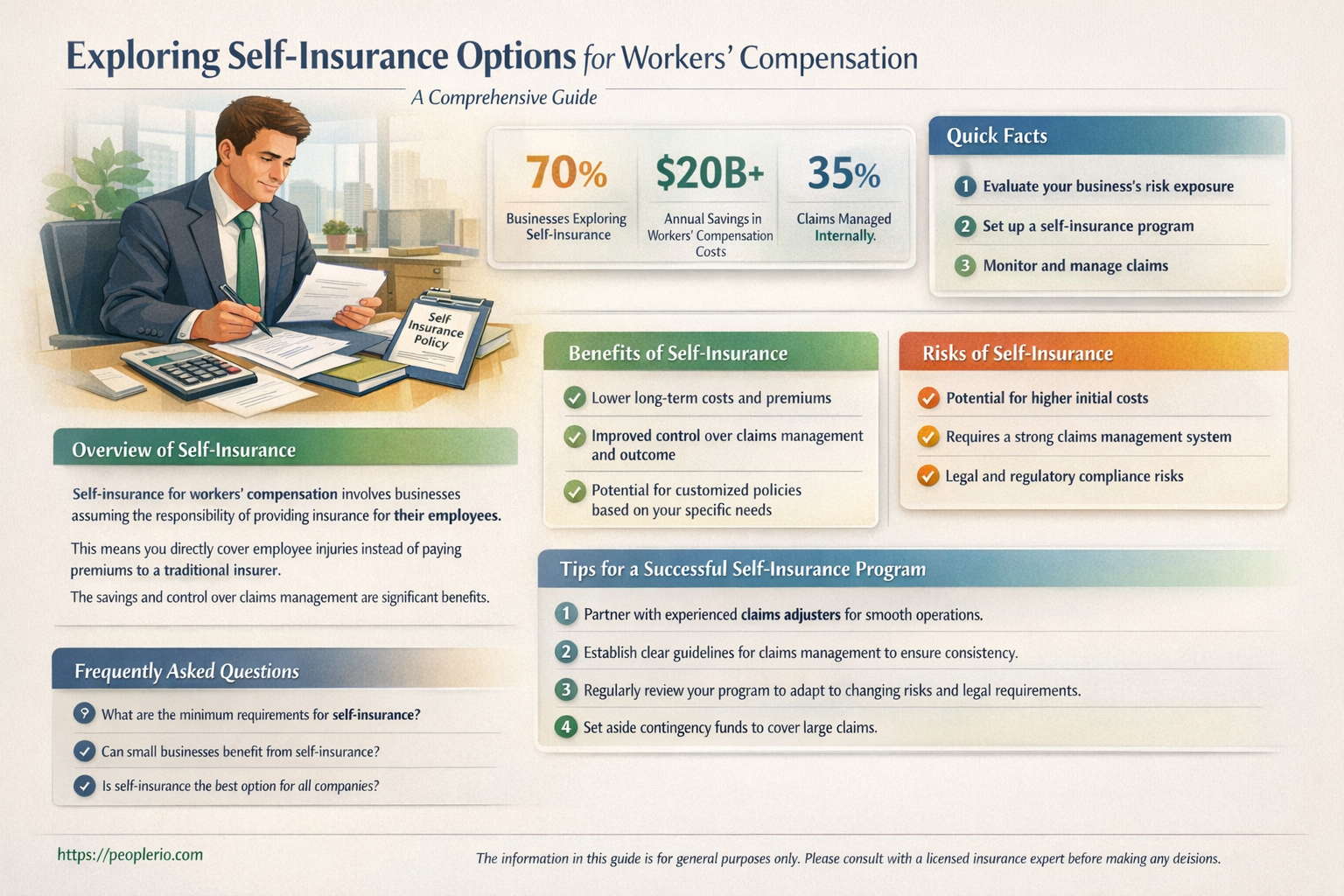

Self-insurance for workers' compensation is a viable option for some businesses, allowing them to manage their own risk and potentially reduce costs. However, it requires careful consideration and a thorough understanding of the legal and financial implications. In this paragraph, we will explore the concept of self-insurance in the context of workers' compensation, discussing its benefits and drawbacks, as well as the key factors that businesses should consider when deciding whether to self-insure. We will also provide an overview of the regulatory requirements and best practices for implementing a successful self-insurance program. By the end of this paragraph, readers will have a clear understanding of the complexities involved in self-insuring for workers' compensation and be better equipped to make an informed decision about whether it is the right choice for their organization.

