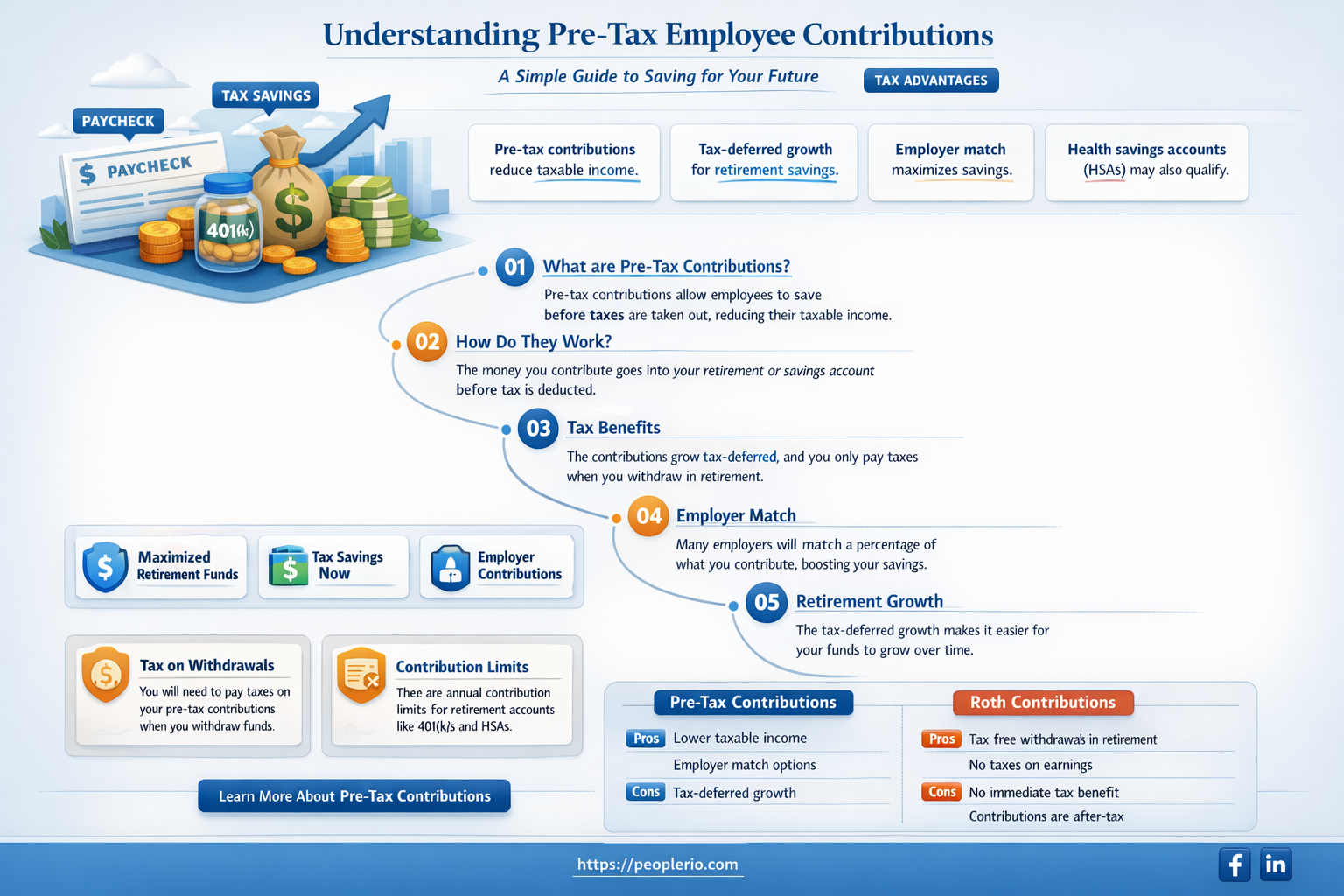

Employee contributions to certain benefit plans, such as 401(k)s or other retirement savings accounts, are often made on a pre-tax basis. This means that the money is deducted from an employee's paycheck before taxes are calculated, reducing their taxable income. Pre-tax contributions can lower an individual's tax liability and increase the amount of money they can save for retirement. However, it's important to note that while these contributions are tax-deferred, they will be taxed when withdrawn in retirement. Additionally, there are typically limits on how much an employee can contribute pre-tax each year, and these limits may vary depending on the specific plan and the employee's age.

