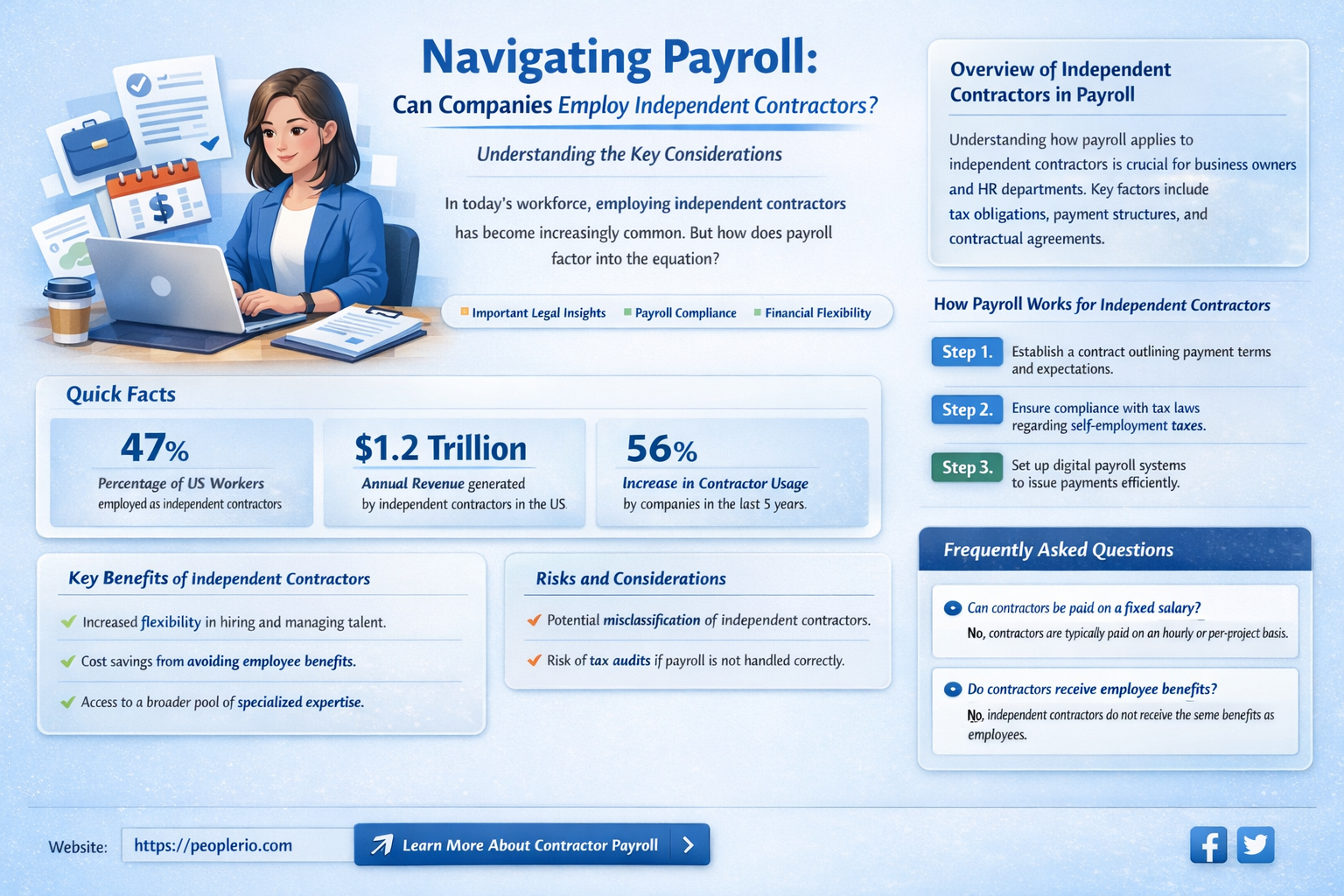

The question of whether a company can have an independent contractor on payroll is a complex one, often leading to confusion among business owners and HR professionals. In general, independent contractors are not considered employees and are therefore not typically included on a company's payroll. Instead, they are usually paid as vendors or suppliers, using a Form 1099 to report their earnings to the IRS. However, there are certain circumstances under which an independent contractor might be considered an employee for payroll purposes, such as if they are regularly working on-site at the company's premises or if they are performing work that is integral to the company's core business functions. In these cases, it may be necessary for the company to include the independent contractor on their payroll and provide them with employee benefits. Ultimately, the determination of whether an independent contractor should be on payroll will depend on a variety of factors, including the nature of the work being performed, the level of control the company has over the contractor's work, and the specific laws and regulations governing independent contractors in the relevant jurisdiction.

| Characteristics | Values |

|---|---|

| Employment Type | Independent Contractor |

| Payroll Status | On Payroll |

| Benefits | Typically not eligible for company benefits |

| Taxes | Company may not withhold taxes; contractor responsible for self-employment taxes |

| Control Level | Contractor has more autonomy; company has less control |

| Work Schedule | Flexible, as agreed upon by both parties |

| Payment Method | Paid per project or hourly, as specified in the contract |

| Legal Protections | Fewer legal protections compared to full-time employees |

| Contract Required | Yes, a formal contract is usually required |

| Termination | Easier to terminate compared to full-time employees |

Explore related products

What You'll Learn

- Definition of Independent Contractor: Understanding the legal distinctions between employees and independent contractors

- Tax Implications: Exploring how payroll taxes differ for independent contractors versus employees

- Benefits and Entitlements: Discussing whether independent contractors are eligible for company benefits

- Control and Direction: Analyzing the level of control a company can exert over independent contractors

- Legal Precedents: Reviewing court cases and legal guidelines that define independent contractor relationships

![]()

Definition of Independent Contractor: Understanding the legal distinctions between employees and independent contractors

An independent contractor is typically defined as a worker who performs services for a company but is not considered an employee. This distinction is crucial for legal and tax purposes, as it determines the rights, responsibilities, and benefits that the worker is entitled to. Independent contractors are usually hired on a project-by-project basis and have more control over their work schedule, methods, and outcomes compared to employees. They are also responsible for their own taxes, insurance, and equipment, which sets them apart from employees who receive these benefits from their employer.

