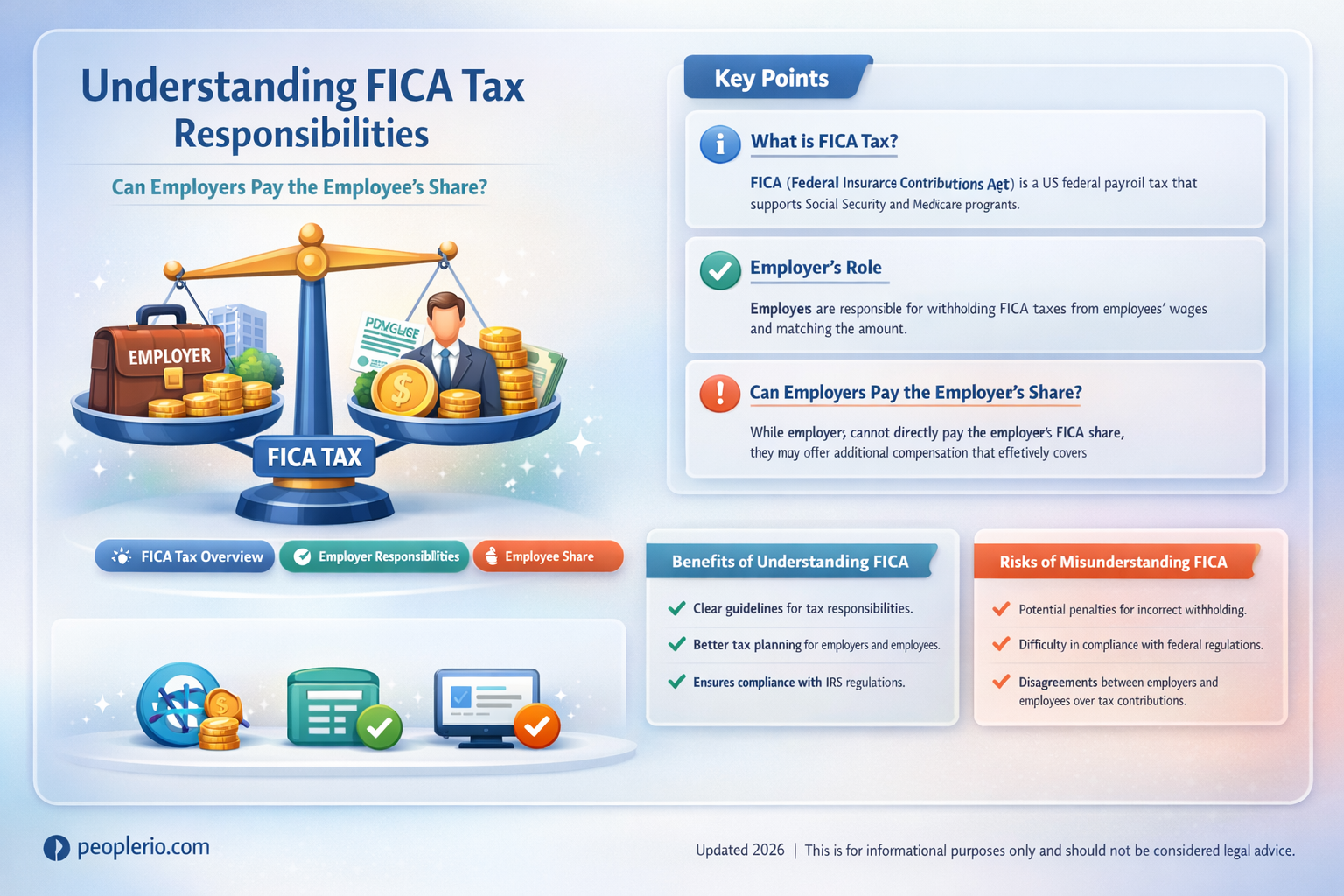

The question of whether employers are permitted to pay the employee's portion of FICA (Federal Insurance Contributions Act) taxes is a common one in the realm of payroll and employment law. FICA taxes, which fund Social Security and Medicare, are typically split between employers and employees, with each party responsible for a specific percentage of the total tax. However, there are circumstances under which an employer might consider paying the employee's share, such as in certain fringe benefit arrangements or as part of a compensation package. It's important to understand the legal implications and potential consequences of such an arrangement, as it can impact both the employer's and employee's tax liabilities and benefits.

