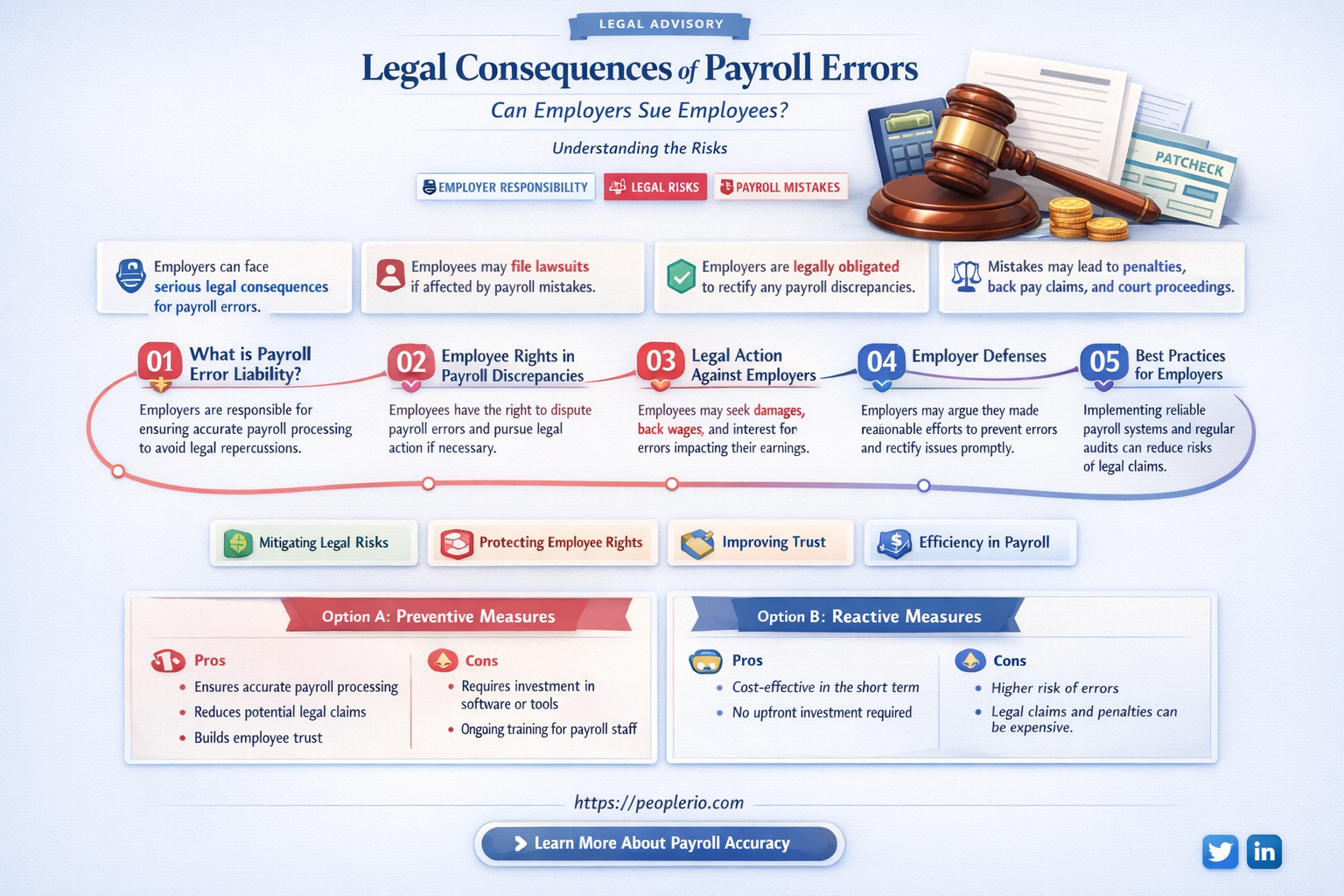

An employer can sue a payroll employee for calculation errors under certain circumstances. Typically, this would involve proving that the employee was negligent or breached their fiduciary duty, resulting in financial losses for the company. However, the specifics of such a case can vary greatly depending on the jurisdiction, the terms of the employee's contract, and the nature of the errors in question. It's important to note that in many cases, payroll errors are addressed through internal disciplinary measures or training rather than legal action. Employers must also consider the potential impact on employee morale and the company's reputation when deciding how to handle such situations.

