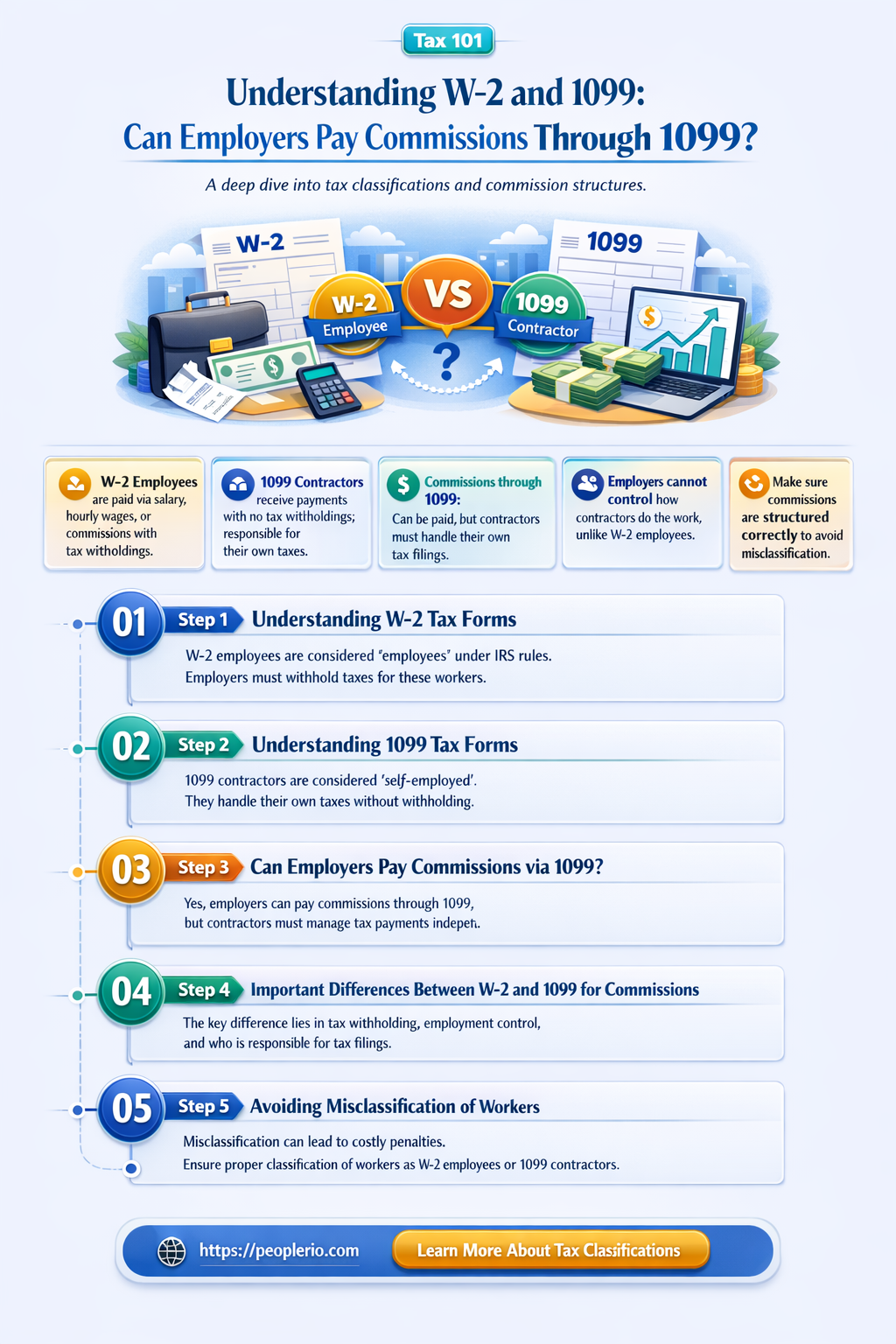

The question of whether an employer can pay a W-2 employee commissions through a 1099 form is a common one in the realm of payroll and tax compliance. Generally, W-2 employees are considered full-time workers who receive a regular salary or wages, and their income is reported on a W-2 form at the end of the year. On the other hand, 1099 forms are typically used to report income paid to independent contractors or freelancers. While it is possible for an employer to pay commissions to a W-2 employee through a 1099 form, it is important to understand the implications and potential consequences of doing so. This includes considering factors such as the employee's classification, the nature of the commissions, and the potential impact on tax withholding and reporting. Employers must ensure that they are in compliance with all applicable laws and regulations when making such payments to avoid penalties or legal issues.