| Characteristics | Values |

|---|---|

| Legal Requirement | Employers are legally required to pay the employer's share of FICA taxes, which funds Social Security and Medicare. |

| Employee Contribution | Employers are generally not allowed to pay the employee's share of FICA taxes, as this is typically deducted from the employee's wages. |

| Tax Rate | The FICA tax rate is 15.3% of an employee's wages, with the employer paying 7.65% and the employee paying the remaining 7.65%. |

| Wage Base Limit | There is a wage base limit for FICA taxes, which means that employers only pay FICA taxes on wages up to a certain amount per year. |

| Exemptions | Certain employees, such as those working for state or local governments, may be exempt from FICA taxes. |

| Consequences of Non-Compliance | Employers who fail to pay their share of FICA taxes may face penalties and interest charges. |

Explore related products

What You'll Learn

- Legal Requirements: Employers must pay their share of FICA taxes; employees pay their share separately

- Tax Compliance: Employers are responsible for withholding and paying employee FICA taxes to the IRS

- Financial Implications: Paying employee FICA taxes can impact an employer's financial planning and budgeting

- Employee Benefits: Some employers may offer to pay employee FICA taxes as a benefit, affecting job satisfaction

- Tax Reform: Changes in tax laws can influence how employers handle FICA tax payments for employees

![]()

Legal Requirements: Employers must pay their share of FICA taxes; employees pay their share separately

Employers are legally obligated to pay their share of FICA taxes, which stands for Federal Insurance Contributions Act taxes. This is a federal payroll tax that funds Social Security and Medicare. The FICA tax rate is 15.3% of an employee's gross wages, with the employer responsible for paying 7.65% and the employee paying the remaining 7.65%. This is a mandatory requirement, and failure to comply can result in penalties and legal action against the employer.

The FICA tax is typically withheld from an employee's paycheck and sent to the Internal Revenue Service (IRS) by the employer. Employers must also match the employee's contribution, meaning they pay an equal amount of FICA tax for each employee. This is a significant financial responsibility for employers, but it is also a crucial part of funding the Social Security and Medicare programs that provide benefits to millions of Americans.

There are some exceptions to the FICA tax requirements. For example, certain types of employees, such as state and local government workers, may be exempt from FICA taxes. Additionally, employers may be able to claim a credit for FICA taxes paid on certain types of wages, such as those paid to employees who are also receiving unemployment benefits. However, these exceptions are limited, and most employers will need to pay their share of FICA taxes for each employee.

Employers who fail to pay their share of FICA taxes can face serious consequences. The IRS can impose penalties and interest on the unpaid taxes, and in some cases, employers may even face criminal charges. Additionally, employees who do not have their FICA taxes withheld may be required to pay the full amount of FICA taxes owed, plus penalties and interest. This can be a significant financial burden for employees, and it is one of the reasons why it is so important for employers to comply with FICA tax requirements.

In conclusion, employers are legally required to pay their share of FICA taxes, and failure to do so can result in serious consequences. The FICA tax is a crucial part of funding the Social Security and Medicare programs, and it is important for employers to understand their responsibilities and comply with the law.

Decoding 1099 Taxes: A Comprehensive Guide for Freelancers

You may want to see also

Explore related products

![]()

Tax Compliance: Employers are responsible for withholding and paying employee FICA taxes to the IRS

Employers have a legal obligation to withhold and pay employee FICA taxes to the Internal Revenue Service (IRS). This responsibility is a critical aspect of tax compliance for businesses, ensuring that both the employer and employee contributions to Social Security and Medicare are accurately calculated and remitted. Failure to comply with these regulations can result in significant penalties and legal repercussions for the employer.

