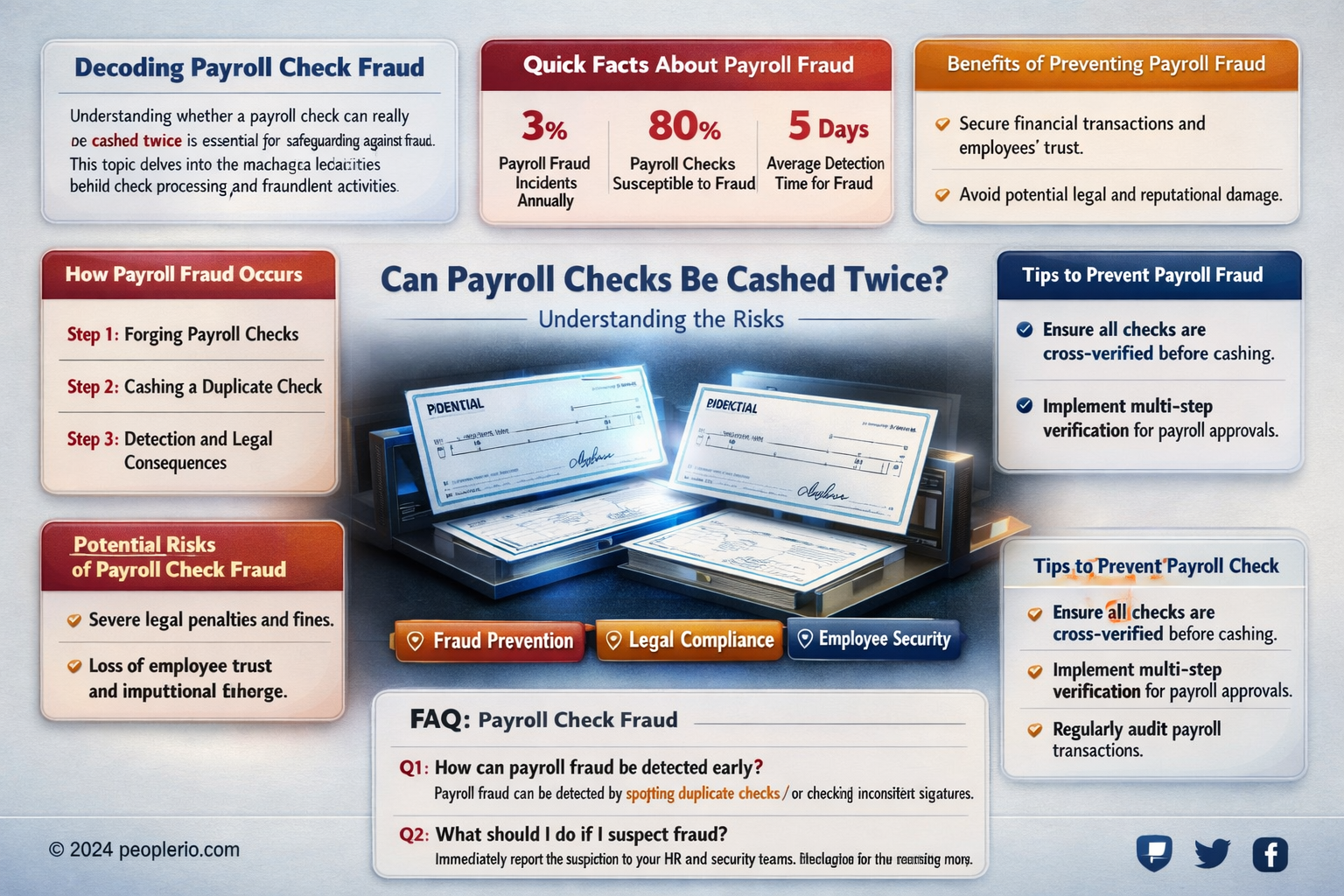

The question of whether a payroll check can be cashed twice is an important one in the realm of personal finance and banking. In general, a payroll check is intended to be cashed or deposited only once, as it represents a single payment for services rendered. Attempting to cash a payroll check twice could potentially lead to legal and financial repercussions. Banks typically have systems in place to prevent duplicate transactions, and if a check is presented for deposit or cashing more than once, it may be flagged as fraudulent. It's crucial for individuals to understand the proper procedures for handling payroll checks to avoid any misunderstandings or legal issues.

| Characteristics | Values |

|---|---|

| Check Type | Payroll Check |

| Action | Cashing Twice |

| Legality | Generally Illegal |

| Potential Consequences | Fraud Charges, Bank Fees |

| Prevention Methods | Bank Verification, Check Number Tracking |

| Related Laws | Check Fraud Statutes, Bank Regulations |

Explore related products

What You'll Learn

- Legal Implications: Discussing the legal consequences and potential fraud involved in attempting to cash a payroll check twice

