrawal | Generally not allowed until retirement |

Explore related products

What You'll Learn

- General Rule: Employee contributions to retirement plans are generally tax-deductible, reducing taxable income

- Limits Apply: There are annual contribution limits set by the IRS; exceeding these limits can result in penalties

- Types of Plans: Different retirement plans (e.g., 401(k), IRA) have varying rules regarding tax deductions

- Tax Filing: Employees must file Form W-2 to report contributions and receive tax benefits

- Consult a Professional: For complex situations or high contributions, consulting a tax professional is advisable

![]()

General Rule: Employee contributions to retirement plans are generally tax-deductible, reducing taxable income

Employee contributions to retirement plans are generally tax-deductible, reducing taxable income. This means that when an employee contributes a portion of their salary to a retirement plan, such as a 401(k) or IRA, that contribution is subtracted from their gross income before taxes are calculated. This can result in a lower tax bill and more money saved for retirement.

For example, if an employee earns $50,000 per year and contributes $5,000 to their 401(k), their taxable income would be reduced to $45,000. This could potentially lower their tax bracket and result in significant savings.

It's important to note that there are limits to how much can be contributed to retirement plans each year. For 2022, the contribution limit for 401(k) plans is $19,500 for employees under age 50 and $26,500 for those 50 and older. IRA contribution limits are $6,000 for those under 50 and $7,000 for those 50 and older.

Additionally, some employers may offer matching contributions to retirement plans, which can further increase the tax benefits. For instance, if an employer matches 50% of an employee's 401(k) contributions up to 6% of their salary, that matching amount is also tax-deductible.

Overall, taking advantage of tax-deductible retirement contributions can be a smart financial move for employees looking to save for the future while also reducing their current tax liability.

Unleashing Fitness Incentives: The Tax Benefits of Employee Gym Memberships

You may want to see also

Explore related products

![]()

Limits Apply: There are annual contribution limits set by the IRS; exceeding these limits can result in penalties

The IRS imposes strict annual contribution limits on various types of retirement accounts, including 401(k)s, IRAs, and Roth IRAs. For 2023, the contribution limit for 401(k) plans is $22,500 for individuals under 50 and $30,000 for those 50 and older. Exceeding these limits can result in penalties, including a 6% excise tax on the excess contribution amount. This penalty is applied annually until the excess contribution is withdrawn.

It's crucial for employees to monitor their contributions throughout the year to avoid surpassing these limits. Employers may also need to adjust their payroll systems to ensure that employee contributions do not exceed the IRS thresholds. Additionally, employees who are covered by multiple retirement plans may need to coordinate their contributions to avoid penalties.

One strategy to avoid exceeding contribution limits is to make regular contributions throughout the year rather than lump-sum contributions. Employees can also consider contributing to other types of retirement accounts, such as IRAs or Roth IRAs, which have separate contribution limits. By diversifying their retirement savings, employees can maximize their tax-advantaged contributions while minimizing the risk of penalties.

In some cases, employees may be able to make catch-up contributions if they have not reached the IRS limits in previous years. This can be a valuable opportunity to boost retirement savings without incurring penalties. However, it's essential to consult with a financial advisor or tax professional to ensure that catch-up contributions are made correctly and do not result in penalties.

Overall, understanding and adhering to the IRS contribution limits is a critical aspect of retirement planning. By staying within these limits, employees can maximize their tax-advantaged savings while avoiding costly penalties.

Understanding Social Security Employee Tax: A Comprehensive Guide

You may want to see also

Explore related products

$14.99 $25

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![]()

Types of Plans: Different retirement plans (e.g., 401(k), IRA) have varying rules regarding tax deductions

Different retirement plans offer various tax advantages, and understanding these can help you make informed decisions about your savings. For instance, a 401(k) plan allows employees to contribute a portion of their salary pre-tax, reducing their taxable income for the year. This means that the money grows tax-deferred until it is withdrawn in retirement. On the other hand, an Individual Retirement Account (IRA) also provides tax benefits, but the specifics depend on the type of IRA. A traditional IRA allows for tax-deductible contributions, similar to a 401(k), while a Roth IRA offers tax-free growth and withdrawals in retirement, but contributions are made with after-tax dollars.

When comparing these plans, it's essential to consider the contribution limits, withdrawal rules, and tax implications. For example, in 2023, the contribution limit for a 401(k) is $22,500 for individuals under 50, while the limit for an IRA is $6,500. Additionally, 401(k) plans often include employer matching contributions, which can significantly boost your savings. IRAs, however, do not have employer contributions but offer more flexibility in terms of investment options.

Another factor to consider is the age at which you can start making withdrawals without incurring penalties. For a 401(k), you can generally start withdrawing funds at age 59½, while for an IRA, the same age applies, but there are exceptions for certain circumstances, such as first-time homebuyer expenses or higher education costs.

