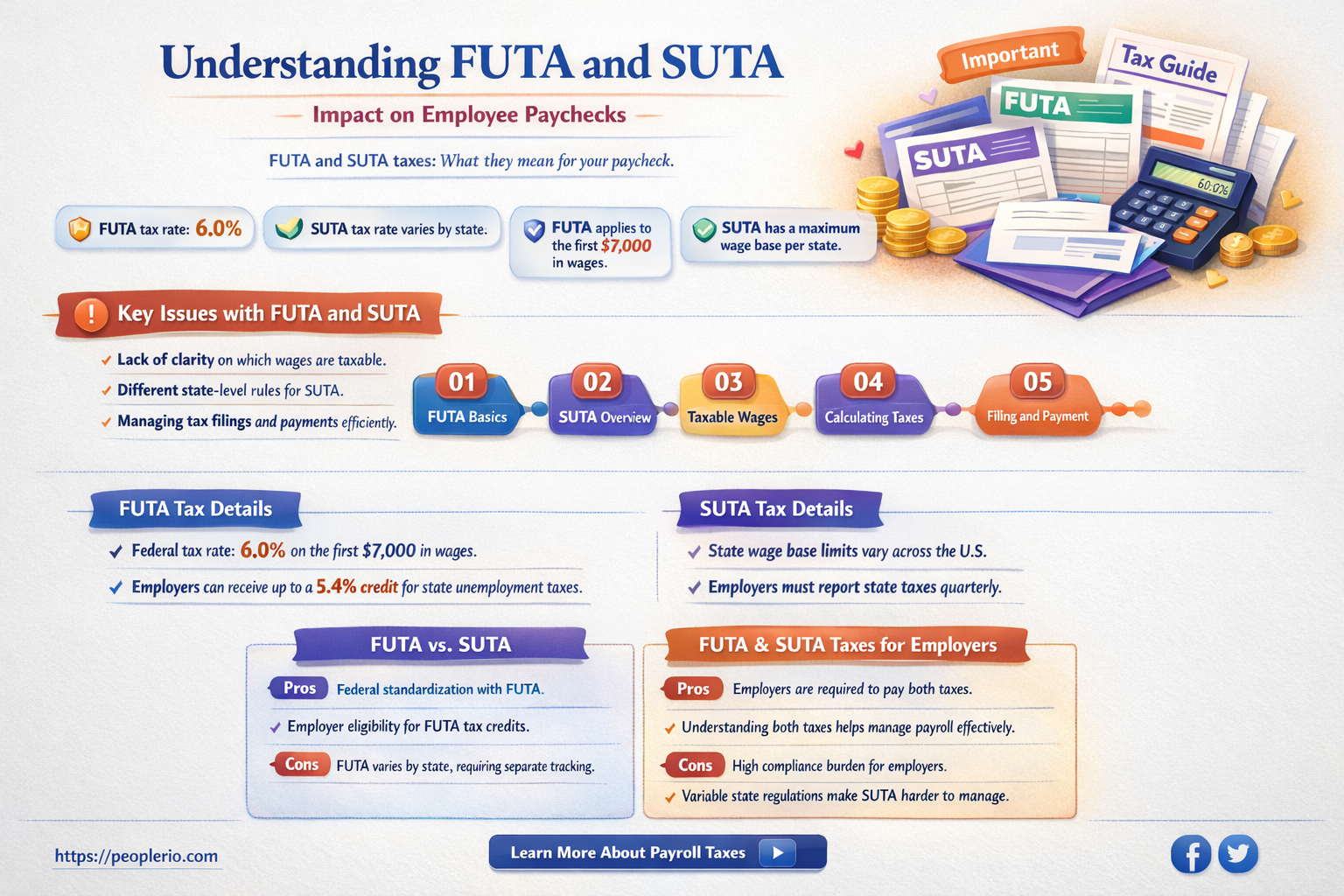

Futa and Suta are types of taxes that can impact an employee's pay. Futa, or Federal Unemployment Tax Act, and Suta, or State Unemployment Tax Act, are both unemployment taxes paid by employers. While these taxes are generally a percentage of an employee's wages, they are not typically deducted directly from an employee's paycheck like income taxes or social security. Instead, employers pay these taxes out of their own funds. However, in some cases, employers may choose to deduct a small amount from an employee's wages to cover these taxes, depending on state laws and company policies. It's important for employees to understand how these taxes work and how they might affect their take-home pay.

| Characteristics | Values |

|---|---|

| FUTA (Federal Unemployment Tax Act) | 6.2% of the first $7,000 of each employee's wages |

| SUTA (State Unemployment Tax Act) | Varies by state, typically a percentage of employee wages |

| Purpose | To fund unemployment insurance programs |

| Payment Frequency | Quarterly |

| Reporting Requirements | Employers must report wages and pay FUTA and SUTA taxes to the IRS and state agencies |

| Employee Impact | Deducted from gross pay, reducing take-home pay |

| Employer Impact | Increases cost of hiring and maintaining employees |

| Compliance | Mandatory for employers with a certain number of employees or wage thresholds |

Explore related products

What You'll Learn

- Definition of Futa and Suta: Understanding the terms and their implications on payroll

