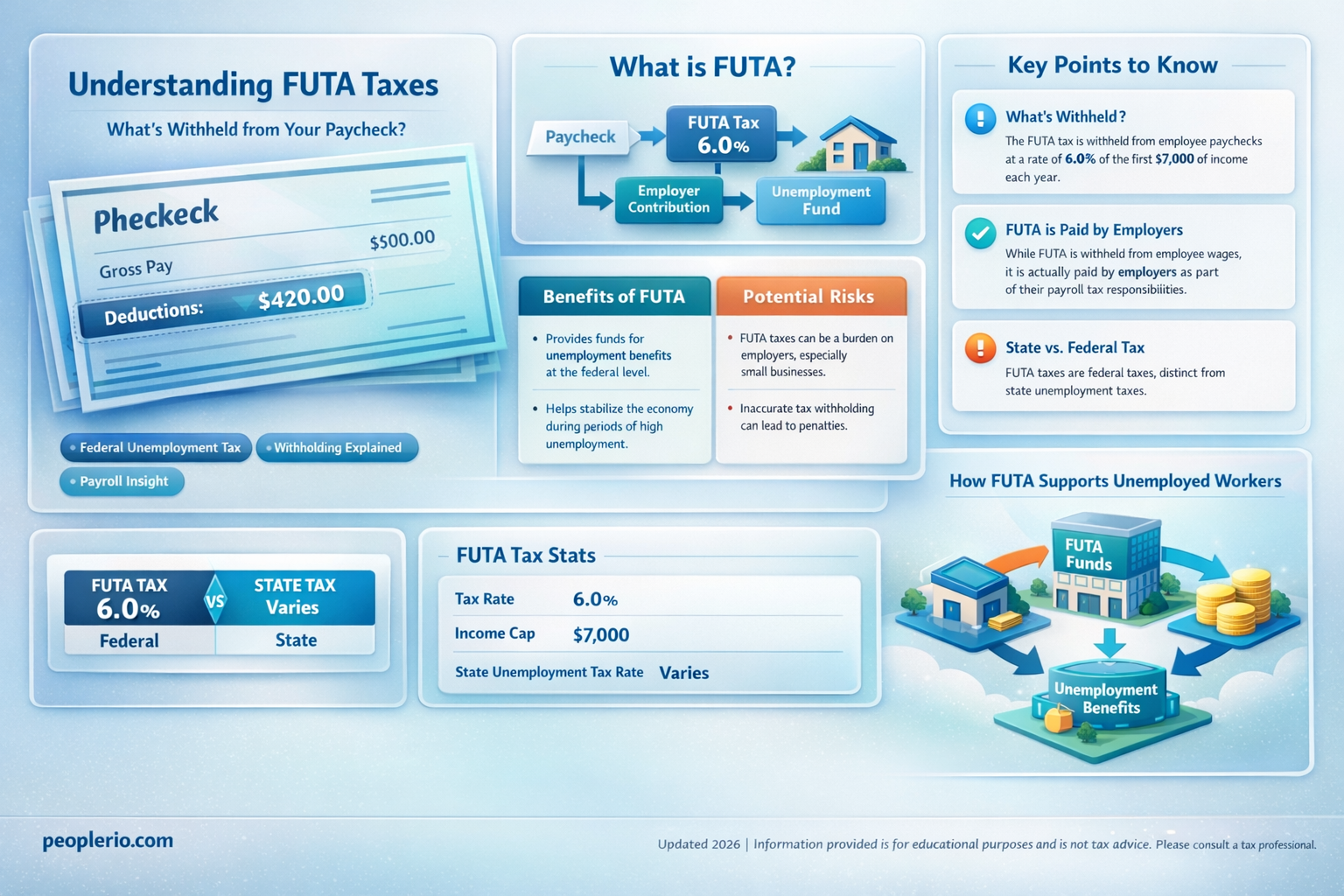

Futa taxes, which are federal unemployment taxes, are indeed withheld from an employee's paycheck. This tax is a crucial component of the United States' unemployment insurance system, providing financial support to workers who have lost their jobs through no fault of their own. The FUTA tax rate is typically 6% of the first $7,000 of an employee's annual wages. Employers are responsible for paying this tax, but it is often deducted from the employee's gross pay, reducing the amount they receive in their paycheck. This deduction is a standard practice in payroll processing, ensuring that both employers and employees contribute to the unemployment insurance fund.

