The question of whether a multi-member LLC owner can be on payroll is a common one among business owners and managers. In general, LLC owners are not considered employees of the company and therefore cannot be placed on payroll in the same way that traditional employees are. However, there are certain circumstances under which an LLC owner may be able to receive compensation through payroll, such as if they are also an employee of the company or if they have a separate agreement in place with the other members of the LLC. It is important for LLC owners to understand the legal and tax implications of receiving compensation through payroll, as well as the potential benefits and drawbacks of doing so. Consulting with a business attorney or accountant can help LLC owners navigate these complex issues and make informed decisions about their compensation arrangements.

| Characteristics | Values |

|---|---|

| Ownership Structure | Multi-member LLC |

| Owner Role | Can be on payroll |

| Employment Status | Employee of the LLC |

| Income Source | Salary or wages from LLC |

| Tax Implications | Subject to payroll taxes |

| Management Involvement | May have management responsibilities |

| Decision-Making Authority | Participates in LLC decisions |

| Profit Distribution | May receive profit distributions |

| Legal Protections | Limited liability protection |

| Compliance Requirements | Must comply with LLC operating agreement and state laws |

Explore related products

What You'll Learn

- Definition of Multi-Member LLC: An LLC with more than one owner, known as members

- Owner Roles in LLC: Members can be actively involved in management or act as passive investors

- Payroll Eligibility: Members actively working in the LLC may be eligible for payroll

- Tax Implications: Being on payroll can affect tax liabilities and deductions for the LLC and members

- Legal Considerations: Employment agreements and state laws may influence whether members can be on payroll

![]()

Definition of Multi-Member LLC: An LLC with more than one owner, known as members

