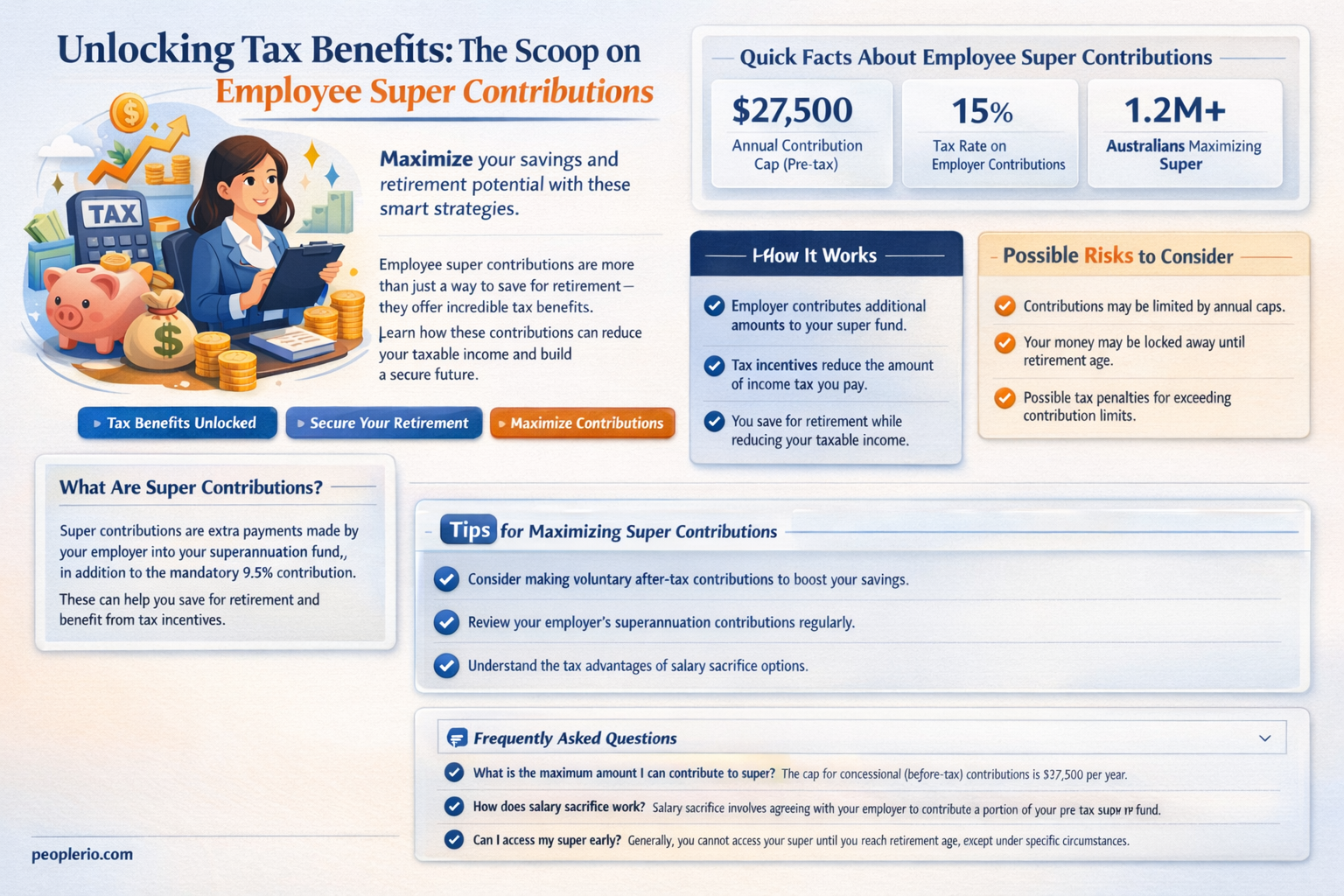

Employee super contributions refer to the additional amounts that employees choose to contribute to their superannuation funds beyond the minimum required by law. These contributions are often made through salary sacrifice arrangements, where employees elect to have a portion of their pre-tax salary directed into their super fund. The tax deductibility of these contributions can have significant implications for both employees and employers. In general, employee super contributions are tax deductible, but there are certain conditions and limits that apply. For instance, the contributions must be made to a complying super fund, and there may be caps on the amount that can be contributed each year. Additionally, the tax benefits may vary depending on the individual's income level and other factors. Employers may also need to consider their obligations in relation to employee super contributions, such as ensuring that the contributions are properly recorded and reported. Overall, understanding the tax implications of employee super contributions is crucial for making informed decisions about retirement savings and financial planning.