Understanding the legal distinctions between employees and independent contractors is essential for companies to avoid misclassification, which can lead to legal disputes, penalties, and back taxes. The classification of a worker as an independent contractor or employee depends on various factors, including the level of control the company has over the worker's activities, the worker's economic dependence on the company, and the nature of the work being performed. Companies must carefully evaluate these factors to ensure that they are correctly classifying their workers and complying with applicable laws and regulations.

One common misconception is that simply labeling a worker as an independent contractor is sufficient to establish their status. However, this is not the case. The substance of the working relationship, rather than the label, is what determines whether a worker is an independent contractor or an employee. For example, if a company exerts significant control over a worker's schedule, tasks, and methods, that worker may be considered an employee, even if they are labeled as an independent contractor.

To avoid misclassification, companies should consider implementing clear policies and procedures for hiring and managing independent contractors. This may include using standardized contracts, providing training on the legal distinctions between employees and independent contractors, and regularly auditing their workforce to ensure compliance with applicable laws. By taking these steps, companies can reduce the risk of legal disputes and penalties related to misclassification.

In conclusion, understanding the legal distinctions between employees and independent contractors is crucial for companies to ensure compliance with applicable laws and regulations. By carefully evaluating the factors that determine a worker's classification and implementing clear policies and procedures, companies can avoid misclassification and the associated risks.

Understanding Payroll Fees: What Companies Can and Can't Charge

You may want to see also

Explore related products

![]()

Tax Implications: Exploring how payroll taxes differ for independent contractors versus employees

Payroll taxes are a critical aspect of employment that can significantly impact both employers and workers. When it comes to independent contractors versus employees, understanding the tax implications is essential for compliance and financial planning. Independent contractors are typically responsible for paying their own payroll taxes, including self-employment tax, which covers Social Security and Medicare. This can result in a higher tax burden compared to employees, who share the cost of these taxes with their employers.