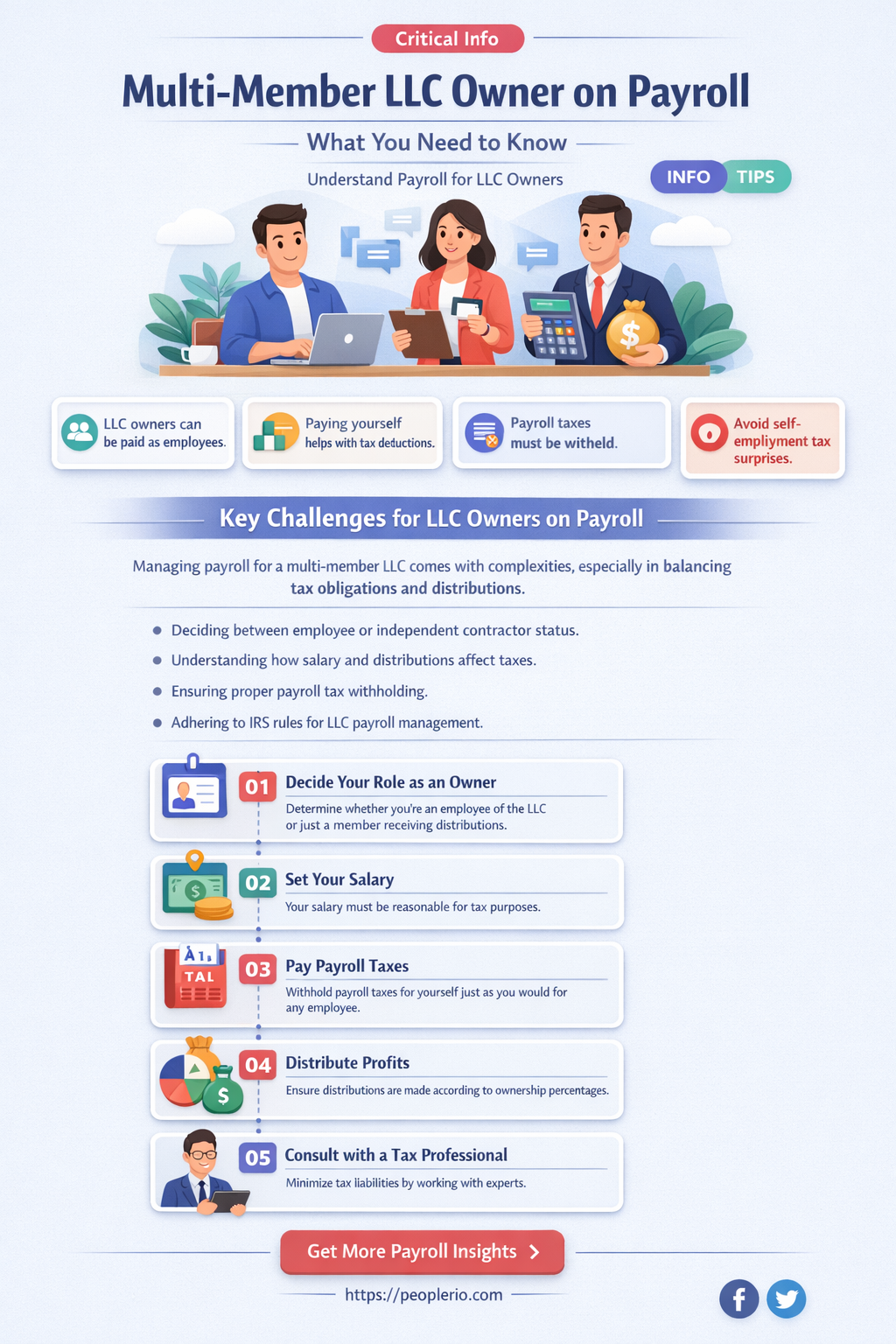

A Multi-Member LLC is a type of Limited Liability Company that has more than one owner, referred to as members. This structure allows for shared management and decision-making among the members, who can number anywhere from two to an unlimited amount, depending on the state's regulations. Each member typically contributes capital to the business and has a percentage ownership stake, which determines their share of profits and losses.

One of the key benefits of a Multi-Member LLC is the flexibility it offers in terms of management. Members can choose to manage the company themselves or appoint managers to oversee the day-to-day operations. This structure also provides limited liability protection, meaning that the personal assets of the members are generally protected from the debts and liabilities of the business.

When it comes to payroll, a Multi-Member LLC can indeed have owners on payroll. However, this arrangement requires careful consideration and adherence to specific guidelines. Members who are actively involved in the management of the company can be compensated for their services, but this compensation must be reasonable and justifiable. It's important to establish clear roles and responsibilities for each member to avoid any conflicts of interest or disputes over compensation.

To ensure compliance with tax regulations, a Multi-Member LLC should maintain accurate records of all payments made to members, including salaries, bonuses, and distributions. These payments should be reported on the appropriate tax forms, such as Form W-2 for employee compensation and Form 1099 for non-employee compensation. Additionally, members should be aware of the potential tax implications of receiving both salary and distributions from the LLC, as this can affect their personal tax liabilities.

In conclusion, a Multi-Member LLC offers a flexible and protective business structure that allows for multiple owners to share in the management and profits of the company. While members can be on payroll, it's crucial to follow proper guidelines and maintain accurate records to ensure compliance with tax regulations and avoid any potential legal issues.

Exploring the Possibilities: Can a 501(c) Organization Offer Payroll Services?

You may want to see also

Explore related products

![]()

Owner Roles in LLC: Members can be actively involved in management or act as passive investors

In a Limited Liability Company (LLC), the flexibility of ownership roles allows members to either take an active part in management or remain as passive investors. This distinction is crucial for understanding how members can be compensated, particularly when it comes to being on the payroll.

Actively involved members, often referred to as managing members, have the authority to make key business decisions and oversee daily operations. They are typically entitled to a salary or wages for their services, as they are essentially working for the company. This compensation is usually structured through an employment agreement or a similar contractual arrangement. In addition to their salary, managing members may also receive distributions from the company's profits, akin to dividends paid to shareholders in a corporation.

On the other hand, passive investors, or non-managing members, do not participate in the day-to-day management of the LLC. Their involvement is generally limited to providing capital and receiving periodic distributions of profits. These members are not typically on the payroll, as they do not perform services for the company. Instead, their returns are primarily through profit distributions, which are subject to the terms outlined in the LLC's operating agreement.

It's important to note that the distinction between active and passive roles can impact tax implications and liability. Managing members are often considered employees for tax purposes, which means they are subject to payroll taxes such as Social Security and Medicare. Non-managing members, however, are usually treated as partners or investors, and their distributions are taxed differently.

In a multi-member LLC, the operating agreement should clearly define the roles and responsibilities of each member, as well as the compensation structure. This document serves as the blueprint for how the company is run and how profits are distributed, ensuring that all members are aligned and understand their respective positions within the company.

In conclusion, whether a multi-member LLC owner can be on the payroll largely depends on their role within the company. Managing members who are actively involved in the business can be compensated through a salary, while non-managing members who act as passive investors typically receive profit distributions and are not on the payroll. Understanding these roles and their implications is essential for structuring an LLC in a way that is both efficient and compliant with tax regulations.

Exploring PPP Eligibility: Can Businesses Without Payroll Apply?

You may want to see also

Explore related products

![]()

Payroll Eligibility: Members actively working in the LLC may be eligible for payroll

To determine payroll eligibility for members of a multi-member LLC, it's essential to understand the criteria that define "actively working" within the organization. This typically involves assessing the member's role, responsibilities, and the amount of time they dedicate to the LLC's operations. Members who are actively involved in the day-to-day management, execution of tasks, or decision-making processes are generally considered eligible for payroll.

