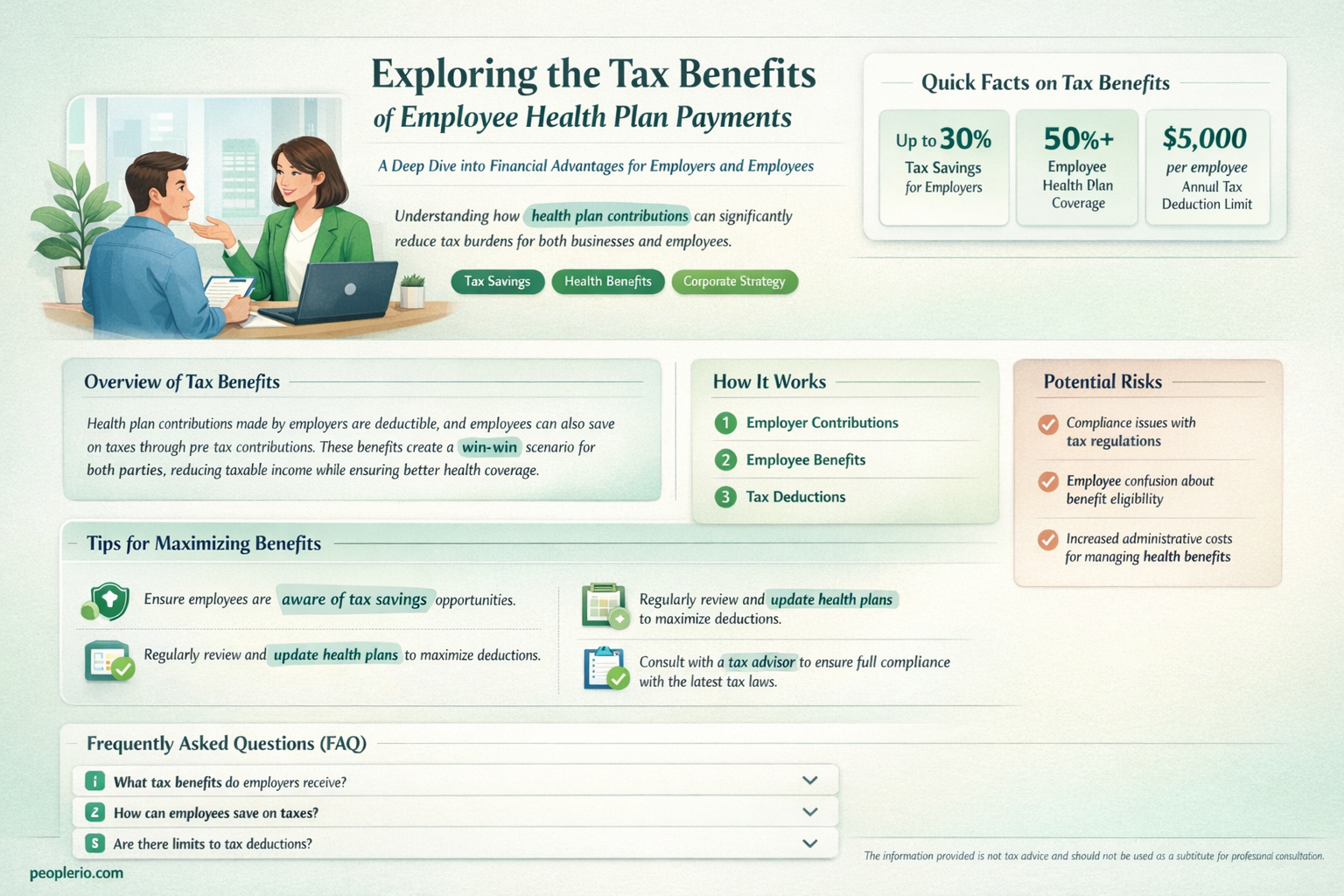

Payments made by an employer towards an employee's health plan are generally considered tax-deductible expenses. This deduction is available under the provisions of the Internal Revenue Code, which allows businesses to deduct the cost of health insurance premiums paid for employees. The deduction helps reduce the employer's taxable income, thereby lowering their overall tax liability. It's important to note that the specifics of these deductions can vary based on the type of health plan, the business structure, and the tax laws in effect for the given year. Employers should consult with a tax professional to ensure they are taking advantage of all available deductions while complying with current tax regulations.

