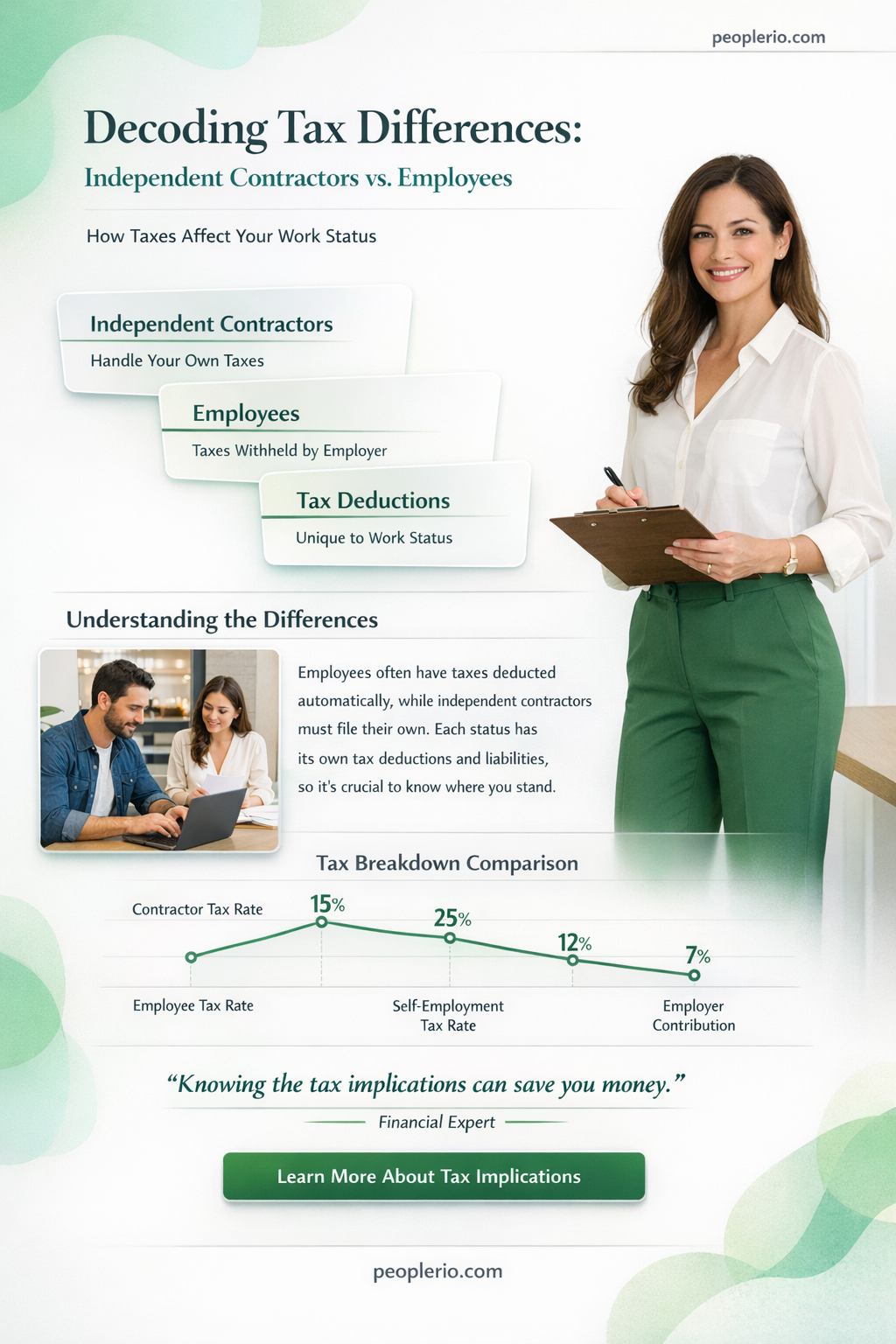

When comparing the tax implications of being an independent contractor versus an employee, several key differences come into play. As an independent contractor, you are responsible for paying both the employer and employee portions of Social Security and Medicare taxes, which can significantly increase your tax burden. Additionally, independent contractors often have more complex tax situations due to the need to track and deduct business expenses, manage estimated tax payments, and navigate the intricacies of self-employment tax. On the other hand, employees typically have their taxes withheld by their employer, simplifying the tax process and potentially reducing the overall tax liability. However, employees may have less control over their tax deductions and credits. Ultimately, the choice between being an independent contractor or an employee can have a substantial impact on your tax obligations and financial planning.

