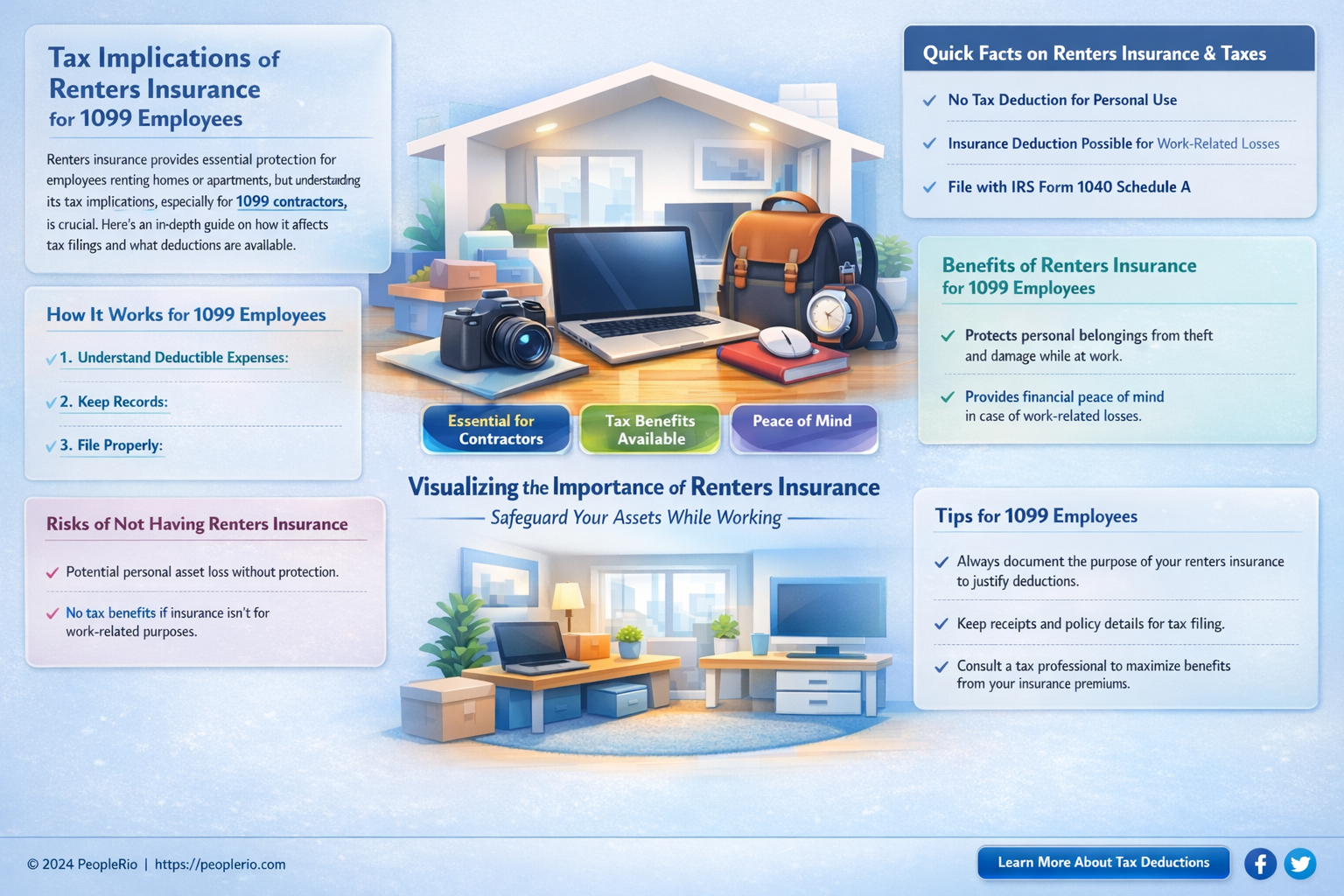

The topic of whether a 10-99 employee can tax renters insurance is an important one for independent contractors and freelancers. As a 10-99 employee, you are considered self-employed and are responsible for paying your own taxes, including self-employment tax. This means that you may be able to deduct certain business expenses, including renters insurance, on your tax return. However, there are specific rules and requirements that must be met in order to qualify for these deductions. In this paragraph, we will explore the ins and outs of taxing renters insurance as a 10-99 employee, including the criteria that must be met and the potential benefits of doing so.

