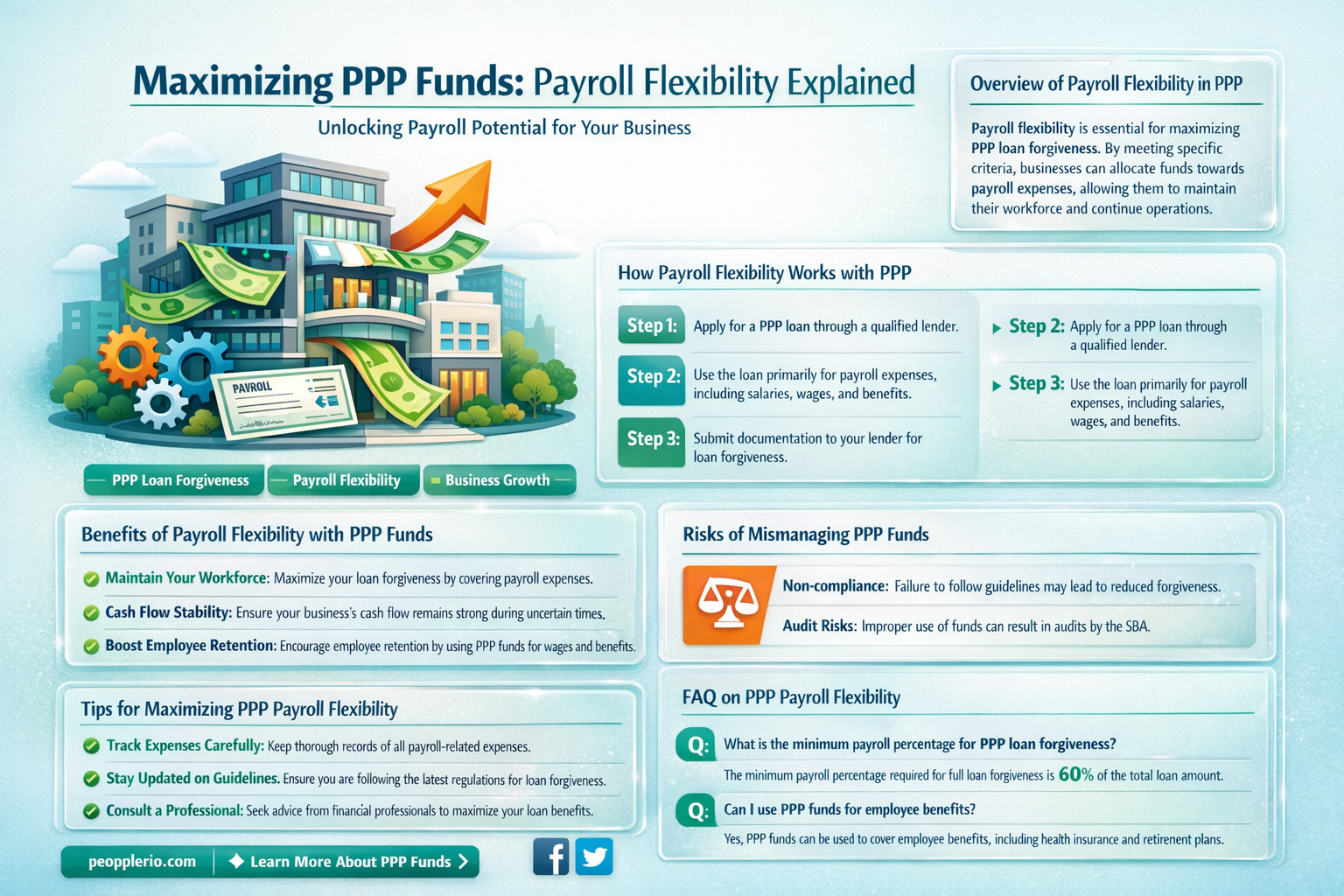

The question of whether all Paycheck Protection Program (PPP) funds can be used for payroll is a common one among business owners and managers. The PPP, established by the CARES Act in response to the COVID-19 pandemic, provides forgivable loans to eligible businesses to help cover payroll costs, rent, utilities, and other expenses. While the primary purpose of the PPP is to support payroll, not all funds can be used exclusively for this purpose. Businesses must use at least 60% of the loan amount for payroll costs to qualify for full loan forgiveness. The remaining 40% can be used for other eligible expenses such as rent, utilities, and mortgage interest. It's important to note that the specific rules and guidelines for PPP loan usage and forgiveness have evolved over time, so businesses should consult the latest information from the Small Business Administration (SBA) or a qualified financial advisor to ensure compliance.

