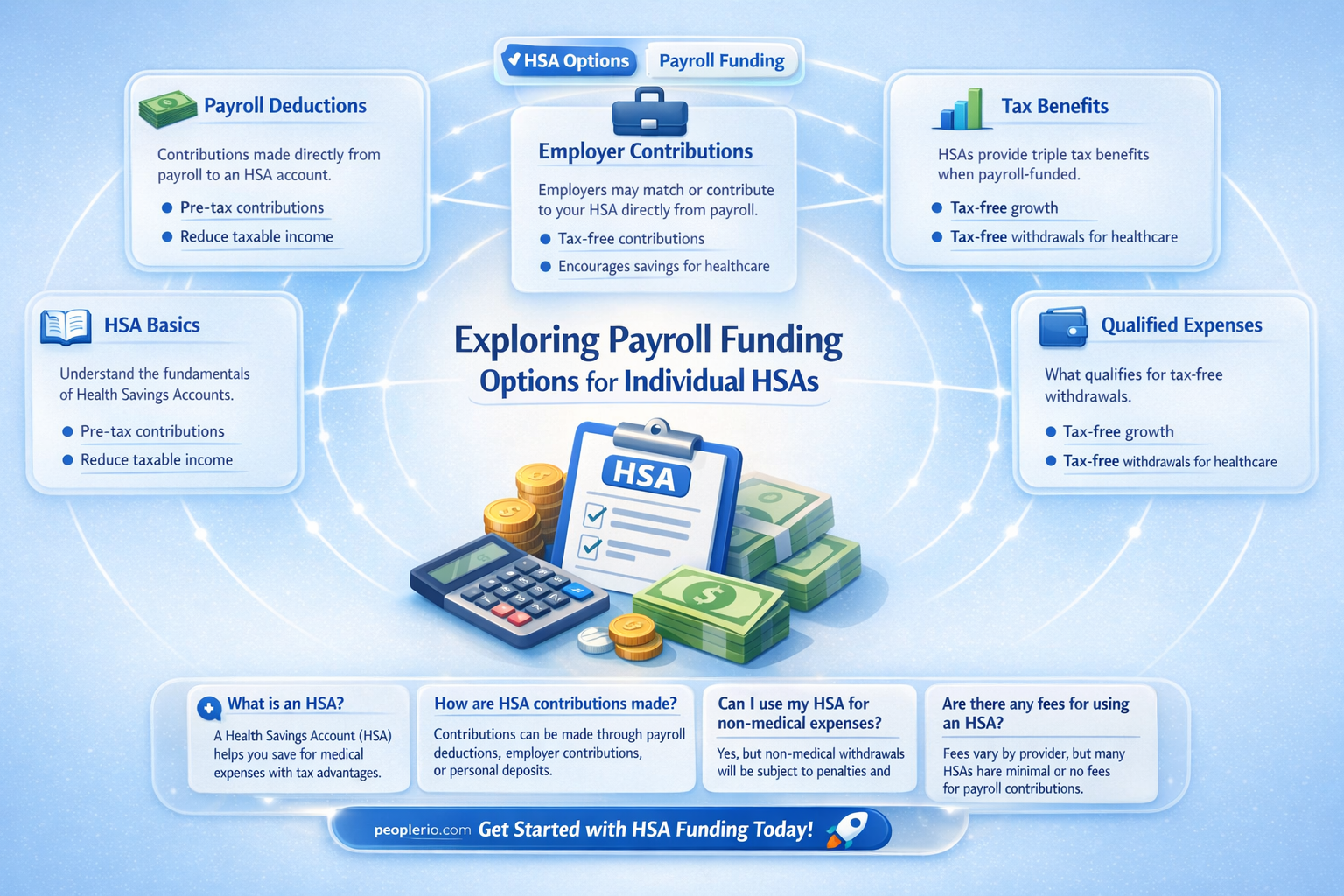

An individual Health Savings Account (HSA) is a tax-advantaged account used for saving and paying for qualified medical expenses. HSAs are typically funded by individuals, but there are circumstances under which they can be funded through payroll deductions. This approach allows employees to contribute to their HSAs directly from their paychecks, making it easier to save for healthcare costs. Employers may also choose to contribute to their employees' HSAs as part of their benefits package. However, it's important to note that payroll funding for HSAs is subject to certain rules and limitations, and not all employers offer this option.

Explore related products

What You'll Learn

- Eligibility: Employees must meet specific criteria to contribute to an HSA via payroll deductions

- Contribution Limits: There are annual limits to how much can be contributed to an HSA through payroll

- Tax Implications: Contributions are tax-deductible, reducing taxable income for the employee

- Employer Involvement: Employers may choose to contribute to employees' HSAs as part of their benefits package

- Administration: Payroll departments must ensure accurate and timely processing of HSA contributions

![]()

Eligibility: Employees must meet specific criteria to contribute to an HSA via payroll deductions

To contribute to a Health Savings Account (HSA) via payroll deductions, employees must meet several specific criteria. First and foremost, they must be enrolled in a high-deductible health plan (HDHP) that is HSA-compatible. This type of plan typically has lower premiums but higher out-of-pocket costs, which the HSA can help cover. Additionally, employees cannot be enrolled in Medicare, as this would disqualify them from contributing to an HSA.