| Characteristics | Values |

|---|---|

| Legal Grounds | Employers may sue payroll employees for calculation errors if it results in financial loss or damage to the company. |

| Common Causes | Common causes include incorrect data entry, miscalculations, failure to follow procedures, or intentional fraud. |

| Potential Damages | Potential damages can include the amount of money lost due to the error, legal fees, and any additional costs incurred to correct the issue. |

| Employer's Burden of Proof | The employer must provide evidence that the payroll employee was negligent or intentionally made the calculation error. |

| Employee Defenses | Employees may defend themselves by arguing that they followed proper procedures, that the error was unintentional, or that the employer's policies were unclear. |

| Statute of Limitations | The statute of limitations for suing a payroll employee for calculation errors varies by jurisdiction, but it typically ranges from one to three years. |

| Impact on Employee | A lawsuit can have a negative impact on the employee's reputation, career, and financial stability. |

| Alternatives to Litigation | Employers may choose to address calculation errors through internal disciplinary measures, training, or mediation instead of litigation. |

| Importance of Accuracy | Payroll calculation errors can have serious consequences for both employers and employees, highlighting the importance of accuracy and attention to detail in payroll processing. |

| Preventive Measures | Employers can implement preventive measures such as double-checking calculations, using automated payroll systems, and providing regular training to reduce the risk of errors. |

Explore related products

What You'll Learn

- Legal Grounds for Lawsuit: Employers may sue for negligence, breach of contract, or fraud if errors are intentional or reckless

- Types of Calculation Errors: Common errors include miscalculating wages, taxes, benefits, or overtime, leading to financial discrepancies

- Consequences of Errors: Errors can result in financial losses, penalties, interest, and damage to the employer's reputation

- Defenses Against Lawsuit: Employees might argue lack of training, system failures, or reasonable mistakes as defenses

- Preventive Measures: Implementing robust payroll systems, regular audits, and employee training can mitigate calculation errors

![]()

Legal Grounds for Lawsuit: Employers may sue for negligence, breach of contract, or fraud if errors are intentional or reckless

Employers have several legal avenues to pursue if they believe a payroll employee has made calculation errors that are either intentional or reckless. The three primary grounds for a lawsuit in such cases are negligence, breach of contract, and fraud.

Negligence occurs when an employee fails to exercise the level of care and attention that a reasonable person would under similar circumstances. In the context of payroll, this could involve making careless mistakes that result in significant financial losses for the employer. To prove negligence, the employer must show that the employee had a duty of care, breached that duty, and caused harm as a result.

Breach of contract arises when an employee violates the terms of their employment agreement. If the contract specifies that the employee is responsible for accurate payroll calculations and they fail to meet this obligation, the employer may have grounds for a lawsuit. The employer must demonstrate that a valid contract existed, the employee breached a specific term, and the breach caused damages.

Fraud is a more serious allegation that involves intentional deception or misrepresentation. If an employer believes that a payroll employee has deliberately manipulated financial data for personal gain or to cause harm to the company, they may sue for fraud. To succeed in a fraud lawsuit, the employer must prove that the employee made a false statement or omission, the employer relied on that statement, and the reliance resulted in damages.

In any of these cases, the employer must be able to provide evidence to support their claims. This may include documentation of the errors, witness testimony, and any relevant communications between the employer and the employee. It is also important for the employer to act promptly, as there may be time limits for filing a lawsuit depending on the jurisdiction and the specific legal grounds being pursued.