| Characteristics | Values |

|---|---|

| Country | United States |

| Tax Year | 2023 |

| Employee Health Plan Type | Self-insured |

| Payment Type | Premiums |

| Payment Recipient | Insurance company |

| Tax Deductibility for Employer | Generally deductible as a business expense |

| Tax Deductibility for Employee | Contributions may be tax-deductible depending on the plan type |

| IRS Code Reference | Section 162(a) |

| Limitations | Subject to annual contribution limits and other IRS regulations |

| Additional Notes | Consult a tax professional for specific guidance |

Explore related products

What You'll Learn

- General Rule: Payments by employers to employee health plans are generally tax-deductible as business expenses

- Employee Contributions: Contributions made by employees towards their health plans are often tax-deductible as well

- Tax Code Section: The relevant section of the tax code that discusses the deductibility of health plan payments

- Conditions and Limitations: Specific conditions and limitations that apply to the tax deductibility of health plan payments

- Recent Changes: Any recent changes or updates in tax laws affecting the deductibility of health plan payments

![]()

General Rule: Payments by employers to employee health plans are generally tax-deductible as business expenses

Employers often provide health plans to their employees as a benefit, and a common question arises regarding the tax implications of such payments. The general rule is that payments made by employers to employee health plans are tax-deductible as business expenses. This deduction is available under the Internal Revenue Code (IRC) Section 162, which allows businesses to deduct ordinary and necessary expenses incurred in the operation of their trade or business.

To qualify for this deduction, the health plan must meet certain criteria. Firstly, it must be a qualified health plan under the Affordable Care Act (ACA). This means that the plan must provide minimum essential coverage and meet certain actuarial standards. Secondly, the payments must be made for the benefit of employees, and not for the employer's own benefit. This can include payments for employee premiums, as well as contributions to Health Savings Accounts (HSAs) or Health Reimbursement Arrangements (HRAs).

It is important to note that while the payments are tax-deductible for the employer, they are generally taxable as income to the employee. However, there are some exceptions to this rule, such as when the payments are made for premiums on a group health plan that provides minimum essential coverage. In such cases, the payments are not taxable as income to the employee.

Employers should also be aware of the potential impact of these payments on their employees' eligibility for certain government benefits, such as Medicaid or the Children's Health Insurance Program (CHIP). If an employee receives health coverage through their employer, they may not be eligible for these benefits. Employers should therefore consider the overall impact of their health plan offerings on their employees' financial and health situations.

In conclusion, while payments made by employers to employee health plans are generally tax-deductible as business expenses, there are certain criteria that must be met in order to qualify for this deduction. Employers should carefully consider these criteria, as well as the potential impact of these payments on their employees, when designing and implementing their health plan offerings.

Are Employee HSA Contributions Subject to FICA Tax?

You may want to see also

Explore related products

![]()

Employee Contributions: Contributions made by employees towards their health plans are often tax-deductible as well

Contributions made by employees towards their health plans are often tax-deductible as well. This means that when employees pay for their health insurance premiums, they may be able to deduct these expenses from their taxable income. This can result in significant tax savings, especially for those in higher tax brackets.

To qualify for this deduction, employees must meet certain criteria. First, the health plan must be a qualified plan, such as a health savings account (HSA) or a high-deductible health plan (HDHP). Second, the employee must not be enrolled in Medicare. Third, the employee must not be able to deduct the expenses as a business expense.

The deduction for employee contributions is limited to the amount of the employee's adjusted gross income (AGI) that is not covered by employer contributions. For example, if an employee's AGI is $50,000 and their employer contributes $20,000 to their health plan, the employee can deduct up to $30,000 of their own contributions.

It's important to note that this deduction is only available for the current tax year. Employees cannot deduct contributions made in previous years. Additionally, the deduction is not available for contributions made to health plans that are not qualified plans.

Employees should consult with a tax professional to determine if they are eligible for this deduction and to ensure that they are taking advantage of all available tax savings.

Maximize Your Savings: Understanding Pre-Tax Employee Stock Purchase Plans

You may want to see also

Explore related products

![]()

Tax Code Section: The relevant section of the tax code that discusses the deductibility of health plan payments

The relevant section of the tax code that discusses the deductibility of health plan payments is Section 106. This section states that gross income does not include compensation paid by an employer to an employee for medical expenses. This means that payments made by an employer to an employee's health plan are generally tax-deductible. However, there are some important exceptions and limitations to this rule. For example, if the payments are made to a health savings account (HSA) or a flexible spending account (FSA), they may not be tax-deductible. Additionally, if the payments are made to a health plan that is not a qualified health plan under the Affordable Care Act, they may not be tax-deductible.

