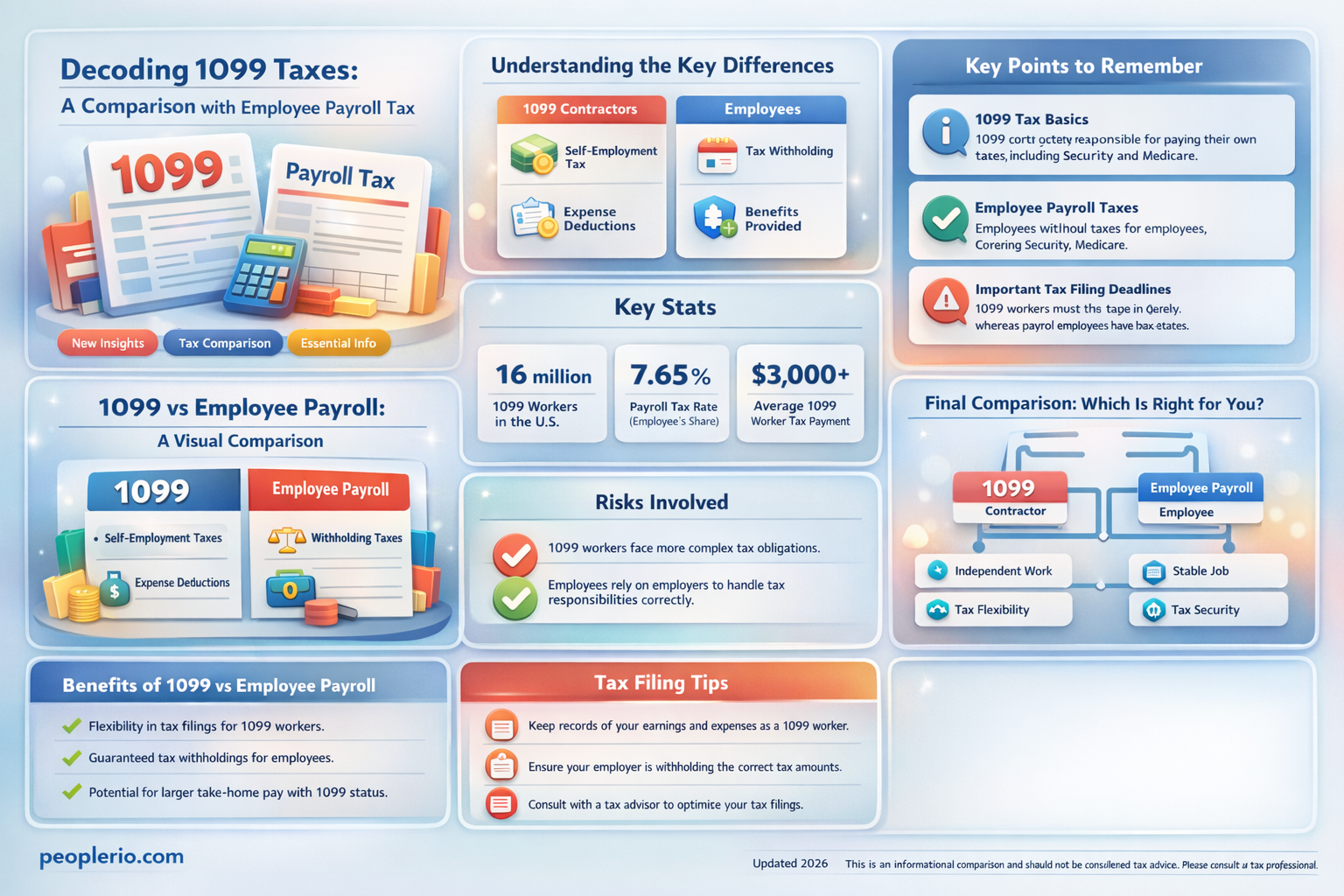

When comparing taxes on 1099 income to employee payroll taxes, it's important to understand the distinctions between these two types of taxation. Taxes on 1099 income, which is typically earned by independent contractors or freelancers, include self-employment taxes that cover both the employer and employee portions of Social Security and Medicare. This means that the individual is responsible for paying the full 15.3% self-employment tax rate on their net earnings. In contrast, employee payroll taxes are split between the employer and the employee, with each party paying 7.65% for Social Security and Medicare combined. Additionally, 1099 earners may also be subject to income tax, which varies based on their tax bracket. Therefore, while the overall tax burden can be higher for 1099 earners due to the self-employment tax, the specific comparison to employee payroll taxes depends on the individual's earnings and tax situation.

Explore related products

What You'll Learn

- Comparison of Tax Rates: Analyze if 1099 taxes are lower than employee payroll taxes

- Tax Deductions: Explore potential deductions available for 1099 contractors vs. employees

- Social Security and Medicare: Compare contributions to Social Security and Medicare between 1099 and payroll taxes

- Filing Requirements: Outline the filing requirements and deadlines for 1099 contractors and employees

- Impact on Take-Home Pay: Calculate the net impact on take-home pay for 1099 contractors vs. employees

![]()

Comparison of Tax Rates: Analyze if 1099 taxes are lower than employee payroll taxes

To analyze whether taxes on 1099 income are lower than employee payroll taxes, we need to delve into the specifics of how each type of income is taxed. 1099 income refers to earnings received by independent contractors or freelancers, which are reported on a Form 1099. This income is subject to self-employment taxes, which include both the employer and employee portions of Social Security and Medicare taxes.