Understanding Payroll Eligibility for ITIN Holders: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Types of Calculation Errors: Common errors include miscalculating wages, taxes, benefits, or overtime, leading to financial discrepancies

Payroll calculation errors can manifest in various ways, each with its own set of consequences and challenges. One common type of error is the miscalculation of wages, which can occur due to incorrect hourly rates, misclassification of employees, or failure to account for deductions such as taxes and benefits. These errors can lead to underpayment or overpayment of employees, resulting in financial discrepancies that may go unnoticed until a thorough audit is conducted.

Another frequent mistake is the inaccurate calculation of taxes, which can arise from misunderstandings of tax laws, incorrect tax rates, or failure to withhold the appropriate amounts. This can lead to penalties and fines for the employer, as well as potential legal action from employees who may have been underpaid or overpaid as a result of the error.

Benefits miscalculations are also a common issue, often stemming from misinterpretations of benefit plans, incorrect enrollment dates, or failure to account for changes in employee status. These errors can result in employees being denied benefits they are entitled to, or being overcharged for benefits they do not qualify for, leading to financial losses and potential legal disputes.

Overtime calculation errors are another area of concern, particularly in industries where overtime is common. These errors can occur due to misclassification of overtime hours, incorrect overtime rates, or failure to account for overtime hours worked. This can lead to underpayment of employees for their overtime work, resulting in financial losses and potential legal action.

To mitigate these risks, employers should implement robust payroll systems with built-in error checking and validation processes. Regular audits and reviews of payroll calculations can also help identify and correct errors before they become major issues. Additionally, employers should ensure that their payroll staff are well-trained and knowledgeable about payroll laws and regulations to minimize the likelihood of calculation errors.

Efficient Timekeeping and Payroll Management with Sage: A Comprehensive Guide

You may want to see also

Explore related products

![Discrimination Laws and Advanced Legal Research for Employees II [The Rite Aid Papers]: How to Prepare, File a Lawsuit, and Win Against Your Employer in California](https://m.media-amazon.com/images/I/71uJOaRYPhL._AC_UY218_.jpg)

![]()

Consequences of Errors: Errors can result in financial losses, penalties, interest, and damage to the employer's reputation

Errors in payroll calculations can have far-reaching consequences for employers. Financial losses are often the most immediate and tangible impact, as incorrect payments can lead to over or underpayment of employees. This can result in the need for costly adjustments and potential legal action to recover lost funds. Additionally, errors can lead to penalties and interest charges from tax authorities if payroll taxes are not calculated and remitted correctly. These financial repercussions can be significant and may require substantial resources to rectify.

Beyond the financial implications, errors in payroll calculations can also damage an employer's reputation. Employees rely on accurate and timely payment for their work, and consistent errors can erode trust and morale within the workforce. This can lead to increased turnover, difficulty in attracting new talent, and a negative impact on overall productivity. Furthermore, word of an employer's payroll issues can spread quickly, potentially affecting business relationships and the company's standing in the community.

Employers must also consider the legal ramifications of payroll errors. In some cases, employees may be entitled to compensation for damages resulting from incorrect payments, such as overdraft fees or late payment penalties. This can lead to costly legal battles and settlements, further exacerbating the financial impact of the errors. Additionally, employers may face regulatory scrutiny and potential fines if payroll errors are found to be in violation of labor laws or tax regulations.

To mitigate these risks, employers should implement robust payroll processes and controls. This includes regular audits and reviews of payroll calculations, training for payroll staff, and the use of reliable payroll software. Employers should also have clear communication channels with employees to address any concerns or issues related to payroll promptly. By taking proactive steps to prevent and address payroll errors, employers can minimize the potential consequences and maintain a positive reputation and financial stability.

Understanding Your Rights: Can an Employer Skip Your Payroll?

You may want to see also

Explore related products

](https://m.media-amazon.com/images/I/81N+sq+EvBL._AC_UY218_.jpg)

![]()

Defenses Against Lawsuit: Employees might argue lack of training, system failures, or reasonable mistakes as defenses

Employees facing lawsuits for payroll calculation errors have several potential defenses at their disposal. One common defense is the lack of adequate training. If an employee can demonstrate that they were not properly trained in the payroll process or the use of specific software, they may argue that the employer is partially or fully responsible for the errors. This defense can be particularly effective if the employee can show that they repeatedly requested additional training or support, which was denied.

