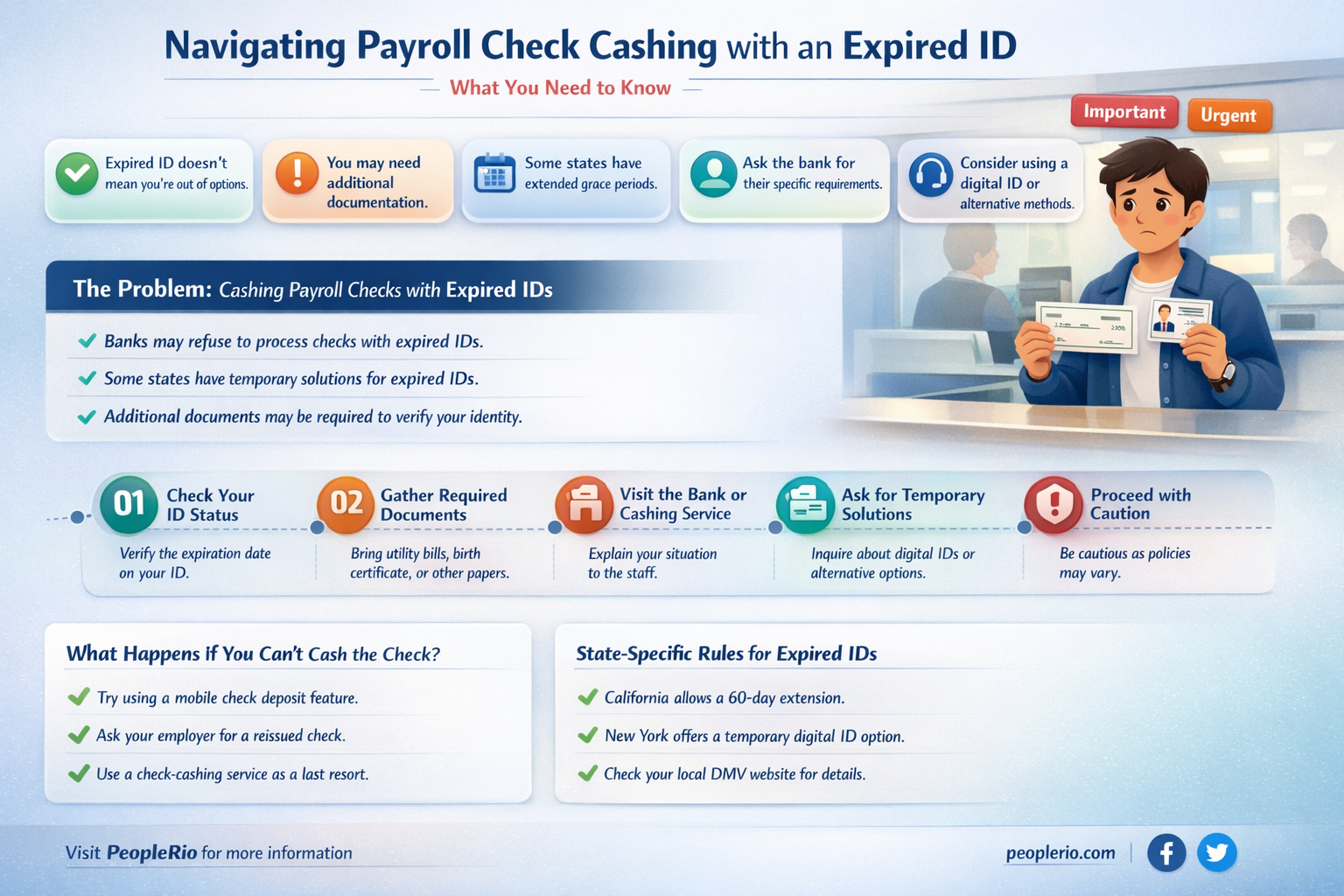

If you're wondering whether you can cash a payroll check with an expired ID, the answer is not straightforward. It largely depends on the policies of the bank or financial institution where you're attempting to cash the check. Some banks may allow you to cash a check with an expired ID if they recognize you as a regular customer and are confident in your identity. However, many banks have strict policies requiring a valid, unexpired ID to cash checks in order to prevent fraud and comply with financial regulations. It's always best to check with your bank's specific policies or visit a branch in person to discuss your situation. Additionally, consider updating your ID as soon as possible to avoid any future complications with financial transactions.

| Characteristics | Values |

|---|---|

| Topic | Cashing a payroll check with an expired ID |

| Importance | High for individuals without valid identification |

| Requirements | Payroll check, Expired ID |

| Potential Issues | Bank policies, Identification verification |

| Alternatives | Using a co-signer, Providing additional documentation |

| Legal Considerations | Varies by jurisdiction, Potential for fraud |

| Financial Institutions | Banks, Credit unions, Check cashing services |

| Success Factors | Employer verification, Check validity, Account status |

Explore related products

What You'll Learn

- Types of ID Accepted: Different states and banks have varying policies on the types of identification accepted for cashing checks

