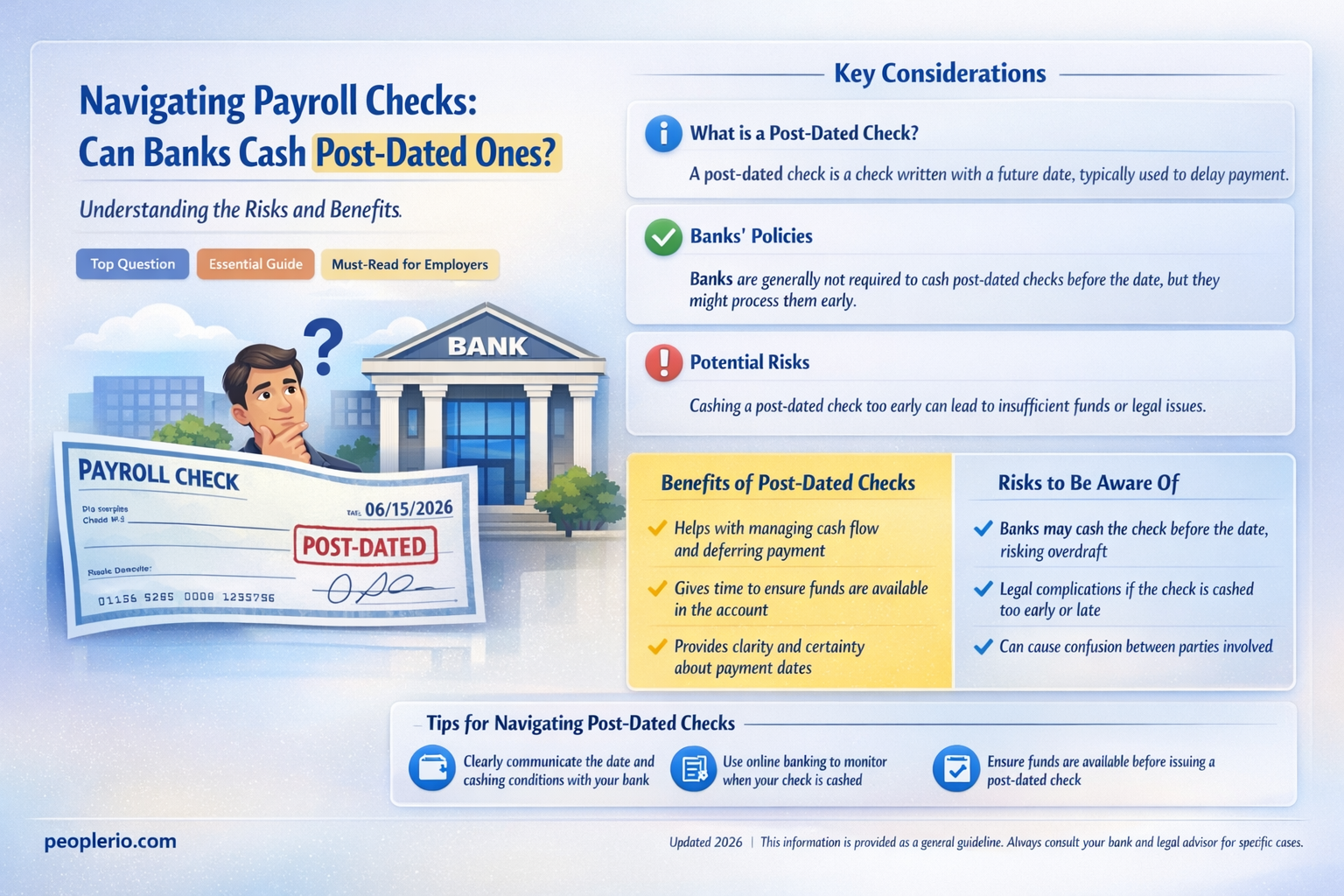

A post-dated payroll check is a check that is issued with a future date, rather than the current date. This can be done for a variety of reasons, such as to ensure that the check is not cashed until after a certain date, or to give the employer time to ensure that the funds are available in their account. However, it is important to note that banks are not required to honor post-dated checks, and they may choose to cash them immediately. This can lead to problems if the employer does not have sufficient funds in their account to cover the check. In some cases, banks may agree to hold the check until the date on it, but this is not always the case. It is important for employers to be aware of their bank's policies regarding post-dated checks, and to ensure that they have sufficient funds in their account to cover any checks that they issue.

| Characteristics | Values |

|---|---|

| Check Type | Payroll check |

| Date | Post-dated |

| Cashing Entity | Bank |

| Legal Considerations | Subject to banking regulations and laws regarding post-dated checks |

| Processing Time | May vary depending on bank policies and check amount |

| Fees | Possible fees for early cashing or processing |

| Requirements | Valid identification and account verification |

| Alternatives | Electronic payroll deposits, prepaid cards |

Explore related products

What You'll Learn

- Definition of a Post-Dated Check: Explaining what a post-dated check is and its common uses