| Characteristics | Values |

|---|---|

| Tax Type | FUTA (Federal Unemployment Tax Act) |

| Purpose | Funds state unemployment insurance programs |

| Tax Rate | 6.2% (as of 2023) |

| Wage Base | First $7,000 of each employee's wages (as of 2023) |

| Payment Frequency | Quarterly |

| Who Pays | Employers |

| Withheld From | Employee paychecks |

| Reporting Requirements | Employers must report FUTA taxes on Form 940 annually |

| Penalties | Employers may face penalties for late payment or underpayment |

| Exemptions | Certain types of workers, such as independent contractors, are exempt from FUTA taxes |

| Impact on Employees | Reduces take-home pay, but provides unemployment benefits if needed |

| Impact on Employers | Increases cost of hiring, but supports state unemployment programs |

| Interaction with Other Taxes | FUTA taxes are in addition to federal income tax and Social Security tax |

| Historical Context | Enacted in 1939 as part of the New Deal |

| Current Status | Active and subject to periodic rate adjustments |

Explore related products

What You'll Learn

- FUTA Tax Basics: Understanding the Federal Unemployment Tax Act and its role in unemployment insurance

- Withholding Mechanics: How FUTA taxes are deducted from employee wages and reported to the IRS

- Employer Responsibilities: Obligations of employers in calculating, withholding, and remitting FUTA taxes

- Employee Impact: The effect of FUTA tax withholding on take-home pay and potential benefits

- Compliance and Penalties: Ensuring adherence to FUTA tax laws and avoiding potential penalties for non-compliance

![]()

FUTA Tax Basics: Understanding the Federal Unemployment Tax Act and its role in unemployment insurance

The Federal Unemployment Tax Act (FUTA) is a crucial component of the United States' unemployment insurance system. Unlike state unemployment taxes, FUTA taxes are not withheld from an employee's paycheck. Instead, FUTA taxes are solely paid by employers. This tax is calculated as a percentage of the first $7,000 of each employee's wages. The current FUTA tax rate is 6%, but employers in states with approved unemployment insurance programs may be eligible for a credit of up to 5.4%, effectively reducing the net FUTA tax rate to as low as 0.6%.

FUTA taxes fund the federal unemployment insurance program, which provides temporary financial assistance to workers who have lost their jobs through no fault of their own. This program is designed to help workers bridge the financial gap while they search for new employment. The funds collected through FUTA taxes are also used to administer the unemployment insurance program and to provide additional support to states with high unemployment rates.

One common misconception about FUTA taxes is that they are similar to Social Security taxes, which are withheld from an employee's paycheck. However, FUTA taxes are distinctly different in that they are paid entirely by employers and are used specifically for unemployment insurance purposes. Social Security taxes, on the other hand, fund the Social Security program, which provides retirement, disability, and survivor benefits.

Employers are required to file a Form 940, Employer's Annual Federal Unemployment Tax Return, to report their FUTA tax liability. This form must be filed by January 31st of each year, and employers must also make quarterly estimated tax payments if their estimated annual FUTA tax liability exceeds $500. Failure to file the required forms or make timely payments can result in penalties and interest charges.

In summary, FUTA taxes play a vital role in funding the federal unemployment insurance program, which provides essential financial support to unemployed workers. While FUTA taxes are not withheld from employee paychecks, they are a significant responsibility for employers, who must ensure accurate calculation, timely filing, and proper payment to avoid penalties. Understanding the basics of FUTA taxes is crucial for both employers and employees to navigate the complexities of the unemployment insurance system effectively.

Decoding Dental Deductions: A Guide to Employee Tax Benefits

You may want to see also

Explore related products

![]()

Withholding Mechanics: How FUTA taxes are deducted from employee wages and reported to the IRS

Employers are responsible for withholding FUTA taxes from their employees' wages. This process involves calculating the tax amount based on the employee's earnings and then deducting it from their paycheck. The FUTA tax rate is currently 6%, but employers may be eligible for a credit reduction, which can lower the effective rate to as low as 0.6%.