- Grace Periods: Some banks offer a grace period after an ID expires, allowing customers to cash checks within a certain timeframe

- Alternative Options: If an ID is expired, there may be alternative methods to verify identity, such as using a passport or military ID

- State-Specific Laws: State laws often dictate the requirements for cashing checks, including the validity period of identification documents

- Bank Discretion: Ultimately, banks have the discretion to decide whether to cash a check with an expired ID based on their internal policies and risk assessment

![]()

Types of ID Accepted: Different states and banks have varying policies on the types of identification accepted for cashing checks

In the United States, the types of identification accepted for cashing checks can vary significantly from state to state and bank to bank. While some states may accept a wide range of IDs, others may have more stringent requirements. For example, some states may accept a driver's license, state ID, or passport as valid forms of identification, while others may also accept military IDs, tribal IDs, or even student IDs. It's important to note that some states may have specific requirements for the ID, such as it being current and unexpired, or that it must be issued by a certain authority.

Banks also have their own policies regarding the types of identification accepted for cashing checks. Some banks may accept a wider range of IDs than others, and some may have specific requirements for the ID, such as it being current and unexpired, or that it must be issued by a certain authority. Additionally, some banks may have different policies for cashing checks for customers versus non-customers. For example, a bank may accept a wider range of IDs for customers who have an established relationship with the bank, but may have more stringent requirements for non-customers.

When it comes to cashing a payroll check with an expired ID, it's important to check with the specific state and bank to see what their policies are. Some states and banks may accept an expired ID as long as it is within a certain timeframe, while others may not accept it at all. Additionally, some banks may have different policies for cashing payroll checks versus other types of checks. For example, a bank may accept an expired ID for cashing a payroll check, but may not accept it for cashing a personal check.

If you are unable to cash a payroll check with an expired ID, there are other options available. For example, you may be able to cash the check at a check cashing store or a payday loan store. However, it's important to note that these options may come with high fees and interest rates. Another option may be to ask your employer to reissue the check with a longer expiration date.

In conclusion, the types of identification accepted for cashing checks can vary significantly from state to state and bank to bank. It's important to check with the specific state and bank to see what their policies are when it comes to cashing a payroll check with an expired ID. If you are unable to cash the check with an expired ID, there are other options available, but it's important to be aware of the potential fees and interest rates associated with these options.

Cashing Payroll Checks at Wells Fargo: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Grace Periods: Some banks offer a grace period after an ID expires, allowing customers to cash checks within a certain timeframe

In the realm of banking and financial transactions, the concept of a grace period holds significant importance, particularly when it comes to cashing checks with an expired ID. A grace period is a timeframe during which a bank allows customers to cash checks even after their identification has expired. This practice is not universal and varies widely among different banks and financial institutions. Some banks may offer a grace period of a few days, while others might extend it to several weeks or even months. The duration of this period is typically determined by the bank's internal policies and may be influenced by factors such as the customer's history with the bank, the type of check being cashed, and the bank's risk assessment procedures.

The grace period serves as a buffer for customers who may have difficulty renewing their IDs immediately. It provides a window of opportunity for individuals to cash their checks without facing the inconvenience of having to wait for a new ID to be issued. This can be particularly beneficial for those who rely heavily on check payments for their daily expenses or payroll. However, it is crucial for customers to be aware of their bank's specific policies regarding grace periods, as failing to cash checks within the stipulated timeframe may result in the checks being returned or declined.

Banks that offer grace periods often have stringent verification processes in place to ensure the legitimacy of the checks being cashed. They may require additional documentation or verification steps to confirm the customer's identity and the validity of the check. This could include requesting a secondary form of identification, such as a utility bill or a lease agreement, or using electronic verification methods to cross-check the customer's details against various databases.

It is also worth noting that the grace period does not absolve customers of the responsibility to renew their IDs. It merely provides a temporary solution to avoid immediate financial disruptions. Customers should make it a priority to renew their IDs as soon as possible to ensure uninterrupted access to their banking services. Failure to do so may not only result in difficulties cashing checks but could also lead to other complications, such as issues with account access or the inability to perform certain transactions.

In conclusion, the grace period is a valuable feature offered by some banks to accommodate customers with expired IDs. It allows for a smooth transition and helps avoid financial inconveniences. However, customers must be proactive in renewing their IDs and should familiarize themselves with their bank's policies and procedures regarding grace periods to make the most of this temporary reprieve.

Understanding Arizona Payroll Check Fees: Employer's Guide

You may want to see also

Explore related products

![]()

Alternative Options: If an ID is expired, there may be alternative methods to verify identity, such as using a passport or military ID

In the event that your ID has expired and you need to cash a payroll check, it's crucial to know that there are alternative methods available to verify your identity. One such option is to use a passport, which is a widely accepted form of identification in many countries. To proceed with this method, you would need to present your passport along with your payroll check to the bank or financial institution where you intend to cash it. It's important to note that the passport must be valid and not expired, as this could lead to further complications.

