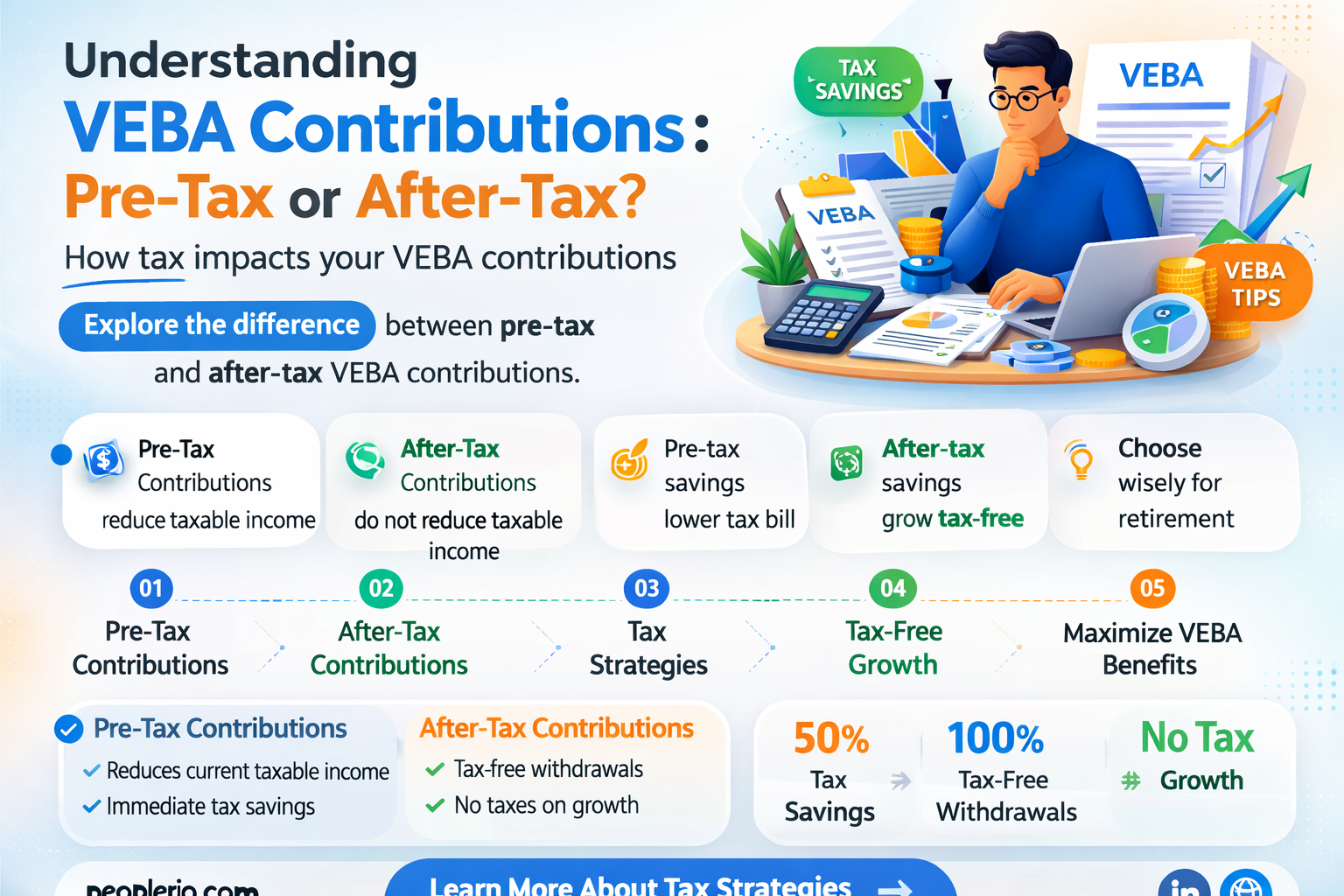

Employee VEBA (Voluntary Employee Beneficiary Association) contributions are a type of pre-tax contribution. This means that the funds are deducted from an employee's paycheck before taxes are applied. The pre-tax nature of VEBA contributions provides a financial advantage to employees, as it reduces their taxable income, thereby lowering the amount of federal, state, and local taxes withheld. These contributions are typically used for qualified medical expenses, and the funds grow tax-free as long as they are used for eligible healthcare costs. Understanding the tax implications of VEBA contributions is crucial for employees looking to maximize their savings and manage their healthcare expenses effectively.