One key difference between independent contractors and employees is the way payroll taxes are calculated and paid. For employees, payroll taxes are deducted from their wages and paid by the employer, with the employee's portion being matched by the employer. In contrast, independent contractors must calculate and pay their own payroll taxes, often through estimated tax payments made quarterly to the IRS. This requires independent contractors to be more proactive and diligent in managing their tax obligations.

Another important consideration is the potential for misclassification of workers. If an independent contractor is misclassified as an employee, the employer may be liable for unpaid payroll taxes, penalties, and interest. To avoid this, employers must carefully evaluate the nature of the working relationship and ensure that independent contractors are properly classified based on factors such as the level of control, the permanence of the relationship, and the method of payment.

In addition to federal payroll taxes, state and local taxes can also vary significantly for independent contractors and employees. Some states have their own payroll tax systems, while others rely on the federal system. Independent contractors may need to pay state income tax, state unemployment tax, and local taxes, depending on their location and the nature of their work. Employers, on the other hand, may need to withhold and pay state and local taxes on behalf of their employees.

To navigate these complex tax implications, both independent contractors and employers should consult with a tax professional or accountant. They can provide guidance on proper classification, tax planning strategies, and compliance with federal, state, and local tax laws. By understanding the unique tax obligations of independent contractors and employees, businesses can avoid costly mistakes and ensure a smooth and compliant payroll process.

Understanding 1099 Forms: Can They Be Included in Payroll?

You may want to see also

Explore related products

![]()

Benefits and Entitlements: Discussing whether independent contractors are eligible for company benefits

Independent contractors are typically not eligible for company benefits, which is a significant distinction from traditional employees. This lack of eligibility stems from the fundamental nature of the independent contractor relationship, which is characterized by a high degree of autonomy and a lack of direct control by the hiring company. As a result, independent contractors are generally responsible for securing their own benefits, such as health insurance, retirement plans, and workers' compensation coverage.

One of the key benefits that independent contractors often miss out on is access to employer-sponsored health insurance plans. This can be a significant disadvantage, especially for contractors who work in industries with high health risks or who have pre-existing medical conditions. Additionally, independent contractors are typically not eligible for paid time off, including vacation days, sick leave, and holidays, which can impact their overall work-life balance and financial stability.

However, there are some exceptions to this general rule. In certain cases, companies may choose to offer benefits to independent contractors as a way to attract and retain top talent. This might include offering access to group health insurance plans, retirement savings options, or other perks such as training and development opportunities. Additionally, some states and localities have laws that require companies to provide certain benefits to independent contractors, such as workers' compensation coverage or paid sick leave.

When it comes to determining whether independent contractors are eligible for company benefits, it's essential to carefully review the terms of the contractor agreement and any applicable laws and regulations. Companies should also consider the potential risks and liabilities associated with providing benefits to independent contractors, as this could impact their legal and financial obligations.

In conclusion, while independent contractors are generally not eligible for company benefits, there are some exceptions and nuances to this rule. Companies should carefully weigh the pros and cons of offering benefits to independent contractors and ensure that they are in compliance with all relevant laws and regulations.

Paying Payroll with Credit Cards: Benefits, Risks, and Best Practices

You may want to see also

Explore related products

![]()

Control and Direction: Analyzing the level of control a company can exert over independent contractors

Companies often engage independent contractors to perform specific tasks or projects, valuing the flexibility and specialized skills they bring. However, a crucial aspect of this arrangement is the level of control the company can exert over the contractor's work. While independent contractors are generally considered self-employed and responsible for their own work methods, companies may still need to provide direction to ensure the work aligns with their objectives and standards.