| Characteristics | Values |

|---|---|

| Fund Type | PPP (Paycheck Protection Program) |

| Purpose | Payroll and other eligible expenses |

| Restriction | Not all PPP funds can be used solely for payroll |

| Eligible Expenses | Payroll, rent, mortgage interest, utilities |

| Forgiveness Criteria | Includes payroll as a qualifying expense |

| Documentation Required | Proof of payroll expenses and other eligible costs |

| Application Process | Through approved lenders and the SBA |

| Repayment Terms | Loans not forgiven must be repaid with interest |

Explore related products

What You'll Learn

- PPP Loan Forgiveness Criteria: Understand the requirements for loan forgiveness, including payroll and rent expenses

- Eligible Payroll Costs: Learn which payroll costs qualify for PPP funds, such as salaries, benefits, and taxes

- Maximum Loan Amount: Discover how the PPP loan amount is calculated based on your business's payroll costs

- Interest Rates and Terms: Explore the interest rates and repayment terms associated with PPP loans

- Application and Documentation: Find out what documents are needed to apply for a PPP loan and how to submit them

![]()

PPP Loan Forgiveness Criteria: Understand the requirements for loan forgiveness, including payroll and rent expenses

To qualify for PPP loan forgiveness, businesses must meet specific criteria regarding the use of funds. The primary requirement is that at least 60% of the loan amount must be used for payroll costs, which include salaries, wages, tips, and benefits. This ensures that the majority of the funds are directed towards maintaining employment and supporting workers.

In addition to payroll expenses, up to 40% of the loan can be used for other eligible costs, such as rent, mortgage interest, or utilities. It's important to note that these expenses must be incurred during the covered period, which is typically the time between February 15, 2020, and June 30, 2021.

One key aspect of the forgiveness criteria is the requirement to maintain employee and compensation levels. Businesses must retain at least 75% of their full-time equivalent (FTE) employees and cannot reduce salaries or hourly wages by more than 25% compared to the baseline period. This provision aims to prevent businesses from using PPP funds to subsidize layoffs or pay cuts.

Another important consideration is the documentation required to support the forgiveness application. Businesses must provide detailed records of how the PPP funds were used, including payroll reports, rent agreements, and utility invoices. This documentation will be used to verify that the funds were spent on eligible expenses and that the business met the necessary criteria.

In summary, PPP loan forgiveness is contingent upon meeting specific requirements, including the allocation of at least 60% of funds to payroll costs, maintaining employee and compensation levels, and providing thorough documentation of fund usage. By adhering to these criteria, businesses can ensure that they are eligible for loan forgiveness and can continue to support their workforce during challenging times.

Empowering Subcontractors: Payroll Certification Possibilities Explored

You may want to see also

Explore related products

![]()

Eligible Payroll Costs: Learn which payroll costs qualify for PPP funds, such as salaries, benefits, and taxes

To qualify for PPP funds, payroll costs must meet specific criteria set by the program. Salaries, wages, and tips are eligible, provided they are paid to employees who were on the payroll before February 15, 2020. This includes full-time, part-time, and seasonal workers, as well as sole proprietors and independent contractors. The maximum eligible salary per employee is $100,000 per year, prorated for the covered period.

Benefits such as health insurance premiums, retirement contributions, and paid leave are also eligible payroll costs. These benefits must be provided to employees who are receiving salary or wages, and the employer must have been offering these benefits before February 15, 2020. The PPP funds can be used to cover the employer's portion of these benefits, but not the employee's portion.

Taxes, including federal payroll taxes, state and local payroll taxes, and unemployment insurance premiums, are eligible payroll costs as well. These taxes must be paid by the employer and must be based on the salaries and wages paid to employees during the covered period. The PPP funds can be used to cover these taxes, but not any penalties or interest associated with them.

It's important to note that not all payroll costs are eligible for PPP funds. For example, severance pay, bonuses, and commissions are not eligible. Additionally, payroll costs for employees who are not on the payroll before February 15, 2020, are not eligible. Employers must carefully review the PPP guidelines to ensure that they are only using the funds for eligible payroll costs.

Multi-Member LLC Owner on Payroll: What You Need to Know

You may want to see also

Explore related products

$7.54

![]()

Maximum Loan Amount: Discover how the PPP loan amount is calculated based on your business's payroll costs

The maximum loan amount for a Paycheck Protection Program (PPP) loan is calculated based on a business's payroll costs, providing a crucial financial lifeline for companies affected by economic downturns. To determine the loan amount, lenders typically consider the borrower's average monthly payroll expenses, multiplied by a specific factor—often 2.5 times the average monthly payroll. This calculation ensures that the loan amount is substantial enough to cover several months of payroll, helping businesses maintain their workforce during challenging times.