Explore related products

What You'll Learn

- Eligibility Criteria: Understand who qualifies for tax deductions on employee super contributions

- Contribution Limits: Explore the maximum allowable contributions that can be deducted

- Tax Benefits: Discover how these contributions reduce taxable income and overall tax liability

- Documentation Requirements: Learn what records are necessary to claim these deductions

- Common Mistakes: Avoid frequent errors that could lead to disallowed deductions or penalties

![]()

Eligibility Criteria: Understand who qualifies for tax deductions on employee super contributions

To qualify for tax deductions on employee super contributions, certain eligibility criteria must be met. These criteria are designed to ensure that only those who are genuinely contributing to their retirement savings and are in a position to benefit from such deductions are able to claim them. Understanding these criteria is crucial for both employees and employers to navigate the complexities of superannuation tax benefits effectively.

One of the primary eligibility criteria is that the employee must be making concessional contributions to a complying super fund. Concessional contributions are those made from pre-tax income, and they are subject to a lower tax rate than non-concessional contributions. This encourages employees to save for their retirement by providing a tax advantage. Additionally, the employee must not have exceeded the concessional contributions cap, which is the maximum amount that can be contributed to a super fund in a given financial year. Exceeding this cap can result in additional tax liabilities.

Another important criterion is that the employee must not be in a position to claim a tax deduction for their super contributions if they are receiving a super pension or annuity. This is because the tax deduction is intended to incentivize saving for retirement, not to provide a tax benefit for those who are already drawing on their super savings. Furthermore, employees who are self-employed or who are members of a defined benefit super fund may have different eligibility criteria to meet, depending on their specific circumstances.

Employers also play a role in ensuring that employees meet the eligibility criteria for tax deductions on super contributions. They are responsible for making concessional contributions on behalf of their employees and for ensuring that these contributions are made to a complying super fund. Employers must also keep accurate records of all super contributions made, as these records will be necessary for employees to claim their tax deductions.

In conclusion, understanding the eligibility criteria for tax deductions on employee super contributions is essential for both employees and employers. By meeting these criteria, employees can take advantage of the tax benefits available to them, while employers can help their employees save for their retirement and comply with their superannuation obligations.

Tax-Free Employee Gifts: What Employers Need to Know

You may want to see also

Explore related products

![]()

Contribution Limits: Explore the maximum allowable contributions that can be deducted

The maximum allowable contributions that can be deducted for tax purposes are a critical aspect of employee super contributions. In Australia, for instance, the concessional contributions cap is set at $27,500 per financial year for individuals under 50 years of age. This limit includes both employer and employee contributions. For those aged 50 and over, the cap is increased to $35,000 per year. It's essential to note that exceeding these limits can result in additional tax liabilities.

To maximize tax deductions, employees should be aware of the contribution limits and plan their super contributions accordingly. One strategy could be to contribute up to the concessional cap each year to take full advantage of the tax benefits. Additionally, employees may consider making non-concessional contributions, which, while not tax-deductible, can still help boost retirement savings.

It's also important to consider the impact of other factors, such as salary sacrifice arrangements and employer contributions, on the overall contribution limits. Salary sacrifice contributions are counted towards the concessional cap, while employer contributions are not. Understanding these nuances can help employees optimize their super contributions and minimize tax liabilities.

In summary, staying within the contribution limits is crucial for maximizing tax deductions on employee super contributions. By planning contributions carefully and considering the impact of other factors, employees can make the most of their retirement savings while minimizing tax liabilities.

Understanding Employee Stock Options: Tax Implications and Strategies

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![]()

Tax Benefits: Discover how these contributions reduce taxable income and overall tax liability

Employee super contributions can significantly reduce taxable income and overall tax liability. When an employee makes a super contribution, it is generally deducted from their gross income before tax is calculated. This means that the amount contributed is not subject to income tax, which can result in a lower tax bill. For example, if an employee earns $80,000 per year and makes a super contribution of $10,000, their taxable income would be reduced to $70,000. This could potentially lower their tax liability by thousands of dollars, depending on their marginal tax rate.