Another key criterion is that the employee must not be claimed as a dependent on someone else's tax return. This means that if an employee is married and their spouse claims them as a dependent, they would not be eligible to contribute to an HSA through payroll deductions. Furthermore, employees who are under the age of 55 cannot contribute more than the annual limit set by the IRS, which is subject to change each year.

Employers may also have their own eligibility requirements, such as a minimum number of hours worked per week or a certain length of employment. It's important for employees to check with their employer's HR department to understand any additional criteria they may need to meet.

Once an employee has determined their eligibility, they can work with their employer to set up payroll deductions for their HSA. This process typically involves filling out a form specifying the amount they wish to contribute each pay period. Employers may also offer a matching contribution, which can help employees save even more for their healthcare expenses.

In summary, while HSAs can be a valuable tool for saving on healthcare costs, employees must carefully review the eligibility criteria to ensure they qualify for payroll deductions. By understanding these requirements and working with their employer, employees can make the most of this tax-advantaged savings opportunity.

Reversing Direct Deposits: What Payroll Companies Can and Can't Do

You may want to see also

Explore related products

![]()

Contribution Limits: There are annual limits to how much can be contributed to an HSA through payroll

The contribution limits to an HSA through payroll are a critical aspect to understand for both employers and employees. As of 2023, the IRS sets the annual contribution limit for individuals at $3,850 and for families at $7,750. These limits apply regardless of whether the contributions are made by the employee, the employer, or a combination of both. It's important to note that these figures are subject to change, and it's advisable to check the IRS website for the most current information.

One unique angle to consider is the impact of these contribution limits on tax savings. Contributions to an HSA are pre-tax, which means they reduce the individual's taxable income for the year. Therefore, maximizing contributions up to the limit can result in significant tax savings. For example, if an individual contributes the full $3,850, they could potentially save around $1,000 in taxes, depending on their tax bracket.

Another aspect to explore is the strategic use of payroll contributions. Employers may choose to contribute to their employees' HSAs as a benefit, which can be a valuable tool for recruitment and retention. However, employer contributions count towards the annual limit, so careful planning is necessary to ensure that the total contributions do not exceed the IRS-imposed limits.

In addition, it's crucial to be aware of the potential penalties for over-contributing. If an individual exceeds the annual contribution limit, they may be subject to a 6% excise tax on the excess amount. This penalty can be avoided by carefully monitoring contributions throughout the year and adjusting payroll deductions accordingly.

Finally, it's worth mentioning the flexibility that HSAs offer in terms of withdrawals. Unlike other tax-advantaged accounts, HSAs allow for penalty-free withdrawals at any time for qualified medical expenses. This feature makes HSAs a versatile tool for managing healthcare costs, especially in conjunction with high-deductible health plans.

In conclusion, understanding the contribution limits to an HSA through payroll is essential for maximizing tax savings, avoiding penalties, and making the most of this valuable financial tool. By staying informed about the current limits and strategically planning contributions, individuals and employers can optimize the benefits of HSAs.

Sharing Payroll Info with Family: Legal and Ethical Considerations

You may want to see also

Explore related products

![]()

Tax Implications: Contributions are tax-deductible, reducing taxable income for the employee

Contributions to an HSA (Health Savings Account) made through payroll deductions offer significant tax advantages. These contributions are considered tax-deductible, which means they reduce the employee's taxable income. This reduction can lead to a lower tax liability, potentially resulting in a larger refund or a smaller tax bill at the end of the year.

One of the key benefits of this tax implication is that it allows employees to save money on their healthcare expenses while also reducing their tax burden. The funds contributed to the HSA are not subject to federal income tax, and in many cases, they are also exempt from state and local taxes. This makes HSAs a powerful tool for tax-efficient savings and healthcare expense management.

To maximize these tax benefits, employees should consider contributing the maximum allowable amount to their HSA each year. The IRS sets annual contribution limits, and for 2023, the limit for individuals is $3,850, while for families, it is $7,750. Contributions made by employers are also tax-deductible for the employee, further enhancing the tax savings potential of HSAs.

It's important to note that while contributions to an HSA are tax-deductible, withdrawals from the account for non-qualified expenses are subject to income tax and a 20% penalty. Therefore, it's crucial for employees to use their HSA funds wisely, reserving them for qualified medical expenses to maintain the tax advantages.

