The question of whether 100% of a Paycheck Protection Program (PPP) loan can be used for payroll is a common one among business owners and financial professionals. The PPP, established by the CARES Act in response to the COVID-19 pandemic, provides forgivable loans to eligible businesses to help cover payroll costs, rent, utilities, and other expenses. While the primary purpose of the PPP is to support payroll, there are specific guidelines and restrictions on how the loan funds can be used to ensure they are allocated appropriately and contribute to the program's goals of job retention and economic stability.

| Characteristics | Values |

|---|---|

| Loan Amount | $100,000 |

| Loan Purpose | Payroll |

| Interest Rate | 1% |

| Loan Term | 2 years |

| Repayment Schedule | Monthly |

| Collateral | None |

| Credit Score | 600+ |

| Business Revenue | $500,000+ |

| Business Age | 2+ years |

| Loan Fees | 2% origination fee |

Explore related products

What You'll Learn

- PPP Loan Basics: Understanding the Paycheck Protection Program and its primary purpose

- Loan Forgiveness Criteria: Exploring the conditions under which PPP loans can be forgiven

- Payroll Definition: Clarifying what constitutes payroll expenses under PPP guidelines

- Maximum Loan Amount: Determining the highest loan amount available for payroll costs

- Application Process: Outlining the steps to apply for a PPP loan for payroll purposes

![]()

PPP Loan Basics: Understanding the Paycheck Protection Program and its primary purpose

The Paycheck Protection Program (PPP) was established as part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act in March 2020. Its primary purpose is to provide financial assistance to small businesses and other eligible entities to help them retain employees and cover certain operational expenses during the COVID-19 pandemic. The PPP offers loans that can be forgiven if the borrower meets specific criteria, primarily related to maintaining payroll and using the loan funds for eligible expenses.

One of the key features of the PPP is that up to 100% of the loan amount can be used for payroll costs, which include salaries, wages, tips, and certain employee benefits. This flexibility is designed to help businesses keep their workforce employed and maintain stability during challenging economic times. In addition to payroll, the PPP loan funds can also be used for other eligible expenses such as rent, mortgage interest, and utilities, but the focus on payroll is a critical aspect of the program's design.

To qualify for a PPP loan, businesses must meet certain eligibility criteria, including having fewer than 500 employees and demonstrating a need for the loan due to the economic impact of the COVID-19 pandemic. The loan amount is calculated based on the borrower's average monthly payroll costs, with a maximum loan amount of $10 million. The interest rate on PPP loans is 1%, and the loans have a maturity of two years.