- Bank Policies: Explaining how banks typically handle duplicate check presentations and their policies on preventing double payments

- Employer's Role: Describing the employer's responsibilities in ensuring payroll checks are not duplicated and their recourse if fraud occurs

- Employee's Perspective: Offering guidance to employees on how to handle situations where they believe their payroll check has been fraudulently cashed

- Preventive Measures: Providing tips and strategies for both employers and employees to prevent payroll check fraud and ensure secure transactions

![]()

Legal Implications: Discussing the legal consequences and potential fraud involved in attempting to cash a payroll check twice

Attempting to cash a payroll check twice can have serious legal implications. This action is considered check fraud, a crime that involves knowingly presenting a check with the intent to deceive or obtain money unlawfully. The legal consequences of such an act can vary depending on the jurisdiction, but generally, it can result in criminal charges, fines, and even imprisonment.

Check fraud is a serious offense because it undermines the integrity of financial transactions and can lead to significant losses for both individuals and businesses. When a payroll check is cashed twice, it creates a false sense of financial security for the recipient, who may then spend the money believing it is rightfully theirs. However, when the fraud is discovered, the victim may be required to repay the stolen funds, leading to financial hardship and potential legal action against them as well.

In addition to the direct legal consequences, attempting to cash a payroll check twice can also have long-term effects on an individual's financial reputation. It can damage their credit score, making it more difficult to obtain loans or credit in the future. Furthermore, it can lead to a loss of trust from employers and financial institutions, which can have lasting impacts on their professional and personal life.

To avoid these legal implications, it is crucial to handle payroll checks with care and honesty. If a check is lost or stolen, it should be reported immediately to the issuer and the appropriate authorities. Additionally, individuals should be aware of the laws and regulations surrounding check fraud in their jurisdiction and take steps to protect themselves from becoming victims of this crime.

In conclusion, the legal implications of attempting to cash a payroll check twice are severe and can have far-reaching consequences. It is essential to understand the risks and potential penalties associated with check fraud and to take proactive measures to prevent it. By doing so, individuals can protect themselves and others from the harmful effects of this crime.

Understanding Payroll Check Validity: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Bank Policies: Explaining how banks typically handle duplicate check presentations and their policies on preventing double payments

Banks have stringent policies in place to prevent duplicate check presentations and double payments. These policies are designed to protect both the bank and its customers from financial losses and fraud. When a check is presented for payment, banks use various systems to verify its authenticity and ensure that it has not been previously cashed or deposited.

One common method used by banks is to compare the check's details, such as the check number, date, and amount, against their internal records. If a duplicate check is detected, the bank will typically reject the second presentation and notify the customer of the issue. In some cases, banks may also use image recognition technology to compare the physical appearance of the check against their database of previously processed checks.

To further prevent double payments, banks often implement strict cutoff times for check processing. This means that checks presented after a certain time of day may not be processed until the next business day, reducing the likelihood of a duplicate check being cashed before the original has cleared. Additionally, banks may place limits on the number of checks that can be cashed or deposited within a certain timeframe, which can help to prevent fraudulent activity.

In the event that a duplicate check is successfully cashed, banks have procedures in place to recover the funds and rectify the situation. This may involve contacting the customer who presented the duplicate check, as well as any other parties involved in the transaction. In some cases, banks may also work with law enforcement to investigate and prosecute cases of check fraud.

Overall, bank policies play a crucial role in preventing duplicate check presentations and double payments. By implementing robust verification systems, cutoff times, and limits on check processing, banks can effectively protect their customers and themselves from financial losses and fraud.

Decoding Payroll Check Cashing: Your Ultimate Guide to Time Limits

You may want to see also

Explore related products

![]()

Employer's Role: Describing the employer's responsibilities in ensuring payroll checks are not duplicated and their recourse if fraud occurs

Employers have a critical role in preventing payroll check fraud, which includes ensuring that checks are not duplicated and cashed multiple times. One of the primary responsibilities is to implement robust internal controls over the payroll process. This involves segregating duties so that no single individual has control over all aspects of payroll processing, from check issuance to reconciliation. Employers should also conduct regular audits of their payroll systems to detect any anomalies or discrepancies that could indicate fraudulent activity.

Another key responsibility is to educate employees about the risks of payroll check fraud and how to protect themselves. This includes providing training on how to properly handle and store payroll checks, as well as how to recognize and report suspicious activity. Employers should also establish clear policies and procedures for reporting lost or stolen checks, and ensure that these policies are communicated to all employees.

In the event of fraud, employers have several recourse options available. They can work with their bank to stop payment on the fraudulent check and recover the funds. Employers may also need to file a police report and cooperate with law enforcement to investigate the fraud. Additionally, they should review their internal controls and make any necessary adjustments to prevent similar incidents from occurring in the future.