- Bank Policies on Post-Dated Checks: Discussing typical bank policies regarding the cashing of post-dated checks

- Legal Considerations: Outlining the legal aspects and implications of cashing a post-dated check

- Alternatives to Cashing: Suggesting alternative methods for handling post-dated checks besides cashing them

- Potential Issues and Risks: Highlighting possible problems and risks associated with cashing post-dated checks

![]()

Definition of a Post-Dated Check: Explaining what a post-dated check is and its common uses

A post-dated check is a check that bears a date later than the current date. It is a financial instrument used to delay the payment until a specified future date. This type of check is commonly used in various scenarios, such as payroll checks, rent payments, or installment payments for goods and services.

One of the primary reasons for using a post-dated check is to ensure that the payment is processed on a specific date, which can be beneficial for both the payer and the payee. For instance, an employer may issue post-dated payroll checks to employees to ensure that the funds are available in the company's account before the checks are cashed. Similarly, a landlord may accept a post-dated check for rent to guarantee that the payment will be received on time.

It is important to note that banks are not obligated to honor post-dated checks before the date specified on the check. In fact, many banks have policies in place that prohibit the cashing of post-dated checks before the indicated date. This is to prevent potential fraud and to ensure that the funds are available in the payer's account when the check is presented for payment.

However, some banks may choose to cash a post-dated check before the specified date if the customer requests it and if the bank has sufficient funds in the payer's account. In such cases, the bank may charge a fee for the early cashing of the check. It is advisable for individuals who receive post-dated checks to verify the bank's policy regarding the cashing of such checks before attempting to cash them.

In conclusion, a post-dated check is a useful financial tool that allows for the delay of payment until a specified future date. It is commonly used in various scenarios, such as payroll checks and rent payments, to ensure that the payment is processed on time. While banks are not obligated to honor post-dated checks before the specified date, some may choose to do so under certain conditions.

Do Payroll Clerks Verify Employee Timecards? An In-Depth Look

You may want to see also

Explore related products

![]()

Bank Policies on Post-Dated Checks: Discussing typical bank policies regarding the cashing of post-dated checks

Banks generally have specific policies in place regarding the cashing of post-dated checks. These policies are designed to protect both the bank and its customers from potential fraud and financial losses. Typically, a bank will not cash a post-dated check until the date specified on the check has passed. This is to ensure that the funds are available in the account and that the check is not being cashed prematurely.

However, there are some exceptions to this rule. For example, if a customer has a history of depositing post-dated checks and then attempting to cash them early, the bank may choose to place a hold on the funds until the date on the check has passed. Additionally, if a check is post-dated by a significant amount of time, the bank may require additional verification from the account holder before cashing it.

It's also important to note that banks may charge fees for cashing post-dated checks. These fees can vary depending on the bank and the specific circumstances of the check. Customers should always check with their bank to understand their policies and fees regarding post-dated checks.

In the case of payroll checks, banks may have slightly different policies. Since payroll checks are typically issued on a regular basis and are expected to be cashed shortly after issuance, banks may be more lenient when it comes to cashing post-dated payroll checks. However, it's still important for customers to check with their bank to understand their specific policies and procedures.

Overall, it's crucial for customers to be aware of their bank's policies regarding post-dated checks to avoid any potential issues or fees. By understanding these policies, customers can ensure that they are able to cash their checks smoothly and without any complications.

Understanding Payroll Checks: Are They a Liability?

You may want to see also

Explore related products

![]()

Legal Considerations: Outlining the legal aspects and implications of cashing a post-dated check

Cashing a post-dated check involves several legal considerations that both the bank and the customer must be aware of. Firstly, it's important to understand that a post-dated check is not legally binding until the date specified on the check. This means that if a customer attempts to cash a post-dated check before the indicated date, the bank is not obligated to honor it. In fact, doing so could potentially lead to legal repercussions for the bank, as it would be considered a breach of the contractual agreement between the bank and the check issuer.

From the customer's perspective, cashing a post-dated check prematurely could also have legal implications. If the check is cashed before the date and the issuer does not have sufficient funds in their account, the customer could be held liable for any damages or losses incurred by the issuer. Additionally, if the customer knowingly cashes a post-dated check before the date, they could be accused of fraud, which is a serious legal offense.

Another legal consideration is the Uniform Commercial Code (UCC), which governs the laws surrounding negotiable instruments like checks. According to the UCC, a bank is not required to honor a post-dated check until the date specified on the check. However, if the bank chooses to honor the check before the date, it must do so in good faith and without knowledge of any potential fraud or misrepresentation.