Explore related products

What You'll Learn

- Definition of Pre-Tax Contributions: Understanding what pre-tax contributions are and how they differ from post-tax contributions

- Types of Pre-Tax Contributions: Exploring various types, such as 401(k), 403(b), and IRA contributions

- Benefits of Pre-Tax Contributions: Discussing the advantages, including tax savings and potential for higher investment returns

- Limits on Pre-Tax Contributions: Reviewing the annual contribution limits set by the IRS for different types of accounts

- Impact on Take-Home Pay: Analyzing how pre-tax contributions affect an employee's take-home pay and overall financial planning

![]()

Definition of Pre-Tax Contributions: Understanding what pre-tax contributions are and how they differ from post-tax contributions

Pre-tax contributions refer to the practice of deducting certain expenses from an individual's gross income before taxes are calculated. This is in contrast to post-tax contributions, where the expenses are deducted after taxes have been applied. Understanding the difference between these two types of contributions is crucial for employees and employers alike, as it can significantly impact the overall tax liability and financial planning.

One common example of pre-tax contributions is the 401(k) retirement plan. When an employee contributes to their 401(k), the amount is deducted from their gross income before federal, state, and local taxes are applied. This reduces the employee's taxable income, resulting in a lower tax bill. Additionally, the contributed funds grow tax-deferred within the 401(k) account, meaning that the investment earnings are not subject to taxation until the funds are withdrawn in retirement.

On the other hand, post-tax contributions are typically made to Roth IRAs or Roth 401(k)s. In these cases, the contributions are made with after-tax dollars, meaning that the individual has already paid taxes on the money before it is invested. However, the advantage of post-tax contributions is that the funds grow tax-free, and qualified withdrawals in retirement are also tax-free.

It is important to note that pre-tax contributions can also include other types of deductions, such as health insurance premiums, flexible spending account (FSA) contributions, and dependent care flexible spending account (DCFSA) contributions. These deductions can help reduce an individual's taxable income, resulting in a lower tax bill.

In conclusion, understanding the difference between pre-tax and post-tax contributions is essential for making informed financial decisions. Pre-tax contributions can help reduce taxable income and lower tax liability, while post-tax contributions offer tax-free growth and withdrawals in retirement. By carefully considering the options available, individuals can optimize their financial planning and achieve their long-term goals.

Unlocking the Tax Benefits of Employee Christmas Parties

You may want to see also

Explore related products

![]()

Types of Pre-Tax Contributions: Exploring various types, such as 401(k), 403(b), and IRA contributions

- K) contributions are one of the most common types of pre-tax contributions. They are offered by many employers and allow employees to save a portion of their income before taxes are taken out. The money saved in a 401(k) account grows tax-deferred, meaning that the earnings on the investments are not taxed until the money is withdrawn in retirement.

- B) contributions are similar to 401(k) contributions but are typically offered by non-profit organizations, such as schools and hospitals. They also allow employees to save a portion of their income before taxes are taken out, and the money grows tax-deferred. However, 403(b) plans may have different investment options and fees compared to 401(k) plans.

IRA contributions are another type of pre-tax contribution that individuals can make to save for retirement. There are two main types of IRAs: traditional IRAs and Roth IRAs. Traditional IRAs allow individuals to contribute pre-tax dollars, while Roth IRAs require after-tax dollars. The money in both types of IRAs grows tax-deferred, but the earnings on Roth IRA investments are not taxed when withdrawn in retirement.

When deciding which type of pre-tax contribution to make, it's important to consider factors such as the fees associated with each plan, the investment options available, and the tax implications of withdrawing the money in retirement. It's also important to consult with a financial advisor to determine which plan is best suited for an individual's specific financial situation and retirement goals.

Unlocking the Tax Benefits of Employee Stock Purchase Plans

You may want to see also

Explore related products

$14.87 $19.99

![]()

Benefits of Pre-Tax Contributions: Discussing the advantages, including tax savings and potential for higher investment returns

Pre-tax contributions offer a significant advantage in the realm of personal finance, particularly when it comes to saving for retirement. By contributing to retirement accounts before taxes are deducted, individuals can reduce their taxable income, thereby lowering the amount of tax owed. This immediate tax benefit can result in substantial savings over time, allowing individuals to allocate more funds towards their retirement goals.

One of the key benefits of pre-tax contributions is the potential for higher investment returns. Since the contributions are made before taxes, the entire amount can be invested, allowing for compound interest to work its magic over the years. This can lead to a larger retirement nest egg compared to after-tax contributions, where a portion of the funds is already reduced by taxes before being invested.

Moreover, pre-tax contributions can also provide a psychological boost to savers. Seeing a larger amount of money being invested can create a sense of accomplishment and motivation to continue saving. Additionally, many employers offer matching contributions to pre-tax retirement accounts, further enhancing the benefits of this savings strategy.

However, it is important to note that pre-tax contributions may have certain limitations and considerations. For instance, there are typically caps on the amount that can be contributed pre-tax each year, and withdrawing funds before retirement may result in penalties and taxes. Therefore, it is crucial for individuals to understand the rules and regulations associated with pre-tax contributions to maximize their benefits while avoiding potential pitfalls.