To calculate the FUTA tax withholding, employers must first determine the employee's gross wages for the pay period. This includes all forms of compensation, such as salary, tips, and bonuses. Once the gross wages are determined, the employer applies the FUTA tax rate to calculate the withholding amount. For example, if an employee earns $1,000 in a pay period, the FUTA tax withholding would be $60 (6% of $1,000).

Employers are required to report the FUTA tax withholding to the IRS on a quarterly basis using Form 940. This form must be filed by the end of the quarter following the quarter in which the taxes were withheld. For example, if an employer withholds FUTA taxes in the first quarter of the year, they must file Form 940 by the end of the second quarter.

In addition to reporting the withholding amount, employers must also report the total wages paid to each employee during the quarter. This information is used by the IRS to calculate the employer's FUTA tax liability. Employers may be subject to penalties if they fail to report the withholding amount or total wages accurately.

To avoid errors and penalties, employers should ensure that they are using the correct FUTA tax rate and that they are accurately calculating the withholding amount. They should also keep detailed records of all wages paid to employees and the corresponding FUTA tax withholding. By following these guidelines, employers can ensure that they are in compliance with FUTA tax regulations and avoid potential issues with the IRS.

Comparing Employee State Taxes: South Carolina vs. Maryland

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal & State Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71OcM906MLL._AC_UL320_.jpg)

$55.99 $79.99

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![TurboTax Premier Desktop Edition 2025, Federal & State Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71ofxs16-9L._AC_UL320_.jpg)

$82.99 $114.99

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UL320_.jpg)

![]()

Employer Responsibilities: Obligations of employers in calculating, withholding, and remitting FUTA taxes

Employers have several key responsibilities when it comes to FUTA taxes. First and foremost, they must accurately calculate the amount of FUTA tax to be withheld from each employee's paycheck. This calculation is based on the employee's gross wages and the current FUTA tax rate. Employers must also ensure that they are withholding the correct amount from each paycheck, as under-withholding or over-withholding can lead to penalties and interest charges.

In addition to calculating and withholding FUTA taxes, employers are also responsible for remitting these taxes to the IRS on a quarterly basis. This involves filing Form 940, which reports the total amount of FUTA taxes withheld during the quarter. Employers must also pay the FUTA taxes that they have withheld, along with any additional taxes that they owe.

One important aspect of FUTA tax responsibilities is that employers must keep accurate records of all FUTA tax calculations, withholdings, and remittances. This includes maintaining records of employee wages, FUTA tax rates, and any changes to these rates. Employers must also keep track of any penalties or interest charges that they have incurred, and take steps to correct any errors or discrepancies.

Employers should also be aware of any changes to FUTA tax laws and regulations, and adjust their practices accordingly. This may involve updating their payroll systems, training their staff on new procedures, or consulting with a tax professional to ensure compliance.

Overall, employers play a critical role in the FUTA tax system, and it is essential that they understand and fulfill their responsibilities. By accurately calculating, withholding, and remitting FUTA taxes, employers can help ensure that the system operates smoothly and efficiently, and that employees receive the benefits they are entitled to.

Understanding Texas Taxation: Are Andrews Employee Exemptions Taxed?

You may want to see also

Explore related products

![TurboTax Business Desktop Edition 2025, Federal Tax Return [Win11 Download]](https://m.media-amazon.com/images/I/71iKclcd6ML._AC_UL320_.jpg)

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![]()

Employee Impact: The effect of FUTA tax withholding on take-home pay and potential benefits

The impact of FUTA tax withholding on an employee's take-home pay can be significant, particularly for those in lower income brackets. FUTA taxes are a federal unemployment tax that employers are required to withhold from their employees' wages. While the tax rate is relatively low, typically around 0.8%, it can still add up over time and reduce an employee's overall earnings. For example, an employee earning $50,000 per year would have approximately $400 withheld for FUTA taxes annually. This amount may not seem substantial, but it can make a difference for employees who are already struggling to make ends meet.