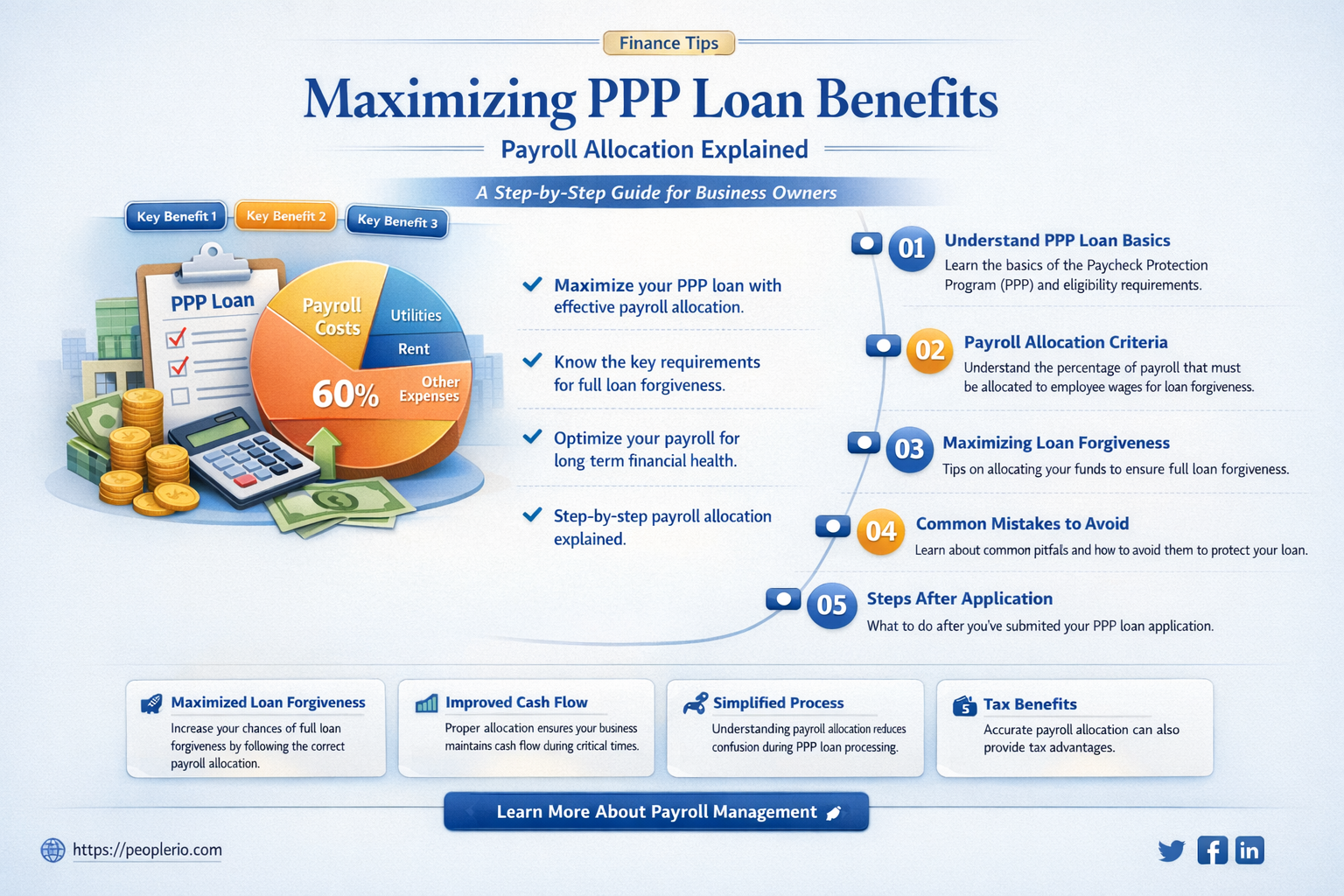

One of the most significant benefits of the PPP is the potential for loan forgiveness. To be eligible for loan forgiveness, borrowers must use at least 60% of the loan funds for payroll costs and the remaining funds for other eligible expenses. They must also maintain their employee headcount and compensation levels during the covered period. If these criteria are met, the borrower can apply for loan forgiveness, and the remaining balance of the loan will be forgiven.

In conclusion, the PPP loan program is a critical tool for small businesses and other eligible entities to maintain their operations and workforce during the COVID-19 pandemic. By providing flexible loan funds that can be used primarily for payroll costs and offering the potential for loan forgiveness, the PPP aims to support businesses in retaining their employees and weathering the economic challenges posed by the pandemic.

How to Locate Your W2 on Paylocity: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Loan Forgiveness Criteria: Exploring the conditions under which PPP loans can be forgiven

To qualify for full forgiveness of a PPP loan, businesses must meet several specific criteria. Firstly, the loan funds must be used for eligible expenses, which include payroll costs, rent, mortgage interest, or utilities. The definition of payroll costs is quite broad and includes salaries, wages, tips, commissions, benefits, and even certain contractor payments. However, it's important to note that not all expenses are eligible for forgiveness, such as bonuses or severance pay.

Secondly, businesses must maintain their employee headcount and compensation levels. This means that the number of full-time equivalent employees on the payroll must remain the same or increase from the reference period, which is typically February 2020. Additionally, employee compensation, including salaries and benefits, must not be reduced by more than 25% compared to the reference period.

Thirdly, businesses must use at least 60% of the loan funds for payroll costs. This is a key requirement, as it ensures that the majority of the loan is being used to support employees. The remaining 40% can be used for other eligible expenses, such as rent or utilities.

Fourthly, businesses must apply for loan forgiveness within the specified timeframe. The application process typically involves submitting documentation to the lender, such as payroll records, rent invoices, and utility bills. The lender will then review the application and determine whether the business meets the forgiveness criteria.

Finally, it's important to be aware of any additional requirements or restrictions that may apply. For example, businesses that have received other forms of government assistance, such as Economic Injury Disaster Loans (EIDLs), may have different forgiveness criteria to meet. Additionally, businesses that have experienced a change in ownership or structure may need to provide additional documentation to support their forgiveness application.

In conclusion, while PPP loans can provide valuable financial support to businesses, it's crucial to understand and meet the specific forgiveness criteria to avoid having to repay the loan. By carefully following the guidelines and maintaining accurate records, businesses can increase their chances of successfully obtaining loan forgiveness.

Can LLC Owners Be on Payroll? Exploring the Legalities and Benefits

You may want to see also

Explore related products

![]()

Payroll Definition: Clarifying what constitutes payroll expenses under PPP guidelines

The Paycheck Protection Program (PPP) guidelines define payroll expenses broadly to include various components of employee compensation. This encompasses not only salaries and wages but also benefits such as health insurance premiums, retirement contributions, and paid leave. Understanding this definition is crucial for businesses to ensure they are correctly allocating their PPP loan funds.

One common misconception is that payroll expenses are limited to direct cash payments to employees. However, the PPP guidelines extend this to include indirect costs associated with employee compensation. For instance, employer contributions to 401(k) plans, unemployment insurance, and social security taxes are all considered payroll expenses under the PPP. This comprehensive definition aims to support businesses in maintaining their workforce during challenging economic times.