In summary, while both 401(k) and IRA plans offer tax benefits, they differ in terms of contribution limits, employer involvement, investment options, and withdrawal rules. It's crucial to evaluate these factors based on your individual financial goals and circumstances to determine which plan is best suited for you.

Maximizing Tax Benefits: Employee Health Insurance Contributions Explained

You may want to see also

Explore related products

![]()

Tax Filing: Employees must file Form W-2 to report contributions and receive tax benefits

Employees are required to file Form W-2 to report their contributions and receive tax benefits. This form is a crucial part of the tax filing process, as it provides the necessary information for the Internal Revenue Service (IRS) to determine the amount of taxes owed and the benefits to which the employee is entitled. The form must be filed by the employer on behalf of the employee, and it includes details such as the employee's wages, tips, and other compensation, as well as the amount of federal income tax withheld.

One of the key benefits of filing Form W-2 is that it allows employees to claim tax deductions for their contributions to certain retirement plans, such as 401(k)s and IRAs. These deductions can help to reduce the employee's taxable income, resulting in a lower tax bill. Additionally, the form is used to report the employee's eligibility for certain tax credits, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit.

It is important to note that employees must file Form W-2 even if they do not have any tax withheld from their wages. This is because the form is used to report the employee's income and contributions, regardless of whether or not they owe taxes. Failure to file the form can result in penalties and fines, as well as the loss of potential tax benefits.

In order to file Form W-2, employees must provide their employer with the necessary information, such as their social security number and their contribution amounts. The employer will then use this information to complete the form and submit it to the IRS. Employees should keep a copy of the form for their own records, as it will be needed when filing their individual tax returns.

Overall, filing Form W-2 is an essential part of the tax filing process for employees. It allows them to report their contributions and receive tax benefits, and it helps to ensure that they are in compliance with federal tax laws. By understanding the importance of this form and providing their employer with the necessary information, employees can help to ensure that they receive the tax benefits to which they are entitled.

Understanding Employee Tax: A Comprehensive Guide for 2023

You may want to see also

Explore related products

![]()

Consult a Professional: For complex situations or high contributions, consulting a tax professional is advisable

Navigating the complexities of tax deductions for employee contributions can be challenging, especially when dealing with substantial amounts or intricate financial situations. In such cases, seeking the expertise of a tax professional becomes not just advisable, but essential. A tax professional can provide tailored guidance that takes into account the specific nuances of your financial circumstances, ensuring that you maximize your deductions while remaining compliant with tax laws.

One of the key benefits of consulting a tax professional is their ability to interpret the often convoluted tax code. They can help you understand which contributions are eligible for deductions, how to properly document these contributions, and what potential pitfalls to avoid. For instance, they might advise on the importance of maintaining detailed records of all contributions, including dates, amounts, and the purpose of each contribution. This level of detail is crucial for substantiating your deductions in the event of an audit.

Moreover, a tax professional can assist in identifying additional deductions or credits that you may be eligible for, which can further reduce your tax liability. They can also help you navigate any state-specific tax laws that may apply, as well as any changes to the tax code that could impact your deductions. This is particularly important given the frequent updates and amendments to tax legislation, which can make it difficult for individuals to stay informed and up-to-date.

When selecting a tax professional, it's important to choose someone with experience and expertise in the area of employee contributions and tax deductions. Look for credentials such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA), and consider seeking recommendations from colleagues or friends who have had positive experiences with tax professionals. Additionally, be sure to discuss their fees upfront and understand their billing structure to avoid any surprises.

In conclusion, while it may be tempting to navigate the tax deduction process on your own, consulting a tax professional can provide invaluable peace of mind and potentially significant financial benefits. Their expertise can help you make the most of your employee contributions while ensuring that you remain in good standing with the tax authorities.

Understanding Household Employees: Tax Implications and Responsibilities Explained

You may want to see also

Frequently asked questions

Employee required contributions, such as those to a 401(k) or other retirement plans, are typically tax-deductible. This means you can reduce your taxable income by the amount you contribute, up to certain limits.

The limits for tax-deductible employee contributions vary depending on the type of plan and your age. For example, in 2023, the contribution limit for a 401(k) plan is $19,500 for individuals under 50 years old, and $26,000 for those 50 and older.

To determine if your contributions are tax-deductible, check with your plan administrator or review the plan documents. Additionally, you can consult with a tax professional or use tax preparation software to ensure you're taking advantage of all eligible deductions.

Yes, in addition to the tax deduction, employee contributions to retirement plans often grow tax-deferred. This means you don't pay taxes on the investment gains until you withdraw the funds in retirement. Some plans also offer a tax credit, which can further reduce your tax liability.