Employers should also consider implementing electronic payroll systems, which can reduce the risk of check fraud. Electronic payroll systems allow employers to deposit employees' wages directly into their bank accounts, eliminating the need for physical checks. This not only reduces the risk of check fraud but also streamlines the payroll process and reduces administrative costs.

In summary, employers play a crucial role in preventing payroll check fraud by implementing strong internal controls, educating employees, and taking swift action in the event of fraud. By taking these steps, employers can protect their employees' wages and maintain the integrity of their payroll systems.

Exploring Payroll Check Transfers: Can You Sign Over to Someone Else?

You may want to see also

Explore related products

![]()

Employee's Perspective: Offering guidance to employees on how to handle situations where they believe their payroll check has been fraudulently cashed

If you suspect that your payroll check has been fraudulently cashed, it's crucial to act quickly and follow a series of steps to protect yourself and your employer's interests. First, contact your bank immediately to report the suspected fraud. Provide them with all relevant details, including the check number, date, and amount. The bank will likely initiate an investigation and may need to freeze your account temporarily to prevent further unauthorized transactions.

Simultaneously, reach out to your employer's payroll department to inform them of the situation. They will need to verify the authenticity of the check and may need to issue a replacement check if the original was indeed cashed fraudulently. Be prepared to provide any necessary documentation, such as a police report or bank statements, to support your claim.

It's also important to monitor your credit report and bank statements closely for any signs of identity theft or additional fraudulent activity. Consider placing a fraud alert on your credit report to prevent the thief from opening new accounts in your name.

In terms of prevention, there are several steps you can take to reduce the risk of payroll check fraud. Always keep your personal information secure, including your Social Security number and bank account details. Be cautious when sharing sensitive information online or over the phone, and avoid using public Wi-Fi networks for financial transactions.

Finally, stay informed about the latest payroll check fraud schemes and scams. Attend training sessions or webinars offered by your employer or financial institution to learn more about how to protect yourself and your assets. By being proactive and vigilant, you can significantly reduce the risk of becoming a victim of payroll check fraud.

Do Payroll Clerks Verify Employee Timecards? An In-Depth Look

You may want to see also

Explore related products

![]()

Preventive Measures: Providing tips and strategies for both employers and employees to prevent payroll check fraud and ensure secure transactions

Employers can take several proactive steps to prevent payroll check fraud. First, they should implement a secure check issuance process, which may include using checks with security features such as watermarks, microprinting, and security threads. Additionally, employers can consider issuing checks with a limited validity period to reduce the window of opportunity for fraud. Regularly reviewing and reconciling payroll accounts can also help detect any discrepancies or unauthorized transactions early on. Employers should also educate their employees about the risks of payroll check fraud and the importance of safeguarding their personal and financial information.

Employees can also play a crucial role in preventing payroll check fraud. They should be vigilant about protecting their personal information, such as their Social Security number and bank account details, and avoid sharing them with unauthorized individuals. Employees should also be cautious when receiving emails or calls requesting sensitive information, as these may be phishing attempts. It is essential to verify the legitimacy of such requests by contacting the employer's payroll department directly. Furthermore, employees should regularly monitor their bank accounts for any suspicious activity and report any unauthorized transactions to their bank and employer immediately.

Another effective preventive measure is the use of direct deposit for payroll payments. Direct deposit eliminates the need for physical checks, reducing the risk of check fraud. Employers can encourage employees to opt for direct deposit by highlighting its convenience, security, and environmental benefits. Additionally, employers can consider implementing multi-factor authentication for payroll systems to add an extra layer of security and prevent unauthorized access.

In conclusion, preventing payroll check fraud requires a collaborative effort between employers and employees. By implementing secure check issuance processes, educating employees about fraud risks, and promoting the use of direct deposit, employers can significantly reduce the likelihood of payroll check fraud. Employees, on the other hand, should remain vigilant about protecting their personal information and report any suspicious activity to their bank and employer promptly.

Can a Friend Cash My Payroll Check? Exploring the Options

You may want to see also

Frequently asked questions

No, a payroll check cannot be cashed twice. Once a check has been cashed or deposited, it is considered processed, and attempting to cash it again is illegal and will likely result in the check being returned or declined.

If someone attempts to cash a payroll check twice, the bank will typically detect the duplicate transaction and flag it as fraudulent. This can lead to the check being returned unpaid, and the person attempting to cash it may face legal consequences, including potential charges for fraud or theft.

Employers can take several steps to prevent employees from cashing payroll checks twice. One common method is to use direct deposit, which eliminates the need for physical checks and reduces the risk of fraud. Employers can also implement strict policies and procedures for handling and distributing payroll checks, such as requiring employees to cash or deposit checks within a specific timeframe.

Cashing a payroll check twice is considered check fraud, which is a criminal offense. Depending on the jurisdiction and the amount of the check, the penalties for check fraud can include fines, community service, and even imprisonment. Additionally, the person who cashed the check twice may be required to pay restitution to the employer or the bank for any losses incurred as a result of the fraud.