| Characteristics | Values |

|---|---|

| Self-insurance | Possible but requires careful consideration |

| Workers' compensation | Mandatory for employers in most states |

| Financial stability | Employer must have sufficient funds to cover claims |

| Risk management | Employer assumes full risk of employee injuries |

| Legal compliance | Must comply with state workers' compensation laws |

| Claim handling | Employer is responsible for managing and paying claims |

| Premiums | No premiums paid to an insurance company |

| Coverage | Typically covers medical expenses and lost wages |

| Employee protection | Ensures employees are protected in case of work-related injuries |

| Business continuity | Helps maintain business operations during claims |

Explore related products

What You'll Learn

- Eligibility for Self-Insurance: Requirements and qualifications for employers to self-insure workers' compensation claims

- Financial Responsibilities: Employer's financial obligations, including setting aside funds to cover potential claims and medical expenses

- Risk Management: Strategies for managing workplace risks and preventing accidents to minimize workers' compensation claims

- Legal Compliance: Ensuring adherence to state laws and regulations regarding workers' compensation self-insurance

- Claim Handling: Procedures for handling and processing workers' compensation claims when self-insured

![]()

Eligibility for Self-Insurance: Requirements and qualifications for employers to self-insure workers' compensation claims

To be eligible for self-insurance in regards to workers' compensation, employers must meet certain requirements and qualifications. These vary by jurisdiction, but generally include having a minimum number of employees, a stable financial history, and a demonstrated ability to manage risk effectively. Employers must also be able to show that they have the resources and expertise necessary to handle workers' compensation claims in-house, including the ability to investigate claims, negotiate settlements, and manage medical care for injured employees.

One of the key requirements for self-insurance is having a sufficient number of employees. This is because self-insurance relies on the principle of risk pooling, where the employer assumes the risk of workers' compensation claims in exchange for paying a lower premium. With a larger workforce, the employer is able to spread the risk of claims across a greater number of employees, reducing the likelihood of any one claim having a significant financial impact.

In addition to having a sufficient number of employees, employers must also demonstrate financial stability in order to be eligible for self-insurance. This typically involves showing a history of profitable operations, as well as having adequate reserves and capital to cover potential claims. Employers may also need to provide evidence of their ability to manage risk effectively, such as through the implementation of safety programs and loss prevention measures.

Another important qualification for self-insurance is having the necessary resources and expertise to manage workers' compensation claims. This includes having trained personnel to investigate claims, negotiate settlements, and manage medical care for injured employees. Employers may also need to demonstrate that they have access to a network of medical providers and other resources necessary to provide quality care to injured employees.

Overall, the requirements and qualifications for self-insurance in regards to workers' compensation are designed to ensure that employers have the necessary resources, expertise, and financial stability to effectively manage workers' compensation claims in-house. By meeting these requirements, employers can potentially save money on workers' compensation premiums while also maintaining control over the claims process.

Unraveling the Confusion: State Unemployment Insurance vs. Unemployment Compensation

You may want to see also

Explore related products

![]()

Financial Responsibilities: Employer's financial obligations, including setting aside funds to cover potential claims and medical expenses

Employers who opt for self-insurance in regards to workers' compensation must be acutely aware of their financial responsibilities. This includes setting aside sufficient funds to cover potential claims and medical expenses that may arise from workplace injuries or illnesses. The amount an employer needs to allocate can vary widely depending on factors such as the industry, the number of employees, and the historical claims experience of the company. Employers must conduct a thorough risk assessment to determine an appropriate reserve amount.