- Calculation Methods: How these taxes are calculated and their impact on gross pay

- Legal Requirements: Federal and state mandates regarding Futa and Suta deductions

- Employee Exemptions: Conditions under which employees might be exempt from these deductions

- Impact on Net Pay: Analyzing how Futa and Suta affect an employee's take-home pay

![]()

Definition of Futa and Suta: Understanding the terms and their implications on payroll

FUTA, or the Federal Unemployment Tax Act, and SUTA, or the State Unemployment Tax Act, are two critical components of the unemployment insurance system in the United States. These acts mandate that employers contribute a certain percentage of their employees' wages to fund unemployment benefits. While these taxes are not directly deducted from an employee's paycheck, they do impact the overall payroll costs for an employer.

The FUTA tax rate is currently 6% on the first $7,000 of each employee's wages per year. However, employers may be eligible for a credit of up to 5.4% if they pay their state unemployment taxes on time. This effectively reduces the federal tax rate to 0.6% for those employers. On the other hand, SUTA tax rates vary by state and are typically a percentage of the employee's wages. These rates can range from as low as 1% to as high as 5% or more, depending on the state and the employer's experience rating.

Understanding the implications of FUTA and SUTA on payroll is crucial for both employers and employees. For employers, these taxes represent a significant cost that must be factored into their overall budget. Failure to pay these taxes can result in penalties and interest, as well as potential legal action. For employees, while they do not directly pay these taxes, they may indirectly bear the cost through lower wages or reduced benefits.

One common misconception is that FUTA and SUTA taxes are deducted from an employee's paycheck. This is not the case; these taxes are paid by the employer out of their own funds. However, the cost of these taxes can be passed on to employees in the form of lower wages or reduced benefits. It is important for employees to understand this distinction and to be aware of the potential impact of these taxes on their overall compensation.

In conclusion, FUTA and SUTA taxes play a vital role in funding unemployment benefits in the United States. While these taxes are not directly deducted from an employee's paycheck, they do have significant implications for payroll costs and overall compensation. Employers must carefully manage these taxes to avoid penalties and to ensure that they are in compliance with both federal and state regulations. Employees, on the other hand, should be aware of the potential impact of these taxes on their wages and benefits.

Can Employers Legally Cover COBRA Premiums for Employees?

You may want to see also

Explore related products

![]()

Calculation Methods: How these taxes are calculated and their impact on gross pay

The calculation of FUTA and SUTA taxes involves a specific methodology that impacts an employee's gross pay. FUTA tax is calculated at a federal level, while SUTA tax is calculated at a state level. Both taxes are typically calculated as a percentage of an employee's wages, up to a certain wage base limit.

For FUTA tax, the current tax rate is 6%, and the wage base limit is $7,000 per employee per year. This means that for an employee earning $7,000 or more, the FUTA tax would be $420 per year. For SUTA tax, the rate and wage base limit vary by state, but the general calculation method is similar.

The impact of these taxes on gross pay can be significant, especially for lower-income employees. For example, if an employee earns $30,000 per year, the FUTA tax would be $1,800 per year, and the SUTA tax could be an additional $1,000 to $2,000 per year, depending on the state. This could result in a total tax deduction of $2,800 to $3,800 per year, which would reduce the employee's gross pay by 9.3% to 12.7%.

Employers are responsible for calculating and deducting these taxes from an employee's pay, and for remitting the taxes to the appropriate government agencies. Employees can typically see the amount of FUTA and SUTA tax deducted from their pay on their pay stubs.

It's important to note that these taxes are not optional, and failure to pay them can result in penalties and interest for both employers and employees. Additionally, these taxes are not refundable, so it's important for employees to understand how they are calculated and their impact on gross pay.

Understanding FUTA Tax: What Employees Need to Know

You may want to see also

Explore related products

![]()

Legal Requirements: Federal and state mandates regarding Futa and Suta deductions

Federal and state mandates regarding FUTA and SUTA deductions are complex and multifaceted. The Federal Unemployment Tax Act (FUTA) requires employers to pay a federal unemployment tax on the first $7,000 of each employee's wages. This tax funds the federal unemployment insurance program, which provides temporary financial assistance to workers who have lost their jobs through no fault of their own. In addition to FUTA, states also impose their own unemployment taxes, known as State Unemployment Tax Act (SUTA) deductions. These state taxes fund the state unemployment insurance programs, which provide additional support to unemployed workers.

The legal requirements for FUTA and SUTA deductions vary depending on the state in which the employer operates. Some states have higher tax rates than others, and the wage bases for these taxes can also differ. Employers must be aware of the specific requirements in each state where they have employees to ensure compliance with the law. Failure to properly deduct and remit FUTA and SUTA taxes can result in penalties and interest charges.

One unique aspect of FUTA and SUTA deductions is that they are typically not deducted from an employee's pay. Instead, these taxes are paid by the employer out of their own funds. This is in contrast to other payroll taxes, such as Social Security and Medicare, which are withheld from an employee's wages. The employer is responsible for calculating the amount of FUTA and SUTA tax owed and remitting it to the appropriate government agencies on a quarterly basis.