On the other hand, employee payroll taxes are deducted from an employee's paycheck and include Social Security, Medicare, and sometimes state and local taxes. The employer also contributes a portion of these taxes. The key difference lies in the fact that independent contractors pay both the employer and employee portions of these taxes, while employees only pay the employee portion.

Let's break down the tax rates:

- Social Security Tax: For employees, the Social Security tax rate is 6.2% of their wages, up to a certain wage base limit. Employers match this amount. For independent contractors, the self-employment tax rate for Social Security is 15.3% of their net earnings, which includes both the employer and employee portions.

- Medicare Tax: Employees pay a Medicare tax of 1.45% on all wages, with an additional 0.9% on wages above a certain threshold. Employers match the 1.45% rate. Independent contractors pay a Medicare tax of 2.9% on their net earnings, which also includes both the employer and employee portions.

By comparing these rates, it's evident that the combined self-employment tax rate for independent contractors (15.3% for Social Security plus 2.9% for Medicare) is higher than the combined payroll tax rate for employees (6.2% for Social Security plus 1.45% for Medicare, with the employer matching these amounts).

However, it's important to note that independent contractors may be able to deduct certain business expenses, which can lower their taxable income and, consequently, their overall tax liability. Additionally, the self-employment tax is calculated based on net earnings, which can be lower than an employee's gross wages due to deductions for business expenses.

In conclusion, while the tax rates on 1099 income are generally higher than employee payroll taxes, the ability to deduct business expenses can help mitigate this difference. Independent contractors should carefully consider their business expenses and consult with a tax professional to optimize their tax strategy.

Understanding Tax Implications of Moving Expenses under Accountable Plans

You may want to see also

Explore related products

![]()

Tax Deductions: Explore potential deductions available for 1099 contractors vs. employees

As a 1099 contractor, you have the advantage of claiming various tax deductions that are not available to traditional employees. One significant deduction is for business expenses, which can include costs such as equipment, supplies, travel, and home office expenses. This deduction can help reduce your taxable income, thereby lowering your overall tax liability.

Another deduction available to 1099 contractors is the deduction for health insurance premiums. If you purchase your own health insurance, you may be able to deduct the premiums on your tax return. This deduction can be particularly valuable, as health insurance costs can be substantial.

In addition to these deductions, 1099 contractors may also be able to take advantage of the deduction for retirement plan contributions. If you contribute to a retirement plan, such as a SEP IRA or a Solo 401(k), you may be able to deduct the contributions on your tax return. This deduction can help you save for retirement while also reducing your taxable income.

It's important to note that while these deductions can be beneficial, they are subject to certain rules and limitations. For example, the deduction for business expenses is only available for expenses that are ordinary and necessary for your business. Similarly, the deduction for health insurance premiums is only available if you are not eligible for employer-sponsored health insurance.

Overall, the ability to claim these deductions can help 1099 contractors reduce their tax liability and save money. However, it's important to carefully review the rules and limitations associated with each deduction to ensure that you are eligible and that you are claiming the deductions correctly.

Unraveling the Tax Deduction Mystery: Employee Entertainment Expenses Explained

You may want to see also

Explore related products

![]()

Social Security and Medicare: Compare contributions to Social Security and Medicare between 1099 and payroll taxes

The comparison between contributions to Social Security and Medicare via 1099 forms versus payroll taxes reveals significant differences. For individuals receiving income through 1099 forms, such as freelancers or independent contractors, the responsibility for contributing to these programs falls squarely on their shoulders. They are required to pay the full amount of Social Security and Medicare taxes, which can be a substantial financial burden. This is in stark contrast to employees who only pay a portion of these taxes, with their employers covering the remaining balance.

One of the key distinctions lies in the tax rates applied. For payroll taxes, the Social Security tax rate is 6.2% for employees, with employers matching this amount. The Medicare tax rate is 1.45% for employees, again matched by employers. However, for those earning income through 1099 forms, the self-employment tax rate for Social Security is 12.4%, and the Medicare tax rate is 2.9%. This means that self-employed individuals pay more than double the amount in Social Security taxes compared to their employed counterparts.

Furthermore, the cap on taxable earnings for Social Security contributions differs between the two scenarios. For employees, the cap is adjusted annually, but for self-employed individuals, it is typically higher, leading to a larger portion of their income being subject to taxation. This can result in a significant disparity in the total amount contributed to Social Security over the course of a year.

In terms of Medicare, while the tax rate is lower for self-employed individuals, they do not benefit from the employer match. This means that, in practice, they may end up paying more out of pocket for Medicare coverage compared to employees who receive a subsidy from their employers.

Overall, the data suggests that taxes on 1099 forms are indeed less favorable than employee payroll taxes when it comes to contributions to Social Security and Medicare. Self-employed individuals bear a heavier tax burden and receive fewer benefits, highlighting the importance of understanding the tax implications of different income sources.