Explore related products

What You'll Learn

- Definition of W-2 and 1099 Employees: Understand the legal distinctions between W-2 employees and 1099 contractors

- Commission Payment Structures: Explore common commission payment methods for W-2 employees and how they differ from 1099 payments

- Tax Implications: Discuss the tax consequences for both the employer and employee when paying commissions through a 1099

- Legal Considerations: Examine the legal requirements and potential issues when transitioning W-2 employees to 1099 contractors for commission payments

- Practical Examples: Provide real-world scenarios illustrating how employers might pay W-2 employees commissions through a 1099 arrangement

![]()

Definition of W-2 and 1099 Employees: Understand the legal distinctions between W-2 employees and 1099 contractors

Understanding the legal distinctions between W-2 employees and 1099 contractors is crucial for employers and workers alike. W-2 employees are considered full-time workers who receive a regular salary or hourly wage, and their employers are responsible for withholding taxes, Social Security, and Medicare from their paychecks. On the other hand, 1099 contractors are independent workers who are paid on a project-by-project basis and are responsible for their own tax withholdings.

One common question that arises is whether an employer can pay a W-2 employee commissions through a 1099 form. The short answer is no, as this would be considered a misclassification of the employee's status. W-2 employees must be paid through a W-2 form, which reports their wages and tax withholdings to the IRS. Paying a W-2 employee through a 1099 form would not only be illegal but could also result in penalties and fines for the employer.

To avoid misclassification, employers should carefully consider the nature of the work being performed and the level of control they have over the worker. If the worker is performing ongoing, regular work and the employer has significant control over their schedule and tasks, they are likely considered a W-2 employee. In contrast, if the worker is performing a specific project with minimal employer oversight, they may be considered a 1099 contractor.

In conclusion, it is essential for employers to understand the legal distinctions between W-2 employees and 1099 contractors to avoid misclassification and potential legal consequences. Employers should consult with a tax professional or labor attorney if they are unsure about the classification of their workers.

Discussing Pay at Work: What Are Your Rights and Employer's Limits?

You may want to see also

Explore related products

![]()

Commission Payment Structures: Explore common commission payment methods for W-2 employees and how they differ from 1099 payments

Commission payment structures for W-2 employees can vary widely depending on the industry, company policies, and the specific role of the employee. Typically, W-2 employees who are paid commissions receive a base salary plus a percentage of the sales they generate. This percentage can range from a few percent to over 50%, depending on the industry and the employee's level of experience and performance. In some cases, W-2 employees may also receive bonuses or other performance-based incentives in addition to their commissions.

One common commission payment method for W-2 employees is the "straight commission" structure, where the employee receives a fixed percentage of each sale they make. For example, a salesperson might receive 10% of the revenue from each sale they close. Another method is the "tiered commission" structure, where the commission rate increases as the employee reaches certain sales targets. For instance, an employee might receive 5% of sales up to $10,000, 10% of sales between $10,001 and $20,000, and 15% of sales above $20,000.

In contrast, 1099 payments are typically made to independent contractors or freelancers who are not considered employees of the company. These payments are usually based on a flat fee or a percentage of the project cost, rather than a commission structure. 1099 recipients are responsible for reporting their income and paying their own taxes, unlike W-2 employees whose taxes are withheld by their employer.

When it comes to paying W-2 employees commissions through a 1099, it's important to note that this is generally not a viable option. W-2 employees are considered employees of the company and must be paid through the company's payroll system, with appropriate taxes and deductions withheld. Paying a W-2 employee through a 1099 could be considered misclassification and could result in legal and financial penalties for the employer.

In summary, commission payment structures for W-2 employees can vary depending on the industry and company policies, but they typically involve a base salary plus a percentage of sales. 1099 payments, on the other hand, are usually made to independent contractors and are based on a flat fee or project cost. Employers should be cautious about paying W-2 employees through a 1099, as this could be considered misclassification and could lead to legal and financial consequences.

Can Employers Suspend Employees Without Pay? Legal Insights and Best Practices

You may want to see also

Explore related products

![]()

Tax Implications: Discuss the tax consequences for both the employer and employee when paying commissions through a 1099

When an employer pays commissions to a W-2 employee through a 1099 form, it can have significant tax implications for both parties. The employer may be attempting to avoid paying payroll taxes, but this practice is generally not advisable and can lead to legal and financial consequences.

From the employer's perspective, paying commissions through a 1099 form may seem like a way to reduce tax liabilities. However, if the employee is classified as a W-2 employee, the employer is required to withhold payroll taxes, including Social Security and Medicare taxes. Failing to do so can result in penalties and interest from the IRS. Additionally, the employer may be liable for back taxes, fines, and legal fees if the employee files a complaint or the IRS audits the company.

For the employee, receiving commissions through a 1099 form instead of a W-2 may seem like a way to avoid paying taxes. However, this is not the case. The employee is still responsible for paying taxes on the income received, and may face penalties and interest if they fail to report the income accurately. Additionally, the employee may miss out on certain benefits, such as unemployment insurance and workers' compensation, if they are not properly classified as a W-2 employee.

In conclusion, paying commissions to a W-2 employee through a 1099 form can have serious tax implications for both the employer and employee. It is important for employers to properly classify their employees and withhold the appropriate taxes to avoid legal and financial consequences. Employees should also be aware of their tax responsibilities and report their income accurately to avoid penalties and interest.