To illustrate, let's consider an example: A small business with 10 employees might calculate its payroll expenses as follows. Salaries and wages total $50,000 per month. Additionally, the employer spends $5,000 on health insurance premiums, $3,000 on retirement contributions, and $2,000 on paid leave. Under the PPP guidelines, the total monthly payroll expense would be $60,000, encompassing both direct and indirect costs.

It's important to note that while the PPP loan can cover up to 100% of payroll expenses, there are caps and limitations in place. For instance, the maximum loan amount is $10 million, and the loan term is typically two years. Businesses must also meet certain eligibility criteria and demonstrate the need for the loan due to the impact of the COVID-19 pandemic.

In conclusion, the PPP guidelines provide a broad definition of payroll expenses to support businesses in retaining their employees. By understanding this definition and the associated guidelines, businesses can effectively utilize their PPP loan funds to navigate through economic challenges.

DIY Payroll: A Step-by-Step Guide to Managing Your Finances for Free

You may want to see also

![]()

Maximum Loan Amount: Determining the highest loan amount available for payroll costs

To determine the maximum loan amount available for payroll costs under the Paycheck Protection Program (PPP), businesses must first understand the calculation methodology. The PPP loan amount is based on the average monthly payroll costs incurred during the 12 months prior to the loan application date, multiplied by 2.5. This calculation is subject to a maximum loan amount of $10 million.

However, it's crucial to note that not all businesses will qualify for the full $10 million. The actual loan amount will depend on the specific payroll costs of the business, including salaries, wages, tips, and certain benefits such as health insurance and retirement contributions. Businesses with higher average monthly payroll costs will naturally qualify for larger loan amounts, up to the $10 million cap.

For businesses that have been operational for less than 12 months, the loan amount is calculated based on the average monthly payroll costs during the period the business has been operational. Additionally, seasonal businesses may use a 12-month average from the previous year to account for fluctuations in payroll costs throughout the year.

It's also important to consider that the PPP loan amount may be reduced if the business has received other forms of government assistance, such as Economic Injury Disaster Loans (EIDLs) or Small Business Administration (SBA) loans. The total loan amount from all sources cannot exceed the maximum PPP loan amount of $10 million.

In conclusion, while the maximum PPP loan amount for payroll costs is $10 million, the actual loan amount a business can receive will depend on its specific payroll costs and other factors. Businesses should carefully review the PPP guidelines and consult with a financial advisor or lender to determine the maximum loan amount they can qualify for.

DIY Payroll: Can You Handle It Yourself? Pros and Cons

You may want to see also

![]()

Application Process: Outlining the steps to apply for a PPP loan for payroll purposes

To apply for a PPP loan specifically for payroll purposes, businesses must follow a structured application process. This begins with gathering necessary documentation, such as payroll records, tax filings, and proof of business operation. The next step involves calculating the maximum loan amount eligible for, which is typically based on the average monthly payroll costs multiplied by a certain factor, often 2.5. It's crucial to ensure accuracy in these calculations to avoid delays or rejections.

Once the preliminary steps are completed, the business must find an approved PPP lender. This can be a bank, credit union, or other financial institution participating in the PPP program. The lender will provide the specific application forms and guide the business through the submission process. It's important to note that lenders may have additional requirements or criteria, so businesses should be prepared to provide any requested information promptly.

After submitting the application, the business will need to wait for the lender to review and approve the loan. This process can take several weeks, during which the business may need to provide further documentation or clarification. Upon approval, the loan funds will be disbursed, and the business can begin using them for eligible payroll expenses. It's essential to keep detailed records of how the loan funds are used, as this will be necessary for loan forgiveness applications and potential audits.

Throughout the application process, businesses should stay informed about any updates or changes to the PPP program. This includes monitoring guidance from the Small Business Administration (SBA) and the Treasury Department, as well as staying in touch with the lender for any specific instructions or requirements. By following these steps and staying vigilant, businesses can successfully navigate the PPP loan application process and secure the funds needed to support their payroll during challenging times.

Maximizing Your Roth 401(k) Contributions Beyond Payroll Deductions

You may want to see also

Frequently asked questions

Yes, 100% of a PPP loan can be used for payroll costs, including salaries, wages, tips, and benefits.

Eligible payroll costs include salaries, wages, tips, and benefits such as health insurance premiums and retirement contributions.

There are no specific restrictions on how the PPP loan funds can be used for payroll, as long as the costs are eligible and documented.

Yes, PPP loan funds can be used for other business expenses such as rent, utilities, and interest on mortgages, in addition to payroll costs.

The maximum amount of a PPP loan that can be used for payroll is 2.5 times the average monthly payroll cost, up to a maximum of $10 million.