It is important to note that the tax code is complex and constantly changing. Employers and employees should consult with a tax professional to ensure that they are taking advantage of all available tax deductions and credits. Additionally, employers should review their health plan documents to ensure that they are in compliance with all applicable tax laws and regulations.

In conclusion, while payments to an employee's health plan are generally tax-deductible, there are some important exceptions and limitations to this rule. Employers and employees should consult with a tax professional to ensure that they are taking advantage of all available tax deductions and credits.

Are Employee Bonuses Tax Deductible? A Comprehensive Guide for Employers

You may want to see also

Explore related products

![]()

Conditions and Limitations: Specific conditions and limitations that apply to the tax deductibility of health plan payments

To qualify for tax deductibility, health plan payments must meet specific conditions set by the IRS. One key condition is that the payments must be for qualified medical expenses. These expenses include costs for medical care, hospitalization, and prescription drugs, among others. However, expenses for cosmetic surgery, except for certain reconstructive procedures, are generally not deductible.

Another important limitation is that the payments must be made directly to the healthcare provider or insurance company. Payments made to employees as reimbursements for their health expenses are not deductible by the employer. Additionally, the health plan must be established and maintained for the benefit of employees, and not for the benefit of the employer or other non-employees.

The IRS also imposes a limit on the amount of health plan payments that can be deducted. For example, there are annual limits on the amount of flexible spending account (FSA) contributions that can be made tax-free. Furthermore, the Affordable Care Act (ACA) imposes a limit on the amount of health insurance premiums that can be deducted for tax purposes.

Employers must also be aware of the nondiscrimination rules that apply to health plans. These rules prohibit employers from favoring certain employees or groups of employees in the design or operation of their health plans. Failure to comply with these rules can result in the loss of tax deductibility for health plan payments.

In conclusion, while health plan payments can be tax deductible, they must meet specific conditions and limitations set by the IRS. Employers must carefully consider these rules when designing and operating their health plans to ensure that they maximize the tax benefits available to them.

Mastering Employee Tax Filing: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![]()

Recent Changes: Any recent changes or updates in tax laws affecting the deductibility of health plan payments

The Tax Cuts and Jobs Act (TCJA) of 2017 introduced significant changes to the tax landscape, including the elimination of the individual mandate penalty and the expansion of Health Savings Accounts (HSAs). While the TCJA did not directly address the deductibility of health plan payments, it did impact the overall tax treatment of health-related expenses. For instance, the increase in the standard deduction and the limitation on itemized deductions may affect the tax benefits of contributing to a health plan.

In 2020, the CARES Act provided additional tax relief in response to the COVID-19 pandemic. This legislation included provisions that allowed for the tax-free distribution of HSA funds for qualified medical expenses and the temporary suspension of the requirement that HSA distributions be used for qualified medical expenses to avoid penalties. These changes may have indirectly influenced the deductibility of health plan payments by altering the tax advantages of using HSAs.

More recently, the Inflation Reduction Act (IRA) of 2022 has introduced new provisions that could impact the tax treatment of health plan payments. For example, the IRA extends the temporary suspension of the HSA distribution requirement for qualified medical expenses through 2025. Additionally, the IRA includes provisions that may affect the tax benefits of employer-sponsored health plans, such as the extension of the tax credit for small employers providing health insurance.

It is essential for employers and employees to stay informed about these recent changes in tax laws to maximize the tax benefits associated with health plan payments. Consulting with a tax professional or financial advisor can help individuals and businesses navigate the complex tax implications of these legislative updates and ensure compliance with current tax regulations.

Understanding 401(k) Tax Exemptions in New Mexico: A Guide for Employees

You may want to see also

Frequently asked questions

Yes, payments made by an employer to an employee health plan are generally tax-deductible as a business expense. This deduction helps reduce the employer's taxable income, providing a financial benefit.

Yes, premiums paid by employees for their health insurance plans can be tax-deductible. If the premiums are paid with pre-tax dollars through a payroll deduction, they are not included in the employee's taxable income. Additionally, if the employee itemizes their deductions on their tax return, they may be able to deduct the premiums paid out-of-pocket.

If an employer reimburses an employee for their health insurance premiums, the reimbursement is generally considered taxable income to the employee. However, if the reimbursement is made through a qualified health reimbursement arrangement (HRA) or a health savings account (HSA), it may be tax-free to the employee. Employers should consult with a tax professional to ensure proper structuring of such arrangements.