The tax benefits of employee super contributions are particularly valuable for high-income earners. As the marginal tax rate increases with income, making super contributions can be an effective way to reduce the amount of tax owed. For instance, an individual earning $150,000 per year could save up to $45,000 in tax by making the maximum allowable super contribution. This is because the super contribution is deducted from their gross income, reducing the amount subject to the highest tax rate.

It is important to note that there are limits to the amount of super contributions that can be made each year. Exceeding these limits can result in additional tax liabilities and penalties. Therefore, it is crucial for employees to be aware of the current super contribution caps and to plan their contributions accordingly. Additionally, the tax benefits of super contributions may change over time due to legislative updates, so it is essential for employees to stay informed about any changes that could impact their tax situation.

In summary, employee super contributions can be a powerful tool for reducing taxable income and overall tax liability. By making regular super contributions, employees can potentially save thousands of dollars in tax each year. However, it is important to be aware of the contribution limits and to stay informed about any changes to the tax laws that could affect the benefits of super contributions.

Understanding Pension Contributions: Pre-Tax or Post-Tax Deductions?

You may want to see also

Explore related products

![]()

Documentation Requirements: Learn what records are necessary to claim these deductions

To claim tax deductions for employee super contributions, it is essential to maintain accurate and comprehensive documentation. This includes keeping records of all contributions made by both the employer and the employee, as well as any relevant correspondence with the super fund.

One of the key documents required is the Superannuation Guarantee (SG) statement, which is issued by the super fund annually. This statement provides a detailed breakdown of the contributions made to the employee's super account, including the amount of SG contributions made by the employer. It is important to review this statement carefully to ensure that all contributions are correctly recorded and that the employer is meeting their SG obligations.

In addition to the SG statement, employers should also keep records of any salary sacrifice contributions made by the employee. This includes maintaining copies of any relevant agreements or arrangements between the employer and the employee, as well as records of the actual contributions made.

It is also important to keep records of any correspondence with the super fund, including emails, letters, and phone calls. This can help to resolve any issues or disputes that may arise in relation to the super contributions.

Finally, employers should ensure that they have a system in place to track and record all super contributions on an ongoing basis. This can help to identify any potential issues or discrepancies early on, and ensure that the employer is able to claim the maximum tax deductions available.

Navigating Employee Health Insurance Premiums: A Business Tax Perspective

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![]()

Common Mistakes: Avoid frequent errors that could lead to disallowed deductions or penalties

One common mistake that could lead to disallowed deductions or penalties is failing to properly document employee super contributions. It is essential to keep accurate records of all contributions, including the amount, date, and method of payment. This documentation will be necessary to substantiate any deductions claimed on tax returns.

Another frequent error is misclassifying employee super contributions as wages or salaries. This can result in incorrect tax withholding and reporting, potentially leading to penalties and interest charges. It is important to correctly categorize these contributions as fringe benefits or retirement plan contributions, depending on the specific circumstances.

Additionally, some employers may make the mistake of not complying with the relevant tax laws and regulations governing employee super contributions. This can include failing to register for the appropriate tax accounts, not filing required reports, or not paying the correct amount of tax on time. To avoid these errors, it is crucial to stay up-to-date with the latest tax laws and seek professional advice if necessary.

Furthermore, employers should be cautious about making excessive contributions to employee super funds, as this can trigger additional tax liabilities. There are limits on the amount of tax-deductible contributions that can be made each year, and exceeding these limits can result in penalties and disallowed deductions.

To avoid these common mistakes, employers should implement a comprehensive record-keeping system, ensure proper classification of employee super contributions, comply with all relevant tax laws and regulations, and seek professional advice when needed. By taking these steps, employers can minimize the risk of disallowed deductions or penalties and ensure that their employee super contribution practices are in line with the law.

Essential Tax Forms for Employees: A Comprehensive Guide

You may want to see also

Frequently asked questions

Yes, employee super contributions are generally tax deductible. This means that the amount you contribute to your superannuation fund from your pre-tax income can be claimed as a tax deduction, reducing your taxable income.

The maximum amount you can contribute to your superannuation fund per year is known as the concessional contributions cap. As of 2023, this cap is $27,500. Contributions above this cap may be subject to additional tax.

To claim a tax deduction for your employee super contributions, you need to complete a tax return and include the amount of your contributions in the relevant section. You will also need to provide evidence of your contributions, such as a statement from your superannuation fund.