The degree of control a company can have over an independent contractor is typically outlined in the contract agreement. This can include specifications on the scope of work, deadlines, deliverables, and performance expectations. Companies may also establish guidelines for communication, reporting, and decision-making processes. However, it's essential to strike a balance between providing necessary direction and respecting the contractor's autonomy. Excessive control could potentially reclassify the relationship as that of an employer and employee, which has legal and tax implications.

In practice, companies can exert control over independent contractors in various ways. For instance, they may require regular progress updates, conduct performance reviews, or provide feedback on deliverables. They might also set standards for quality, safety, and compliance that the contractor must adhere to. However, these measures should be implemented carefully to avoid crossing the line into micromanagement, which could undermine the contractor's independence and potentially lead to disputes or legal challenges.

To maintain a healthy working relationship with independent contractors, companies should focus on clear communication and mutual respect. This involves setting realistic expectations, providing timely feedback, and being open to the contractor's input and suggestions. By fostering a collaborative environment, companies can ensure that independent contractors feel valued and motivated to deliver their best work, while still maintaining the necessary level of control to achieve their business objectives.

Ultimately, the key to successfully managing independent contractors lies in finding the right balance between control and autonomy. Companies must be mindful of the legal and practical implications of their actions and strive to create a working relationship that is beneficial for both parties. By doing so, they can leverage the unique skills and expertise of independent contractors while maintaining the necessary oversight to ensure the work meets their standards and objectives.

Exploring PPP Eligibility: Can Businesses Without Payroll Apply?

You may want to see also

Explore related products

![]()

Legal Precedents: Reviewing court cases and legal guidelines that define independent contractor relationships

The determination of whether a worker is an independent contractor or an employee is a critical aspect of labor law, with significant implications for both the worker and the employer. Legal precedents and guidelines play a crucial role in defining these relationships, and understanding them is essential for companies looking to engage independent contractors.

One key legal precedent is the case of NLRB v. United Insurance Co. of America, where the National Labor Relations Board (NLRB) established a set of criteria to determine whether a worker is an independent contractor or an employee. These criteria include the degree of control the employer has over the worker's activities, the worker's economic dependence on the employer, and the nature of the work being performed.

Another important guideline is the IRS's 20-factor test, which is used to determine whether a worker is an employee or an independent contractor for tax purposes. This test considers factors such as the level of control the employer has over the worker's schedule, the worker's ability to subcontract work, and the worker's investment in their own business.

In addition to these precedents and guidelines, there are also industry-specific regulations that can impact the classification of workers. For example, the Fair Labor Standards Act (FLSA) has specific rules for determining whether a worker is an employee or an independent contractor in the context of wage and hour laws.

Companies looking to engage independent contractors should carefully review these legal precedents and guidelines to ensure that they are properly classifying their workers. Failure to do so can result in significant legal and financial consequences, including back wages, penalties, and even criminal charges.

Ultimately, the key to successfully engaging independent contractors is to have a clear understanding of the legal framework that governs these relationships. By staying informed and up-to-date on the latest legal precedents and guidelines, companies can minimize their risk and ensure that they are in compliance with the law.

Maximizing Your 401(k) Match: Understanding Certified Payroll Contributions

You may want to see also

Frequently asked questions

Yes, a company can have an independent contractor on payroll. However, it's important to note that independent contractors are typically not considered employees and therefore are not entitled to the same benefits and protections as employees.

There are several benefits to having an independent contractor on payroll. These include:

- Flexibility: Independent contractors can be hired on a project-by-project basis, allowing companies to scale their workforce up or down as needed.

- Cost savings: Independent contractors are not entitled to the same benefits and protections as employees, which can save companies money on things like health insurance and workers' compensation.

- Expertise: Independent contractors often have specialized skills and expertise that can be valuable to companies.

There are also some drawbacks to having an independent contractor on payroll. These include:

- Lack of control: Independent contractors are not employees, so companies have less control over their work and schedules.

- Potential for misclassification: If an independent contractor is misclassified as an employee, the company could face legal and financial consequences.

- Limited loyalty: Independent contractors may not be as loyal to the company as employees, as they are not invested in the company's long-term success.