The process of withholding FICA taxes involves calculating the appropriate amount based on the employee's gross wages and the current FICA tax rates. Employers must then deduct these taxes from the employee's paycheck and set aside the funds for payment to the IRS. This typically occurs on a quarterly basis, although larger employers may be required to make more frequent payments.

In addition to withholding the employee's portion of FICA taxes, employers are also responsible for paying their own share. This includes matching the employee's contribution dollar for dollar, up to the annual wage base limit. For 2023, the Social Security wage base is $147,000, and the Medicare wage base is unlimited. Employers must also pay an additional Medicare tax of 0.9% on wages exceeding $200,000 for single filers and $250,000 for joint filers.

To ensure compliance with FICA tax regulations, employers should maintain accurate records of all wage payments and tax withholdings. This includes filing Form 941, Employer's Quarterly Federal Tax Return, and providing employees with Form W-2, Wage and Tax Statement, at the end of each year. Employers should also stay informed about changes to FICA tax rates and wage base limits, as these can impact their tax obligations and payroll processes.

In summary, employers play a crucial role in the administration of FICA taxes, with responsibilities that include withholding and paying both employee and employer contributions. By understanding and adhering to these tax compliance requirements, employers can avoid penalties and ensure the financial security of their employees through proper Social Security and Medicare funding.

Understanding Minimum Salary Requirements for Salaried Employees: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Financial Implications: Paying employee FICA taxes can impact an employer's financial planning and budgeting

Paying employee FICA taxes can have significant financial implications for employers, impacting their financial planning and budgeting in several ways. One of the primary effects is on cash flow management. When employers pay the employee portion of FICA taxes, they are essentially reducing the take-home pay of their employees. This can lead to increased cash flow for the employer in the short term, as they retain more money from each paycheck. However, this practice may also lead to decreased employee morale and potentially higher turnover rates, as employees may feel that their compensation is being unfairly reduced.

Another financial implication is the potential impact on employee benefits. Some employers may choose to pay the employee portion of FICA taxes as a way to enhance their benefits package and attract top talent. However, this can increase the overall cost of employee compensation, which may need to be factored into the employer's budget. Additionally, employers who pay employee FICA taxes may need to adjust their accounting practices to ensure accurate tracking and reporting of these payments.

Employers should also consider the long-term financial implications of paying employee FICA taxes. While this practice may provide short-term cash flow benefits, it could lead to increased costs over time, particularly if employee morale suffers or if the practice becomes a standard expectation among employees. Employers may need to weigh the potential benefits against the long-term costs and consider alternative strategies for managing cash flow and employee compensation.

In conclusion, paying employee FICA taxes can have a range of financial implications for employers, from short-term cash flow management to long-term budgeting and employee benefits considerations. Employers should carefully evaluate these implications and consider the potential impact on their financial planning and overall business strategy.

Understanding Wage Reduction: Legal Implications for Employers and Employees

You may want to see also

Explore related products

![]()

Employee Benefits: Some employers may offer to pay employee FICA taxes as a benefit, affecting job satisfaction

Offering to pay employee FICA taxes can be a significant benefit that impacts job satisfaction. FICA, which stands for Federal Insurance Contributions Act, requires both employers and employees to contribute a portion of their earnings to fund Social Security and Medicare. Typically, employers match the employee's contribution, but some employers go a step further by offering to cover the employee's share as well. This can be a powerful incentive for employees, as it effectively increases their take-home pay and demonstrates the employer's commitment to their financial well-being.

From an employee's perspective, having their FICA taxes paid by their employer can lead to higher job satisfaction and loyalty. It's a tangible benefit that directly affects their bottom line, and it can make them feel more secure about their financial future. Additionally, it can help attract top talent, as employees may be more likely to choose an employer that offers this benefit over one that doesn't.