One of the key financial obligations of self-insured employers is to establish a reserve fund. This fund acts as a financial cushion to pay for workers' compensation claims as they are incurred. Employers must ensure that the reserve is adequately funded to avoid financial instability in the event of a large claim or a series of claims. Additionally, employers may need to purchase excess insurance to cover claims that exceed the reserve fund. This excess insurance acts as a safety net, protecting the employer from catastrophic financial losses.

Employers must also consider the administrative costs associated with self-insurance. This includes the cost of claims processing, medical bill review, and legal fees. Employers may need to hire additional staff or outsource these functions to a third-party administrator. Furthermore, employers must stay abreast of changes in workers' compensation laws and regulations, which can impact their financial obligations.

Another important aspect of financial responsibility is the management of cash flow. Employers must ensure that they have sufficient liquidity to pay claims as they come due. This may involve setting up a separate bank account for the reserve fund or investing the funds in low-risk, liquid assets. Employers should also have a plan in place for handling large, unexpected claims that could strain their cash reserves.

In conclusion, self-insured employers bear significant financial responsibilities in regards to workers' compensation. They must carefully manage their reserve funds, consider excess insurance, account for administrative costs, and maintain sufficient liquidity to meet their obligations. By doing so, employers can mitigate the financial risks associated with self-insurance and provide a stable source of compensation for injured or ill employees.

Understanding Workers' Compensation Insurance Requirements for Employers

You may want to see also

Explore related products

![]()

Risk Management: Strategies for managing workplace risks and preventing accidents to minimize workers' compensation claims

Implementing effective risk management strategies is crucial for any organization aiming to reduce workplace accidents and minimize workers' compensation claims. One approach is to conduct regular safety audits to identify potential hazards and assess the likelihood and impact of accidents. This proactive measure allows companies to address risks before they result in injuries or fatalities. For instance, a manufacturing plant could identify the risk of machinery malfunctions and take preventive steps such as regular maintenance and employee training to mitigate this risk.

Another strategy is to promote a culture of safety within the workplace. This involves encouraging employees to report hazards and near misses, as well as fostering an environment where safety is prioritized over productivity. Companies can achieve this by incorporating safety into their core values, providing ongoing training, and recognizing and rewarding safe behaviors. A construction company, for example, could implement a safety incentive program that rewards workers for identifying and reporting potential hazards, thereby reducing the likelihood of accidents.

In addition to these strategies, organizations should also focus on ergonomics to prevent work-related injuries. This includes designing workstations and tasks to minimize physical strain, providing proper equipment and tools, and ensuring that employees are trained in safe lifting and handling techniques. A healthcare facility could reduce the risk of musculoskeletal injuries among its staff by investing in ergonomic equipment such as adjustable beds and patient lifts.

Furthermore, companies should consider implementing a return-to-work program for employees who have experienced work-related injuries. This program should focus on gradually reintegrating injured workers into their roles, providing necessary accommodations, and ensuring that they receive appropriate medical care and support. By doing so, organizations can reduce the duration and severity of workers' compensation claims, as well as foster a sense of loyalty and commitment among their employees.

Lastly, it is essential for companies to stay informed about changes in workers' compensation laws and regulations. This includes understanding the requirements for self-insurance, if applicable, and ensuring that their risk management strategies align with legal and regulatory standards. By staying up-to-date and compliant, organizations can avoid costly penalties and legal disputes, while also maintaining a safe and healthy work environment for their employees.

Exploring Workers' Compensation Insurance for Single-Member Corporations

You may want to see also

Explore related products

![]()

Legal Compliance: Ensuring adherence to state laws and regulations regarding workers' compensation self-insurance

Ensuring legal compliance when self-insuring for workers' compensation is a complex but crucial task. Each state has its own set of laws and regulations that govern self-insurance programs, and failure to adhere to these can result in significant legal and financial repercussions. To navigate this landscape effectively, it's essential to have a thorough understanding of the specific requirements in your state.