Explore related products

What You'll Learn

- Eligibility: Determine if a 10-99 employee qualifies for renters insurance tax deductions

- Tax Benefits: Explore potential tax benefits available for renters insurance premiums paid by 10-99 employees

- Documentation: Understand the necessary documentation required to claim renters insurance expenses on tax returns for 10-99 employees

- State Regulations: Review state-specific regulations regarding renters insurance and tax implications for 10-99 employees

- Comparison: Compare different renters insurance policies and their tax advantages for 10-99 employees

![]()

Eligibility: Determine if a 10-99 employee qualifies for renters insurance tax deductions

To determine if a 10-99 employee qualifies for renters insurance tax deductions, we need to examine the specific criteria set by the IRS. First, it's essential to understand that 10-99 employees are considered independent contractors, and as such, they are responsible for their own taxes, including self-employment tax. This distinction is crucial because it affects how they can claim deductions.

One of the primary requirements for claiming renters insurance tax deductions is that the insurance policy must cover the employee's business property. This means that the policy should specifically list the business equipment, tools, or inventory that are being insured. Additionally, the employee must be able to prove that the rental property is used for business purposes. This can be done by providing documentation such as a lease agreement, utility bills, or a letter from the landlord confirming the business use of the property.

Another important factor to consider is the percentage of the rental property that is used for business purposes. If only a portion of the property is used for business, then the employee can only claim a deduction for that portion of the renters insurance premium. For example, if 50% of the rental property is used for business, then the employee can claim a deduction for 50% of the renters insurance premium.

It's also worth noting that the IRS has specific rules regarding the types of expenses that can be deducted. For instance, the employee cannot claim a deduction for personal expenses, such as rent or utilities, unless they are directly related to the business use of the property. Furthermore, the employee must be able to substantiate all expenses with receipts or other documentation.

In conclusion, determining if a 10-99 employee qualifies for renters insurance tax deductions requires a careful examination of the specific criteria set by the IRS. The employee must be able to prove that the rental property is used for business purposes, that the insurance policy covers business property, and that they have substantiated all expenses with proper documentation. By following these guidelines, 10-99 employees can ensure that they are taking advantage of all available tax deductions.

Unlocking Tax Benefits: The Scoop on Employee Super Contributions

You may want to see also

Explore related products

![]()

Tax Benefits: Explore potential tax benefits available for renters insurance premiums paid by 10-99 employees

As a 10-99 employee, you may be eligible for certain tax benefits related to your renters insurance premiums. One potential benefit is the ability to deduct your premiums from your taxable income. This can help reduce your overall tax liability and put more money back in your pocket. To qualify for this deduction, you must itemize your deductions on your tax return and ensure that your premiums are not already being reimbursed by your employer.

Another tax benefit to consider is the possibility of deducting your renters insurance premiums as a business expense. If you use part of your rented space for business purposes, you may be able to deduct a portion of your premiums as a business expense on your tax return. This can help offset the cost of your insurance and reduce your taxable income. To qualify for this deduction, you must be able to demonstrate that you use part of your rented space regularly and exclusively for business purposes.

Additionally, some states offer tax credits or deductions specifically for renters insurance premiums. These state-specific benefits can vary, so it's important to research the tax laws in your state to see if you qualify for any additional benefits. To take advantage of these state-specific benefits, you may need to file additional forms or provide documentation of your insurance coverage.

When exploring potential tax benefits for your renters insurance premiums, it's important to keep accurate records of your payments and any relevant documentation. This can help you substantiate your deductions and credits when filing your tax return. Additionally, consulting with a tax professional can help you navigate the complex tax laws and ensure that you're taking advantage of all the benefits available to you as a 10-99 employee.

In summary, as a 10-99 employee, you may be eligible for various tax benefits related to your renters insurance premiums. These benefits can include deductions from your taxable income, business expense deductions, and state-specific tax credits or deductions. By keeping accurate records and consulting with a tax professional, you can maximize your tax savings and ensure that you're taking advantage of all the benefits available to you.

Comparing Employee State Taxes: South Carolina vs. Maryland

You may want to see also

Explore related products

![]()

Documentation: Understand the necessary documentation required to claim renters insurance expenses on tax returns for 10-99 employees

To claim renters insurance expenses on tax returns for 10-99 employees, it is essential to understand the necessary documentation required. This includes maintaining accurate records of the insurance premiums paid, as well as any claims made during the policy period. Additionally, employees should keep track of any receipts or invoices related to the rental property, such as rent payments, utility bills, and maintenance costs. These documents will help substantiate the expenses claimed on the tax return and ensure compliance with IRS regulations.