In conclusion, pre-tax contributions can be a powerful tool in building a secure financial future. By offering immediate tax benefits and the potential for higher investment returns, this savings strategy can help individuals achieve their retirement goals more effectively. However, it is essential to be aware of the limitations and considerations associated with pre-tax contributions to make the most of this financial opportunity.

Understanding PPP Loans: Do They Cover Employee Taxes?

You may want to see also

Explore related products

![]()

Limits on Pre-Tax Contributions: Reviewing the annual contribution limits set by the IRS for different types of accounts

The IRS sets annual contribution limits for various types of retirement accounts, which can significantly impact an individual's ability to save for retirement on a pre-tax basis. For example, in 2023, the contribution limit for a Traditional IRA is $6,500 for individuals under age 50, and $7,500 for those 50 and older. These limits apply to the total contributions made across all IRAs, including both Traditional and Roth IRAs.

For employer-sponsored plans such as 401(k)s, the contribution limits are higher. In 2023, employees can contribute up to $22,500 to a 401(k) plan, with an additional $7,500 catch-up contribution allowed for those 50 and older. These limits apply to each plan separately, allowing individuals with multiple 401(k) plans to contribute the maximum amount to each.

It's important to note that these contribution limits are subject to change, and individuals should consult the IRS website or a tax professional for the most up-to-date information. Exceeding these limits can result in penalties and taxes, so it's crucial to stay within the guidelines set by the IRS.

One strategy to maximize pre-tax contributions is to contribute the maximum amount allowed to each type of account. For example, an individual could contribute $6,500 to a Traditional IRA and $22,500 to a 401(k) plan, for a total of $29,000 in pre-tax contributions. This can significantly reduce taxable income and increase retirement savings.

However, it's also important to consider the trade-offs between contributing to different types of accounts. For example, while Traditional IRA contributions are tax-deductible, the earnings grow tax-deferred, and withdrawals are taxed as ordinary income. In contrast, Roth IRA contributions are made with after-tax dollars, but the earnings grow tax-free, and withdrawals are generally tax-free. Understanding these differences can help individuals make informed decisions about how to allocate their retirement contributions.

Understanding Pre-Tax Employee Health Insurance Contributions

You may want to see also

Explore related products

![]()

Impact on Take-Home Pay: Analyzing how pre-tax contributions affect an employee's take-home pay and overall financial planning

Pre-tax contributions can significantly impact an employee's take-home pay, affecting their overall financial planning and budgeting. When an employee contributes to a pre-tax retirement plan, such as a 401(k) or IRA, the amount contributed is deducted from their gross income before taxes are calculated. This reduces the employee's taxable income, resulting in a lower tax liability and, consequently, a higher take-home pay. For example, if an employee contributes $5,000 to a pre-tax retirement plan and their marginal tax rate is 25%, they would save $1,250 in taxes, increasing their take-home pay by that amount.

However, it's essential to consider the long-term implications of these contributions. While pre-tax contributions can increase take-home pay in the short term, they also reduce the amount of money available for other financial goals, such as saving for a down payment on a house or paying off high-interest debt. Employees must carefully balance their retirement savings goals with their current financial needs to ensure they are making the most informed decisions about their pre-tax contributions.

Another factor to consider is the potential for investment growth within the retirement plan. Pre-tax contributions can grow tax-deferred, meaning the earnings on those contributions are not taxed until withdrawal. This can significantly increase the overall value of the retirement plan over time, providing a more substantial financial cushion for the employee's future. However, it's crucial to understand the investment options available within the plan and to make informed decisions about asset allocation to maximize growth potential while managing risk.

In conclusion, pre-tax contributions can have a profound impact on an employee's take-home pay and overall financial planning. While they can increase take-home pay in the short term and provide long-term investment growth, employees must carefully consider their current financial needs and future goals to ensure they are making the most informed decisions about their pre-tax contributions. By understanding the implications of these contributions and balancing them with other financial priorities, employees can optimize their financial planning and achieve greater financial security.

Tax-Free Employee Bonuses: Smart Strategies for Rewarding Your Team

You may want to see also

Frequently asked questions

"Pre-tax" refers to deductions taken from an employee's gross income before taxes are calculated. These contributions are subtracted from the total taxable income, potentially lowering the overall tax liability.

Not all employee contributions are pre-tax. While some contributions, like those to 401(k) plans or certain health insurance premiums, are typically pre-tax, others may be post-tax, meaning they are deducted after taxes have been calculated.

Pre-tax employee contributions reduce an individual's taxable income. This can result in a lower tax bill because the contributions are not subject to income tax until they are withdrawn, if at all, depending on the type of plan.

Common examples of pre-tax employee contributions include 401(k) plan contributions, certain health insurance premiums, flexible spending account (FSA) contributions, and dependent care assistance program (DCAP) contributions.

Pre-tax contributions are typically used for specific types of employee benefits that are designed to provide tax advantages. These include retirement plans, health insurance, and certain types of savings plans. Not all employee benefits qualify for pre-tax contributions.