Another alternative method to verify your identity is by using a military ID. This option is particularly useful for individuals who are currently serving or have served in the armed forces. Military IDs are typically valid for a longer period than regular IDs, and they are recognized by most financial institutions. To use this method, you would need to present your military ID along with your payroll check to the bank or financial institution.

It's also worth considering other forms of identification that may be accepted by the bank or financial institution. For example, some institutions may accept a combination of a birth certificate and a social security card as proof of identity. However, it's important to check with the specific institution beforehand to determine which forms of identification they accept.

In addition to these alternative methods, it's also important to be aware of any potential risks or challenges associated with using an expired ID. For instance, some financial institutions may have strict policies against accepting expired IDs, and this could lead to delays or even denial of service. Furthermore, using an expired ID could potentially expose you to identity theft or fraud, as it may be easier for someone to forge or manipulate an expired ID.

To mitigate these risks, it's advisable to renew your ID as soon as possible. This will not only ensure that you have a valid form of identification, but it will also provide you with greater peace of mind knowing that your personal information is secure. In the meantime, exploring alternative methods of verification, such as using a passport or military ID, can help you to cash your payroll check without any unnecessary delays or complications.

Free Payroll Check Creation: A Step-by-Step Guide for Small Businesses

You may want to see also

Explore related products

![]()

State-Specific Laws: State laws often dictate the requirements for cashing checks, including the validity period of identification documents

State laws play a crucial role in determining the requirements for cashing checks, including the validity period of identification documents. While federal law sets some overarching guidelines, individual states have the authority to enact their own regulations, which can vary significantly. For instance, some states may allow the cashing of checks with expired IDs under certain conditions, while others may have strict policies against it.

One of the key aspects of state-specific laws is the definition of what constitutes a valid form of identification. Some states may accept a wider range of documents, such as utility bills or lease agreements, in addition to traditional forms of ID like driver's licenses and passports. Others may have more stringent requirements, mandating that only government-issued IDs with specific features, such as a photograph or a holographic seal, are acceptable.

Another important consideration is the grace period that some states may offer for expired IDs. In certain jurisdictions, individuals may be allowed to cash checks with an ID that has expired within a certain timeframe, such as 30 or 60 days. This grace period can provide a buffer for individuals who are in the process of renewing their ID but have not yet received the new document.

Furthermore, state laws may also dictate the procedures that financial institutions must follow when verifying the identity of check cashers. Some states may require banks to use specific databases or verification methods to ensure that the ID presented is genuine and up-to-date. Others may allow for more discretion on the part of the bank, relying on the judgment of the teller or other bank employee to determine the validity of the ID.

In conclusion, understanding state-specific laws is essential for individuals who need to cash checks, especially if their ID is expired. By familiarizing themselves with the regulations in their state, individuals can avoid potential issues and ensure a smooth check cashing process.

Understanding Payroll Checks: Are Deductions Mandatory?

You may want to see also

Explore related products

![]()

Bank Discretion: Ultimately, banks have the discretion to decide whether to cash a check with an expired ID based on their internal policies and risk assessment

Banks are not legally obligated to cash checks presented with expired identification. Their decision is guided by internal policies designed to mitigate risk and ensure compliance with regulatory requirements. These policies can vary widely between institutions, influenced by factors such as the bank's size, customer base, and risk tolerance. For instance, a large national bank may have more stringent policies compared to a local credit union.

When assessing the risk associated with cashing a check with an expired ID, banks consider several factors. They may evaluate the customer's history with the bank, the frequency of such requests, and the overall transaction amount. Banks might also use additional verification methods, such as cross-referencing the check details with the account holder's information or utilizing third-party verification services.

In practice, this discretion means that customers may experience different outcomes when attempting to cash a check with an expired ID at different banks or even at different branches of the same bank. Some banks may be more lenient, especially for long-standing customers or for checks drawn from accounts with a history of regular, legitimate transactions. Others may adopt a zero-tolerance policy, refusing to cash any check presented with an expired ID.

To navigate this variability, individuals should familiarize themselves with their bank's specific policies regarding expired identification. This can typically be done by reviewing the bank's website, contacting customer service, or visiting a branch in person. Understanding these policies can help customers avoid potential inconveniences and ensure a smoother banking experience.

Ultimately, the key takeaway is that while banks have the authority to cash checks with expired IDs, they are not required to do so. Their discretion is a critical aspect of maintaining financial security and regulatory compliance, and it underscores the importance of customers staying informed about their bank's policies and procedures.

Understanding Your Payroll Check: A Detailed Look at Its Components

You may want to see also

Frequently asked questions

Generally, banks require a valid, unexpired ID to cash a check. An expired ID may not be accepted as it does not provide current verification of your identity.

Commonly accepted IDs for cashing a payroll check include a driver's license, state ID card, passport, or military ID. These must be current and unexpired.

Some banks may have specific policies or exceptions, such as allowing the use of an expired ID within a certain time frame after expiration. Alternatively, you might consider using an online check cashing service that may have different verification methods. However, it's best to check with your bank or the check issuer for their specific requirements and options.