Exploring the Possibility: Can Companies Pay Taxes for Their Employees?

You may want to see also

Explore related products

![]()

Legal Considerations: Examine the legal requirements and potential issues when transitioning W-2 employees to 1099 contractors for commission payments

Transitioning W-2 employees to 1099 contractors for commission payments involves navigating a complex legal landscape. Employers must understand the distinctions between employee and contractor classifications to avoid misclassification, which can lead to legal repercussions including penalties, fines, and potential lawsuits. The IRS has specific guidelines for determining worker classification, focusing on factors such as the level of control the employer has over the worker, the worker's economic opportunity for profit or loss, and the degree of permanence in the relationship.

One of the primary legal considerations is ensuring compliance with tax laws. When an employer transitions a W-2 employee to a 1099 contractor, they must accurately report the contractor's earnings on Form 1099-MISC. This includes providing the contractor with a copy of the form by January 31st of the following year. Failure to do so can result in penalties for the employer. Additionally, employers must ensure that they are not withholding taxes from the contractor's payments, as this is the contractor's responsibility.

Another critical aspect is understanding the implications for employee benefits. W-2 employees are typically eligible for a range of benefits, including health insurance, retirement plans, and paid time off. When transitioning to a 1099 contractor status, these benefits may no longer be available, which can create challenges for both the employer and the contractor. Employers must communicate these changes clearly and ensure that they are not inadvertently depriving contractors of benefits they are entitled to under law.

Employers must also be aware of potential issues related to wage and hour laws. While 1099 contractors are generally not subject to minimum wage and overtime laws, misclassification of employees as contractors can lead to violations of these laws. Employers should carefully review their wage and hour policies to ensure compliance and avoid potential legal disputes.

In conclusion, transitioning W-2 employees to 1099 contractors for commission payments requires careful consideration of various legal requirements and potential issues. Employers must navigate tax laws, employee benefits, and wage and hour regulations to ensure a smooth transition and avoid legal pitfalls. By understanding these complexities and taking appropriate steps, employers can effectively manage the transition while minimizing risks and ensuring compliance with the law.

Understanding FUTA and SUTA: Impact on Employee Paychecks

You may want to see also

Explore related products

![]()

Practical Examples: Provide real-world scenarios illustrating how employers might pay W-2 employees commissions through a 1099 arrangement

In the realm of employment and taxation, there are instances where employers may consider paying W-2 employees commissions through a 1099 arrangement. This can be a complex process, as it involves navigating the nuances of tax law and employment regulations. One practical example of this scenario could be a company that hires sales representatives as W-2 employees but wants to incentivize them with commissions typically associated with independent contractors.

To accomplish this, the employer might establish a separate entity, such as a limited liability company (LLC), through which the commissions are paid. The W-2 employees would then be required to invoice the LLC for their commission earnings, and the LLC would issue them a 1099 form at the end of the year. This arrangement allows the employer to maintain control over the sales representatives while still providing them with the financial incentives of a commission-based structure.

Another example could be a company that contracts with freelancers or consultants who are also W-2 employees. In this case, the employer might pay the freelancers' commissions through a 1099 arrangement to simplify the payment process and avoid the need for additional payroll processing. However, it is crucial for the employer to ensure that the freelancers meet the IRS's criteria for independent contractors to avoid potential tax liabilities and penalties.

When implementing such an arrangement, employers must be mindful of the legal and tax implications. They should consult with a tax professional or employment attorney to ensure compliance with all applicable laws and regulations. Additionally, employers should clearly communicate the terms of the arrangement to the employees, including the payment structure, tax responsibilities, and any potential risks or benefits.

In conclusion, while it is possible for employers to pay W-2 employees commissions through a 1099 arrangement, it requires careful planning and consideration of the legal and tax implications. Employers should weigh the potential benefits of such an arrangement against the risks and consult with professionals to ensure compliance with all applicable laws and regulations.

Unpaid Labor: Know Your Rights as an Employee

You may want to see also

Frequently asked questions

Generally, no. W-2 employees are considered full-time workers and should receive their commissions as part of their regular wages, reported on a W-2 form. Paying commissions through a 1099 form is typically reserved for independent contractors or freelancers.

Employers who pay W-2 employee commissions through a 1099 form may face penalties and fines from the IRS for misclassifying employees. This is because the employer is avoiding payroll taxes and other obligations associated with W-2 employees.

Employers should pay commissions to W-2 employees as part of their regular wages, reported on a W-2 form. Commissions should be included in the employee's gross income and subject to payroll taxes, such as Social Security and Medicare.

W-2 employees are full-time workers who receive a regular salary and benefits, and their commissions are considered part of their wages. 1099 contractors, on the other hand, are independent workers who are paid on a project-by-project basis and are responsible for their own taxes. Commissions paid to 1099 contractors are typically reported on a 1099 form and are not subject to payroll taxes.