One key consideration is the distinction between an active member and a passive investor. While passive investors may contribute capital to the LLC, they do not typically engage in the regular operations of the business. As such, they would not be eligible for payroll. On the other hand, active members who contribute their time, skills, and expertise to the LLC's activities would be considered employees and thus eligible for compensation through payroll.

It's also important to note that payroll eligibility may be influenced by the LLC's operating agreement. This document should clearly outline the terms and conditions under which members are entitled to receive compensation. If the operating agreement specifies certain criteria for payroll eligibility, such as a minimum number of hours worked or specific roles and responsibilities, these must be adhered to when determining which members qualify.

In some cases, it may be necessary to consult with a legal or financial professional to ensure that the LLC is complying with all applicable laws and regulations regarding payroll eligibility. This is particularly important when dealing with complex situations, such as members who work in multiple capacities or those who are also investors in the LLC. By seeking expert guidance, the LLC can ensure that it is making accurate and lawful determinations about payroll eligibility for its members.

Navigating Little Caesars Customer Service for Effective Complaint Resolution

You may want to see also

Explore related products

![]()

Tax Implications: Being on payroll can affect tax liabilities and deductions for the LLC and members

When a multi-member LLC owner is on payroll, it can have significant tax implications for both the LLC and its members. One of the primary considerations is the impact on self-employment taxes. LLC members who are on payroll may be subject to FICA taxes, which include Social Security and Medicare taxes. This can result in a higher tax burden compared to if they were simply taking distributions from the LLC.

Another important factor to consider is the potential for increased tax deductions. When an LLC owner is on payroll, they may be able to deduct certain expenses related to their employment, such as health insurance premiums and retirement plan contributions. This can help to offset some of the additional tax liabilities incurred by being on payroll.

The tax implications can also vary depending on the specific structure of the LLC. For example, if the LLC is taxed as a partnership, the members may be able to deduct their share of the LLC's business expenses on their personal tax returns. However, if the LLC is taxed as a corporation, the members may not be able to deduct these expenses, and the LLC may be subject to corporate income tax.

It's also important to consider the impact of payroll taxes on the LLC's cash flow. When an LLC owner is on payroll, the LLC will need to withhold and remit payroll taxes to the IRS. This can reduce the amount of cash available to the LLC for other purposes, such as investing in the business or making distributions to members.

In conclusion, being on payroll can have a significant impact on the tax liabilities and deductions for both the LLC and its members. It's important for LLC owners to carefully consider these implications and consult with a tax professional to ensure they are making the most tax-efficient decisions for their business.

Contractor's Right to Request Payroll Proof from Subcontractors

You may want to see also

Explore related products

![]()

Legal Considerations: Employment agreements and state laws may influence whether members can be on payroll

Employment agreements and state laws play a crucial role in determining whether members of a multi-member LLC can be on payroll. This is because the legal structure of an LLC allows for flexibility in how members are compensated, but certain legal considerations must be taken into account. For instance, if an LLC is treated as a partnership for tax purposes, members may not be able to receive a salary in the traditional sense, as they are considered self-employed. However, they may be able to take distributions from the LLC, which are taxed as personal income.

One of the key legal considerations is the distinction between members and employees. In many states, LLC members are not considered employees unless they are explicitly hired as such. This means that members may not be entitled to certain employee benefits, such as unemployment insurance or workers' compensation, unless they are also employees of the LLC. To avoid confusion and potential legal issues, it is important for LLCs to clearly define the roles and compensation of their members in their operating agreements.

Another important consideration is the impact of state laws on payroll practices. Some states have specific laws governing the payment of wages, including minimum wage requirements, overtime pay, and payroll frequency. LLCs must comply with these laws when paying their employees, including members who are also employees. Failure to comply with state wage laws can result in penalties and legal action against the LLC.

In addition to state laws, federal laws also play a role in determining whether LLC members can be on payroll. For example, the Fair Labor Standards Act (FLSA) sets minimum wage and overtime requirements for employees, including those working for LLCs. The FLSA also defines the criteria for determining whether an individual is an employee or an independent contractor, which can impact how LLC members are compensated.

To navigate these legal considerations, LLCs should consult with an attorney or a payroll professional to ensure that their payroll practices comply with both state and federal laws. They should also review their operating agreements to ensure that the roles and compensation of members are clearly defined and consistent with legal requirements. By taking these steps, LLCs can avoid potential legal issues and ensure that their members are properly compensated for their work.

Maximizing Your Roth 401(k) Contributions Beyond Payroll Deductions

You may want to see also