One important aspect to consider is the distinction between personal and business use of the rental property. If the property is used for both personal and business purposes, the expenses must be allocated accordingly. This can be done by calculating the percentage of time the property is used for business purposes and applying that percentage to the total expenses incurred. It is crucial to maintain clear and separate records for personal and business use to avoid any confusion or discrepancies during the tax filing process.

Furthermore, it is recommended to consult with a tax professional or accountant to ensure that all necessary documentation is properly organized and submitted. They can provide guidance on the specific requirements for claiming renters insurance expenses and help identify any potential deductions or credits that may be available. By working with a tax expert, 10-99 employees can maximize their tax savings while minimizing the risk of errors or omissions on their tax returns.

In summary, understanding the documentation requirements for claiming renters insurance expenses on tax returns for 10-99 employees is crucial for compliance and maximizing tax savings. By maintaining accurate records, distinguishing between personal and business use, and consulting with a tax professional, employees can navigate the tax filing process with confidence and efficiency.

Unlocking Tax Benefits: A Guide to Employee Event Deductions

You may want to see also

Explore related products

![]()

State Regulations: Review state-specific regulations regarding renters insurance and tax implications for 10-99 employees

Navigating the complex landscape of state regulations regarding renters insurance and tax implications for 10-99 employees requires a keen understanding of the nuances in different state laws. Each state has its own set of rules and guidelines that govern how renters insurance can be taxed and what deductions are permissible for independent contractors. For instance, in California, renters insurance premiums are generally not tax-deductible for 10-99 employees, whereas in New York, they may be deductible if the employee uses the space for business purposes.

To ensure compliance and optimize tax benefits, 10-99 employees must be aware of the specific regulations in their state. This involves researching state tax codes, consulting with tax professionals, and keeping meticulous records of insurance premiums and business-related expenses. Failure to adhere to state regulations can result in penalties, fines, or even legal action, making it crucial for independent contractors to stay informed and proactive in managing their tax obligations.

One effective strategy for 10-99 employees is to work closely with a tax advisor who specializes in state tax laws. This professional can provide tailored guidance on how to navigate the intricacies of state regulations, identify potential deductions, and ensure that all necessary documentation is in order. Additionally, employees should consider bundling their renters insurance with other business-related insurance policies, as this may offer cost savings and simplify the tax deduction process.

In conclusion, understanding and complying with state regulations regarding renters insurance and tax implications is essential for 10-99 employees. By staying informed, seeking professional advice, and maintaining accurate records, independent contractors can minimize their tax liabilities and avoid potential legal issues.

Understanding Withholding Allowances: A Guide to Employee Tax Implications

You may want to see also

Explore related products

![]()

Comparison: Compare different renters insurance policies and their tax advantages for 10-99 employees

When comparing different renters insurance policies for 10-99 employees, it's crucial to consider the tax advantages each policy offers. This can be a complex task, as various factors influence the tax benefits, such as the type of policy, the coverage limits, and the specific needs of the business. To make an informed decision, it's essential to understand the different types of renters insurance policies available and how they can impact your business's tax situation.

One type of renters insurance policy is the Business Owners Policy (BOP), which typically covers property damage, liability, and business interruption. A BOP can offer tax advantages by allowing businesses to deduct the premiums as a business expense. However, it's important to note that the tax benefits may vary depending on the specific terms of the policy and the business's tax situation.

Another option is the General Liability Insurance policy, which provides coverage for bodily injury, property damage, and personal injury claims. While this type of policy may not offer the same tax advantages as a BOP, it can still be beneficial for businesses with 10-99 employees. For example, if an employee accidentally damages a rented property, the General Liability Insurance policy can help cover the costs, which can be tax-deductible as a business expense.

When comparing policies, it's also important to consider the coverage limits and how they may impact your business's tax situation. For instance, if a policy has a low coverage limit, it may not provide adequate protection for your business, which could lead to financial losses that are not tax-deductible. On the other hand, a policy with a high coverage limit may offer more protection, but it could also result in higher premiums, which may not be fully tax-deductible.

To make the most informed decision, it's recommended to consult with a tax professional or an insurance agent who specializes in business insurance. They can help you understand the tax implications of different renters insurance policies and how they can impact your business's bottom line. By taking the time to compare policies and consider the tax advantages, you can make a smart decision that will protect your business and maximize your tax benefits.

Maximizing Tax Benefits: Employee Contributions to Simple Plans

You may want to see also