Explore related products

What You'll Learn

- Definition of VEBA: Understand what a Voluntary Employee Beneficiary Association (VEBA) is and its purpose

- Tax Treatment: Explore whether contributions to a VEBA are made before or after taxes are applied

- Benefits: Discover the advantages of making pre-tax contributions versus after-tax contributions to a VEBA

- IRS Regulations: Learn about the Internal Revenue Service (IRS) rules and guidelines governing VEBA contributions

- Comparison: Compare VEBA contributions to other types of employee benefits, such as 401(k) plans

![]()

Definition of VEBA: Understand what a Voluntary Employee Beneficiary Association (VEBA) is and its purpose

A Voluntary Employee Beneficiary Association (VEBA) is a type of tax-exempt organization established under Section 501(c)(9) of the Internal Revenue Code. It is designed to provide benefits to employees and their beneficiaries, typically in the form of medical expense reimbursements. VEBAs are often used by employers to offer flexible spending accounts (FSAs) or health reimbursement arrangements (HRAs) to their employees.

The primary purpose of a VEBA is to allow employees to set aside a portion of their income on a pre-tax basis to cover qualified medical expenses. This can include costs such as deductibles, copayments, and prescription medications that are not covered by the employer's health insurance plan. By using a VEBA, employees can reduce their taxable income, which in turn lowers their tax liability.

One of the key benefits of a VEBA is that the contributions made by employees are considered pre-tax contributions. This means that the money is deducted from the employee's paycheck before taxes are calculated, reducing the amount of income subject to taxation. Additionally, the earnings on the contributions within the VEBA account are tax-free, as long as the funds are used for qualified medical expenses.

To establish a VEBA, an employer must create a written plan document that outlines the terms and conditions of the arrangement. This document should include details such as the types of expenses that will be reimbursed, the contribution limits, and the procedures for claiming reimbursements. Employers are also responsible for ensuring that the VEBA complies with all applicable tax laws and regulations.

In summary, a Voluntary Employee Beneficiary Association (VEBA) is a tax-exempt organization that allows employees to set aside pre-tax dollars to cover qualified medical expenses. This can provide significant tax savings for employees while also helping employers to offer more comprehensive benefits packages. By understanding the definition and purpose of a VEBA, employers and employees can make informed decisions about how to best utilize this valuable tool.

Unlocking Tax Benefits: A Guide to Employee Event Deductions

You may want to see also

Explore related products

![Smart Baby Bottle Monitor® [AS SEEN ON Shark Tank], Smart Milk Tracker, Baby Feeding Essentials, Track Breast Milk & Formula Expiration, Temperature Monitor, Feeding Log, App Control](https://m.media-amazon.com/images/I/71tvS+aXxkL._AC_UL320_.jpg)

![]()

Tax Treatment: Explore whether contributions to a VEBA are made before or after taxes are applied

Contributions to a Voluntary Employee Beneficiary Association (VEBA) are typically made on a pre-tax basis. This means that the funds are deducted from an employee's gross income before federal, state, and local taxes are applied. The pre-tax nature of VEBA contributions provides a significant tax advantage, as it reduces the employee's taxable income, thereby lowering their overall tax liability.

For example, if an employee contributes $1,000 to a VEBA, this amount would be subtracted from their gross income before taxes are calculated. Assuming a combined federal, state, and local tax rate of 30%, the employee would save $300 in taxes by making the VEBA contribution. This tax savings can be a strong incentive for employees to participate in VEBA plans.

However, it's important to note that while VEBA contributions are generally pre-tax, the tax treatment may vary depending on the specific type of VEBA and the employee's individual circumstances. For instance, some VEBAs may be subject to different tax rules, such as those related to unrelated business income tax (UBIT). Additionally, the tax benefits of VEBA contributions may be affected by factors such as the employee's income level, tax bracket, and other deductions or credits they may be eligible for.

In conclusion, while VEBA contributions are typically made on a pre-tax basis, offering employees a valuable tax advantage, it's essential to consider the specific tax implications based on the type of VEBA and individual tax circumstances. Employees should consult with a tax professional or financial advisor to fully understand the tax benefits and potential implications of contributing to a VEBA.

Are Employee HSA Contributions Subject to Social Security Tax?

You may want to see also

Explore related products

![]()

Benefits: Discover the advantages of making pre-tax contributions versus after-tax contributions to a VEBA

Making pre-tax contributions to a VEBA (Voluntary Employee Benefit Association) offers several advantages over after-tax contributions. One of the primary benefits is the immediate tax savings. When you contribute to a VEBA before taxes are deducted, you reduce your taxable income, which in turn lowers the amount of tax you owe. This can result in a significant increase in your take-home pay.

Another advantage of pre-tax contributions is the potential for long-term tax benefits. The money you contribute to a VEBA grows tax-free, meaning you won't have to pay taxes on the investment gains until you withdraw the funds. This can lead to substantial savings over time, especially if you're in a higher tax bracket.

Pre-tax contributions to a VEBA also allow you to set aside more money for healthcare expenses. Because the contributions are deducted from your gross income, you can allocate a larger portion of your earnings to your VEBA than you could if you were contributing after taxes. This can be particularly beneficial if you have high healthcare costs or if you're saving for future medical expenses.