One of the first steps in ensuring legal compliance is to familiarize yourself with the state's workers' compensation laws. This includes understanding the eligibility criteria for self-insurance, the necessary documentation and filings, and the ongoing reporting requirements. Many states require self-insured employers to obtain a certificate of self-insurance, which involves demonstrating financial stability and the ability to pay claims.

Another key aspect of legal compliance is maintaining adequate financial reserves. Self-insured employers must have sufficient funds set aside to cover potential claims, as well as to pay for ongoing administrative costs and legal expenses. This often involves working with a third-party administrator (TPA) who can help manage the program and ensure that claims are handled efficiently and fairly.

In addition to financial considerations, self-insured employers must also comply with state regulations regarding claims handling and dispute resolution. This includes adhering to specific timelines for reporting and investigating claims, as well as following established procedures for resolving disputes with employees. Failure to comply with these regulations can lead to penalties, fines, and even the revocation of self-insurance status.

To mitigate these risks, many self-insured employers choose to work with legal counsel who specializes in workers' compensation law. These attorneys can provide valuable guidance on compliance issues, help develop effective claims handling procedures, and represent the employer in legal proceedings if necessary.

Ultimately, ensuring legal compliance when self-insuring for workers' compensation requires a proactive and ongoing commitment. By staying informed about state laws and regulations, maintaining adequate financial reserves, and working with experienced professionals, self-insured employers can minimize their legal risks and create a more effective and efficient workers' compensation program.

Understanding Workers' Compensation Insurance Costs: A Comprehensive Guide

You may want to see also

![]()

Claim Handling: Procedures for handling and processing workers' compensation claims when self-insured

When handling workers' compensation claims as a self-insured entity, it's crucial to establish a clear and efficient claims processing procedure. This begins with the immediate reporting of the claim by the employee to the employer. Employers should then promptly notify their third-party administrator (TPA) or claims adjuster, who will guide the claim through the necessary steps.

The next phase involves a thorough investigation of the claim. This includes gathering all relevant documentation, such as medical reports, witness statements, and any other evidence that can substantiate the claim. The adjuster will also conduct interviews with the employee, employer, and any witnesses to gain a comprehensive understanding of the incident.

Once the investigation is complete, the adjuster will make a determination on the compensability of the claim. If the claim is deemed compensable, the adjuster will then calculate the appropriate benefits, which may include medical expenses, lost wages, and any other applicable costs. The self-insured employer will then be responsible for paying these benefits directly to the employee.

Throughout the claims handling process, it's essential for self-insured employers to maintain open lines of communication with their employees. This can help to ensure that the employee feels supported and informed, which can ultimately lead to a smoother claims process and a more positive outcome for all parties involved.

In addition to these procedural steps, self-insured employers should also be aware of the potential risks and challenges associated with claims handling. For example, there is always the risk of fraudulent claims, which can be mitigated through thorough investigation and verification processes. Employers should also be prepared for the possibility of disputes or appeals, which may require additional resources and expertise to resolve.

Overall, effective claims handling is a critical component of self-insurance for workers' compensation. By establishing clear procedures, maintaining open communication, and being aware of potential risks, self-insured employers can ensure that claims are processed efficiently and fairly, which can ultimately lead to cost savings and improved employee satisfaction.

Understanding Workers' Compensation Insurance Requirements for Businesses

You may want to see also

Frequently asked questions

Yes, some businesses choose to be self-insured for workers' compensation, meaning they pay for each out-of-pocket claim as they are incurred instead of purchasing insurance.

Benefits of being self-insured include potentially lower costs if you have a low number of claims, more control over the claims process, and the ability to invest the money you would have spent on premiums.

Risks include the potential for large, unexpected claims that could significantly impact your business's finances, the administrative burden of managing claims, and the need to comply with state regulations.

To determine if being self-insured is right for your business, consider factors such as your company's financial stability, the number and severity of workers' compensation claims you've had in the past, your risk tolerance, and your ability to manage the administrative aspects of claims.