In some cases, banks may have their own policies and procedures in place for handling post-dated checks. These policies may include waiting a certain number of days before cashing the check, or requiring additional verification from the check issuer before honoring the check. Customers should be aware of their bank's policies regarding post-dated checks to avoid any potential legal issues.

Finally, it's worth noting that the legal implications of cashing a post-dated check can vary depending on the jurisdiction. Some states may have specific laws or regulations governing the cashing of post-dated checks, so it's important for both banks and customers to be familiar with the laws in their particular state.

In conclusion, cashing a post-dated check involves several legal considerations that both banks and customers must be aware of. Understanding these legal implications can help prevent potential issues and ensure that all parties involved are protected under the law.

Mastering Payroll: A Step-by-Step Guide to Calculating Your Check

You may want to see also

Explore related products

![]()

Alternatives to Cashing: Suggesting alternative methods for handling post-dated checks besides cashing them

If you're considering alternatives to cashing a post-dated check, one viable option is to deposit the check into your bank account. This method allows you to access the funds once the check's date has passed, without the need for physical cash. Many banks offer mobile deposit services, enabling you to deposit checks remotely using your smartphone. This can be particularly useful if you're unable to visit a bank branch in person.

Another alternative is to use a check cashing app. These apps allow you to cash checks using your mobile device, often for a small fee. The funds are typically deposited directly into your bank account or onto a prepaid debit card. This option can be convenient, especially if you need access to the funds quickly.

For those who prefer a more traditional approach, you could consider opening a savings account specifically for post-dated checks. This dedicated account can help you keep track of your pending funds and ensure that you have a separate reserve for future expenses.

In some cases, it may be possible to negotiate with the issuer of the post-dated check to see if they can provide an alternative form of payment, such as a money order or a cashier's check. This can be beneficial if you need immediate access to the funds and are unable to wait for the check's date to pass.

Lastly, if you're receiving post-dated checks regularly, you might want to consider setting up a system to track and manage these checks. This could involve using a spreadsheet or a specialized app to keep record of the check's date, amount, and issuer. By staying organized, you can better plan your finances and ensure that you're prepared when the checks become available for cashing.

Cashing Payroll Checks at CVS: A Convenient Option for Employees

You may want to see also

Explore related products

![]()

Potential Issues and Risks: Highlighting possible problems and risks associated with cashing post-dated checks

Cashing post-dated checks can present several potential issues and risks for both the individual and the bank. One primary concern is the possibility of the check being returned due to insufficient funds. If the account holder does not have enough money in their account on the date the check is presented, the bank may return the check, resulting in fees for the account holder and potential delays in payment for the recipient.

Another risk associated with cashing post-dated checks is the potential for fraud. If a check is stolen or forged, the thief may attempt to cash it before the actual date, leading to financial losses for the account holder and the bank. Additionally, if the account holder disputes the check, claiming it was unauthorized or fraudulent, the bank may be held liable for any losses incurred.

Furthermore, cashing post-dated checks can also lead to complications in accounting and record-keeping. For businesses, accurately tracking and recording post-dated checks can be challenging, especially if the checks are for payroll. This can result in errors in financial statements and potentially lead to audits or other financial issues.

To mitigate these risks, it is essential for individuals and businesses to carefully manage their finances and ensure that they have sufficient funds in their accounts to cover post-dated checks. Banks can also implement policies and procedures to verify the authenticity of checks and to prevent fraud. Additionally, using electronic payment methods, such as direct deposit, can reduce the risks associated with cashing post-dated checks.

Understanding Payroll Checks: Are Deductions Mandatory?

You may want to see also

Frequently asked questions

Generally, banks will not cash a post-dated check before the date indicated on the check. This is because the check is not considered valid until the date it is written for. However, some banks may have specific policies or exceptions, so it's best to check with your bank directly.

If a post-dated payroll check is deposited before the date on the check, the bank may hold the check until the date it is written for. This means that the funds will not be available for withdrawal until the check clears on the specified date.

Cashing a post-dated payroll check early can potentially have legal implications. It may be considered fraud or misrepresentation, as the check is not valid until the date it is written for. It's important to follow the proper procedures and guidelines set by your bank and the laws in your jurisdiction.

Employers can ensure that post-dated payroll checks are handled correctly by clearly communicating with their employees and the bank. They should inform employees about the post-dating policy and the date the checks will be valid. Employers should also verify with their bank that the checks will not be cashed or deposited before the specified date.

Some alternatives to post-dated payroll checks include direct deposit, electronic funds transfer (EFT), or using a payroll card. These methods can provide more flexibility and control over when employees receive their pay, and can also reduce the risk of fraud or misrepresentation associated with post-dated checks.