In contrast, after-tax contributions to a VEBA do not offer the same level of tax savings. While the contributions are still tax-deductible, you'll have to pay taxes on the money before you can deduct it, reducing the overall benefit. Additionally, after-tax contributions won't grow tax-free, which means you'll have to pay taxes on any investment gains when you withdraw the funds.

Overall, pre-tax contributions to a VEBA provide a more effective way to save for healthcare expenses while reducing your tax burden. By taking advantage of these contributions, you can increase your take-home pay, save for future medical costs, and potentially enjoy long-term tax benefits.

Unlocking the Tax Benefits of Employee Gift Cards: A Comprehensive Guide

You may want to see also

Explore related products

![]()

IRS Regulations: Learn about the Internal Revenue Service (IRS) rules and guidelines governing VEBA contributions

The IRS has specific regulations regarding VEBA contributions that are crucial for both employers and employees to understand. These regulations dictate how contributions are made, the tax implications, and the conditions under which the funds can be used. According to IRS guidelines, VEBA contributions are generally considered pre-tax contributions. This means that the funds are deducted from an employee's gross income before taxes are calculated, reducing the taxable income and, consequently, the tax liability.

However, it's important to note that not all VEBA contributions are treated equally under IRS regulations. For instance, contributions made towards medical expenses are typically pre-tax, while contributions towards dependent care expenses may have different tax implications. The IRS also sets limits on the maximum amount that can be contributed to a VEBA plan annually, and these limits can vary based on the type of expense the funds are intended for.

Employers are responsible for ensuring that their VEBA plans comply with IRS regulations. This includes maintaining accurate records of contributions, distributions, and any administrative fees associated with the plan. Failure to comply with IRS regulations can result in penalties and fines for both the employer and the employee.

Employees should also be aware of the IRS regulations governing VEBA contributions to ensure they are making informed decisions about their financial planning. For example, understanding the tax implications of VEBA contributions can help employees optimize their tax strategy and potentially save money on their annual tax bill.

In conclusion, IRS regulations play a significant role in determining the tax treatment of VEBA contributions. By understanding these regulations, both employers and employees can ensure they are in compliance and making the most of this valuable employee benefit.

Are Employee HSA Contributions Subject to Medicare Tax?

You may want to see also

![]()

Comparison: Compare VEBA contributions to other types of employee benefits, such as 401(k) plans

VEBA contributions offer a unique advantage over traditional 401(k) plans in terms of tax benefits. While both types of contributions are made pre-tax, VEBA contributions are specifically designated for medical expenses, which can provide additional tax savings. For example, if an employee contributes $10,000 to a VEBA plan, they may be able to deduct this amount from their taxable income, reducing their overall tax liability. In contrast, 401(k) contributions are subject to income tax when withdrawn in retirement, which can offset some of the initial tax benefits.

Another key difference between VEBA contributions and 401(k) plans is the flexibility of withdrawals. VEBA funds can be withdrawn tax-free at any time for qualified medical expenses, whereas 401(k) funds are generally restricted until retirement age. This makes VEBA contributions a more accessible option for employees who may need to cover unexpected medical costs or who want to use their funds for health-related expenses before retirement.

However, it's important to note that VEBA contributions are typically limited to a specific dollar amount each year, whereas 401(k) contributions can be much higher. In 2023, the maximum annual contribution to a VEBA plan is $5,000, while the maximum contribution to a 401(k) plan is $22,500. This means that employees who want to maximize their tax benefits and retirement savings may need to contribute to both types of plans.

In conclusion, while both VEBA contributions and 401(k) plans offer pre-tax contribution options, VEBA contributions provide additional tax benefits and flexibility for medical expenses. However, 401(k) plans allow for higher contribution limits and are more focused on long-term retirement savings. Employees should consider their individual financial goals and needs when deciding how to allocate their contributions between these two types of plans.

Unlocking the Secrets: Are Employee Parties Tax Deductible?

You may want to see also

Frequently asked questions

Employee VEBA (Voluntary Employee Beneficiary Association) contributions are typically pre-tax contributions. This means that the money is deducted from your paycheck before taxes are calculated, which can lower your taxable income and potentially reduce your tax liability.

VEBA contributions reduce your taxable income because they are deducted from your paycheck before taxes are applied. This pre-tax deduction can result in a lower tax bill, as you are taxed on a smaller amount of income.

Contributing to a VEBA plan offers several tax benefits. Firstly, your contributions are made on a pre-tax basis, which lowers your taxable income. Secondly, the earnings on your VEBA contributions grow tax-deferred, meaning you don't pay taxes on the investment gains until you withdraw the funds. Finally, qualified withdrawals from a VEBA plan are tax-free, allowing you to use the funds for eligible medical expenses without incurring additional taxes.