Another important consideration for employers is the potential for tax credits. Some states offer tax credits to employers who pay FUTA and SUTA taxes on time and in full. These credits can help offset the cost of the taxes and provide a financial incentive for employers to comply with the law. Employers should consult with a tax professional to determine if they are eligible for any tax credits related to FUTA and SUTA deductions.

In conclusion, understanding the legal requirements for FUTA and SUTA deductions is crucial for employers to ensure compliance with federal and state laws. These taxes play an important role in funding unemployment insurance programs, which provide vital support to workers who have lost their jobs. Employers must be aware of the specific requirements in each state where they operate and take steps to properly calculate, deduct, and remit these taxes to avoid penalties and interest charges.

Employee Training Pay: Legal Requirements and Best Practices Explained

You may want to see also

Explore related products

![]()

Employee Exemptions: Conditions under which employees might be exempt from these deductions

Certain employees may be exempt from FUTA and SUTA deductions under specific conditions. For instance, if an employee is classified as an independent contractor rather than an employee, they may not be subject to these taxes. Additionally, some states have exemptions for certain types of workers, such as agricultural laborers or domestic workers.

To determine if an employee is exempt, employers must consider various factors, including the nature of the work, the level of control exerted over the worker, and the worker's economic dependence on the employer. Employers should consult state-specific guidelines and seek professional advice if they are unsure about an employee's exemption status.

Exemptions can also apply to certain types of wages, such as tips or overtime pay. For example, under federal law, tips are generally not subject to FUTA tax. However, some states may require employers to pay SUTA on tips. Employers must be aware of these nuances to ensure compliance with all applicable laws.

In some cases, exemptions may be granted on a case-by-case basis. For instance, an employer may apply for a waiver of FUTA tax for a specific employee who meets certain criteria, such as being a student or a veteran. These waivers are typically granted at the discretion of the state or federal tax authority and require careful documentation and application.

Employers must keep accurate records of all employees, including those who are exempt from FUTA and SUTA deductions. This includes maintaining documentation of each employee's classification, wages, and any applicable exemptions. Failure to do so can result in penalties and fines.

In conclusion, while FUTA and SUTA deductions are generally mandatory, there are certain conditions under which employees may be exempt. Employers must be aware of these exemptions and take steps to ensure compliance with all applicable laws and regulations.

Decoding 1099 Taxes: A Comprehensive Guide for Freelancers

You may want to see also

Explore related products

$49.96 $62.99

![]()

Impact on Net Pay: Analyzing how Futa and Suta affect an employee's take-home pay

The impact of FUTA and SUTA on an employee's net pay can be significant, as these taxes are specifically designed to fund unemployment insurance programs. While the exact amount deducted will vary depending on the state and the employee's earnings, it's essential to understand how these taxes affect take-home pay.

FUTA, the Federal Unemployment Tax Act, imposes a tax of 6% on the first $7,000 of an employee's wages. However, employers are often able to claim a credit of up to 5.4% for state unemployment taxes, reducing the effective FUTA tax rate to 0.6%. SUTA, or State Unemployment Tax Act, rates vary by state but typically range from 1% to 5%.

To calculate the impact of FUTA and SUTA on net pay, employees can refer to their pay stubs or W-2 forms, which will list the amounts deducted for these taxes. For example, if an employee earns $50,000 per year and their state has a SUTA rate of 3%, they would pay $1,500 in SUTA taxes annually. With the FUTA tax rate at 0.6%, they would pay an additional $300 in FUTA taxes, for a total of $1,800 in unemployment taxes per year.

It's important to note that these taxes are not optional and are required by law. However, understanding how they affect net pay can help employees make informed decisions about their finances and plan accordingly. For instance, employees may want to adjust their withholding or make additional contributions to retirement accounts to offset the impact of these taxes on their take-home pay.

In conclusion, while FUTA and SUTA taxes are necessary to fund unemployment insurance programs, they can have a noticeable impact on an employee's net pay. By understanding how these taxes work and how they affect take-home pay, employees can better manage their finances and make informed decisions about their financial future.

Accessing Past Pay Stubs: A Comprehensive Guide for Employees

You may want to see also

Frequently asked questions

FUTA (Federal Unemployment Tax Act) and SUTA (State Unemployment Tax Act) are taxes employers pay to fund unemployment insurance programs. While these taxes are typically paid by employers, some states may require employees to contribute a small portion as well. These contributions are deducted from an employee's paycheck to support the unemployment benefits system, ensuring financial assistance is available for workers who lose their jobs through no fault of their own.

The amount deducted from an employee's pay for FUTA and SUTA varies by state and is usually a small percentage of the employee's wages. For example, in some states, the employee contribution for SUTA might be around 0.1% to 0.5% of their earnings. It's important to note that these rates can change, and employees should consult their state's unemployment insurance guidelines for the most current information.

Generally, employees cannot opt out of FUTA and SUTA deductions if they are required by state law. These deductions are mandatory to ensure the sustainability of the unemployment insurance system. However, if an employee believes they are being overcharged or incorrectly charged, they should contact their employer's human resources department or the state's unemployment insurance office to address the issue.