Understanding FERS: Are Employee Contributions Made with After-Tax Dollars?

You may want to see also

Explore related products

![]()

Filing Requirements: Outline the filing requirements and deadlines for 1099 contractors and employees

For 1099 contractors, the filing requirements and deadlines are distinct from those of traditional employees. Contractors must file their taxes as self-employed individuals, which involves different forms and schedules compared to the W-2 forms used by employees. The primary form for contractors is the 1099-MISC, which reports miscellaneous income. Contractors must also file Schedule C (Form 1040) to report their business income and expenses. The deadline for filing these forms is typically April 15th, the same as for individual income tax returns.

In contrast, employees have their taxes withheld by their employers and reported on W-2 forms. Employers are responsible for filing these forms with the IRS by the end of January each year. Employees then use the information from their W-2 forms to file their individual income tax returns by April 15th.

One key difference between contractors and employees is the responsibility for paying self-employment taxes. Contractors must pay both the employer and employee portions of Social Security and Medicare taxes, which can be a significant additional cost. Employees, on the other hand, only pay the employee portion of these taxes, with their employers covering the employer portion.

Contractors must also be aware of the requirement to make estimated tax payments throughout the year. Since their taxes are not withheld by an employer, contractors must make quarterly payments to the IRS to avoid penalties. These payments are based on the contractor's estimated annual tax liability.

In summary, while both contractors and employees must file tax returns by April 15th, the specific forms and requirements differ significantly. Contractors must file 1099-MISC forms and Schedule C, pay self-employment taxes, and make estimated tax payments, whereas employees file W-2 forms and have their taxes withheld by their employers.

Understanding the Relationship Between Employee Income Tax and Expenses

You may want to see also

Explore related products

![]()

Impact on Take-Home Pay: Calculate the net impact on take-home pay for 1099 contractors vs. employees

To calculate the net impact on take-home pay for 1099 contractors versus employees, we need to consider several factors. First, let's understand the basic difference in tax withholding between the two. Employees have taxes withheld from their paychecks, including federal income tax, Social Security tax, and Medicare tax. In contrast, 1099 contractors are responsible for paying these taxes themselves, typically through quarterly estimated tax payments.

One key advantage for 1099 contractors is the potential to deduct business expenses, which can reduce their taxable income. Employees, on the other hand, have limited deductions available to them. For example, an employee might be able to deduct the cost of commuting or work-related education, but these deductions are often capped or subject to specific rules.

Another factor to consider is the self-employment tax, which 1099 contractors must pay. This tax covers the contractor's share of Social Security and Medicare taxes, and it can be a significant additional cost. Employees pay these taxes through payroll withholding, but they do not have to worry about making separate payments.

To get a clear picture of the impact on take-home pay, let's look at a hypothetical example. Suppose an employee earns $50,000 per year, and their employer withholds 25% of their income for taxes. This means the employee takes home $37,500. Now, let's consider a 1099 contractor who earns the same amount. Assuming they have $10,000 in business expenses, their taxable income would be $40,000. If they pay 25% in taxes, they would owe $10,000. However, they would also need to pay self-employment tax, which could add another $3,000 to their tax bill. This means the contractor's take-home pay would be $37,000.

In this example, the employee's take-home pay is slightly higher than the contractor's. However, it's important to note that this is just one scenario, and the actual impact on take-home pay can vary widely depending on individual circumstances. Factors such as the amount of business expenses, the tax bracket, and the state of residence can all influence the final outcome.

In conclusion, while 1099 contractors may have more flexibility in terms of deductions and tax planning, they also face additional costs such as self-employment tax. Employees, on the other hand, have taxes withheld from their paychecks, but they may have fewer deductions available to them. To determine the net impact on take-home pay, it's essential to consider all these factors and calculate the specific situation for each individual.

Exploring the Tax Benefits of School Employee Union Dues

You may want to see also

Frequently asked questions

Taxes on a 1099 form can be different from employee payroll taxes. 1099 forms are used for reporting income to independent contractors, and the tax rates can vary based on the type of income and the contractor's tax situation. Employee payroll taxes, on the other hand, are typically withheld from an employee's paycheck and include Social Security and Medicare taxes. The comparison between the two can depend on various factors, including the individual's income level and tax deductions.

1099 taxes and employee payroll taxes both include Social Security and Medicare taxes, but the way they are calculated and paid can differ. For employees, these taxes are withheld from their paychecks, with the employer matching the employee's contribution. For independent contractors receiving income through a 1099 form, they are responsible for paying both the employee and employer portions of these taxes, which can result in a higher overall tax liability.

Several factors can influence whether 1099 taxes are less than employee payroll taxes. These include the individual's income level, tax deductions and credits, the state in which they reside, and their overall tax situation. Independent contractors may have more opportunities for tax deductions related to their business expenses, which could potentially lower their tax liability. However, they also have to pay both the employee and employer portions of Social Security and Medicare taxes, which can increase their tax burden. Ultimately, the comparison between 1099 taxes and employee payroll taxes depends on the specific circumstances of the individual.