In summary, the tax implications of funding an HSA through payroll deductions can provide employees with a valuable opportunity to save on taxes while also setting aside funds for future healthcare needs. By understanding and leveraging these tax benefits, employees can make the most of their HSA and improve their overall financial well-being.

Exploring Payroll Options for Freelancers: A Comprehensive Guide

You may want to see also

Explore related products

$13.99 $14.99

![]()

Employer Involvement: Employers may choose to contribute to employees' HSAs as part of their benefits package

Employers have the option to contribute to their employees' Health Savings Accounts (HSAs) as part of their benefits package. This can be a strategic move for both the employer and the employee. From the employer's perspective, contributing to HSAs can be a tax-efficient way to provide additional compensation, as the contributions are generally tax-deductible for the employer and tax-free for the employee when used for qualified medical expenses.

For employees, employer contributions can significantly boost their HSA balance, allowing them to save more for future healthcare costs or invest the funds for potential growth. This can be particularly beneficial for employees who are trying to maximize their retirement savings or who anticipate higher healthcare expenses in the future.

When an employer chooses to contribute to an employee's HSA, it's important to understand the rules and regulations that govern these contributions. For example, the employer must ensure that the contributions are made on a pre-tax basis and that they do not exceed the annual contribution limits set by the IRS. Additionally, the employer should have a clear policy in place regarding the timing and amount of the contributions, as well as any vesting requirements or conditions that may apply.

From a practical standpoint, employers may need to work with their payroll provider to set up the HSA contributions as part of their regular payroll process. This may involve coordinating with the HSA administrator to ensure that the contributions are properly allocated to each employee's account. Employers should also consider providing education and resources to their employees to help them understand the benefits of HSAs and how to make the most of their employer's contributions.

In conclusion, employer involvement in funding HSAs can be a valuable benefit for both parties. By contributing to their employees' HSAs, employers can provide additional compensation in a tax-efficient manner, while employees can save more for future healthcare costs or invest for potential growth. However, it's important for employers to understand the rules and regulations that govern these contributions and to have a clear policy in place to ensure that the process is managed effectively.

Exploring Schedule C: Payroll and Dividends Explained

You may want to see also

Explore related products

![RENPHO Active Thermacool 2 Massage Gun with Heat and Cold, [2026 Upgraded] Percussion Deep Tissue Handheld Neck Massager, FSA Approved, Muscle Masajeador for Men Women Athletes HSA](https://m.media-amazon.com/images/I/61mtD8h+HyL._AC_UL320_.jpg)

![]()

Administration: Payroll departments must ensure accurate and timely processing of HSA contributions

Payroll departments play a critical role in the administration of Health Savings Accounts (HSAs). Ensuring accurate and timely processing of HSA contributions is essential for maintaining compliance with IRS regulations and providing employees with the benefits they need. This involves a meticulous process of calculating, deducting, and depositing contributions into individual HSA accounts.

One of the key responsibilities of payroll departments is to accurately calculate HSA contributions based on employee elections and IRS guidelines. This includes considering factors such as the employee's age, marital status, and the type of health insurance coverage they have. Payroll must also ensure that contributions do not exceed the annual limits set by the IRS, which can change from year to year.

Timely processing is equally important. Payroll departments must deduct HSA contributions from employee paychecks and deposit them into the appropriate HSA accounts promptly. Delays in processing can lead to employee dissatisfaction and potential compliance issues. Additionally, payroll must handle any changes to employee elections or account information in a timely manner to avoid errors and ensure that contributions are allocated correctly.

To facilitate accurate and timely processing, payroll departments should implement robust systems and procedures. This may include using specialized payroll software that can automate calculations and deductions, as well as providing employees with online tools to manage their HSA elections and account information. Regular training and updates for payroll staff are also crucial to ensure they are knowledgeable about the latest IRS regulations and best practices for HSA administration.

In conclusion, payroll departments must prioritize the accurate and timely processing of HSA contributions to ensure compliance with IRS regulations and provide employees with the benefits they need. By implementing effective systems and procedures, payroll can streamline the administration of HSAs and contribute to the overall financial well-being of employees.

Understanding Payroll Fees: What Companies Can and Can't Charge

You may want to see also

Frequently asked questions

Yes, an individual HSA can be funded by payroll deductions. This is a common method for contributing to an HSA, as it allows for regular, tax-free contributions directly from your paycheck.

Yes, funding an HSA through payroll deductions offers tax benefits. The contributions are made pre-tax, which reduces your taxable income. Additionally, the funds in the HSA grow tax-free, and qualified medical expenses can be paid with tax-free withdrawals.

Yes, there are contribution limits for HSAs. For 2023, the annual contribution limit for an individual is $3,850, and for a family, it is $7,750. These limits include both employer and employee contributions. It's important to note that these limits may change over time, so it's always a good idea to check the current IRS guidelines.