However, it's important to note that this benefit may not be universally applicable or equally valued by all employees. For example, employees who are already maxing out their Social Security contributions may not see as much value in this benefit. Furthermore, the tax implications of having an employer pay FICA taxes can be complex, and employees should consult with a tax professional to understand how it might affect their individual situation.

Employers considering offering this benefit should weigh the potential impact on job satisfaction against the additional costs. Paying employee FICA taxes can be a significant expense, and employers need to ensure that it aligns with their overall compensation strategy and budget. Additionally, employers should be aware of the potential legal and tax implications of offering this benefit, as it may require careful structuring to comply with relevant laws and regulations.

In conclusion, offering to pay employee FICA taxes can be a valuable benefit that enhances job satisfaction and attracts top talent. However, it's important for both employers and employees to carefully consider the implications and ensure that it's a good fit for their individual needs and circumstances.

Understanding FUTA Tax: What Employees Need to Know

You may want to see also

![]()

Tax Reform: Changes in tax laws can influence how employers handle FICA tax payments for employees

Tax reform can significantly impact how employers manage FICA tax payments for their employees. FICA, which stands for Federal Insurance Contributions Act, encompasses Social Security and Medicare taxes. Employers are typically responsible for withholding and paying these taxes, but changes in tax laws can alter this responsibility. For instance, the Tax Cuts and Jobs Act (TCJA) of 2017 introduced substantial changes to the tax code, affecting both individual and business taxpayers. One of the key provisions of the TCJA was the reduction in the corporate tax rate from 35% to 21%, which indirectly influenced how employers approached FICA tax payments.

Under the TCJA, employers saw an increase in the amount of FICA taxes they were required to pay due to the reclassification of certain income. This reclassification meant that income previously exempt from FICA taxes, such as certain fringe benefits, became taxable. As a result, employers had to adjust their payroll systems to account for these changes, ensuring they were in compliance with the new tax laws. This involved not only recalculating FICA tax payments but also updating employee records and payroll software.

Moreover, tax reform can lead to changes in the way employers structure their employee compensation packages. For example, some employers might choose to increase employee wages to offset the impact of higher FICA tax payments, while others might opt to provide additional fringe benefits that are not subject to FICA taxes. This strategic restructuring of compensation packages can help employers manage the financial burden of FICA tax payments while remaining competitive in the job market.

Another aspect of tax reform that can influence FICA tax payments is the introduction of new tax credits or deductions. For instance, the TCJA introduced a new tax credit for employers who provide paid family and medical leave. This credit can help offset the cost of FICA tax payments, providing employers with an incentive to offer these benefits. Employers must carefully analyze these tax credits and deductions to determine how they can best leverage them to reduce their FICA tax liabilities.

In conclusion, tax reform can have a profound impact on how employers handle FICA tax payments for their employees. From changes in tax rates to the reclassification of income and the introduction of new tax credits, employers must stay informed and adapt their payroll practices accordingly. By doing so, they can ensure compliance with the tax laws while also managing their financial resources effectively.

Understanding Electronic Tax Payment Requirements for Employees

You may want to see also

Frequently asked questions

Generally, employers are not permitted to pay the employee's portion of FICA taxes. FICA taxes, which include Social Security and Medicare, are typically split between the employer and the employee, with each paying a specific percentage of the employee's wages.

If an employer pays the employee's FICA taxes, it could be considered additional taxable income to the employee. This could potentially increase the employee's tax liability and affect their Social Security benefits. It's important for employers to understand the implications and consult with a tax professional before making such arrangements.

Employers and employees cannot legally agree to alter the FICA tax withholding rates or the employer's responsibility to match the employee's contribution. FICA tax rates are set by law, and both parties must adhere to these regulations. Any attempt to circumvent these rules could result in penalties and legal consequences for both the employer and the employee.