Another defense is system failures. If the payroll errors were caused by a malfunction in the payroll system or software, the employee may argue that they are not liable for the mistakes. This defense can be strengthened if the employee can provide evidence of previous system issues or complaints from other employees about the reliability of the payroll system.

Reasonable mistakes can also serve as a defense. If the employee can show that the errors were made in good faith and were not the result of negligence or intentional misconduct, they may be able to avoid liability. This defense can be more challenging to prove, as it requires the employee to demonstrate that they exercised reasonable care and diligence in performing their duties.

In addition to these defenses, employees may also argue that the employer's policies or procedures were unclear or inadequate, leading to the errors. If the employee can show that the employer's guidelines were ambiguous or contradictory, they may be able to shift some of the blame for the errors onto the employer.

Ultimately, the success of these defenses will depend on the specific facts of the case and the ability of the employee to present compelling evidence. Employees facing lawsuits for payroll calculation errors should consult with an attorney to discuss their potential defenses and develop a strategy for responding to the lawsuit.

Navigating Payroll Without a W-4: What Employers Need to Know

You may want to see also

Explore related products

![]()

Preventive Measures: Implementing robust payroll systems, regular audits, and employee training can mitigate calculation errors

Implementing robust payroll systems is a critical preventive measure against calculation errors. This involves investing in reliable software that automates payroll calculations, reducing the risk of human error. Such systems should have built-in checks and balances, like automatic alerts for discrepancies or unusual entries, to catch potential mistakes before they result in incorrect payments. Regular updates and maintenance of these systems are also essential to ensure they remain accurate and compliant with changing tax laws and regulations.

Regular audits are another key strategy in preventing payroll calculation errors. These audits should be conducted by an independent party to ensure objectivity and thoroughness. Auditors should review payroll records, check for consistency in payment amounts, verify that deductions and contributions are correctly calculated, and confirm that all payments are authorized and documented. Audits can help identify patterns of errors or even fraudulent activities, allowing employers to take corrective action before significant financial losses occur.

Employee training is equally important in mitigating payroll calculation errors. Payroll staff should receive comprehensive training on payroll laws, regulations, and procedures. This includes understanding tax withholding requirements, overtime calculations, and the intricacies of different pay structures. Ongoing training is crucial to keep staff updated on any changes in payroll legislation or company policies. Employers should also encourage a culture of continuous learning and improvement, where employees feel comfortable asking questions and seeking clarification when they encounter complex or unfamiliar payroll issues.

In addition to these measures, employers can implement internal controls to further reduce the risk of payroll errors. This might include segregating payroll duties among different employees to prevent conflicts of interest, requiring dual authorization for payroll disbursements, and regularly reconciling payroll accounts with bank statements. Employers should also establish clear policies and procedures for handling payroll errors, including prompt notification of affected employees and timely correction of any discrepancies.

By taking these preventive measures, employers can significantly reduce the likelihood of payroll calculation errors and the potential legal and financial consequences that may follow. It is important to remember that while these measures can mitigate risks, they do not eliminate them entirely. Employers should remain vigilant and proactive in their payroll management practices to ensure ongoing accuracy and compliance.

Exploring the Legality of Mandatory Voluntary Payroll Deductions

You may want to see also

Frequently asked questions

Yes, an employer can sue a payroll employee for calculation errors if the errors result in financial losses or other damages to the employer.

Common reasons for payroll calculation errors include incorrect data entry, misinterpretation of payroll laws and regulations, and software or system malfunctions.

Employers can prevent payroll calculation errors by implementing robust payroll systems, providing thorough training to payroll staff, regularly auditing payroll processes, and staying up-to-date with payroll laws and regulations.

The potential consequences for a payroll employee sued for calculation errors can include financial penalties, damage to their professional reputation, and possible termination of employment.