In addition to the direct impact on take-home pay, FUTA tax withholding can also affect an employee's potential benefits. For instance, some employers may choose to reduce an employee's wages by the amount of FUTA taxes withheld, which could lead to a decrease in the employee's 401(k) contributions or other benefits that are based on their salary. Furthermore, FUTA taxes can also impact an employee's eligibility for certain government programs, such as unemployment benefits. If an employee has had a significant amount of FUTA taxes withheld, they may be ineligible for unemployment benefits if they lose their job.

One unique aspect of FUTA tax withholding is that it can have a disproportionate impact on certain groups of employees. For example, employees who work multiple jobs may have FUTA taxes withheld from each paycheck, which could lead to a higher overall tax burden. Similarly, employees who are paid on a commission basis may have FUTA taxes withheld at a higher rate than those who are paid a fixed salary. This can create a sense of unfairness among employees and may lead to resentment towards the tax system.

To mitigate the impact of FUTA tax withholding, employees can take steps to reduce their overall tax burden. For example, they can contribute to a 401(k) or other retirement plan, which can reduce their taxable income and lower the amount of FUTA taxes withheld. Additionally, employees can take advantage of tax credits and deductions that are available to them, such as the Earned Income Tax Credit or the Child Tax Credit. By understanding how FUTA taxes work and taking steps to reduce their tax burden, employees can minimize the impact of FUTA tax withholding on their take-home pay and potential benefits.

Understanding Employee Tax Deductions: A Comprehensive Guide for Workers

You may want to see also

Explore related products

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UL320_.jpg)

![]()

Compliance and Penalties: Ensuring adherence to FUTA tax laws and avoiding potential penalties for non-compliance

Ensuring adherence to FUTA tax laws is crucial for employers to avoid potential penalties for non-compliance. The Federal Unemployment Tax Act (FUTA) requires employers to pay a federal tax on employee wages to fund unemployment insurance programs. Failure to comply with FUTA regulations can result in significant financial penalties and legal consequences.

To maintain compliance, employers must accurately calculate and remit FUTA taxes on a quarterly basis. This involves determining the taxable wage base, applying the appropriate tax rate, and filing Form 940 with the IRS. Employers should also be aware of any state-specific unemployment tax requirements, as these may differ from federal regulations.

Penalties for non-compliance with FUTA tax laws can be severe. The IRS may impose a penalty of 5% of the unpaid tax amount for each month or part of a month that the tax remains unpaid, up to a maximum of 25%. Additionally, employers may be subject to interest charges on the unpaid tax amount. In cases of willful neglect or fraud, employers may face criminal penalties, including fines and imprisonment.

To avoid these penalties, employers should implement robust payroll processes and tax compliance systems. This may include using payroll software that automatically calculates and remits FUTA taxes, as well as conducting regular audits to ensure accuracy and compliance. Employers should also stay informed about changes to FUTA tax laws and regulations, and seek professional advice if they are unsure about their tax obligations.

In conclusion, compliance with FUTA tax laws is essential for employers to avoid costly penalties and legal repercussions. By implementing effective payroll processes, staying informed about tax regulations, and seeking professional guidance when needed, employers can ensure they meet their FUTA tax obligations and maintain a compliant business operation.

Understanding Employee Stock Options: Tax Implications and Strategies

You may want to see also

Frequently asked questions

Yes, FUTA taxes are typically withheld from an employee's paycheck. Employers are responsible for deducting the appropriate amount and submitting it to the IRS.

The FUTA tax rate is 6.2% on the first $7,000 of an employee's wages. However, employers may be eligible for a credit reduction, which can lower the effective tax rate.

FUTA taxes fund the federal unemployment insurance program, which provides temporary financial assistance to workers who have lost their jobs through no fault of their own.

Certain types of workers, such as independent contractors, agricultural workers, and some religious organization employees, may be exempt from FUTA tax withholding. Additionally, some states have their own unemployment tax systems that may affect FUTA tax requirements.

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![The Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS Penalties](https://m.media-amazon.com/images/I/617DYgupSxL._AC_UL320_.jpg)