Explore related products

$14.99 $14.99

$30.91 $39.99

What You'll Learn

- Tax Rates Comparison: Independent contractors often face higher tax rates due to self-employment taxes, impacting overall income

- Deductions and Credits: Employees may have more opportunities for tax deductions and credits through employer-sponsored benefits and programs

- Filing Requirements: Independent contractors must file quarterly estimated taxes and pay self-employment taxes, adding complexity to tax obligations

- Health Insurance: Employees typically receive health insurance through their employer, which can be a significant tax advantage

- Retirement Savings: Employer-sponsored retirement plans, like 401(k)s, offer tax benefits that independent contractors may not have access to

![]()

Tax Rates Comparison: Independent contractors often face higher tax rates due to self-employment taxes, impacting overall income

Independent contractors often face higher tax rates due to self-employment taxes, impacting overall income. This is because, unlike employees, independent contractors are responsible for paying both the employer and employee portions of Social Security and Medicare taxes. This can result in a significant increase in tax liability, reducing the overall income of independent contractors compared to employees.

For example, in the United States, the self-employment tax rate is 15.3% of net earnings, which is comprised of 12.4% for Social Security and 2.9% for Medicare. In contrast, employees only pay 7.65% of their wages in Social Security and Medicare taxes, with their employers matching this amount. This means that independent contractors pay more than double the amount in self-employment taxes compared to employees.

Furthermore, independent contractors may also be subject to additional taxes, such as state and local income taxes, as well as other business-related taxes, such as sales tax or property tax. These additional taxes can further reduce the overall income of independent contractors, making it even more challenging to manage their finances effectively.

To mitigate the impact of higher tax rates, independent contractors can take advantage of various tax deductions and credits available to them. For example, they can deduct business expenses, such as equipment, supplies, and travel costs, as well as claim credits for health insurance premiums and retirement plan contributions. By carefully managing their tax liabilities and taking advantage of available deductions and credits, independent contractors can reduce the overall impact of higher tax rates on their income.

In conclusion, independent contractors face higher tax rates due to self-employment taxes, which can significantly impact their overall income. However, by understanding their tax obligations and taking advantage of available deductions and credits, independent contractors can effectively manage their tax liabilities and maximize their income.

Exploring the Tax Benefits of HRA Employee Contributions

You may want to see also

Explore related products

![]()

Deductions and Credits: Employees may have more opportunities for tax deductions and credits through employer-sponsored benefits and programs

Employees may have more opportunities for tax deductions and credits through employer-sponsored benefits and programs. This is because employers often provide a range of benefits that can reduce an employee's taxable income, such as health insurance, retirement plans, and flexible spending accounts. Additionally, employers may offer programs that allow employees to deduct certain expenses from their paychecks, such as charitable contributions or dependent care costs. These deductions and credits can significantly reduce an employee's tax liability, potentially resulting in a lower tax bill or even a refund.

One example of an employer-sponsored benefit that can provide tax deductions is a 401(k) retirement plan. Contributions to a 401(k) plan are made on a pre-tax basis, which means that the amount contributed is deducted from the employee's taxable income. This can result in a significant tax savings, especially for employees who contribute a large portion of their income to the plan. Additionally, some employers may offer a matching contribution to the 401(k) plan, which can further increase the tax savings for the employee.

Another example of an employer-sponsored benefit that can provide tax credits is a health savings account (HSA). HSAs are available to employees who have a high-deductible health plan and are not enrolled in Medicare. Contributions to an HSA are made on a pre-tax basis, and the funds can be used to pay for qualified medical expenses. The tax credit for HSA contributions can be significant, especially for employees who have high medical expenses.

Employers may also offer programs that allow employees to deduct certain expenses from their paychecks. For example, some employers may offer a dependent care flexible spending account (FSA), which allows employees to deduct the cost of child care or elder care from their taxable income. This can result in a significant tax savings for employees who have high dependent care costs.

In conclusion, employees may have more opportunities for tax deductions and credits through employer-sponsored benefits and programs. These deductions and credits can significantly reduce an employee's tax liability, potentially resulting in a lower tax bill or even a refund. Examples of employer-sponsored benefits that can provide tax deductions and credits include 401(k) retirement plans, health savings accounts, and dependent care flexible spending accounts.

Unlocking the Perks: Are Employee Benefits Tax Deferred?

You may want to see also

Explore related products

![]()

Filing Requirements: Independent contractors must file quarterly estimated taxes and pay self-employment taxes, adding complexity to tax obligations

Independent contractors face a unique set of tax obligations that can significantly impact their financial planning and compliance. Unlike employees, who have taxes withheld from their paychecks, independent contractors are responsible for estimating and paying their own taxes on a quarterly basis. This includes self-employment taxes, which cover Social Security and Medicare, and are calculated based on the contractor's net earnings.

The process of filing quarterly estimated taxes involves several steps. First, contractors must calculate their estimated tax liability for the year, taking into account their projected income and deductions. They then divide this amount by four and submit a payment to the IRS by the 15th of April, June, September, and January. Failure to make these payments on time can result in penalties and interest charges.

In addition to estimated taxes, independent contractors must also pay self-employment taxes. This involves calculating the self-employment tax rate, which is currently 15.3% for 2023, and applying it to their net earnings. Contractors must report their self-employment income and taxes on Schedule SE of their Form 1040 tax return.