For example, if a business has an average monthly payroll of $100,000, the maximum PPP loan amount would be $250,000 (100,000 x 2.5). This formula is designed to provide immediate financial relief, allowing businesses to continue paying their employees and covering other essential expenses.

It's important to note that while the maximum loan amount is based on payroll costs, the actual amount a business can borrow may be subject to additional factors, such as the business's creditworthiness, the lender's criteria, and the specific guidelines of the PPP program. Borrowers should carefully review the program's terms and conditions to understand the full scope of eligibility and loan usage.

In conclusion, the PPP loan amount calculation is a critical aspect of the program, designed to provide targeted financial support to businesses based on their payroll expenses. By understanding how the loan amount is determined, businesses can better navigate the application process and make informed decisions about their financial strategies during uncertain times.

Exploring Schedule C: Payroll and Dividends Explained

You may want to see also

Explore related products

![]()

Interest Rates and Terms: Explore the interest rates and repayment terms associated with PPP loans

The interest rates and repayment terms of PPP loans are critical factors for businesses to consider when evaluating the viability of this financial assistance program. Unlike traditional loans, PPP loans offer relatively low interest rates, typically ranging from 1% to 2%. This is a significant advantage for businesses struggling to maintain cash flow during challenging economic times. However, it's essential to note that these rates are subject to change based on market conditions and regulatory adjustments.

Repayment terms for PPP loans are also more flexible compared to conventional loans. Borrowers generally have up to 10 years to repay the loan in full, with payments deferred for the first six to twelve months. This deferral period provides businesses with immediate relief, allowing them to allocate funds to essential operations such as payroll, rent, and utilities. Moreover, PPP loans do not require collateral or personal guarantees, reducing the risk for borrowers and making the application process more accessible.

One unique aspect of PPP loans is the potential for loan forgiveness. If a business meets specific criteria, such as maintaining employee headcount and salary levels, and using loan funds for eligible expenses, a portion or all of the loan may be forgiven. This feature can significantly reduce the overall financial burden on businesses, effectively converting the loan into a grant. However, it's crucial for borrowers to carefully review and comply with the forgiveness requirements to avoid any penalties or legal issues.

In conclusion, the interest rates and repayment terms of PPP loans offer businesses a favorable financial solution during times of economic uncertainty. With low interest rates, flexible repayment terms, and the possibility of loan forgiveness, PPP loans can provide essential support for businesses looking to maintain operations and retain employees. By understanding these key aspects, businesses can make informed decisions about whether a PPP loan is the right choice for their financial needs.

Exploring Business Loan Options for Payroll Management

You may want to see also

![]()

Application and Documentation: Find out what documents are needed to apply for a PPP loan and how to submit them

To apply for a Paycheck Protection Program (PPP) loan, businesses must gather and submit several key documents. These typically include proof of business operation, such as articles of incorporation or a business license, as well as financial statements like income tax returns and bank statements. Additionally, applicants must provide payroll records to demonstrate the average monthly payroll costs for the previous year.

The application process for a PPP loan involves submitting these documents to an approved lender, who will then review the information and determine eligibility. It's important to note that the lender may request additional documentation based on the specific circumstances of the business. For example, if the business has recently changed ownership, the lender may require documentation of the change.

One common mistake businesses make when applying for a PPP loan is failing to provide complete and accurate documentation. This can lead to delays in the application process or even denial of the loan. To avoid this, it's crucial to carefully review the lender's requirements and ensure that all necessary documents are submitted in a timely manner.

Another important consideration is the timeframe for submitting the application. PPP loans are typically offered on a first-come, first-served basis, so it's essential to apply as soon as possible. Businesses should also be aware of any deadlines set by the lender or the government for submitting applications.

In conclusion, the key to a successful PPP loan application lies in providing complete and accurate documentation in a timely manner. By carefully reviewing the lender's requirements and submitting all necessary documents promptly, businesses can increase their chances of securing the funding they need to support their operations during challenging times.

Legal Insights: Can a Court Order Garnish a Company Payroll Account?

You may want to see also

Frequently asked questions

No, not all PPP (Paycheck Protection Program) funds can be used solely for payroll. While a significant portion of the funds is intended to support payroll costs, the program also allows for the use of funds to cover other eligible expenses such as rent, mortgage interest, and utilities.

To qualify for loan forgiveness under the PPP, at least 60% of the loan funds must be used for payroll costs. The remaining 40% can be allocated to other eligible expenses like rent, mortgage interest, and utilities.

Yes, there are restrictions on the use of PPP funds for payroll. The funds can only be used to cover payroll costs for employees who were on the payroll as of February 15, 2020. Additionally, the funds cannot be used to pay for the payroll costs of employees who earn more than $100,000 per year.