One of the complexities of being an independent contractor is the need to keep accurate records of all income and expenses throughout the year. This is crucial for estimating taxes accurately and avoiding underpayment penalties. Contractors should also be aware of the various deductions and credits available to them, such as the home office deduction, business expense deductions, and the Earned Income Tax Credit.

To navigate these complex tax obligations, many independent contractors choose to work with a tax professional or use tax preparation software. These resources can help ensure that contractors are meeting their tax obligations and taking advantage of all available deductions and credits. By staying informed and proactive about their tax responsibilities, independent contractors can minimize their tax liability and avoid costly penalties.

Understanding Pre-Tax Employee Contributions: A Simple Guide

You may want to see also

Explore related products

![]()

Health Insurance: Employees typically receive health insurance through their employer, which can be a significant tax advantage

Employees often receive health insurance as a benefit from their employer, which can offer substantial tax advantages. This perk is typically not available to independent contractors, who must secure their own health coverage. The tax benefits stem from the fact that employer-provided health insurance premiums are generally excluded from the employee's taxable income. This exclusion can significantly reduce an employee's tax liability compared to an independent contractor who must pay for health insurance out of pocket and then deduct the premiums as a business expense.

For employees, the tax advantage of employer-provided health insurance can be particularly valuable. It not only lowers their taxable income but also helps them avoid the complexity of itemizing deductions on their tax return. In contrast, independent contractors must navigate the intricacies of self-employment taxes, including the deduction of health insurance premiums, which can be a more complicated and less straightforward process.

Moreover, employer-sponsored health plans often offer better coverage and lower premiums than individual plans available to independent contractors. This is because employers can negotiate rates with insurance providers based on the collective health needs and risks of their workforce. As a result, employees may enjoy more comprehensive health benefits at a lower cost, further enhancing the tax advantage.

In summary, the tax benefits of employer-provided health insurance can be a significant factor in the overall tax burden of employees versus independent contractors. Employees who receive health insurance through their employer can take advantage of tax exclusions and potentially better coverage, while independent contractors must manage their own health insurance expenses and deductions, which can be both costly and complex.

Maximizing Tax Benefits: Employee FSA Contributions Explained

You may want to see also

Explore related products

![]()

Retirement Savings: Employer-sponsored retirement plans, like 401(k)s, offer tax benefits that independent contractors may not have access to

One significant advantage of being an employee rather than an independent contractor is access to employer-sponsored retirement plans, such as 401(k)s. These plans offer substantial tax benefits that can significantly boost an individual's retirement savings. Contributions to a 401(k) are made pre-tax, reducing the employee's taxable income for the year. This not only lowers their current tax liability but also allows their savings to grow tax-deferred until withdrawal in retirement.

In contrast, independent contractors are responsible for setting up and funding their own retirement accounts, such as Individual Retirement Accounts (IRAs) or Solo 401(k)s. While these options do provide some tax advantages, they are generally less generous than employer-sponsored plans. For instance, the contribution limits for IRAs are lower than those for 401(k)s, and independent contractors may not have access to employer matching contributions, which can substantially increase the amount saved over time.

Furthermore, employer-sponsored retirement plans often come with additional benefits, such as employer matching contributions, which can further enhance an employee's retirement savings. Many employers will match a certain percentage of the employee's contributions, essentially providing free money that can significantly boost the overall savings amount. This benefit is not typically available to independent contractors, who must rely solely on their own contributions to fund their retirement.

Another advantage of employer-sponsored retirement plans is the ease of participation. Employees are often automatically enrolled in these plans, with contributions deducted directly from their paychecks. This makes it simple and convenient to save for retirement without having to take additional steps. Independent contractors, on the other hand, must actively set up and manage their own retirement accounts, which can be time-consuming and require more financial knowledge and discipline.

In summary, employer-sponsored retirement plans offer significant tax benefits and other advantages that independent contractors may not have access to. These benefits can substantially increase an individual's retirement savings, making it easier to achieve financial security in later life. As such, employees may find it easier to save for retirement compared to independent contractors, who must take a more proactive approach to managing their retirement savings.

Understanding PPP Loans: Do They Cover Employee Taxes?

You may want to see also

Frequently asked questions

Taxes can be higher for independent contractors because they are responsible for paying both the employer and employee portions of Social Security and Medicare taxes, which totals 15.3% of their net earnings. Employees only pay half of these taxes, with their employers covering the other half.

Independent contractors may be eligible for a variety of tax deductions that are not available to employees, such as deductions for business expenses, home office use, depreciation of business assets, and health insurance premiums. These deductions can help offset the higher tax rates that independent contractors face.

Independent contractors typically need to file more complex tax forms, such as Schedule C, which details their business income and expenses. They may also need to make estimated tax payments throughout the year. Employees, on the other hand, usually have their taxes withheld from their paychecks and file a simpler Form 1040 at the end of the year.